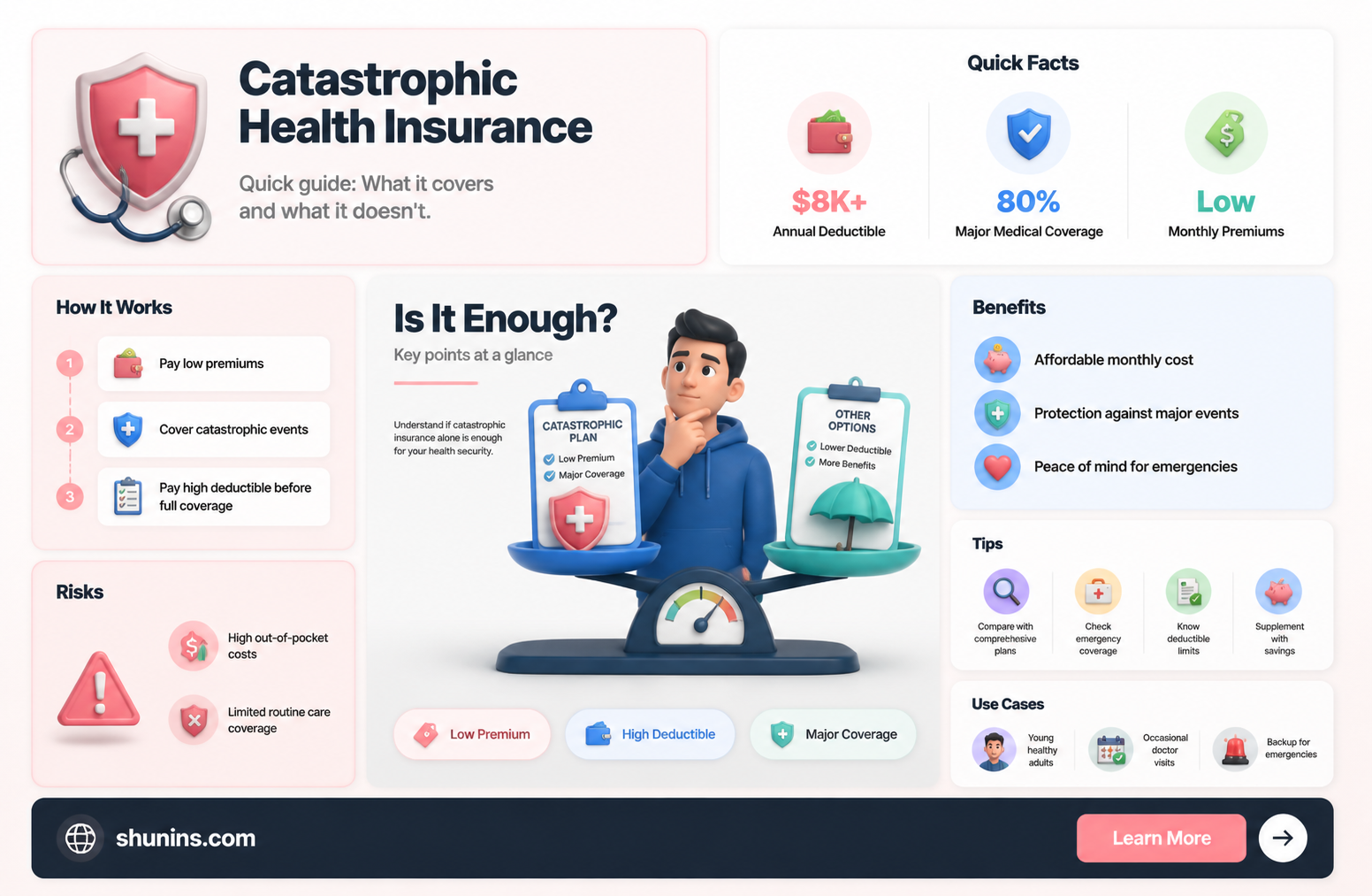

Considering whether catastrophic health insurance is sufficient for your needs involves weighing its limited coverage against potential financial risks. Catastrophic plans typically cover only major medical emergencies, leaving you responsible for routine care, prescriptions, and minor illnesses. While these plans often come with lower monthly premiums and high deductibles, they may not provide adequate protection if you require frequent medical attention or have ongoing health conditions. Before deciding, assess your current health, lifestyle, and financial situation to determine if the savings outweigh the risk of facing significant out-of-pocket expenses in case of unexpected medical events.

Explore related products

$14.07 $24.95

What You'll Learn

![]()

Understanding catastrophic health insurance basics

Catastrophic health insurance is designed for the worst-case scenario, not the everyday sniffles or routine check-ups. It’s a high-deductible plan that covers you after you’ve spent thousands out of pocket, typically kicking in at $7,000 to $10,000 for an individual or double that for a family. This plan is ideal for those who are young, healthy, and confident they won’t need frequent medical care. For example, a 25-year-old with no chronic conditions might pay as little as $200 a month for catastrophic coverage, saving significantly compared to comprehensive plans that cost $400 or more. However, if you break your leg and face a $30,000 hospital bill, you’ll still be on the hook for the first $8,000 before coverage begins.

To determine if catastrophic insurance is right for you, assess your health and financial risk tolerance. Start by reviewing your medical history: Do you have chronic conditions like diabetes or hypertension? If so, catastrophic coverage will leave you exposed to high costs for ongoing care. Next, evaluate your emergency fund. Could you comfortably cover a $7,000 deductible if hospitalized? If not, this plan could lead to financial strain. For instance, a 30-year-old with asthma might save $3,000 annually on premiums but risk paying $10,000 for an asthma-related hospitalization. In contrast, a healthy freelancer with $15,000 in savings might find this plan a smart hedge against unexpected disasters.

One overlooked aspect of catastrophic insurance is its inclusion of preventive care, as mandated by the Affordable Care Act. This means you can still access free annual check-ups, vaccinations, and screenings without meeting the deductible. For example, a 28-year-old on this plan can get a flu shot, cancer screenings, and birth control at no cost. However, if you need a specialist visit or diagnostic test outside preventive care, you’ll pay full price until the deductible is met. This feature makes catastrophic plans more viable for those who prioritize staying healthy but want protection against major events.

Finally, consider the long-term implications of choosing catastrophic coverage. While it’s cheaper upfront, it shifts the risk of high medical costs entirely onto you. For instance, a 40-year-old who switches to this plan might save $500 monthly but face $12,000 in out-of-pocket costs for an unexpected surgery. Alternatively, pairing catastrophic insurance with a health savings account (HSA) can offset costs. Contributing $3,000 annually to an HSA, tax-free, could build a safety net for deductibles while lowering your taxable income. This strategy works best for those with stable finances and a disciplined savings approach.

In summary, catastrophic health insurance is a gamble—a low-cost bet that you’ll stay healthy enough to avoid high medical expenses. It’s not for everyone, but for young, healthy individuals with solid savings, it can be a financially savvy choice. Before committing, calculate your potential out-of-pocket costs, assess your health risks, and explore complementary strategies like HSAs. Done right, it’s a way to protect against financial ruin without overpaying for coverage you may never use.

Health Insurance and Retroactive Coverage: Understanding the Limits

You may want to see also

Explore related products

![]()

Evaluating personal health risks and needs

Catastrophic health insurance, designed to cover major medical emergencies, leaves a significant gap in everyday healthcare coverage. This makes evaluating your personal health risks and needs critical before relying solely on such a plan. Start by assessing your age, lifestyle, and medical history. Younger, healthier individuals with no chronic conditions might find catastrophic insurance sufficient, as their risk of frequent medical needs is lower. However, those with pre-existing conditions like diabetes, hypertension, or asthma, or individuals over 40, should carefully consider the potential costs of unmanaged routine care. For example, a 30-year-old with no health issues might save on premiums, while a 50-year-old with high blood pressure could face thousands in out-of-pocket expenses for regular check-ups and medications.

Next, analyze your tolerance for financial risk. Catastrophic plans typically have high deductibles, often $7,000 or more, which must be paid before coverage kicks in. If you’re comfortable setting aside an emergency fund to cover this amount, the plan might align with your financial strategy. However, if unexpected expenses would strain your budget, the lack of coverage for routine care—like vaccinations, screenings, or minor illnesses—could lead to deferred treatment and compounded health issues. For instance, skipping a $200 annual physical could result in undetected early-stage conditions that later require costly interventions.

Consider your lifestyle and preventive care habits. If you prioritize wellness, exercise regularly, and maintain a balanced diet, your risk of sudden health crises may be lower. However, accidents and unforeseen illnesses can happen to anyone. Evaluate whether you’re willing to pay out-of-pocket for preventive services like flu shots, cancer screenings, or mental health visits, which aren’t covered under catastrophic plans. For example, a mammogram can cost $200–$500, while a therapy session averages $100–$200 per visit. If these expenses are manageable for you, catastrophic insurance might remain a viable option.

Finally, weigh the long-term implications of limited coverage. While catastrophic insurance protects against bankruptcy from major events like surgeries or hospitalizations, it doesn’t address chronic disease management or aging-related health declines. If you anticipate needing regular care as you age, or if your family history suggests a higher risk of conditions like heart disease or cancer, a more comprehensive plan might be wiser. For instance, a 45-year-old with a family history of diabetes would benefit from a plan covering regular A1C tests and medications, which catastrophic insurance excludes.

In summary, deciding if catastrophic insurance is sufficient requires a detailed self-assessment of health risks, financial stability, and lifestyle choices. While it can be a cost-effective option for low-risk individuals, those with higher health needs or limited savings may find the gaps in coverage more costly in the long run. Practical steps include consulting a healthcare advisor, estimating annual out-of-pocket costs for routine care, and honestly evaluating your ability to manage unexpected medical expenses.

Diabetes Medicine Coverage Denials: Why Insurance Companies Are Refusing to Pay

You may want to see also

Explore related products

![]()

Comparing costs versus comprehensive plans

Catastrophic health insurance plans are designed to protect against high medical costs from severe illnesses or accidents, but they come with low monthly premiums and high deductibles. For instance, a typical catastrophic plan might have a deductible of $7,000 or more, meaning you pay all medical expenses out of pocket until you reach that threshold. In contrast, comprehensive plans, such as PPOs or HMOs, offer lower deductibles (often $1,000–$3,000) and cover a broader range of services, including preventive care, prescriptions, and specialist visits. The trade-off? Comprehensive plans cost significantly more in monthly premiums—sometimes double or triple that of catastrophic plans.

Consider a 30-year-old individual in good health. A catastrophic plan might cost $200–$300 per month, while a comprehensive plan could range from $500–$800. If this person rarely visits the doctor and has no chronic conditions, the catastrophic plan saves them $3,600–$7,200 annually in premiums. However, if they face an unexpected emergency—say, a broken leg requiring surgery—they’d pay the full deductible before insurance kicks in. The out-of-pocket cost for such an event could easily exceed $10,000. Meanwhile, a comprehensive plan would cap their out-of-pocket expenses at a much lower amount, often around $5,000–$8,000, while covering preventive care that could avoid future emergencies.

For those under 30 or in excellent health, catastrophic plans can seem appealing due to their affordability. But this demographic should weigh the risk: Are you financially prepared to cover a $7,000 deductible if an accident occurs? Alternatively, comprehensive plans provide peace of mind and encourage regular check-ups, which can detect issues early. For example, a yearly physical or cancer screening covered under a comprehensive plan could identify a treatable condition before it becomes catastrophic—both medically and financially.

A practical tip: If you’re considering catastrophic insurance, pair it with a health savings account (HSA) to set aside pre-tax dollars for medical expenses. Aim to save at least $2,000–$3,000 annually to offset potential out-of-pocket costs. Conversely, if you opt for a comprehensive plan, review its network restrictions and prescription coverage to ensure it aligns with your healthcare needs. For families or individuals with chronic conditions, the higher premiums of comprehensive plans often outweigh the risk of facing unforeseen medical debt.

Ultimately, the decision hinges on your risk tolerance, health status, and financial stability. Catastrophic plans are a gamble—ideal for those who rarely need medical care and can afford high deductibles in emergencies. Comprehensive plans, while pricier, offer predictable costs and broader coverage, making them a safer bet for those prioritizing preventive care or managing ongoing health issues. Assess your lifestyle, budget, and medical history before choosing, as the wrong decision could leave you underinsured or overpaying.

Insurance Companies That Skip MIB Checks: Your Guide

You may want to see also

Explore related products

![]()

Assessing coverage limits and exclusions

Catastrophic health insurance plans are designed to protect against high medical costs, but they come with significant coverage limits and exclusions that can leave you financially vulnerable. Understanding these restrictions is crucial to determining whether this type of plan is sufficient for your needs. For instance, most catastrophic plans have a high deductible—often $7,000 or more for an individual—which means you’ll pay out of pocket for most routine and preventive care until you reach that threshold. This structure makes catastrophic insurance ideal for young, healthy individuals who rarely visit the doctor but can be risky for those with chronic conditions or unpredictable health needs.

To assess whether catastrophic insurance aligns with your health profile, start by reviewing the plan’s exclusions. Common exclusions include prescription drugs, mental health services, maternity care, and physical therapy. For example, if you take daily medication for a condition like asthma or hypertension, the lack of prescription coverage could result in hundreds or even thousands of dollars in annual expenses. Similarly, if you’re planning to start a family, the exclusion of maternity care could leave you with bills exceeding $10,000 for a standard pregnancy and delivery. Identifying these gaps early can help you decide if supplemental insurance or a more comprehensive plan is necessary.

Another critical aspect to evaluate is the coverage limits for emergency care and hospitalization. While catastrophic plans typically cover these services after the deductible is met, they may impose caps on certain treatments or procedures. For instance, a plan might limit coverage for specialized surgeries or extended hospital stays, leaving you responsible for costs beyond a certain point. To mitigate this risk, compare the plan’s coverage limits to average costs in your area. For example, the average cost of a three-day hospital stay in the U.S. is around $30,000—ensure your plan covers this amount without additional out-of-pocket expenses.

Finally, consider the long-term implications of relying solely on catastrophic insurance. While it may save you money on premiums in the short term, the lack of preventive care coverage can lead to undetected health issues that become costly to treat later. For example, skipping regular screenings for conditions like diabetes or cancer could delay diagnosis and increase treatment complexity. If you’re over 30 or have a family history of serious illnesses, the potential savings from a catastrophic plan may not outweigh the risks. Pairing this type of insurance with a health savings account (HSA) can provide a financial cushion, but it’s essential to contribute regularly to cover unexpected expenses.

In conclusion, catastrophic health insurance can be a viable option if you’re young, healthy, and willing to accept the trade-off of lower premiums for limited coverage. However, carefully assessing the plan’s coverage limits and exclusions is essential to avoid unexpected financial burdens. By evaluating your current health needs, potential future risks, and the specific gaps in catastrophic plans, you can make an informed decision about whether this type of insurance is truly sufficient for your situation.

Malpractice Insurance: Coverage for Lawsuits Filed by Colleagues?

You may want to see also

Explore related products

![]()

Planning for out-of-pocket expenses and savings

Catastrophic health insurance, designed to cover major medical emergencies, leaves policyholders responsible for routine and minor healthcare costs. This gap necessitates proactive planning for out-of-pocket expenses to avoid financial strain. Start by estimating annual healthcare needs based on age, health status, and lifestyle. For instance, a 30-year-old with no chronic conditions might budget $500–$1,000 for check-ups, prescriptions, and unexpected illnesses, while a 50-year-old with diabetes could allocate $2,000–$3,000 for specialist visits, lab tests, and medication. Use past medical expenses as a benchmark, adjusting for inflation and anticipated changes in health.

Next, establish a dedicated health savings account (HSA) or emergency fund to cover these costs. HSAs offer triple tax advantages—contributions are tax-deductible, grow tax-free, and can be withdrawn tax-free for qualified medical expenses. Aim to save at least your annual deductible, typically $7,000–$9,000 for catastrophic plans, to ensure readiness for a major event. Automate contributions by allocating a fixed amount monthly, such as $200–$500, depending on your budget and risk tolerance. For those ineligible for HSAs, a high-yield savings account provides liquidity and modest growth.

Compare costs proactively to minimize out-of-pocket spending. Prescription prices vary widely between pharmacies; tools like GoodRx can save hundreds annually. For procedures, request itemized estimates from multiple providers and negotiate rates, especially for cash payments. For example, an MRI might cost $500 at a freestanding clinic versus $2,000 at a hospital. Similarly, generic medications often cost 80–85% less than brand-name equivalents. These small savings compound over time, reducing the burden on your savings.

Finally, adopt preventive measures to lower healthcare utilization. A $100 annual flu shot reduces the risk of a $3,000 hospitalization. Regular exercise, a balanced diet, and stress management can prevent chronic conditions that drive up costs. For instance, managing blood pressure through lifestyle changes can avert the need for lifelong medication and monitoring. While catastrophic insurance covers emergencies, investing in prevention and cost-conscious habits ensures your savings remain intact for when they’re truly needed.

Explore Medical Insurance Coverage for House Cleaning Services

You may want to see also

Frequently asked questions

Catastrophic health insurance is a low-cost plan designed to cover major medical emergencies, such as accidents or serious illnesses. It typically has high deductibles and limited coverage for routine care, making it unsuitable for regular medical needs.

It can be a good option for young, healthy individuals who rarely need medical care and want to protect against unexpected, high-cost events. However, it’s important to ensure you’re comfortable with limited coverage for routine care.

Generally, catastrophic plans do not cover preventive care or prescriptions unless you’ve met the high deductible. Some plans may cover a few preventive services, but this varies by provider.

Yes, the main downside is the lack of coverage for routine medical needs, which can lead to out-of-pocket expenses for doctor visits, prescriptions, or minor illnesses. It’s best suited for those who prioritize low premiums over comprehensive coverage.