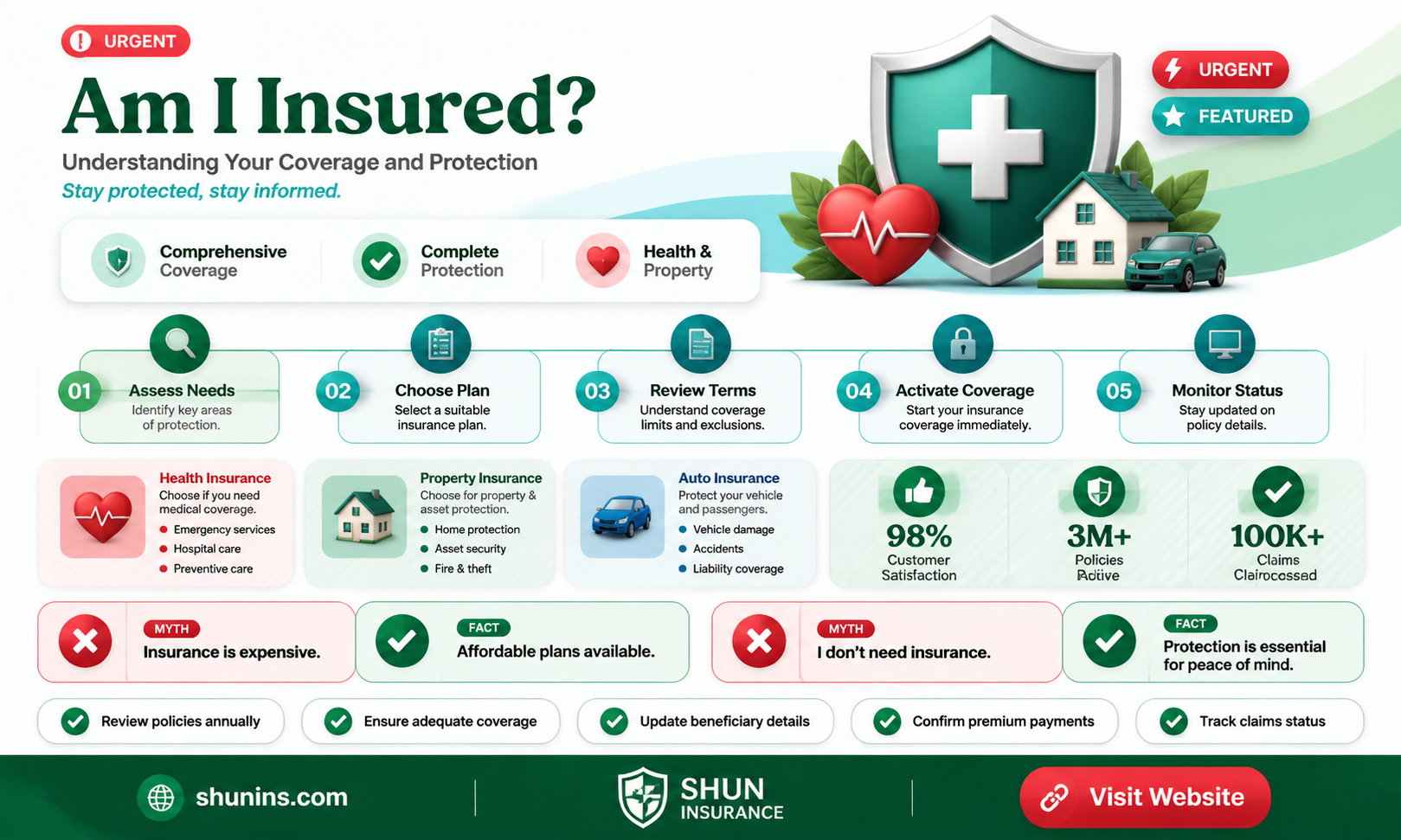

Navigating the complexities of insurance coverage can often leave individuals questioning, Am I insured? This fundamental question arises in various aspects of life, from health and auto to home and life insurance. Understanding the extent of your coverage, the conditions under which it applies, and any potential gaps is crucial for financial security and peace of mind. Whether you're dealing with unexpected medical bills, a car accident, or damage to your property, knowing your insurance status ensures you're prepared for life's uncertainties. This topic delves into how to verify your insurance, what to look for in your policy, and steps to take if you discover you're underinsured or uninsured.

| Characteristics | Values |

|---|---|

| Purpose | Tool to help individuals determine their insurance coverage status |

| Functionality | Provides a self-assessment questionnaire to evaluate insurance coverage |

| Target Audience | Individuals seeking clarity on their insurance policies |

| Key Features | Interactive questionnaire, personalized results, educational resources |

| Types of Insurance Covered | Health, auto, home, life, renters, and more |

| Accessibility | Online platform, mobile-friendly |

| Cost | Typically free to use |

| Data Security | Ensures user data privacy and security |

| Latest Update | Continuously updated with the latest insurance regulations and policies |

| User Support | FAQs, customer service, and educational guides |

| Integration | May integrate with insurance provider databases for accurate information |

| Languages Supported | Primarily English, with some platforms offering multilingual support |

| User Reviews | Generally positive, with users appreciating the clarity and ease of use |

| Limitations | Not a substitute for professional insurance advice; relies on user-provided information |

| Availability | Widely available through insurance company websites and third-party platforms |

Explore related products

What You'll Learn

- Understanding Policy Coverage: Know what your insurance policy covers and excludes to avoid surprises

- Checking Insurance Status: Verify if your policy is active and up-to-date for full protection

- Types of Insurance: Explore auto, health, home, and life insurance to ensure comprehensive coverage

- Claim Process: Learn how to file a claim and what documents are required for approval

- Policy Renewal: Stay informed about renewal dates and options to maintain continuous coverage

![]()

Understanding Policy Coverage: Know what your insurance policy covers and excludes to avoid surprises

Understanding your insurance policy coverage is crucial to ensuring you’re adequately protected when you need it most. Insurance policies are not one-size-fits-all; they vary widely in terms of what they cover and exclude. To avoid unexpected financial burdens, take the time to thoroughly review your policy documents. Start by identifying the key sections that outline covered events, such as accidents, natural disasters, or medical emergencies, depending on the type of insurance (auto, health, home, etc.). Familiarize yourself with the specific terms and definitions used in your policy, as these can significantly impact your coverage. For example, a home insurance policy might cover fire damage but exclude flood damage, requiring you to purchase additional flood insurance if needed.

Exclusions are just as important to understand as inclusions. Insurance policies often contain clauses that explicitly state what is not covered. These exclusions can range from specific types of damage (e.g., earthquakes in standard home insurance) to certain high-risk activities (e.g., extreme sports in health or life insurance). Ignoring these exclusions could leave you vulnerable to out-of-pocket expenses when you file a claim. For instance, if your auto insurance excludes rental car coverage, you may need to purchase additional protection when renting a vehicle. Always ask your insurance provider to clarify any exclusions you don’t understand.

Policy limits are another critical aspect of understanding your coverage. These limits define the maximum amount your insurer will pay for a covered claim. For example, a health insurance policy might have a yearly limit on outpatient services or a home insurance policy might cap coverage for high-value items like jewelry. Knowing these limits helps you assess whether your policy aligns with your needs. If your possessions or potential liabilities exceed your policy limits, consider increasing your coverage or purchasing supplemental insurance to bridge the gap.

Deductibles and premiums also play a significant role in your policy coverage. A deductible is the amount you must pay out of pocket before your insurance coverage kicks in. Higher deductibles often result in lower premiums, but they also mean higher costs when you file a claim. Evaluate your financial situation to determine the right balance between premiums and deductibles. Additionally, some policies offer optional add-ons or endorsements that expand coverage for specific needs, such as roadside assistance in auto insurance or identity theft protection in homeowners’ insurance. Assess whether these add-ons are worth the extra cost based on your lifestyle and risks.

Finally, don’t hesitate to ask questions or seek professional advice. Insurance policies can be complex, and it’s easy to overlook important details. Contact your insurance agent or broker to discuss your coverage in detail and clarify any uncertainties. They can help you tailor your policy to better suit your needs and ensure you’re not left with gaps in protection. Regularly reviewing your policy, especially after major life changes like buying a home or starting a family, is essential to maintaining adequate coverage. By understanding what your policy covers and excludes, you can avoid surprises and ensure you’re fully protected when it matters most.

Term Insurance vs Life Insurance: What's the Difference?

You may want to see also

Explore related products

![]()

Checking Insurance Status: Verify if your policy is active and up-to-date for full protection

Ensuring that your insurance policy is active and up-to-date is crucial for maintaining full protection and peace of mind. The first step in checking your insurance status is to review your policy documents. These documents, typically provided when you first purchased the policy, contain essential details such as the policy number, coverage period, and terms and conditions. Look for the expiration date to confirm if your policy is still active. If you cannot locate the physical documents, log into your insurer’s online portal or mobile app, where digital copies are often stored. Most insurance companies provide a user-friendly dashboard that displays your policy status, coverage details, and renewal dates.

If you’re unsure about your policy’s status, contact your insurance provider directly. Customer service representatives can verify if your policy is active, confirm your coverage limits, and address any discrepancies. Have your policy number and personal identification details ready to expedite the process. Additionally, inquire about any pending payments or updates required to keep your policy current. Some insurers also offer automated phone systems or chatbots that can provide quick updates on your policy status without the need for a live agent.

Another effective method to check your insurance status is to monitor your payment history. Regular premium payments are essential to keeping your policy active. Review your bank or credit card statements to ensure payments have been processed as scheduled. If you’ve set up automatic payments, verify that they are still active and that sufficient funds are available to avoid lapses in coverage. In case of missed payments, contact your insurer immediately to discuss reinstatement options and avoid a gap in protection.

For those with multiple insurance policies, consolidate your information in one place to stay organized. Create a spreadsheet or use a personal finance app to track policy details, renewal dates, and contact information for each insurer. This centralized approach makes it easier to monitor all your policies and ensures none are overlooked. Regularly update this information, especially after making changes to your coverage or switching providers.

Lastly, be proactive about policy renewals. Insurance policies typically require renewal annually or at specified intervals. Mark your calendar or set reminders for renewal dates to avoid accidental lapses. If you receive a renewal notice, review the updated terms and premiums carefully before confirming. If you’re considering switching providers, ensure your new policy is active before canceling the old one to maintain continuous coverage. By staying vigilant and taking these steps, you can confidently verify that your insurance policy is active and up-to-date, providing you with full protection when you need it most.

Global Life Insurance: Is It a Smart Choice?

You may want to see also

![]()

Types of Insurance: Explore auto, health, home, and life insurance to ensure comprehensive coverage

When asking yourself, "Am I insured?" it’s crucial to understand the different types of insurance available to ensure you have comprehensive coverage tailored to your needs. Auto insurance is one of the most common and legally required types of insurance in many places. It protects you financially in case of accidents, theft, or damage to your vehicle. Policies typically include liability coverage, which pays for injuries or damages you cause to others, as well as collision and comprehensive coverage, which protect your own vehicle. Without adequate auto insurance, you risk facing significant out-of-pocket expenses or legal consequences.

Another essential type of insurance to consider is health insurance, which covers medical expenses such as doctor visits, hospital stays, prescription medications, and preventive care. With rising healthcare costs, having health insurance ensures you can access necessary medical services without incurring overwhelming debt. Policies vary widely, so it’s important to evaluate factors like premiums, deductibles, and network coverage to find a plan that suits your health needs and budget. Without health insurance, even minor illnesses or injuries can lead to financial strain.

Home insurance is vital for homeowners and renters alike, as it protects your property and belongings from risks like fire, theft, or natural disasters. For homeowners, this coverage typically includes the structure of the house, personal belongings, and liability protection if someone is injured on your property. Renters insurance, on the other hand, focuses on personal belongings and liability, as the landlord’s insurance usually covers the building itself. Ensuring you have adequate home insurance safeguards your investment and provides peace of mind in case of unexpected events.

Lastly, life insurance is a critical component of financial planning, especially if you have dependents or financial obligations. It provides a financial safety net for your loved ones in the event of your death, covering expenses like funeral costs, outstanding debts, or daily living expenses. There are two main types: term life insurance, which offers coverage for a specified period, and whole life insurance, which provides lifelong coverage and includes an investment component. Evaluating your family’s needs and long-term goals will help you determine the right type and amount of life insurance.

Exploring these types of insurance—auto, health, home, and life—is essential to answer the question, "Am I insured?" comprehensively. Each type serves a unique purpose and addresses specific risks, ensuring you are protected in various aspects of life. By assessing your individual circumstances and prioritizing coverage gaps, you can build a robust insurance portfolio that provides financial security and peace of mind. Remember, being adequately insured is not just about meeting legal requirements but also about safeguarding your future and the well-being of your loved ones.

Insurance Solutions: A-Z Llanelli's Comprehensive Coverage

You may want to see also

![]()

Claim Process: Learn how to file a claim and what documents are required for approval

Filing an insurance claim can seem daunting, but understanding the process and required documents can make it smoother. The first step is to notify your insurance provider as soon as possible after an incident occurs. Most insurers have a dedicated claims hotline or online portal for this purpose. Provide them with essential details such as your policy number, the date and time of the incident, and a brief description of what happened. Prompt notification is crucial, as delays may affect the approval process. Once reported, the insurer will assign a claims adjuster to your case, who will guide you through the next steps.

Next, gather the necessary documents to support your claim. The required paperwork varies depending on the type of insurance (e.g., auto, health, home) and the nature of the claim. Common documents include a completed claim form, a police report (if applicable), medical records, repair estimates, and proof of ownership for damaged or stolen items. For example, if you’re filing a car insurance claim, you’ll need photos of the accident scene, a copy of the other driver’s information, and any witness statements. Ensure all documents are accurate and complete to avoid delays in approval.

Once you’ve submitted the required documents, the insurance company will review your claim. This process involves verifying the details, assessing the damage or loss, and determining coverage based on your policy terms. The claims adjuster may contact you for additional information or clarification. Be responsive and cooperative during this stage to expedite the process. If your claim is approved, the insurer will outline the settlement amount or repair arrangements. If denied, they will provide a reason, and you may have the option to appeal the decision.

Throughout the claim process, keep detailed records of all communications with your insurer, including emails, letters, and phone calls. Note the names of representatives you speak with and the dates of interactions. This documentation can be invaluable if disputes arise or if you need to follow up on your claim. Additionally, familiarize yourself with your policy’s coverage limits, deductibles, and exclusions to manage expectations and ensure you’re filing a valid claim.

Finally, follow up with your insurer if you haven’t heard back within the expected timeframe. Claims processing times vary, but staying proactive ensures your case remains a priority. If you encounter challenges or have questions, don’t hesitate to seek assistance from your insurance agent or a claims representative. Understanding the claim process and being prepared with the right documents can significantly increase your chances of a successful and timely resolution.

Primary vs. Secondary Insurance: A Clear Guide to Determine Coverage Order

You may want to see also

![]()

Policy Renewal: Stay informed about renewal dates and options to maintain continuous coverage

Staying informed about your policy renewal dates and options is crucial to maintaining continuous insurance coverage. Insurance policies typically have a set term, after which they expire unless renewed. Missing a renewal deadline can lead to a lapse in coverage, leaving you unprotected and potentially facing financial risks. To avoid this, it’s essential to mark your calendar with the renewal date and set reminders well in advance. Most insurers send renewal notices via mail, email, or through their online portal, but it’s your responsibility to ensure you receive and act on these notifications. If you’ve moved or changed contact information, update your details with your insurer promptly to avoid missing critical communications.

Understanding your renewal options is equally important. When your policy is up for renewal, your insurer may offer different choices, such as maintaining the same coverage, adjusting your policy limits, or adding new features. Take the time to review these options carefully. Assess whether your current coverage still meets your needs or if changes in your life—like a new car, home improvements, or a growing family—require adjustments. Some insurers may also provide discounts or incentives for renewing early or bundling multiple policies, so explore these opportunities to maximize value. If you’re unsure about the best course of action, contact your insurance agent or customer service for guidance.

Proactively managing your policy renewal can also help you avoid unexpected premium increases. Insurers may adjust rates based on factors like claims history, market trends, or changes in risk assessment. Before renewing, review your premium amount and compare it to the previous term. If there’s a significant increase, inquire about the reasons and explore ways to reduce costs, such as increasing your deductible or removing unnecessary coverage. Additionally, consider shopping around for quotes from other insurers to ensure you’re getting the best deal. However, be cautious about switching providers solely for a lower price, as the level of coverage and customer service may differ.

Automating your renewal process can provide added peace of mind. Many insurers offer auto-renewal options, where your policy is renewed automatically unless you opt out. If you choose this route, ensure your payment method is up to date to avoid accidental lapses. Even with auto-renewal, it’s wise to review your policy details annually to confirm everything is accurate and aligned with your needs. If you prefer manual renewals, set up multiple reminders leading up to the deadline to give yourself ample time to act. Staying organized and proactive ensures you remain insured without interruption.

Finally, don’t wait until the last minute to address renewal issues. If you’re facing financial difficulties or have questions about your policy, reach out to your insurer well before the renewal date. They may offer payment plans, extensions, or alternative solutions to help you maintain coverage. Ignoring renewal notices or delaying action can result in policy cancellation or penalties, making it harder and more expensive to reinstate coverage later. By staying informed, reviewing your options, and taking timely action, you can ensure continuous protection and avoid unnecessary risks. Remember, being insured isn’t just about having a policy—it’s about keeping it active and up to date.

Life Insurance: Divorce Impact and Financial Planning

You may want to see also

Frequently asked questions

Check your policy documents, insurance cards, or contact your insurance provider directly to confirm your coverage status.

A lapsed policy means your coverage has expired due to non-payment or other reasons, leaving you uninsured until it’s reinstated or a new policy is purchased.

Yes, depending on the type of insurance (e.g., auto, health), you may be covered under someone else’s policy if you meet the criteria specified in their plan.

Review your policy details, contact your insurance agent or provider, and ask for clarification on what is and isn’t covered under your plan.