Navigating the complexities of health insurance after remarriage can be overwhelming, especially when it involves your new spouse’s children. Whether you are responsible for their health insurance depends on several factors, including legal custody arrangements, your spouse’s financial situation, and the terms of your marriage or prenuptial agreement. In many cases, the biological or custodial parent is primarily responsible for providing health insurance for their children, but remarriage may introduce new obligations or opportunities to include stepchildren in your family coverage. It’s essential to review your employer’s health insurance policy, consult with a legal professional, and communicate openly with your spouse to ensure compliance with legal requirements and to make informed decisions that prioritize the well-being of the children involved.

| Characteristics | Values |

|---|---|

| Legal Responsibility | Generally, you are not legally obligated to provide health insurance for your stepchildren unless you legally adopt them. |

| State Variations | Some states may have specific laws or court rulings that could influence responsibility, especially in cases of divorce or child support agreements. |

| Voluntary Coverage | You can choose to add your stepchildren to your health insurance plan if your policy allows it, but this is not mandatory. |

| Employer Policies | Many employer-sponsored health plans allow coverage for stepchildren, but this depends on the specific plan and employer policies. |

| Cost Implications | Adding stepchildren to your insurance may increase premiums, deductibles, and out-of-pocket costs. |

| Alternative Options | Stepchildren may be eligible for coverage under their other parent’s insurance, Medicaid, CHIP (Children’s Health Insurance Program), or other state-sponsored programs. |

| Legal Adoption | If you legally adopt your stepchildren, you become fully responsible for their health insurance as their legal parent. |

| Divorce Agreements | Court-ordered divorce agreements may require one or both parents to provide health insurance for the children, which could impact your responsibility. |

| Tax Implications | Providing health insurance for stepchildren may offer tax benefits, such as claiming them as dependents if certain criteria are met. |

| Policy Exclusions | Some insurance policies may exclude stepchildren unless they are legally adopted or specifically added to the plan. |

Explore related products

What You'll Learn

- Legal obligations for stepparent coverage under health insurance policies

- Existing health insurance plans and stepchild inclusion rules

- Financial responsibility for stepchildren’s medical expenses

- State laws affecting stepparent health insurance requirements

- Alternatives to providing health insurance for stepchildren

![]()

Legal obligations for stepparent coverage under health insurance policies

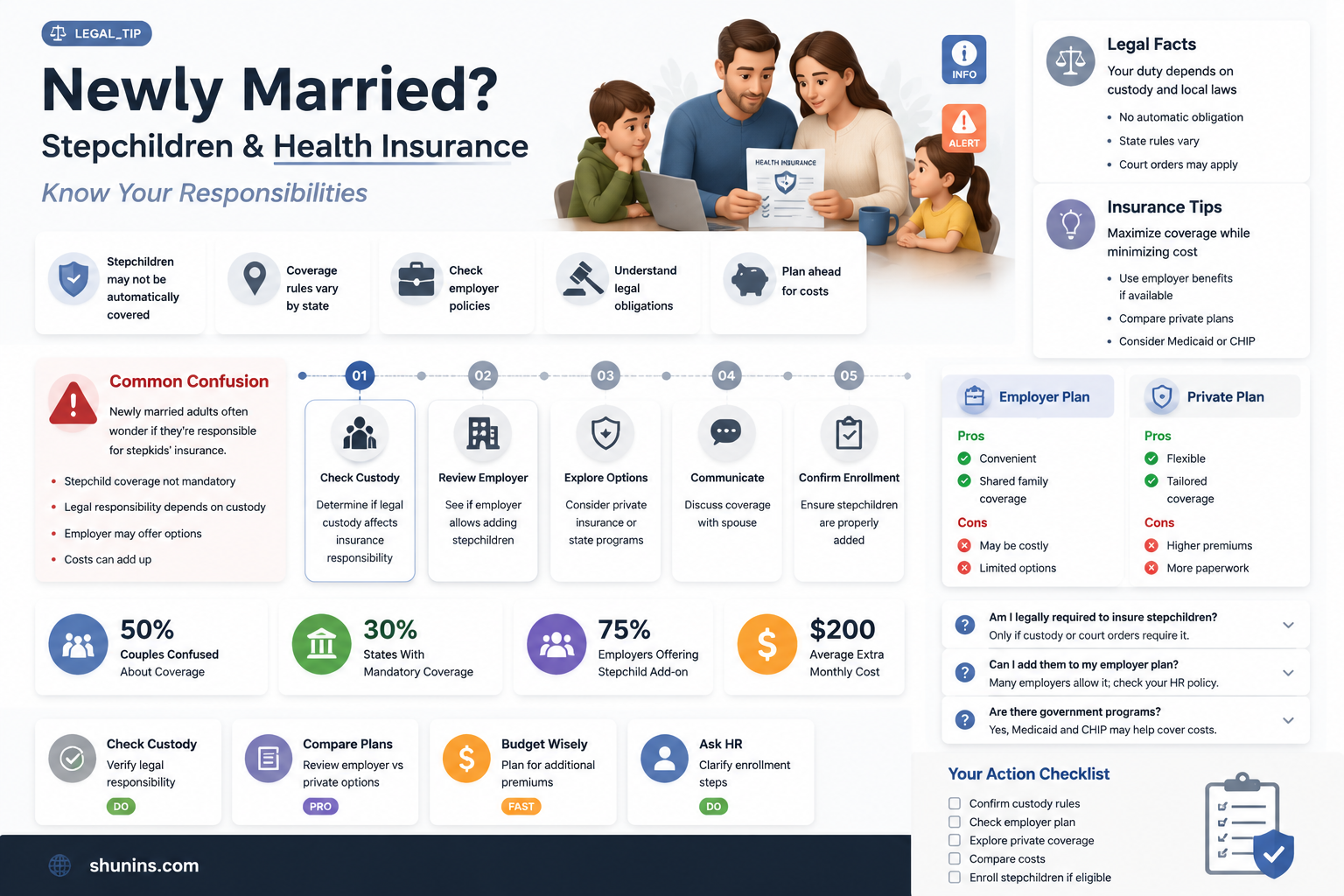

Stepparents often wonder about their legal obligations to provide health insurance for their new spouse's children. The answer is not straightforward, as it depends on various factors, including state laws, the terms of the insurance policy, and existing custody agreements. In most cases, stepparents are not automatically legally responsible for their stepchildren's health insurance. However, certain circumstances may require them to contribute to coverage.

Understanding Legal Requirements

In the United States, the Affordable Care Act (ACA) mandates that employers offering health insurance must allow employees to cover their spouse's children if the employee is legally responsible for them. However, "legally responsible" is a key term. This typically means the stepparent has formally adopted the child or a court has ordered them to provide support. Absent these conditions, the obligation falls primarily on the biological parents. For instance, if the non-custodial parent is required to provide insurance through a divorce decree, the stepparent is generally not obligated unless they voluntarily agree to do so.

Policy Variations and Practical Considerations

Health insurance policies vary widely in their treatment of stepchildren. Some plans automatically include stepchildren as dependents if the stepparent is the policyholder, while others require proof of legal responsibility. It’s crucial to review your policy’s specific terms. For example, if your employer-sponsored plan allows stepchild coverage, you may choose to add them voluntarily, even if not legally required. This can simplify logistics and ensure continuous care, especially if the other parent’s coverage is unreliable.

State-Specific Nuances

State laws play a significant role in determining stepparent obligations. In some states, such as California, stepparents may be held financially responsible for stepchildren if they have taken them into their home and held them out as their own. Other states, like Texas, require a formal adoption or court order before imposing such obligations. Always consult local family law statutes or an attorney to understand your jurisdiction’s stance.

Strategic Decision-Making

If you’re considering adding your stepchildren to your health insurance, weigh the costs against the benefits. Premiums for additional dependents can be substantial, but the coverage may be more comprehensive or stable than what’s available through the other parent’s plan. Additionally, voluntarily providing insurance can strengthen family relationships and ensure the children’s well-being. However, avoid making verbal agreements without formal documentation, as this can lead to legal complications later.

In summary, while stepparents are generally not legally obligated to provide health insurance for their stepchildren, exceptions exist based on adoption, court orders, or state laws. Understanding your policy’s terms and local regulations is essential for making informed decisions. Whether you choose to cover your stepchildren or not, clarity and compliance with legal requirements will protect all parties involved.

Accident Insurance: Student Safety Net

You may want to see also

Explore related products

![]()

Existing health insurance plans and stepchild inclusion rules

Stepchild inclusion in existing health insurance plans hinges on the specific terms of your policy and the legal framework governing family coverage. Most employer-sponsored group health plans allow for the addition of stepchildren as dependents, but this is not automatic. You must actively update your plan during open enrollment or within a qualifying life event period, such as marriage. Failure to do so may leave your stepchildren uninsured until the next enrollment window, exposing them to gaps in coverage.

The Affordable Care Act (ACA) mandates that children under 26 can remain on their parent’s health insurance, but this does not automatically extend to stepchildren. Instead, it depends on whether your plan explicitly defines stepchildren as eligible dependents. Individual market plans often mirror employer-sponsored plans in this regard, but some may have stricter eligibility criteria. Always review your policy’s definition of "dependent" to ensure compliance and avoid unexpected denials of coverage.

Adding stepchildren to your plan may increase premiums, but this cost is often offset by the financial security of comprehensive coverage. Some plans require proof of legal guardianship or marriage certificates to verify eligibility, so have these documents ready when applying. If your plan excludes stepchildren, consider alternative options like enrolling them in a state-sponsored program (e.g., CHIP) or purchasing individual coverage through the ACA marketplace.

A practical tip: Coordinate with your spouse to determine the most cost-effective coverage option. For instance, if your spouse’s employer offers better benefits for dependents, it may be more advantageous to enroll the children under their plan. Conversely, if your plan provides broader coverage or lower premiums, take the lead in updating your policy. Communication and careful comparison are key to avoiding duplication or gaps in coverage.

In conclusion, stepchild inclusion in existing health insurance plans is not guaranteed but is often feasible with proper action. Review your policy, understand its dependent eligibility rules, and act promptly during open enrollment or qualifying life events. By taking these steps, you can ensure your stepchildren receive the coverage they need while navigating the complexities of family health insurance.

Discovering Canada's Top Insurance Giant: Who Leads the Market?

You may want to see also

Explore related products

![]()

Financial responsibility for stepchildren’s medical expenses

Marrying someone with children brings a host of new financial considerations, and health insurance for stepchildren is a complex one. Legally, you are not automatically responsible for your stepchildren's medical expenses simply by marrying their parent. Parenthood, not marriage, establishes legal financial obligation for a child's healthcare. However, your involvement in their lives and your desire to contribute to their well-being might lead you to want to provide coverage.

Understanding the legal landscape is crucial. In most cases, the biological parent remains primarily responsible for securing health insurance for their children. This is typically outlined in divorce decrees or child custody agreements. These documents often specify which parent is responsible for providing health insurance and how uncovered medical expenses are shared.

There are scenarios where you might choose to include your stepchildren on your health insurance plan. If your employer offers dependent coverage and your spouse's plan is inadequate or unavailable, adding them to yours could be a practical solution. This decision should be made in consultation with your spouse, considering factors like premiums, deductibles, and the specific needs of the children.

Some couples opt for a blended approach. The biological parent might maintain primary coverage while the stepparent contributes to premiums or out-of-pocket costs. This arrangement requires clear communication and a written agreement to avoid misunderstandings.

It's important to remember that even if you're not legally obligated, contributing to your stepchildren's healthcare demonstrates commitment to your new family. Open communication with your spouse, a thorough understanding of legal agreements, and careful consideration of your financial situation are key to navigating this aspect of stepparenting successfully.

Eye Exam Coverage: Medical Insurance's Visionary Move

You may want to see also

Explore related products

![]()

State laws affecting stepparent health insurance requirements

Stepparent health insurance obligations vary widely by state, making it crucial to understand local laws before assuming or denying responsibility. Some states, like California, mandate that stepparents provide health insurance for stepchildren if the biological parent is unable to do so. This requirement often hinges on the stepparent’s legal status as a "responsible party" under state family law. For instance, if a stepparent adopts the child or is granted legal guardianship, insurance coverage becomes a legal duty. Conversely, states like Texas may not impose such obligations unless the stepparent formally adopts the child or agrees to financial responsibility in writing. Always consult state statutes or a family law attorney to clarify your specific obligations.

In states with no explicit stepparent insurance mandates, courts may still order coverage based on the child’s best interests. For example, in New York, judges have discretion to require stepparents to contribute to health insurance costs if the biological parent’s income is insufficient. This decision often considers factors like the stepparent’s income, the child’s medical needs, and the duration of the marriage. To avoid surprises, stepparents should review prenuptial or postnuptial agreements to address potential financial responsibilities. Proactively discussing these issues with your spouse and documenting agreements can prevent legal disputes later.

Employer-sponsored health insurance plans further complicate state requirements. Federal law, specifically the Employee Retirement Income Security Act (ERISA), often preempts state laws, meaning your employer’s policy may dictate whether stepchildren can be added to your plan. However, some states, like Illinois, require employers to offer coverage to stepchildren if the plan covers dependents. Check your employer’s policy and state insurance regulations to determine eligibility. If your plan excludes stepchildren, explore alternatives like state-sponsored programs (e.g., CHIP) or private insurance options.

Stepparents in states with community property laws, such as Arizona or Washington, may face unique challenges. In these states, income earned during the marriage is considered jointly owned, which could influence a court’s decision on insurance responsibility. For instance, if a stepparent’s income significantly contributes to the household, a judge might require them to provide health insurance for stepchildren, even without formal adoption. Understanding your state’s property laws and their implications for financial obligations is essential for navigating this complex landscape.

Finally, stepparents should be aware of the emotional and financial implications of voluntarily providing health insurance. While not legally required in some states, covering stepchildren can strengthen family bonds and ensure their well-being. However, this decision should be made after careful consideration of long-term costs and legal advice. Voluntary coverage does not automatically confer legal responsibility, but it could be factored into future court decisions if disputes arise. Balancing compassion with practicality is key to making an informed choice.

Unemployed and Uninsured: Getting Medical Insurance Coverage

You may want to see also

Explore related products

![]()

Alternatives to providing health insurance for stepchildren

Stepparenthood often blurs financial boundaries, especially regarding health insurance for stepchildren. While legal responsibility typically rests with the biological parents, stepparents may seek alternatives to ensure their stepchildren’s well-being without directly providing insurance. One immediate option is to explore government-sponsored programs like Medicaid or the Children’s Health Insurance Program (CHIP), which offer low-cost or free coverage based on household income. Eligibility varies by state, but these programs often extend to children in blended families, provided the household meets income thresholds. For instance, a family of four earning up to $53,000 annually may qualify for CHIP in some states, though exact limits differ.

Another strategic alternative involves negotiating with the child’s other biological parent to maintain or increase their contribution to health insurance. This requires clear communication and, in some cases, legal mediation to ensure fairness. For example, if the custodial parent’s employer-sponsored plan is insufficient, the non-custodial parent could be compelled to provide additional coverage through their own employer or private insurance. Documentation of such agreements in a parenting plan or court order ensures accountability and avoids future disputes.

Health savings accounts (HSAs) or flexible spending accounts (FSAs) offer a third avenue, particularly if the stepparent’s employer provides these options. By allocating pre-tax dollars to cover medical expenses, stepparents can contribute financially without directly providing insurance. For instance, an HSA allows contributions of up to $3,850 annually for individuals or $7,750 for families in 2023, with funds rolling over if unused. This approach requires careful budgeting but provides flexibility for unexpected medical costs.

Lastly, community health clinics and nonprofit organizations often provide low-cost or sliding-scale healthcare services for uninsured children. Organizations like the National Association of Free & Charitable Clinics (NAFC) operate over 1,400 clinics nationwide, offering primary care, dental services, and prescriptions at reduced rates. While not a replacement for comprehensive insurance, these resources can bridge gaps in coverage, particularly for routine care. Combining these alternatives—government programs, shared parental responsibility, financial tools, and community resources—creates a safety net that prioritizes stepchildren’s health without placing the entire burden on the stepparent.

RV Medical Emergencies: Is COBRA Insurance Necessary?

You may want to see also

Frequently asked questions

Generally, you are not legally obligated to provide health insurance for your stepchildren unless you legally adopt them or a court orders you to do so. However, it’s a good idea to check local laws and any prenuptial or postnuptial agreements.

Many employer-sponsored health insurance plans allow coverage for stepchildren. Check with your employer’s HR department or insurance provider to confirm eligibility and enrollment requirements.

Unless a court orders you to provide insurance, you are not legally responsible. However, if your spouse is unable to secure coverage, you may choose to add the children to your plan voluntarily.

Adding dependents to your health insurance plan will likely increase your premiums. The exact amount depends on your plan and insurer. Contact your insurance provider for a cost estimate.

If you divorce, you are no longer responsible for your ex-spouse’s children’s health insurance unless a court orders otherwise. However, if you legally adopted the children, your obligations may differ. Consult a family law attorney for specific guidance.