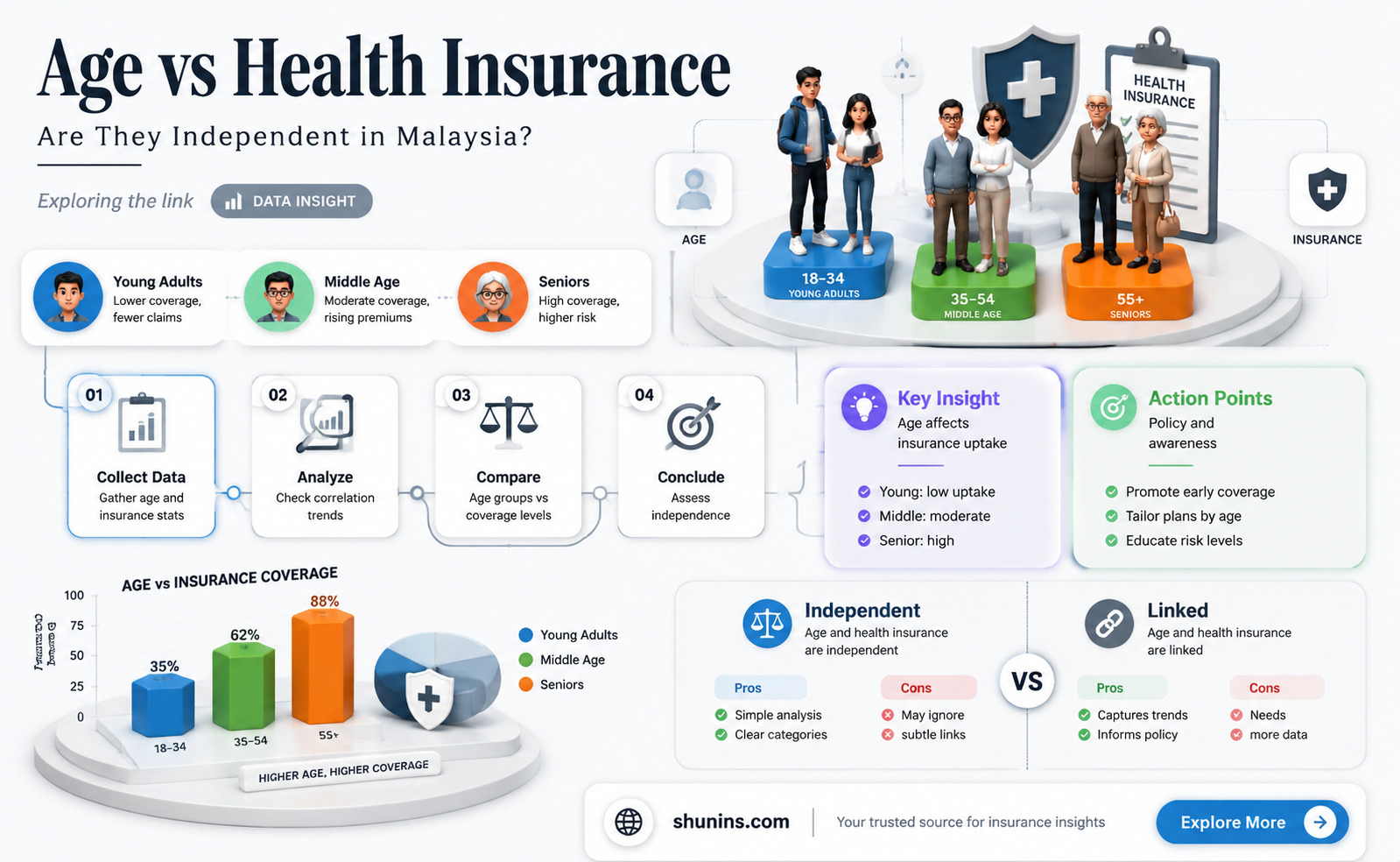

In Malaysia, the relationship between age and health insurance is a topic of significant interest, particularly in understanding whether these two factors operate as independent variables. Age is often considered a critical determinant in health insurance policies, influencing premiums, coverage options, and eligibility criteria. As individuals grow older, they typically face higher health risks, which insurers account for by adjusting costs or benefits. However, the question arises whether age alone dictates health insurance outcomes or if other factors, such as lifestyle, pre-existing conditions, or government policies, play a more substantial role in shaping insurance dynamics. Examining this independence is crucial for policymakers, insurers, and consumers to ensure equitable and accessible healthcare coverage across all age groups in Malaysia.

| Characteristics | Values |

|---|---|

| Relationship Between Age and Health Insurance | Not strictly independent; age is a significant factor influencing health insurance premiums and coverage in Malaysia. |

| Premium Calculation | Premiums increase with age due to higher perceived health risks and potential medical costs. |

| Coverage Limitations | Older individuals may face restrictions on coverage, higher deductibles, or exclusions for pre-existing conditions. |

| Government Schemes | Malaysia’s public healthcare system (e.g., MySalam, PEKA B40) provides coverage regardless of age, but private insurance often differentiates based on age. |

| Private Insurance Trends | Private insurers use age as a key variable in underwriting and pricing policies. |

| Age-Based Policies | Some insurers offer age-specific plans (e.g., senior citizen plans) with tailored benefits. |

| Regulatory Environment | Bank Negara Malaysia (BNM) regulates health insurance, allowing age-based pricing but ensuring fairness and transparency. |

| Market Data (2023) | Average premium increases by 5-10% annually for individuals aged 40 and above in private health insurance plans. |

| Consumer Behavior | Younger individuals are more likely to opt for basic plans, while older individuals seek comprehensive coverage. |

| Health Risk Factors | Age correlates with increased health risks, influencing insurance providers’ assessments. |

Explore related products

What You'll Learn

![]()

Age-based health insurance premiums in Malaysia

In Malaysia, health insurance premiums are intricately tied to age, reflecting a global trend where insurers assess risk based on demographic factors. As individuals age, their health risks generally increase, leading to higher medical claims. Malaysian insurers, like their international counterparts, use actuarial data to price policies, ensuring that premiums align with the anticipated healthcare costs of different age groups. For instance, a 25-year-old might pay RM500 annually for a basic health plan, while a 55-year-old could face premiums exceeding RM2,000 for similar coverage. This age-based pricing model is not arbitrary but a calculated response to statistical trends in healthcare utilization.

The age-based premium structure in Malaysia is further complicated by the country’s aging population. By 2030, Malaysia is projected to become an aged nation, with 15% of its population over 60. This demographic shift places additional strain on the healthcare system, prompting insurers to adjust premiums to remain financially viable. However, this model raises concerns about affordability for older adults, who often have fixed incomes but greater health needs. For example, a retiree on a pension might struggle to afford premiums that increase exponentially with age, potentially leaving them underinsured or uninsured.

To mitigate the impact of age-based premiums, Malaysian insurers offer tiered plans with varying levels of coverage. Younger individuals can opt for basic plans with lower premiums, while older adults may choose comprehensive plans that include critical illness coverage or hospitalization benefits. Additionally, some insurers provide discounts or loyalty bonuses for long-term policyholders, softening the premium increases over time. Practical tips for Malaysians include purchasing health insurance early in life to lock in lower rates and regularly reviewing policies to ensure they remain cost-effective as health needs evolve.

A comparative analysis reveals that Malaysia’s approach to age-based premiums is similar to countries like Singapore and Australia, where risk-based pricing is standard. However, Malaysia’s unique challenge lies in balancing affordability with sustainability, particularly as healthcare costs rise. The government has introduced initiatives like the *Perbadanan Takaful Malaysia* and tax incentives for medical insurance to encourage uptake, but more targeted solutions are needed for older adults. For instance, a community-based health insurance model or government subsidies could alleviate the financial burden on this demographic.

In conclusion, age-based health insurance premiums in Malaysia are a reflection of broader demographic and economic trends. While this model ensures insurers remain solvent, it poses challenges for older adults who face higher costs at a time when they need coverage most. By understanding the factors driving premium increases and exploring alternative solutions, Malaysians can navigate this complex landscape more effectively. Early planning, regular policy reviews, and advocacy for inclusive insurance policies are essential steps toward achieving affordable healthcare for all age groups.

The Dark Side of Employment: No Medical Insurance

You may want to see also

Explore related products

![]()

Health insurance coverage trends across age groups

In Malaysia, health insurance coverage varies significantly across age groups, reflecting both individual priorities and systemic factors. Younger adults aged 20-35 typically exhibit lower coverage rates, often due to perceived good health and competing financial demands like education loans or housing. This demographic tends to rely on employer-provided insurance or government schemes, with only 30% purchasing standalone policies. In contrast, the 36-50 age group shows a sharp increase in coverage, driven by growing health awareness and family responsibilities. Here, 60% of individuals hold comprehensive health insurance, frequently opting for riders like critical illness or hospitalization benefits.

Analyzing the 51-65 age bracket reveals a paradox. Despite higher health risks, coverage rates plateau at around 55%, as insurers impose stricter underwriting criteria and higher premiums. Seniors over 65 face even greater challenges, with only 40% insured, largely due to pre-existing conditions and limited product availability. Government initiatives like the *MySalam* scheme partially address this gap, but private insurance remains inaccessible for many. This trend underscores the need for age-specific policy interventions, such as subsidized premiums or mandatory coverage for employers.

A comparative analysis highlights the role of income and education in shaping these trends. Higher-income groups across all ages are more likely to purchase insurance, while lower-income individuals rely heavily on public healthcare. For instance, 70% of Malaysians earning above RM10,000 monthly have private insurance, compared to 20% in the RM3,000-RM5,000 bracket. Education also correlates with coverage: university graduates are twice as likely to be insured as those with secondary education. This disparity suggests that financial literacy and access to information are critical determinants of insurance uptake.

To bridge these gaps, practical steps can be taken. Employers can offer tiered insurance plans catering to different age groups, with younger employees receiving basic coverage and older workers accessing enhanced benefits. Policymakers should incentivize insurers to develop affordable, age-specific products, possibly through tax breaks or public-private partnerships. Individuals can proactively assess their needs using online tools like the *Health Insurance Needs Calculator* provided by the Malaysian Takaful Association. For seniors, exploring community-based health programs or joining associations that negotiate group insurance rates can be viable alternatives.

Ultimately, understanding these trends is key to fostering inclusive health insurance coverage in Malaysia. By addressing age-related barriers through targeted policies, employer initiatives, and individual action, the nation can move toward a system where health protection is not a privilege but a universal right. Age and health insurance may not be entirely independent variables, but with strategic interventions, their interdependence can be managed to benefit all Malaysians.

Medicare and ACA Insurance: What's the Difference?

You may want to see also

Explore related products

![]()

Impact of age on policy exclusions in Malaysia

In Malaysia, age significantly influences health insurance policy exclusions, often dictating what is covered and what is not. Insurers categorize policyholders into age groups—typically young adults (18–35), middle-aged (36–55), and seniors (56 and above)—to assess risk and tailor exclusions accordingly. For instance, seniors may face exclusions for pre-existing conditions like hypertension or diabetes, while younger policyholders might encounter limitations on maternity coverage if they are below a certain age. This age-based stratification reflects the industry’s effort to balance risk with affordability, but it also highlights the need for consumers to scrutinize policies closely.

Consider the practical implications for someone aged 60 applying for health insurance in Malaysia. They are likely to encounter higher premiums and more stringent exclusions, such as limited coverage for chronic illnesses or critical care. Insurers justify this by citing higher healthcare utilization rates among older adults, but it leaves seniors vulnerable to out-of-pocket expenses. To mitigate this, seniors should seek policies with riders that specifically address age-related exclusions, such as add-ons for chronic disease management or senior care packages. Additionally, comparing policies from multiple providers can reveal variations in exclusions, offering a chance to find more inclusive coverage.

From a persuasive standpoint, age-based exclusions in Malaysian health insurance policies underscore the importance of early planning. Young adults often delay purchasing comprehensive health insurance, assuming they are invincible to age-related health issues. However, starting early not only locks in lower premiums but also minimizes the risk of accumulating exclusions as they age. For example, a 25-year-old who secures a policy with maternity and chronic illness coverage will retain these benefits as they grow older, whereas a 45-year-old applying for the first time may face exclusions for the same conditions. This proactive approach ensures long-term financial security and peace of mind.

A comparative analysis reveals that while age-based exclusions are common globally, Malaysia’s regulatory environment offers some protections. The country’s Health Insurance Association (HIAM) mandates transparency in policy terms, requiring insurers to clearly outline age-related exclusions. This contrasts with markets like the U.S., where exclusions can be more opaque. However, Malaysian consumers must still navigate these terms carefully. For instance, a policy might exclude coverage for joint replacement surgery for those over 65, but another might offer partial coverage with a higher deductible. Understanding these nuances empowers consumers to make informed decisions and advocate for their needs.

In conclusion, age is far from an independent variable in Malaysia’s health insurance landscape—it is a pivotal factor shaping policy exclusions. By understanding how age categories influence coverage, consumers can take strategic steps to secure comprehensive protection. Whether through early planning, careful policy comparison, or leveraging regulatory safeguards, Malaysians can navigate age-based exclusions effectively. This knowledge not only ensures better health outcomes but also fosters financial resilience in the face of evolving healthcare needs.

Small Business, Big Costs: Understanding High Insurance Expenses for Employees

You may want to see also

Explore related products

![]()

Age-related claims frequency in Malaysian health insurance

In Malaysia, the relationship between age and health insurance claims frequency is a critical factor for insurers and policyholders alike. Data from the Malaysian Health Insurance Association (MHIA) reveals a clear trend: claims frequency increases significantly with age. For instance, individuals aged 50 and above file claims at a rate nearly three times higher than those in their 30s. This pattern underscores the importance of understanding age as a determinant in health insurance dynamics.

Analyzing the claims data further, it becomes evident that the type of claims also varies by age group. Younger policyholders (20–35 years) tend to file claims for outpatient treatments, such as minor surgeries or consultations, while older policyholders (60+ years) are more likely to claim for chronic conditions like diabetes, hypertension, and cardiovascular diseases. Insurers often adjust premiums based on these age-related claim patterns, reflecting the higher risk associated with older age groups. For policyholders, this means that premiums may increase substantially as they transition into higher age brackets.

To mitigate the financial impact of age-related claims, Malaysian insurers have introduced tiered pricing models and wellness programs. For example, some policies offer discounted premiums for policyholders who maintain a healthy lifestyle, as evidenced by regular health screenings or participation in fitness programs. Additionally, critical illness riders are often marketed to older individuals to provide additional coverage for age-related diseases. Policyholders should carefully review these options to ensure their coverage aligns with their health needs as they age.

A comparative analysis of Malaysian health insurance policies highlights the need for transparency in age-related pricing. Unlike some countries where age-based premiums are capped, Malaysia allows insurers to adjust premiums annually based on age and claims history. This flexibility can lead to unexpected premium hikes for older policyholders. To navigate this, individuals should consider long-term care plans or government-subsidized health schemes like MySalam, which offer more predictable coverage for age-related health issues.

In conclusion, age-related claims frequency in Malaysian health insurance is not just a statistical observation but a practical consideration for both insurers and policyholders. By understanding these trends and exploring tailored solutions, individuals can better prepare for the financial implications of aging while ensuring adequate health coverage. Insurers, on the other hand, must balance risk with affordability to maintain a sustainable and inclusive health insurance ecosystem.

Does Health Insurance Cover Gym Memberships? What You Need to Know

You may want to see also

Explore related products

![]()

Regulatory policies on age and health insurance in Malaysia

In Malaysia, regulatory policies on age and health insurance are designed to balance accessibility and sustainability, reflecting the nation’s aging population and rising healthcare costs. The *Health Insurance Association of Malaysia* (PIAM) and the *Ministry of Health* have implemented frameworks that explicitly link age to premium rates and coverage limits. For instance, individuals aged 50 and above often face higher premiums due to increased health risks, while those under 40 may access more affordable plans with broader benefits. This age-based stratification is not arbitrary but rooted in actuarial data, ensuring insurers remain solvent while providing coverage to a diverse demographic.

One critical policy is the *Lifetime Limit for Critical Illness Coverage*, which caps payouts based on age at purchase. For example, a 30-year-old buying a policy with a RM1 million limit may retain it until age 70, whereas a 50-year-old might face a reduced limit of RM500,000. This policy incentivizes early enrollment and mitigates insurer risk from late-entry, high-risk individuals. Additionally, the *Senior Citizens Act 2008* mandates discounts of up to 30% on healthcare services for those aged 60 and above, indirectly influencing insurance pricing by reducing out-of-pocket expenses for seniors.

A comparative analysis reveals Malaysia’s approach differs from countries like the UK, where age-based discrimination in insurance is prohibited under equality laws. In contrast, Malaysia’s regulatory framework acknowledges age as a determinant of risk, allowing insurers to price policies accordingly. However, safeguards exist to prevent exploitation: the *Financial Services Act 2013* requires insurers to justify age-based pricing with empirical data, ensuring fairness. This blend of pragmatism and protection underscores Malaysia’s unique regulatory stance.

Practical tips for consumers navigating these policies include purchasing health insurance before age 45 to lock in lower premiums and higher coverage limits. For seniors, exploring government-backed schemes like *MySalam* or *Perkaso* can supplement private insurance gaps. Employers can also play a role by offering group health plans that mitigate age-based premium hikes for older employees. Understanding these policies empowers individuals to make informed decisions, aligning their health insurance choices with Malaysia’s regulatory landscape.

Do Health Insurance Brokers Charge Fees? Understanding Costs and Services

You may want to see also

Frequently asked questions

No, age and health insurance are not independent variables in Malaysia. Age is a significant factor that influences health insurance premiums, coverage, and eligibility.

In Malaysia, older individuals typically face higher health insurance premiums due to increased health risks and medical needs associated with aging.

Yes, younger individuals in Malaysia often benefit from lower premiums and more comprehensive coverage options because they are perceived as lower-risk policyholders.

Yes, most health insurance policies in Malaysia have age limits for new applicants, typically ranging from 65 to 70 years, depending on the insurer and plan.