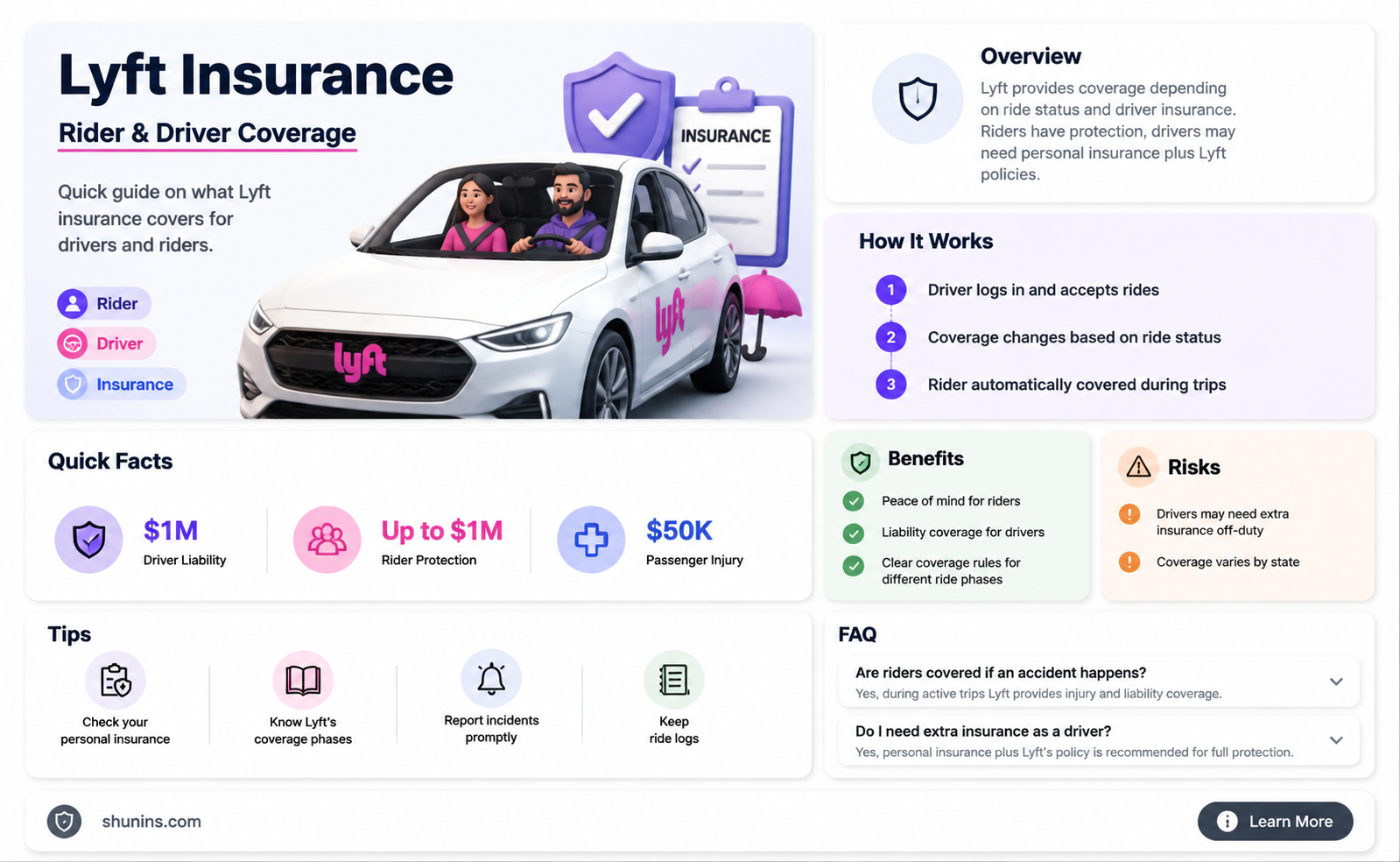

If you're a Lyft driver or passenger, it's important to understand the company's insurance policies and how they apply to you. Lyft provides insurance coverage for its drivers, but it's not all-encompassing, and there are periods when you may not be covered. For instance, if you're driving in a state like New York with Taxi and Limousine Commission regulations, you'll need to procure your own insurance. Understanding the different periods of coverage and how they interact with your personal insurance is key to ensuring you're protected.

| Characteristics | Values |

|---|---|

| Lyft insurance coverage | Lyft insurance provides liability, collision and comprehensive coverage, but coverage varies depending on where you are in the rideshare process. |

| Lyft insurance coverage limits | Lyft maintains at least $1,000,000 for third-party auto liability coverage, but these limits are lower or not procured in certain markets. |

| Lyft insurance coverage for drivers with personal auto insurance | Lyft's insurance policy kicks in when the app is open, providing liability coverage with lower limits during Period 1 and more coverage once the driver picks up and begins transporting passengers. |

| Lyft insurance coverage for drivers without personal auto insurance | Lyft requires drivers to have auto insurance that meets minimum state coverage requirements. Drivers without personal auto insurance may be suspended by the rideshare company until they reinstate their insurance. |

| Lyft insurance coverage for drivers with rideshare endorsement | Rideshare endorsement insurance extends the driver's personal car insurance policy while they are working but haven't accepted a ride request yet. Once a ride is accepted, Lyft's coverage takes over. |

| Lyft insurance coverage for Taxi and Limousine Commission (TLC) drivers in New York City and specific NY counties | Lyft does not procure insurance for rides with TLC drivers in these locations. TLC drivers must procure their own policies consistent with state and local requirements. |

| Lyft insurance coverage for livery and/or Transportation Charter Permit (TCP) drivers | Lyft does not procure insurance for rides with TCP drivers countrywide. TCP drivers must procure their own policies consistent with state and local requirements. |

| Lyft insurance coverage for drivers who rented a car through Express Drive | The standard insurance included with the rental car applies. |

Explore related products

What You'll Learn

![]()

Lyft insurance coverage while waiting for a ride request

Lyft provides insurance coverage for drivers and passengers. However, it is important to note that Lyft does not provide a full-coverage commercial policy. Instead, they offer a contingent policy, which means that their insurance is secondary to the driver's personal policy. Lyft's insurance coverage is dependent on the driver's status and can be broken down into three distinct periods.

During the first period, when a driver is waiting for a ride request, Lyft provides insurance coverage of $50,000 per person for injuries, $100,000 per accident for injuries, and $25,000 for property damage. This coverage is in place to protect drivers and passengers while they are waiting for a ride request to come through on the Lyft app. It is important to note that this coverage may vary depending on the state and local regulations.

The second period begins when the driver accepts a ride request and is en route to pick up the passenger. During this time, Lyft provides at least $1,000,000 in third-party auto liability coverage, which may include uninsured motorist coverage, underinsured motorist coverage, PIP, MedPay, and/or Occupational Accident coverage. This coverage is designed to protect both the driver and the passenger during the ride request process.

The third period starts when the driver picks up the passenger and the ride is in progress. The coverage during this period is similar to the second period, but it now extends to the passenger as well. Lyft provides up to $50,000 in comprehensive and collision coverage with a $2,500 deductible. Additionally, Lyft offers uninsured/underinsured motorist coverage if the at-fault driver lacks adequate insurance.

It is important to note that Lyft's insurance coverage is contingent upon the driver having valid personal auto insurance that meets the minimum state coverage requirements. If a driver does not have valid personal insurance, they may not be covered by Lyft's policy, and their access to the ridesharing service may be suspended until they reinstate their insurance.

Get a Life Insurance License in Washington: What You Need to Know

You may want to see also

Explore related products

![]()

Lyft insurance coverage while en route to pick up a passenger

Lyft provides insurance coverage for drivers and passengers. When the Lyft app is on and a driver is on their way to pick up a passenger, Lyft provides $1 million in liability coverage and $1 million in uninsured/underinsured motorist protection. This is known as Period 2.

During Period 2, Lyft-specific coverage kicks in, which includes third-party liability insurance for covered accidents if your personal insurance does not apply. Lyft maintains at least $1 million in third-party auto liability coverage in most markets, though this amount may be lower or not procured in certain markets.

In Maryland, for example, third-party liability insurance is $125,000 (combined single limits for bodily injury and property damage) during the time in which a driver is en route to pick up a passenger, consistent with state requirements.

Lyft does not provide a full-coverage commercial policy. Instead, it offers a contingent policy, which means that if you're in an accident while driving for Lyft, their insurance is secondary to your personal policy. If you have comprehensive and collision coverage on your personal auto policy, Lyft maintains contingent comprehensive and collision coverage up to the actual cash value of the car ($2,500 deductible).

It's important to note that Lyft does not procure insurance for rides with Taxi and Limousine Commission (TLC) drivers originating in the five boroughs of New York City and specific NY counties (Westchester, Nassau, Suffolk, Dutchess, Ulster, and Rockland). In these cases, TLC drivers must procure their own policies consistent with state and local requirements.

Converting Term Life Insurance to Permanent: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Lyft insurance coverage while driving with a passenger

Lyft maintains third-party liability insurance for covered accidents if your personal insurance does not apply. Lyft insurance coverage for drivers with comprehensive and collision coverage on their personal auto policy includes at least $1,000,000 for third-party auto liability coverage. First-party coverages may include uninsured motorist coverage, underinsured motorist coverage, PIP, MedPay, and/or Occupational Accident coverage.

In Maryland, third-party liability insurance is $125,000 (combined single limits for bodily injury and property damage) during the time in which a driver is en route to pick up a passenger, consistent with state requirements. In Arizona and Nebraska, third-party liability insurance is $25,000 per person for bodily injury, $50,000 per accident for bodily injury, and $20,000 per accident for property damage, consistent with state requirements.

It is important to note that Lyft does not procure insurance for rides with Taxi and Limousine Commission (TLC) drivers in the five boroughs of New York City and specific NY counties (Westchester, Nassau, Suffolk, Dutchess, Ulster, and Rockland), and livery and/or Transportation Charter Permit (TCP) drivers countrywide. TLC, livery, and TCP drivers must procure their own policies consistent with state and local requirements.

Converting Group Life Insurance: Understanding Your Time Limit

You may want to see also

Explore related products

![]()

Lyft insurance coverage for drivers with personal insurance

Period 0:

This is when you are not driving for Lyft and your personal insurance policy applies. It is important to note that most personal auto policies do not cover you while driving for Lyft, so it is recommended to purchase a rideshare endorsement or a separate rideshare insurance policy.

Period 1:

Period 1 begins when you turn on the Lyft app and start waiting for ride requests. During this period, your personal insurance policy and Lyft's coverage work together. Lyft provides contingent comprehensive and collision coverage with a $2,500 deductible, while your personal insurance fills in the gaps with liability, uninsured motorist, and other types of coverage.

Period 2:

Period 2 starts when you accept a ride request and are on your way to pick up the passenger. At this point, Lyft's coverage takes over, providing at least $1,000,000 in third-party auto liability coverage and first-party coverages such as uninsured motorist protection and medical payments.

Period 3:

Period 3 begins when you are driving your passenger to their destination. Lyft's coverage continues from Period 2, but now it extends to the passenger as well, ensuring they are covered in the event of an accident.

It is important to note that Lyft does not provide insurance for Taxi and Limousine Commission (TLC) drivers in certain areas, such as New York City and specific counties in New York state. In these cases, TLC drivers must procure their own insurance policies in accordance with state and local requirements. Additionally, Lyft's coverage varies by state, so it is essential to review the specific insurance details for your location.

To ensure you have adequate insurance coverage as a Lyft driver, it is recommended to purchase a rideshare endorsement or a separate rideshare insurance policy. This will extend your personal insurance policy to cover the period when you are working but have not yet accepted a ride request, providing comprehensive protection while driving for Lyft.

Gerber Life Insurance: Doubling Benefits for Parents

You may want to see also

Explore related products

![]()

Lyft insurance coverage for drivers without personal insurance

Lyft requires its drivers to have auto insurance that meets the minimum state coverage requirements. However, most personal auto insurance policies do not cover you while driving for Lyft, as it is considered a business activity. Therefore, Lyft drivers without personal insurance will need to purchase additional coverage.

Rideshare insurance or a rideshare endorsement is an inexpensive policy add-on that extends your personal car insurance policy while driving for Lyft. This type of insurance typically costs between $10 to $350 per year, depending on your location and insurer, and can usually be added to your existing policy. Some insurance companies that offer rideshare endorsements include State Farm, Allstate, and Mercury.

If you do not have a rideshare endorsement on your personal policy, your insurance company may deny coverage for incidents occurring during business use of the vehicle, and Lyft's contingent policy will not apply. Lyft's insurance is secondary to your personal policy and only comes into effect after your personal policy has been exhausted.

It is important to note that Lyft does not provide a full-coverage commercial policy. Their coverage is limited and only applies in specific situations, such as when you have accepted a ride request and have certain types of coverage on your personal insurance policy. Therefore, it is essential for Lyft drivers to carefully review their insurance policies and understand the limitations of their coverage.

Life Insurance: Secure Your Family's Future with 1MM Cover

You may want to see also

Frequently asked questions

Lyft provides liability, collision and comprehensive coverage, including $1 million of third-party liability coverage, uninsured/underinsured motorist bodily injury coverage, and contingent comprehensive and collision coverage.

Lyft insurance coverage kicks in when you have the Lyft app active and have received a ride request.

You need a rideshare endorsement, which extends your personal car insurance policy while you are working but have not accepted a ride request.

Yes, Lyft insurance covers passengers during a ride in progress.

If you get into an accident while driving for Lyft, you should follow the structured claims process, which includes obtaining information about the rideshare's insurance provider, reviewing their coverage policies, and understanding how it interacts with your personal insurance.

![YSY LED Car Window Accessory Sign RIDESHARE for Ride Share Drivers taxi light - 6ft. USB Cable [On/Off Switch] (Green)](https://m.media-amazon.com/images/I/51VINH-AdqL._AC_UL320_.jpg)