Health insurance is a critical component of financial and personal well-being, providing individuals and families with protection against the high costs of medical care. AM Health Insurance likely refers to a specific provider or plan offering coverage for various healthcare services, including doctor visits, hospital stays, prescription medications, and preventive care. Understanding the details of such a policy—such as premiums, deductibles, copayments, and network restrictions—is essential for maximizing its benefits. With rising healthcare expenses, having reliable health insurance ensures access to necessary treatments while minimizing out-of-pocket expenses, making it a vital investment for long-term health and financial security.

Explore related products

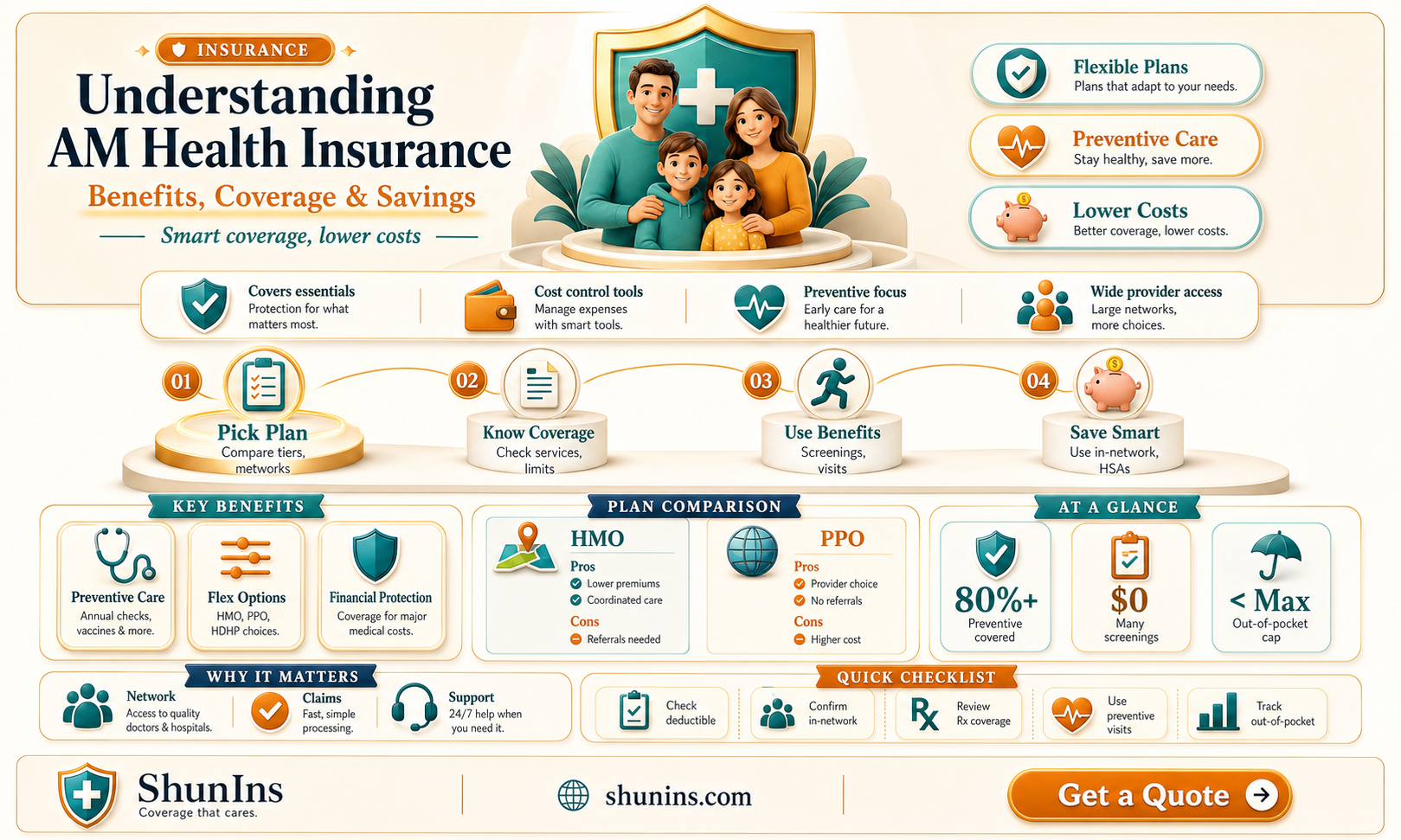

What You'll Learn

- Coverage Options: Types of plans, benefits, exclusions, and add-ons available for individuals and families

- Premiums & Costs: Monthly payments, deductibles, copays, and out-of-pocket expenses explained

- Provider Networks: In-network vs. out-of-network care, and finding preferred providers

- Enrollment Periods: Open enrollment, special enrollment, and how to apply for coverage

- Claims & Appeals: Filing claims, understanding denials, and the appeals process for disputes

![]()

Coverage Options: Types of plans, benefits, exclusions, and add-ons available for individuals and families

Health insurance plans are not one-size-fits-all. Individuals and families must navigate a complex landscape of options, each with unique benefits, exclusions, and add-ons. Understanding these differences is crucial to selecting a plan that aligns with specific health needs and financial constraints. For instance, a young professional might prioritize lower premiums and basic coverage, while a family with children may seek comprehensive benefits including pediatric care and vaccinations.

Analyzing Plan Types:

Health insurance plans typically fall into categories like Health Maintenance Organization (HMO), Preferred Provider Organization (PPO), Exclusive Provider Organization (EPO), and High-Deductible Health Plan (HDHP). HMOs offer lower costs but require in-network providers and referrals for specialists, making them ideal for those who value cost-efficiency and don’t mind limited flexibility. PPOs, on the other hand, allow out-of-network care at higher costs, suitable for individuals seeking broader provider access. EPOs combine HMO and PPO features, offering lower premiums without requiring referrals but restricting out-of-network care. HDHPs pair with Health Savings Accounts (HSAs), appealing to those who want to save on taxes while managing higher out-of-pocket costs.

Benefits and Exclusions:

Most plans cover essential health benefits like emergency services, maternity care, and prescription drugs, but the extent varies. For example, some plans may cover 80% of prescription costs after a deductible, while others might exclude certain high-cost medications. Exclusions often include cosmetic procedures, experimental treatments, and specific pre-existing conditions during waiting periods. Families should scrutinize these details, especially if they have chronic illnesses or anticipate significant medical expenses. For instance, a plan with robust maternity benefits is essential for expecting parents, while one with extensive mental health coverage is critical for those with ongoing therapy needs.

Add-Ons to Enhance Coverage:

Add-ons like dental, vision, and disability insurance can fill gaps in standard plans. Dental coverage, for example, often includes 100% coverage for preventive care (cleanings, X-rays) and partial coverage for major procedures (crowns, root canals). Vision plans typically cover annual eye exams and provide allowances for glasses or contacts. Critical illness insurance offers lump-sum payouts for conditions like cancer or heart attack, providing financial relief during recovery. Families with children might consider add-ons like accident insurance, which covers costs associated with injuries from falls or sports.

Practical Tips for Selection:

Start by assessing your health needs and budget. For instance, a family with a history of diabetes should prioritize plans with robust prescription drug coverage. Compare out-of-pocket maximums, which cap annual expenses, and consider whether an HSA-eligible HDHP aligns with your financial strategy. Use online tools to estimate costs based on expected medical usage. For example, if you anticipate frequent doctor visits, a plan with lower copays might be more cost-effective than one with a lower premium but higher visit fees. Finally, review customer satisfaction ratings and provider networks to ensure accessibility and quality care.

By carefully evaluating plan types, understanding benefits and exclusions, and strategically adding optional coverages, individuals and families can tailor their health insurance to meet their unique needs. This proactive approach ensures financial protection and peace of mind in the face of unpredictable health challenges.

Discover the Most Affordable Motorcycle Insurance Providers Today

You may want to see also

Explore related products

![]()

Premiums & Costs: Monthly payments, deductibles, copays, and out-of-pocket expenses explained

Understanding the financial mechanics of health insurance is crucial for making informed decisions. Premiums, the monthly payments you make to maintain coverage, are just the tip of the iceberg. They vary widely based on factors like age, location, plan type, and provider. For instance, a 30-year-old in Texas might pay $300 monthly for a mid-tier plan, while a 55-year-old in New York could face $700 or more. These costs are not arbitrary; they reflect actuarial calculations of risk and expected healthcare utilization. To optimize your spending, compare premiums across providers and consider whether a higher monthly cost might save you money in the long run if it comes with better coverage.

Deductibles are the next critical piece of the puzzle. This is the amount you must pay out of pocket before your insurance kicks in for most services. Plans with lower premiums often have higher deductibles—sometimes as much as $6,000 annually for an individual. Conversely, higher-premium plans might offer deductibles as low as $500. For example, if you’re generally healthy and rarely visit the doctor, a high-deductible plan paired with a Health Savings Account (HSA) could be cost-effective. However, if you have chronic conditions requiring frequent care, a lower deductible plan may be more economical despite the higher monthly cost.

Copays and coinsurance further complicate the cost structure but are essential to understand. A copay is a fixed amount you pay for a specific service, like $25 for a doctor’s visit or $10 for a generic prescription. Coinsurance, on the other hand, is a percentage of the cost you share with your insurer after meeting your deductible. For instance, if your plan has 20% coinsurance for hospital stays, you’ll pay one-fifth of the bill. These costs can add up quickly, especially for high-ticket items like surgeries or imaging tests. Pro tip: Always ask for an estimate of out-of-pocket costs before scheduling non-emergency procedures.

Out-of-pocket maximums are your financial safety net. This is the most you’ll spend in a year on deductibles, copays, and coinsurance before your insurance covers 100% of costs. For 2023, the maximum for individual plans is $8,700, though some plans cap at lower amounts. This limit does not include premiums, which can total $10,000 or more annually for comprehensive coverage. Families should note that their out-of-pocket maximum is typically double the individual amount. Understanding this cap helps you budget for worst-case scenarios and ensures you’re not blindsided by unexpected expenses.

Finally, consider the trade-offs between cost and coverage. While it’s tempting to choose the cheapest plan, skimping on coverage can lead to financial strain if you need significant care. For example, a plan with a $1,000 deductible and $30 copays might save you $200 monthly in premiums compared to a plan with a $500 deductible and $15 copays. However, if you require multiple specialist visits or prescriptions, the latter plan could save you thousands in the long run. Evaluate your health needs, financial stability, and risk tolerance to strike the right balance.

Capital One Cardholders: Travel Insurance Benefits and Exclusions

You may want to see also

Explore related products

![]()

Provider Networks: In-network vs. out-of-network care, and finding preferred providers

Health insurance plans often hinge on provider networks, a critical yet confusing aspect for many policyholders. In-network providers have agreements with your insurer, offering services at pre-negotiated rates, which typically result in lower out-of-pocket costs for you. Out-of-network providers, on the other hand, haven’t agreed to these terms, often leading to higher costs and sometimes requiring you to pay the difference between the provider’s charge and what the insurer covers. Understanding this distinction is the first step in maximizing your insurance benefits.

Consider a scenario where you need a specialist. If you visit an in-network provider, your insurer covers a larger portion of the cost, and you pay a co-pay or co-insurance as outlined in your plan. For instance, a $200 specialist visit might cost you only $30 after insurance. However, if you see an out-of-network provider, the same visit could cost you $150 or more, depending on your plan’s out-of-network coverage (if any). Some plans offer no out-of-network coverage at all, leaving you responsible for the full bill. This financial disparity underscores the importance of staying in-network whenever possible.

Finding preferred providers within your network requires proactive effort. Start by logging into your insurer’s online portal or mobile app, where most plans provide a searchable directory of in-network providers. Filter by specialty, location, and patient ratings to narrow your options. For example, if you’re a 45-year-old seeking a cardiologist in downtown Chicago, you can input these specifics to find a provider who meets your needs. Additionally, calling your insurer’s customer service line can provide personalized assistance, especially if you have unique requirements, such as language preferences or accessibility needs.

While staying in-network is cost-effective, there are exceptions where out-of-network care might be necessary. For instance, if you require a highly specialized treatment not available within your network, your insurer may grant an exception. However, this typically involves pre-authorization and documentation from your provider. Another scenario is emergency care, where federal law mandates coverage regardless of network status, though follow-up care must return to in-network providers to avoid additional costs. Always verify coverage details with your insurer before proceeding with out-of-network care to avoid unexpected bills.

In conclusion, navigating provider networks is a cornerstone of effective health insurance utilization. By prioritizing in-network care, leveraging your insurer’s tools to find preferred providers, and understanding exceptions for out-of-network care, you can optimize both your health outcomes and financial well-being. Remember, a little research upfront can save significant costs and hassle down the line.

Applying for Marketplace Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

$32.28 $49.99

![]()

Enrollment Periods: Open enrollment, special enrollment, and how to apply for coverage

Health insurance enrollment isn't a year-round free-for-all. Understanding the designated periods is crucial for securing coverage. Open enrollment, typically occurring annually in the fall, is the primary window for individuals and families to enroll in or change their health insurance plans. This period, often lasting a few months, is your chance to assess your needs, compare options, and make informed decisions without facing penalties for lack of coverage. Missing this window generally means waiting until the next open enrollment, unless you qualify for a special enrollment period.

Marketplaces like Healthcare.gov provide clear dates and resources to navigate this process.

Life doesn't always align with open enrollment schedules. Special enrollment periods (SEPs) offer a safety net for those experiencing qualifying life events. These events include losing job-based coverage, getting married, having a baby, or moving to a new area. Each event triggers a specific timeframe, usually 60 days, during which you can enroll in a new plan or change your existing one. Documentation proving the qualifying event is essential when applying during an SEP. For instance, a marriage certificate or a letter from an employer confirming job loss will be required. Understanding SEPs ensures you're not left uninsured during life's transitions.

Applying for coverage, whether during open or special enrollment, involves a structured process. Start by gathering necessary documents: proof of income, Social Security numbers, and information about current coverage (if applicable). Utilize online marketplaces or work with a licensed broker to compare plans based on premiums, deductibles, and network coverage. Once you've selected a plan, complete the application, ensuring accuracy to avoid delays. Be mindful of deadlines; submitting your application close to the enrollment period's end might lead to coverage starting later than expected. Many marketplaces offer assistance via phone or in-person to guide you through the application process.

While enrollment periods provide opportunities, they also come with pitfalls. Procrastination is a common mistake; starting early allows time for research and comparison. Another misstep is underestimating the importance of understanding plan details. A lower premium might mean higher out-of-pocket costs, so consider your healthcare needs carefully. Lastly, failing to update your information during enrollment can lead to incorrect subsidy calculations or coverage gaps. Regularly reviewing and updating your application details ensures your coverage remains aligned with your current situation.

In conclusion, navigating enrollment periods requires awareness, preparation, and timely action. Open enrollment is your annual opportunity, while special enrollment periods accommodate life's unexpected changes. By understanding these windows, gathering necessary documentation, and avoiding common pitfalls, you can secure health insurance that meets your needs. Remember, staying informed and proactive is key to maintaining continuous coverage and financial protection.

Why Insurance Companies Require Current Bodily Injury Limits: Explained

You may want to see also

Explore related products

$9.97 $19.99

![]()

Claims & Appeals: Filing claims, understanding denials, and the appeals process for disputes

Filing a health insurance claim can feel like navigating a labyrinth, especially when you're already dealing with a medical issue. The process begins with understanding what your policy covers and ensuring your provider submits the claim correctly. Most insurers require a detailed claim form, including the diagnosis, treatment codes, and provider information. For instance, if you’re filing for a prescription, include the drug name, dosage (e.g., 20mg of atorvastatin daily), and the pharmacy’s National Provider Identifier (NPI). Submitting claims electronically often speeds up processing, so confirm if your insurer or provider offers this option.

Denials are a common frustration, but they’re not always the end of the road. Understanding the reason for a denial is crucial. Common causes include missing documentation, services deemed "not medically necessary," or errors in coding. For example, a claim for physical therapy might be denied if the insurer requires pre-authorization, which wasn’t obtained. Insurers are required to provide a clear explanation for denials, often in writing, so review this carefully. If the denial seems unjustified, don’t hesitate to contact your insurer’s customer service for clarification. Sometimes, a simple resubmission with corrected information resolves the issue.

The appeals process is your next step if a denial persists. This formal procedure varies by insurer but typically involves submitting a written appeal within a specific timeframe, often 60–180 days. Include all supporting documents, such as medical records, a letter from your healthcare provider, or proof of prior authorization. For instance, if your insurer denied coverage for a specialized MRI, a radiologist’s statement explaining its medical necessity could strengthen your case. Some states also offer external review processes, where an independent third party evaluates the dispute.

A successful appeal often hinges on persistence and organization. Keep a detailed record of all communications, including dates, names, and summaries of conversations. If you’re unsure how to proceed, many insurers provide appeal templates or guidance on their websites. For complex cases, consider consulting a patient advocate or attorney specializing in healthcare disputes. While the process can be time-consuming, appealing a denial can result in coverage for critical treatments, making it a worthwhile effort.

Finally, prevention is key to avoiding claims disputes. Review your policy annually to understand exclusions and requirements, especially if you have a chronic condition or anticipate major medical expenses. For example, if you’re planning surgery, verify coverage and obtain pre-authorization weeks in advance. Staying proactive reduces the likelihood of denials and ensures you’re prepared to act if issues arise. With the right knowledge and approach, navigating claims and appeals becomes less daunting and more manageable.

How to Disenroll from Medical Insurance: A Comprehensive Guide

You may want to see also

Frequently asked questions

AM Health Insurance refers to health insurance policies that provide coverage for medical expenses, including hospitalization, doctor visits, prescription drugs, and preventive care. The term "AM" may refer to a specific provider or plan type, so it’s important to verify the details with the insurer.

Coverage varies by plan, but AM Health Insurance typically includes hospitalization, outpatient care, emergency services, maternity care, mental health services, and prescription medications. Some plans may also offer additional benefits like dental, vision, or wellness programs.

Enrollment in AM Health Insurance can be done through the insurer’s website, a licensed broker, or during the annual open enrollment period. You may also qualify for a special enrollment period if you experience a life event like marriage, birth, or loss of other coverage.

Yes, under most AM Health Insurance plans, pre-existing conditions are covered. The Affordable Care Act (ACA) prohibits insurers from denying coverage or charging higher premiums based on pre-existing conditions. However, coverage specifics may vary, so review your policy details carefully.