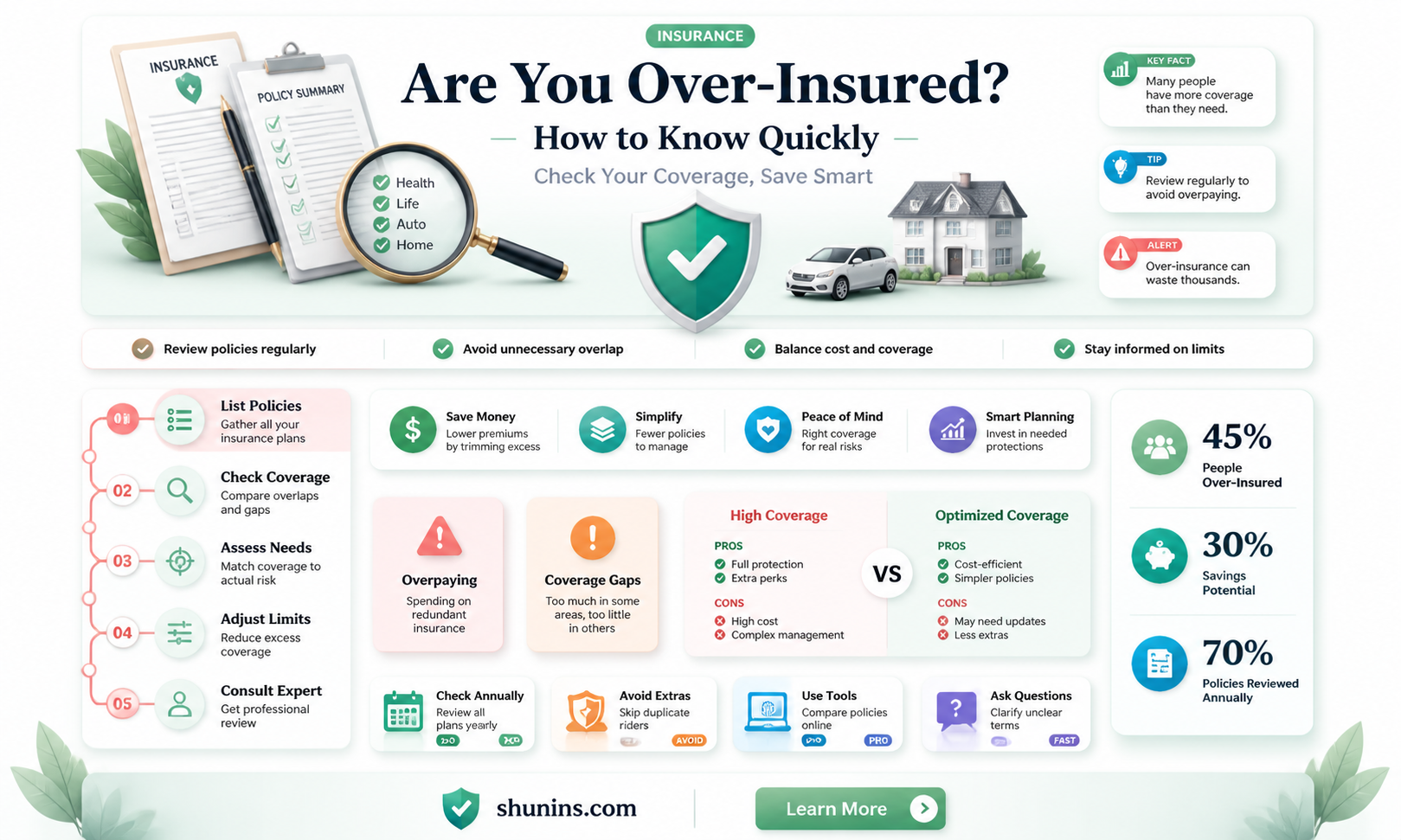

Insurance is a crucial tool to protect against financial uncertainty and unexpected events, but it's possible to have too much of a good thing. Overinsurance refers to having more coverage than you need or can reasonably afford, and it can hinder your financial goals. For example, you may be overinsured if your coverage limits are higher than the actual cash value of your property, or you have policies covering risks you don't face. Being overinsured can result in unnecessary expenses, impacting your ability to save for retirement, pay off debt, or build an emergency fund. To avoid this, it's important to review your policies regularly and consult experts to ensure you have the right amount of coverage for your unique circumstances.

| Characteristics | Values |

|---|---|

| Definition | Overinsurance refers to having more insurance coverage than you need or can reasonably afford. |

| Financial burden | Additional insurance coverage may cause an undue financial burden, hindering financial goals like saving for retirement or paying off debt. |

| Duplicate policies | Having multiple policies that cover the same thing leads to wasted money. |

| Unnecessary coverage | You may have coverage for risks you don't face or types of coverage you don't need. |

| Excessive policy amounts | Your coverage limits may be higher than the actual cash value of your property. |

| Overlapping coverage | You may have overlapping coverage if you switch insurance companies before your old coverage ends. |

| Premium costs | Being over-insured may lead to higher premium costs that work against your financial health. |

Explore related products

What You'll Learn

![]()

Review your insurance policies

Reviewing your insurance policies is a crucial step in ensuring you are not overinsured. Here are some detailed instructions to guide you through the process:

Firstly, understand your individual circumstances and protection needs. Evaluate your current financial situation, including your income, debts, and expenses. Consider your assets, such as your home, car, and any other valuable possessions. Assess your lifestyle, family situation, and health status. By comprehending your unique context, you can tailor your insurance coverage accordingly.

Next, carefully review your existing insurance policies. Gather all your policy documents and scrutinize the coverage details. Identify the types of insurance you have, such as auto, home, health, and life insurance. Examine the policy amounts, premiums, deductibles, and covered risks. Look out for any unnecessary expenses or overlapping coverage. For instance, you may have added ride-sharing coverage to your car insurance policy when you don't work for a ride-sharing service. Be vigilant about canceling redundant policies, especially when switching insurance providers, to avoid paying for duplicate coverage.

Additionally, pay attention to the specific terms and conditions of your policies. Check if there are any optional coverages that may not be relevant to your situation. For example, if you live in a low-risk flood area, separate flood insurance may be unnecessary. Ensure your home insurance is based on the replacement cost rather than the market value of your home, as the latter often includes the value of the land, which is irrelevant to the cost of rebuilding the structure.

Periodically reevaluate your coverage needs, especially after significant life events such as marriage, the birth of a child, purchasing a new home, or a change in your health status. Adjust your policies and coverage limits as necessary to align with your evolving circumstances.

If you are unsure about properly analyzing your policies, consider consulting an independent insurance agent or a financial advisor. They can provide expert guidance in determining your insurance needs and help you make informed decisions about adjusting your coverage.

Remember, the goal is to strike a balance between having sufficient insurance protection and avoiding unnecessary costs associated with being overinsured. By regularly reviewing and adjusting your policies, you can optimize your coverage and make your insurance work for you.

Life Insurance Certification: What's Needed to Sell?

You may want to see also

Explore related products

![]()

Calculate how much life insurance you need

While insurance is a crucial tool to prevent a financial crisis in the event of a costly, unexpected event, it is possible to have too much coverage, which can hinder your financial goals. Being overinsured means you have more insurance than you need or can afford. This may manifest as excessive policy amounts, unnecessary coverage, duplicate policies, or coverage that far exceeds the cost of a potential loss.

To calculate how much life insurance you need, you can use a life insurance calculator, which takes your marital status, age, life stage, existing assets, debts, and other factors into account to estimate how much insurance you may need to help your family meet their financial goals.

- Add up your outstanding debts, including your auto loan, mortgage, and personal loans.

- Estimate how much replacement income is needed. Your survivors will likely need to replace your income if you die, but the required amount can vary depending on your personal situation. One way to do this is to multiply your annual income by the number of years you want to replace that income.

- Consider any future needs such as college fees and funeral costs.

- The ""10 times income" guideline is often suggested, which involves multiplying your annual income by 10. However, this method does not take into account your family's specific needs, savings, or existing life insurance policies.

- Another method is to divide your annual income by a conservative rate of return, such as 4% or 5%. For example, if your income is $50,000 and you estimate a 5% rate of return, you would get $1 million.

- If you need help, consider consulting a life insurance agent or financial advisor, who can help you assess your situation and determine the appropriate type and level of coverage.

Selling Life Insurance: An Uphill Battle?

You may want to see also

Explore related products

![]()

Understand the cost of being over-insured

While insurance is a crucial tool to protect against financial uncertainty, having too much coverage can hinder your financial goals. Being over-insured means you have more insurance than you need or can afford. This can result in you spending more than necessary on insurance, which means you're losing money that could be spent on other things.

There are several ways you can be over-insured. You might have duplicate or overlapping insurance policies, coverage you don't need, or policies that cover much more than the cost of a potential loss. For example, you might have auto insurance for every conceivable hazard but no life insurance or dental insurance. You could also be paying so much for insurance that you're unable to meet other financial obligations, such as saving for retirement or paying off debt.

To determine if you're over-insured, review your auto, home, health, and life insurance policies, as well as any other coverage you have. Look at policy amounts, premiums, and covered risks to decide if your coverage is adequate or excessive. Coverage amounts should be based on need. For example, if you live in an area with a low risk of flooding, it may be unnecessary to have a separate flood insurance policy.

If you find that you are over-insured, there are several ways to reduce your coverage and save on costs. You can adjust your coverage by reducing policy amounts, cancelling unnecessary policies, and cutting redundant coverage. You can also shop around and compare rates from different insurers to get the best rates for the coverage you need. Additionally, increasing your deductible can result in lower premiums, but ensure that you can pay the increased deductible if you need to file a claim.

Life Insurance: Is It Really That Hard to Get?

You may want to see also

Explore related products

![]()

Identify unnecessary expenses or overlap in coverage

Overlapping insurance coverage can result in paying for coverage that is unnecessary and can be a financial burden. It is important to identify and address any unnecessary expenses or overlaps in your insurance coverage to ensure you are not overinsured. Here are some ways to identify and manage these situations:

Review Policy Terms

Carefully review the terms, conditions, and coverage provided by each of your insurance policies. Understand the coverage details, limits, exclusions, and types of coverage provided, as well as the vehicles and individuals covered. This will help you identify any potential areas of overlap or duplication. For example, you may have added rideshare coverage to your car insurance policy, but if you don't work for a rideshare service, this type of coverage may be unnecessary.

Evaluate Costs and Coverage Adequacy

Assess the premiums and costs associated with each policy. Determine if the added coverage justifies the additional expense. Consider whether the coverage limits and benefits provided by your primary policy are sufficient for your needs. If the coverage is adequate and meets your requirements, then overlapping coverage may be unnecessary.

Communicate with Insurance Providers

Reach out and communicate with your insurance providers to clarify any questions or concerns about coverage. Discuss potential overlaps and conflicts to gain a better understanding of how the policies will interact in the event of a claim. They can help assess your coverage and recommend the best course of action, such as adjusting coverage limits or dropping redundant policies.

Choose Comprehensive Plans

Consider selecting comprehensive insurance plans that consolidate coverage, reducing the need for multiple policies. Having one clear source of coverage avoids confusion during claims processing and ensures you can confidently rely on your warranty plan.

Understand Exclusions and Limitations

Carefully read and understand the fine print of your insurance policies to identify any exclusions or limitations. Paying for multiple plans without additional benefits can increase costs unnecessarily. Review your policies regularly and adjust them as your life circumstances change to avoid being overinsured or underinsured.

By following these steps, you can identify and manage unnecessary expenses or overlaps in your insurance coverage, ensuring that your insurance policies meet your coverage needs in a cost-effective manner.

Celiac Disease: Life Insurance Impact and Exclusions

You may want to see also

Explore related products

![]()

Adjust your coverage

You can also adjust your coverage by reducing policy amounts, cancelling unnecessary policies, and cutting redundant coverage. For example, if you have an optional coverage that you likely won't need, such as separate flood insurance if you live in a low-risk flood area, it may not be worth the added cost. Similarly, if your home insurance policy includes every endorsement your insurance company offers but costs so much that you decide to forgo car insurance, you may be driving in violation of your state's laws and going without adequate coverage.

Additionally, you can adjust your coverage by shopping around for different insurance providers and comparing rates to get the best value for the coverage you need. Policy prices can fluctuate frequently, so it's important to compare rates from different insurers every six months or when your situation changes. You can also increase your deductible, which can result in lower premiums, but ensure that you can pay for the increased deductible if you need to file a claim.

Consider consulting an independent insurance agent or financial advisor if you need help determining your insurance needs and purchasing adequate coverage for your situation. They can help you identify any unnecessary expenses or overlaps in your coverage and make sure your coverage amounts are based on your needs and individual circumstances.

Globe Insurance: Term Life Insurance Options and Availability

You may want to see also

Frequently asked questions

Being over-insured means having more insurance than you need or can afford. This may hinder your financial goals and result in you spending more than you need to.

Review your insurance policies carefully and look out for duplicate or overlapping policies, coverage you don't need, or policies that cover more than the cost of a potential loss.

If your insurance coverage and riders are causing an undue financial burden, you may be over-insured. This could be hindering your ability to save for retirement or pay off debts.

You could reduce your coverage, cancel unnecessary policies, or cut redundant coverage. You could also shop around for better rates or increase your deductible.

Understand your individual circumstances and protection needs. Review your policies periodically and adjust them as your situation changes. Consult an independent insurance agent or financial advisor if needed.

![Iron Deficiency Test Kit [2 Tests] – Ferritin Anemia Home Test Kit for Iron Level Detection in 15 Minutes – Convenient Home Test for Adults & Children](https://m.media-amazon.com/images/I/61fJKKuVHuL._AC_UL320_.jpg)