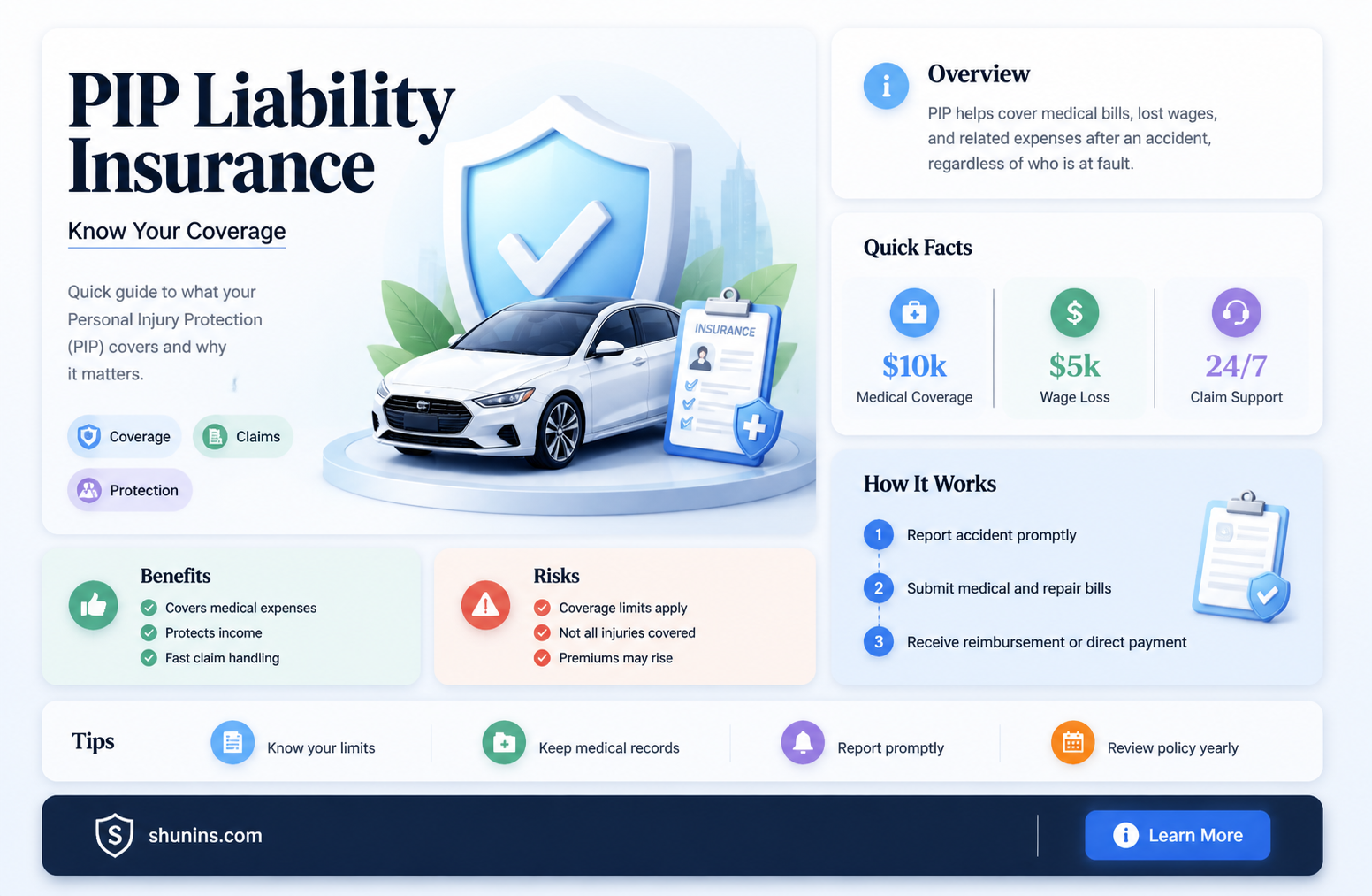

Personal Injury Protection (PIP) insurance, also known as no-fault insurance, covers medical bills and related costs resulting from an accident, regardless of who is at fault. PIP insurance covers the policyholder and their passengers, and in some cases, pedestrians. It also covers lost wages and other expenses such as funeral costs and property damage. Liability insurance, on the other hand, covers expenses resulting from property damage or injuries caused by the policyholder in an accident. It is important to understand the differences between PIP and liability insurance to make an informed decision about the level of coverage required and to ensure adequate protection in the event of an accident.

| Characteristics | Values |

|---|---|

| What is PIP? | Personal Injury Protection (PIP) covers medical expenses and related costs resulting from an accident, no matter who caused it. |

| Who does PIP cover? | PIP covers medical expenses for both injured policyholders and passengers, even if some don't have health insurance. |

| When is PIP mandatory? | PIP is mandatory in some states, optional in others, and not available in others. |

| When is PIP useful? | PIP is useful when you don't have health insurance or when your health insurance deductible is high. It can also cover lost wages and other expenses not covered by health insurance. |

| What is liability insurance? | Liability insurance covers expenses that result from property damage or injuries caused by the policyholder in an accident. It includes bodily injury liability and property damage liability. |

| When is liability insurance mandatory? | Liability insurance is required in most states, but the specific requirements vary. |

| How do PIP and liability insurance differ? | PIP covers the policyholder's expenses regardless of fault, while liability insurance covers expenses for third parties when the policyholder is at fault. |

Explore related products

What You'll Learn

- PIP covers medical expenses for policyholders and passengers, regardless of fault

- Liability insurance covers third-party medical costs if the policyholder is at fault

- Liability insurance is required in most states, while PIP is optional in many

- PIP covers lost wages, while liability insurance does not

- PIP can help cover expenses like childcare and house cleaning

![]()

PIP covers medical expenses for policyholders and passengers, regardless of fault

Personal Injury Protection (PIP) insurance, also known as no-fault insurance, covers medical expenses and lost wages for the policyholder and their passengers in the event of an accident, regardless of who is at fault. PIP is mandatory in some states and optional or not offered in others. Twelve states require PIP coverage: Delaware, Florida, Hawaii, Kansas, Massachusetts, Michigan, Minnesota, New Jersey, New York, North Dakota, Oregon, and Utah. In these states, drivers are required to carry PIP coverage to ensure that their medical expenses resulting from a car accident are covered by their insurance, regardless of fault.

While nearly every state requires liability insurance for all drivers, PIP coverage is only mandatory or optional in certain states. In at-fault states, liability insurance is required, and PIP coverage may be optional or not available. However, even in at-fault states, PIP can be a valuable addition to a car insurance policy. It provides prompt payment for auto accident injuries, lost wages, and other additional costs.

The cost of PIP coverage varies depending on factors such as the amount of coverage, the number of cars on the policy, age, and the type of car driven. PIP typically covers medical expenses first, followed by health insurance for any remaining costs. It's important to note that PIP doesn't cover all injury-related expenses. For injuries caused to others, the bodily injury portion of liability insurance would be applicable. Additionally, PIP doesn't cover expenses unrelated to personal injuries, such as damage to your vehicle, which would require comprehensive car insurance.

In summary, PIP insurance provides valuable coverage for medical expenses and lost wages, regardless of fault. It is essential to understand the specific requirements and offerings of your state, as well as the details of your insurance policy, to make informed decisions about your coverage needs.

Obama's Mother's Insurance Battle: A Son's Witness

You may want to see also

Explore related products

![]()

Liability insurance covers third-party medical costs if the policyholder is at fault

Personal injury protection (PIP) insurance, also known as no-fault insurance, covers the policyholder's medical expenses and lost wages resulting from a car accident, regardless of who is at fault. PIP insurance may also cover the policyholder's passengers and, in some cases, pedestrians. In addition to medical costs, PIP can also cover lost wages, funeral expenses, and other costs related to injuries sustained in an accident, such as household services or child care.

Liability insurance, on the other hand, covers third-party medical costs if the policyholder is at fault. It pays for expenses resulting from property damage or injuries caused by the policyholder or anyone listed on their policy. This includes bodily injury liability, which covers medical expenses and lost wages for injured third parties, and property damage liability, which covers repairs or replacements for damaged property belonging to someone else.

The key difference between PIP and liability insurance is who benefits from the coverage. While PIP covers the policyholder and their passengers, liability insurance covers third parties who have been injured or had their property damaged by the policyholder.

The requirements for PIP and liability insurance vary by state. Some states mandate PIP coverage through "no-fault insurance" laws, while others make it optional or unavailable. In contrast, 49 states and Washington, D.C., require motorists to carry liability insurance, with penalties for non-compliance ranging from fines to jail time.

When determining whether to purchase PIP or liability insurance, individuals should consider their state's requirements, the coverage provided by their existing health insurance, and their ability to pay out of pocket for medical treatment and repair bills.

Life Insurance Options for People with Ulcerative Colitis

You may want to see also

Explore related products

![]()

Liability insurance is required in most states, while PIP is optional in many

Personal Injury Protection (PIP) insurance, also known as no-fault insurance, covers medical expenses and lost wages for you and your passengers if you're injured in an accident. It also covers funeral expenses and other costs related to injuries, such as house cleaning. PIP is required in some states, optional in others, and not available in a few. The Insurance Information Institute reports that 12 states require PIP coverage: Delaware, Florida, Hawaii, Kansas, Massachusetts, Michigan, Minnesota, New Jersey, New York, North Dakota, Oregon, and Utah.

On the other hand, Liability insurance covers expenses that result from property damage or injuries suffered by someone else in an accident that is your fault. It also covers legal costs, settlements, and judgments if you are sued due to an accident. Nearly every state requires liability insurance for all drivers, except for New Hampshire, which only mandates it for some drivers.

The main difference between the two types of insurance is who benefits from them. PIP covers the policyholder's expenses, while liability insurance covers expenses resulting from damage or injuries caused by the policyholder. In most no-fault insurance states, drivers are still required to carry bodily injury liability coverage to pay for injuries that exceed the state's threshold for bodily injury lawsuits. If your state doesn't require or offer PIP, you may be able to add medical payments coverage (Med Pay) to your auto policy instead.

If you live in a state where PIP is optional, consider purchasing at least the minimum amount of coverage if you don't have health insurance or have a high-deductible health plan. PIP can provide valuable additional coverage for lost wages and other expenses not typically covered by health insurance. However, if you have a good health insurance plan that adequately covers car accident injuries, you might choose to decline PIP.

Breadwinners: Choosing the Right Life Insurance for Peace of Mind

You may want to see also

Explore related products

![]()

PIP covers lost wages, while liability insurance does not

Personal Injury Protection (PIP), also known as no-fault insurance, covers medical expenses and lost wages for you and your passengers if you're injured in an accident. PIP coverage protects you regardless of who is at fault. PIP insurance can pay for medical bills, lost wages, and more after a car accident. PIP coverage may include a deductible, with a range of deductible amounts to choose from. In some states, non-medical benefits such as coverage for lost wages, household services, and disability can protect you, your passengers, and family members in your household, even if they're not on your policy.

PIP covers lost wages up to a specific amount and length of time. If you're self-employed and your injuries require you to hire subcontractors or temporary employees, PIP can help cover those costs as well. PIP can also help pay for services that you'd normally perform if you weren't injured, like childcare and house cleaning.

On the other hand, liability insurance does not cover lost wages. Liability coverage pays for expenses that result from property damage or injuries suffered by someone else in an accident that is your fault. Liability coverage pays for injuries to people (bodily injury liability) or damage to property (property damage liability) caused by the policyholder or another covered driver. Bodily injury liability coverage applies to injuries that the policyholder or anyone listed on their policy causes to someone else in a car accident. It may cover expenses such as hospital bills, lost wages for an injured person, or legal bills if an injured person sues the policyholder.

Understanding Insurance and MOT Exemptions

You may want to see also

Explore related products

![]()

PIP can help cover expenses like childcare and house cleaning

Personal Injury Protection (PIP) insurance, also known as no-fault insurance, covers medical expenses and lost wages for you and your passengers if you're injured in an accident. PIP coverage protects you regardless of who is at fault. In some states, non-medical benefits, such as coverage for lost wages, household services, and disability, can protect you, your passengers, and family members in your household, even if they're not on your policy.

PIP insurance can help cover expenses like childcare and house cleaning. This is especially useful if you are unable to perform these tasks due to injuries sustained in an accident. PIP coverage can provide reimbursement for lost wages and payments for services you cannot carry out, such as house cleaning. This means that if you are unable to work or perform household chores due to your injuries, PIP can help cover the cost of childcare and house cleaning services.

While PIP covers a range of expenses, it is important to note that it may not cover all injury-related expenses in the event of a car accident. For instance, if you are at fault in an accident that results in injuries to others, you will need to rely on the bodily injury portion of your liability car insurance. Additionally, PIP may not cover all types of household services, so it is essential to review your specific policy to understand what is included in your coverage.

The cost of PIP coverage can vary depending on factors such as the amount of coverage, the number of vehicles insured, and personal factors like age. In some states, PIP coverage may include a deductible, allowing you to choose from a range of deductible amounts. It is recommended to consult with your insurance company or agent to determine the specific details of your PIP coverage and whether it includes expenses like childcare and house cleaning.

Overall, PIP insurance provides valuable protection by covering medical expenses, lost wages, and certain non-medical benefits. Its ability to cover expenses like childcare and house cleaning can be especially beneficial for individuals and families who rely on these services, ensuring that they receive the necessary support during challenging times.

Why Life Insurance Agents Have High Turnover Rates

You may want to see also

Frequently asked questions

PIP insurance covers medical expenses and lost wages for the policyholder and passengers in the event of an accident, regardless of who is at fault. Liability insurance, on the other hand, covers expenses incurred by third parties, such as injuries to other drivers, passengers, and pedestrians, as well as damage to property.

Yes, certain states follow a "no-fault" insurance system, where each person must cover their own expenses in the event of an accident, regardless of fault. In these states, PIP coverage is mandatory, and drivers are required to have a minimum amount of PIP insurance.

If your state requires PIP, you must purchase it. If you are caught without the necessary insurance, you may face penalties such as fines, suspension of your driver's license, loss of vehicle registration, or even jail time.

It depends on the coverage provided by your health insurance plan. If your health insurance covers injuries and rehabilitation services, you may only need the minimum amount of PIP required by your state. PIP offers additional benefits that health insurance may not, such as reimbursement for lost wages and payments for services you cannot perform due to your injuries.