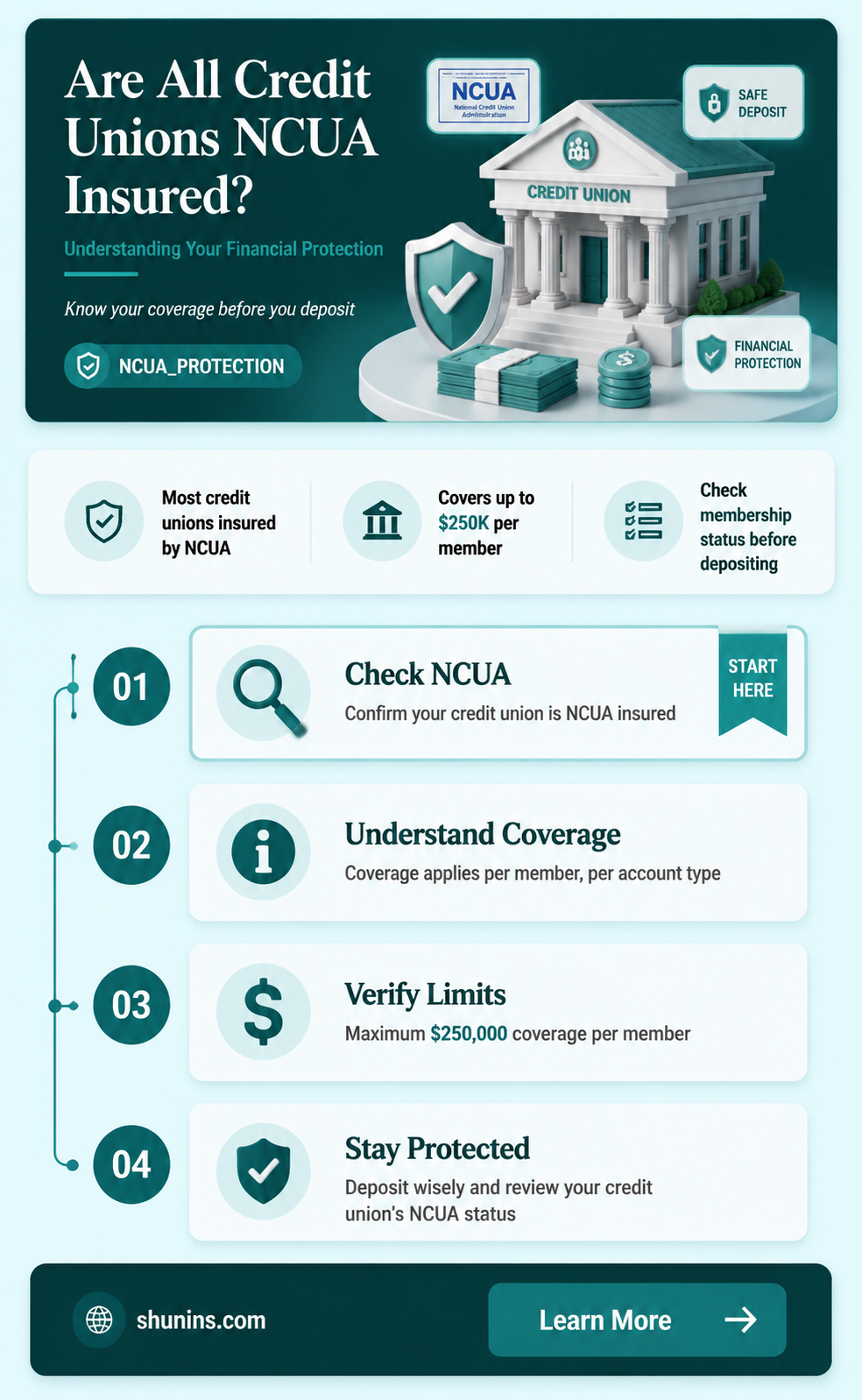

When considering joining a credit union, one of the most important questions potential members often ask is whether their deposits are insured. The National Credit Union Administration (NCUA) is the independent federal agency that insures deposits in federally insured credit unions, similar to how the FDIC insures deposits in banks. Not all credit unions are insured by the NCUA, as some may be privately insured or not insured at all. Federally insured credit unions are denoted by the official NCUA insurance sign, and members can verify a credit union’s insurance status through the NCUA’s online tool. Understanding the insurance coverage is crucial for ensuring the safety of your funds, as NCUA insurance protects deposits up to $250,000 per share owner, per insured credit union, for each account ownership category.

| Characteristics | Values |

|---|---|

| Are all credit unions insured by NCUA? | No, not all credit unions are insured by the NCUA. |

| Eligibility for NCUA Insurance | Federally insured credit unions must be chartered by the federal government or have applied for NCUA insurance. |

| State-Chartered Credit Unions | Some state-chartered credit unions may opt for NCUA insurance, but others may choose private insurance or state-specific coverage. |

| Coverage Limit | Up to $250,000 per share owner, per insured credit union, for each account ownership category. |

| Types of Accounts Covered | Checking, savings, money market accounts, share certificates, and certain retirement accounts. |

| Accounts Not Covered | Investments like mutual funds, stocks, bonds, and annuities. |

| How to Verify NCUA Insurance | Check the credit union’s official website, look for the NCUA logo, or use the NCUA’s online tool to confirm insurance status. |

| Alternative Insurance Options | Some credit unions may be insured by private insurers or state-specific funds, such as the National Credit Union Share Insurance Fund (NCUSIF) equivalents. |

| Importance of NCUA Insurance | Provides federal protection to members’ deposits, ensuring safety and confidence in credit unions. |

| NCUA vs. FDIC | NCUA insures credit unions, while FDIC insures banks; both offer similar coverage limits and protections. |

Explore related products

What You'll Learn

- NCUA Insurance Basics: Covers share accounts up to $250,000 per depositor, similar to FDIC for banks

- Eligibility Criteria: Only federally insured credit unions qualify; state-chartered may opt in or use private insurance

- Coverage Limits: Includes checking, savings, and retirement accounts but excludes investments like stocks or bonds

- Verification Process: Members can confirm NCUA insurance status via the official website or credit union disclosures

- Non-Covered Entities: Business accounts, government deposits, and foreign credit unions are not NCUA-insured

![]()

NCUA Insurance Basics: Covers share accounts up to $250,000 per depositor, similar to FDIC for banks

The National Credit Union Administration (NCUA) is the independent agency that oversees and insures credit unions in the United States, much like the Federal Deposit Insurance Corporation (FDIC) does for banks. One of the most critical aspects of NCUA insurance is its coverage of share accounts, which are the equivalent of deposit accounts in banks. NCUA Insurance Basics ensure that these share accounts are protected up to $250,000 per depositor, per insured credit union. This coverage is automatic for all members of federally insured credit unions, providing a safety net that safeguards members' funds in the unlikely event of a credit union failure.

It’s important to note that the $250,000 coverage limit applies per depositor, not per account. This means that if an individual has multiple share accounts within the same credit union—such as a savings account, checking account, and certificate account—all of these accounts are combined and insured up to the $250,000 limit. However, if the same individual has accounts at different federally insured credit unions, each institution’s accounts are insured separately up to $250,000. This structure allows members to maximize their insurance coverage by strategically spreading their funds across multiple credit unions if needed.

The NCUA insurance coverage is similar to FDIC insurance for banks, offering comparable protection to credit union members. Both programs are backed by the full faith and credit of the U.S. government, ensuring that depositors’ funds are secure. This similarity in coverage levels the playing field between credit unions and banks, giving members confidence that their money is safe regardless of the type of financial institution they choose. However, it’s essential to verify that a credit union is federally insured by the NCUA, as not all credit unions are covered. Federally insured credit unions display the official NCUA insurance sign, and members can confirm coverage using the NCUA’s online tool.

Another key aspect of NCUA insurance is its coverage of different types of share accounts, including regular share savings accounts, share draft (checking) accounts, money market accounts, and certificates of deposit. Additionally, certain retirement accounts, such as IRAs held in credit unions, are separately insured up to $250,000. This means that an individual could have $250,000 in regular share accounts and another $250,000 in IRA accounts at the same credit union, all fully insured by the NCUA. Understanding these coverage categories helps members optimize their insurance protection.

While NCUA Insurance Basics provide robust protection, it’s worth mentioning that not all financial products offered by credit unions are covered. For example, investments like stocks, bonds, mutual funds, and annuities are not insured by the NCUA. Similarly, contents stored in safe deposit boxes are not covered. Members should carefully distinguish between insured share accounts and uninsured investment products to ensure their funds are protected. By focusing on the fundamentals of NCUA insurance, credit union members can confidently manage their finances, knowing their share accounts are safeguarded up to $250,000 per depositor, just as bank customers rely on FDIC insurance.

Legacy Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Eligibility Criteria: Only federally insured credit unions qualify; state-chartered may opt in or use private insurance

When considering whether all credit unions are insured by the National Credit Union Administration (NCUA), it’s essential to understand the eligibility criteria for federal insurance. Only federally insured credit unions qualify for NCUA coverage. This means that credit unions chartered at the federal level are automatically eligible for this protection. The NCUA, as an independent federal agency, provides insurance through the National Credit Union Share Insurance Fund (NCUSIF), ensuring that members’ deposits are safeguarded up to $250,000 per account ownership category. This federal insurance is a cornerstone of trust and stability for members of federally chartered credit unions.

State-chartered credit unions, on the other hand, are not automatically covered by NCUA insurance. However, they have the option to opt into federal insurance by meeting specific regulatory requirements. To qualify, these credit unions must apply for federal insurance through the NCUA and adhere to federal standards, including financial reporting and operational guidelines. Once approved, they receive the same protections as federally chartered credit unions, ensuring their members’ funds are insured by the NCUSIF. This option allows state-chartered credit unions to offer the same level of security as their federal counterparts.

For state-chartered credit unions that choose not to opt into federal insurance, private insurance is an alternative. Private insurers, such as the National Deposit Insurance Corporation (NDIC) or American Share Insurance (ASI), provide coverage for these institutions. While private insurance can offer similar protections, it is important for members to verify the credibility and coverage limits of the insurer, as these may differ from the NCUA’s $250,000 guarantee. Members should carefully review their credit union’s insurance status to ensure their deposits are adequately protected.

It’s crucial to note that not all credit unions are insured by the NCUA, as state-chartered institutions have the flexibility to choose their insurance path. Members of credit unions should confirm whether their institution is federally insured by the NCUA, opted into federal insurance, or covered by a private insurer. This information is typically available on the credit union’s website, in branch materials, or through the NCUA’s online database. Understanding the insurance status of a credit union is vital for making informed financial decisions.

In summary, eligibility for NCUA insurance is limited to federally insured credit unions, with state-chartered credit unions having the option to opt in or rely on private insurance. Members must be proactive in verifying their credit union’s insurance status to ensure their deposits are protected. The NCUA’s federal insurance provides a robust safety net, but it is not universal, and awareness of these distinctions is key to financial security. Always confirm your credit union’s insurance coverage to safeguard your funds effectively.

Benefit Term Life Insurance: What's the Deal?

You may want to see also

Explore related products

![]()

Coverage Limits: Includes checking, savings, and retirement accounts but excludes investments like stocks or bonds

The National Credit Union Administration (NCUA) provides insurance coverage for credit union members, ensuring their funds are protected. This insurance is a crucial aspect of credit unions, offering peace of mind to members regarding the safety of their deposits. When discussing coverage limits, it's essential to understand what types of accounts are included and excluded from this protection.

Coverage for Essential Accounts: NCUA insurance covers a wide range of accounts that are fundamental to an individual's financial well-being. This includes checking accounts, which are typically used for day-to-day transactions, allowing members to manage their regular expenses and income. Savings accounts are also insured, encouraging members to set aside funds for future goals or emergencies. Additionally, retirement accounts, such as Individual Retirement Accounts (IRAs), are protected, ensuring that members' long-term financial plans remain secure. These accounts are considered essential for financial stability and are therefore a priority for NCUA insurance coverage.

The coverage extends to various types of credit union accounts, providing a safety net for members' hard-earned money. For instance, share draft accounts (similar to checking accounts) and share accounts (similar to savings accounts) are both insured. This comprehensive coverage ensures that members' funds are protected across different account types, catering to diverse financial needs.

Exclusions and Limitations: While NCUA insurance offers extensive coverage, it's important to note that not all financial products are included. Investments such as stocks, bonds, mutual funds, and other securities are not covered. These are considered riskier assets, and their value can fluctuate, making them ineligible for the same level of protection as traditional deposit accounts. This exclusion is standard across most deposit insurance schemes, including those offered by the FDIC for banks.

Furthermore, it's worth mentioning that the coverage limits apply per account owner and account type. This means that if an individual has multiple accounts of the same type (e.g., several savings accounts) at the same credit union, the total amount insured is still subject to the coverage limit for that specific account type. Understanding these limits is crucial for members to ensure their funds are adequately protected.

In summary, NCUA insurance provides a robust safety net for credit union members' essential accounts, including checking, savings, and retirement funds. However, it's essential to be aware of the exclusions, particularly regarding investments, to make informed financial decisions. This knowledge empowers credit union members to maximize the benefits of their insured accounts while also understanding the boundaries of this protection.

Alex Honnold: Life Insurance for a Daredevil?

You may want to see also

Explore related products

![]()

Verification Process: Members can confirm NCUA insurance status via the official website or credit union disclosures

The verification process for confirming NCUA insurance status is a straightforward and essential step for credit union members. Members can begin by visiting the official NCUA (National Credit Union Administration) website, which serves as a reliable resource for insurance-related information. The website provides a user-friendly interface where individuals can access the 'Credit Union Locator' tool. By entering the name of their credit union or its location, members can quickly retrieve details about the institution, including its NCUA insurance status. This online tool is regularly updated, ensuring that the information provided is accurate and current, giving members peace of mind regarding their deposits' safety.

Another method to verify NCUA insurance is by reviewing the credit union's official disclosures. Credit unions are required to provide transparent information about their insurance coverage to members. These disclosures are typically available on the credit union's website, often in a section dedicated to membership information or account terms and conditions. Members should look for specific statements indicating that the credit union is federally insured by the NCUA. Such disclosures may also include the insurance coverage limits, which are essential for members to understand the extent of their deposit protection.

During the verification process, members should be aware of the key indicators of NCUA insurance. The official NCUA website will display the credit union's charter number and the insurance status, which should be listed as 'Federally Insured' for covered institutions. Additionally, credit union disclosures might feature the NCUA's official logo or a statement confirming federal insurance. It is crucial to ensure that the information is up-to-date, as insurance status can change over time. Members are encouraged to periodically check these sources to stay informed, especially before making significant financial decisions.

For those who prefer a more direct approach, contacting the credit union's customer service can also provide the necessary verification. Members can call or visit their local branch and request information about the credit union's NCUA insurance. Credit union representatives should be able to provide immediate confirmation and address any concerns or questions regarding deposit insurance. This personal interaction can be particularly reassuring for members who prefer a more human-centric approach to financial matters.

In summary, verifying NCUA insurance status is a simple process that empowers credit union members to take control of their financial security. By utilizing the official NCUA website, reviewing credit union disclosures, and understanding the key indicators of insurance, members can quickly confirm their deposits' protection. This knowledge is vital for building trust in the credit union system and ensuring that members' funds are safeguarded by federal insurance. Regularly checking these sources is a prudent practice for all credit union members.

Employer Life Insurance: A False Sense of Security?

You may want to see also

![]()

Non-Covered Entities: Business accounts, government deposits, and foreign credit unions are not NCUA-insured

While the National Credit Union Administration (NCUA) provides valuable insurance for many credit union accounts, it's crucial to understand that not all accounts fall under its protective umbrella. Non-Covered Entities: Business accounts, government deposits, and foreign credit unions are not NCUA-insured. This means that funds held in these types of accounts are not guaranteed by the federal government in case of credit union failure.

Business accounts, even those held at NCUA-insured credit unions, are generally excluded from coverage. This includes accounts owned by corporations, partnerships, sole proprietorships, and other business entities. The rationale behind this exclusion is that businesses are considered to have a higher risk tolerance and access to other risk management tools compared to individual consumers. Therefore, it's essential for businesses to carefully consider their banking options and potentially explore alternative insurance solutions for their deposits.

Similarly, government deposits are not covered by NCUA insurance. This includes funds held by federal, state, or local government agencies, as well as political subdivisions and other governmental entities. The assumption is that government entities have their own mechanisms for safeguarding public funds and are not reliant on federal deposit insurance.

Foreign credit unions, regardless of their affiliation with U.S.-based credit unions, are also not eligible for NCUA insurance. This is because the NCUA's jurisdiction is limited to credit unions chartered under U.S. federal or state law. Foreign credit unions operate under different regulatory frameworks and are subject to the deposit insurance schemes (if any) of their respective countries.

It's important for account holders to be aware of these exclusions and to verify the insurance status of their accounts. Credit unions are required to clearly disclose whether an account is NCUA-insured or not. If you're unsure about the coverage of your account, don't hesitate to contact your credit union directly for clarification. Understanding these limitations will help you make informed decisions about where to keep your funds and ensure that your deposits are adequately protected.

Remember, while NCUA insurance provides valuable protection for many credit union members, it's not a blanket guarantee for all types of accounts. Being aware of the non-covered entities will help you navigate the financial landscape with greater confidence and security.

Life Insurance for Your Boyfriend: Is It Possible?

You may want to see also

Frequently asked questions

No, not all credit unions are insured by the NCUA. Only federally insured credit unions are covered by the National Credit Union Administration (NCUA) insurance, known as the National Credit Union Share Insurance Fund (NCUSIF).

You can verify if your credit union is federally insured by the NCUA by checking for the official NCUA insurance sign at the credit union’s branch or by using the NCUA’s online tool, "Find a Credit Union," which lists insured institutions.

NCUA insurance covers deposits (shares) in federally insured credit unions up to $250,000 per share owner, per insured credit union, for each account ownership category, similar to FDIC insurance for banks.

Some state-chartered credit unions are insured by the NCUA, while others may be insured by private insurers. To confirm, check with your credit union or use the NCUA’s online resources to verify their insurance status.