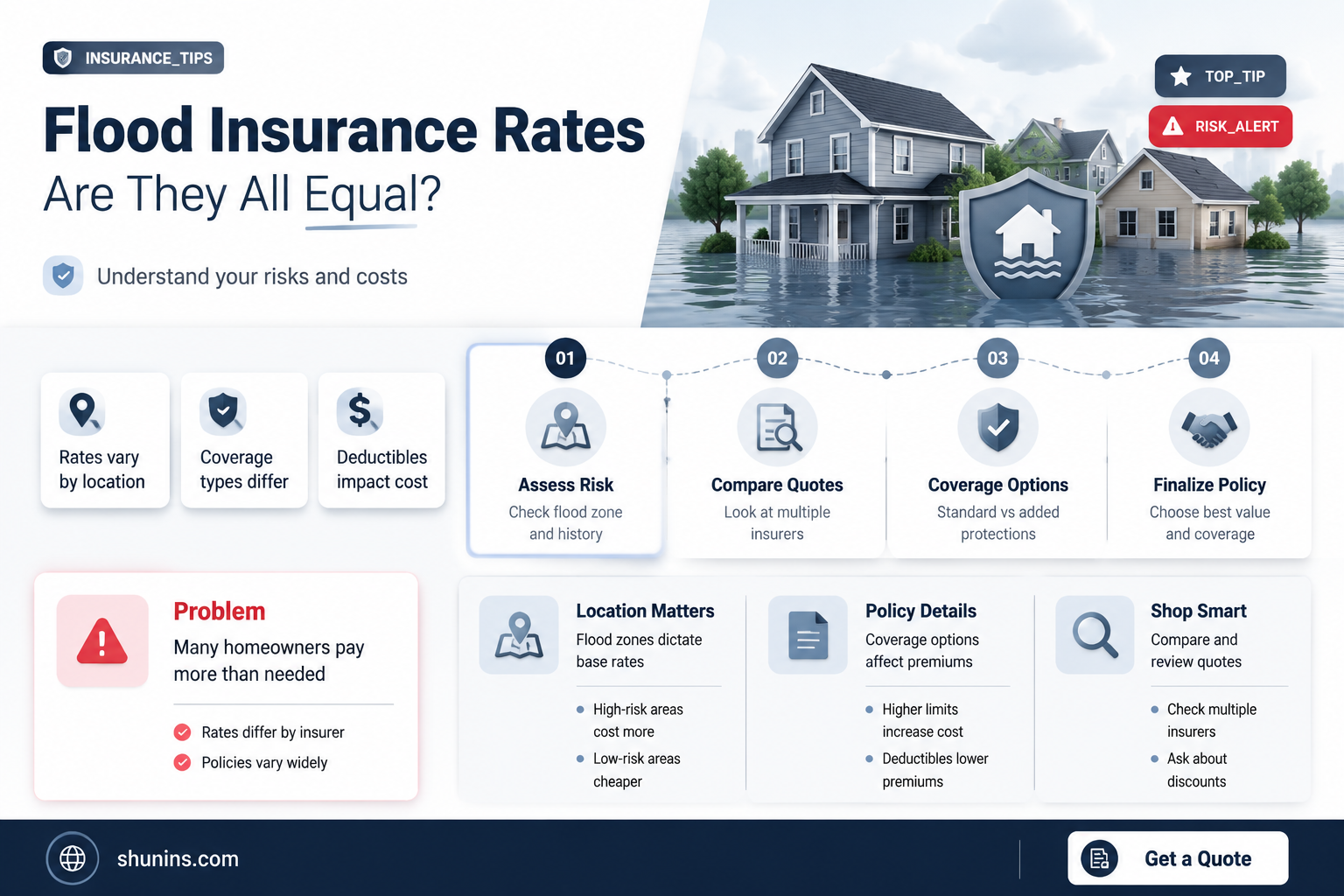

Flood insurance rates are determined by several factors, and they vary depending on the property and location. The National Flood Insurance Program (NFIP) calculates flood insurance rates based on a combination of rating variables that reflect a property's flood risk. Factors such as a property's location, elevation, characteristics, cost to rebuild, and flood history are considered when determining flood insurance rates. Additionally, communities that take extra steps to reduce flood risk may be eligible for discounts, and homeowners can take measures to lower their flood insurance rates by reducing their property's flood risk. As a result, flood insurance rates can differ significantly from one state to another and even within a single city.

| Characteristics | Values |

|---|---|

| Average annual cost | $888 |

| Average monthly cost | $68 |

| Highest average annual cost by state | West Virginia ($1,450) |

| Lowest average annual cost by state | Utah ($658) |

| Factors determining cost | Home location, elevation, characteristics, and cost to rebuild |

| Factors determining risk | Home value, rebuild costs, flood history, flood type, foundation type, first-floor elevation, distance from flooding sources, and replacement cost value |

| Discount eligibility factors | Flood vents, higher elevation, community-wide discounts, higher deductible, and sump pump |

Explore related products

What You'll Learn

- Flood insurance rates depend on your home's location and elevation

- Discounts are available for homes elevated off the ground

- Flood insurance is not included in standard homeowners, condo, or renters insurance

- The cost of flood insurance depends on the home's value and how it was built

- Flood insurance rates are higher in areas with a higher flood risk

![]()

Flood insurance rates depend on your home's location and elevation

Flood insurance rates are not the same and depend on several factors, including your home's location and elevation. The National Flood Insurance Program (NFIP) uses a unique combination of rating variables for each property to reflect its flood risk.

The location of your home relative to flooding sources such as coasts, rivers, and lakes is a crucial factor in determining flood insurance rates. Homes closer to these sources are typically at a higher risk of flooding and may have higher insurance rates.

Elevation plays a significant role in flood insurance rates. The ground elevation of your home compared to the surrounding area and nearby flooding sources is essential. Homes with elevated foundations or first floors higher off the ground generally have lower flood risk and, consequently, lower insurance rates. Documenting your home's elevation with an elevation certificate and comparing it to the estimated height of floodwater can help reduce your insurance costs.

Additionally, the number of floors in a building can impact flood risk. Buildings with more floors distribute flood risk across a larger area, potentially reducing the overall risk and insurance rates.

Mitigating flood risk can help lower insurance costs. This can be achieved by floodproofing your house, raising utilities like water heaters and air conditioners to higher locations, filling in basements and crawl spaces, and installing flood openings or vents. These measures not only reduce the potential for flood damage but can also lead to discounted insurance rates.

FEMA's Risk Rating 2.0 system further refines flood insurance pricing by considering additional factors such as property value, rebuild costs, flood history, and flood type. This approach aims to align premiums more closely with a property's actual flood risk, resulting in more equitable rates.

Auto Insurance: Understanding Corrosion Coverage

You may want to see also

Explore related products

![]()

Discounts are available for homes elevated off the ground

Flood insurance rates are not all the same, and they are determined by several factors. The Federal Emergency Management Agency (FEMA) considers factors such as home value, rebuild costs, flood history, flood type, and third-party software under its Risk Rating 2.0 system. The cost of a flood insurance policy is based on an individual property's specific flood risk and flooding history, rather than being placed in a general risk category based on location and property type.

One of the most effective ways to lower your flood insurance rates is to elevate your house. Discounts are available for homes that are elevated off the ground, as this reduces the risk of flood damage. Specifically, there are discounts for each foot that the house is elevated. This strategy gained popularity in the 1920s when Le Corbusier announced structures on pilotis as one of the 5 points of modern architecture. Elevating your house can preserve the natural terrain and create a free space with a greater connection between the public and private spheres, as seen in Le Corbusier's Villa Savoye.

In addition to elevating the entire house, you can also move utilities like your air conditioner or water heater to a higher location, preferably above the base flood elevation or the expected height of floodwaters. This will not only make them less likely to be damaged in a flood but can also result in an insurance discount. Filling in basements and crawl spaces can also help lower flood insurance rates, especially if you live in a high-risk flood zone, as homeowners with basements in these areas may pay up to 20% more for flood insurance.

Community-wide discounts are also available through FEMA's Community Rating System, which rewards communities that take extra steps to reduce flood risk. If you live in one of the participating communities, you can benefit from a flood insurance discount. Overall, by taking proactive measures to protect your home from flood damage, you can not only reduce the potential financial burden of repairs but also unlock flood insurance discounts and save on your flood insurance premium.

Auto Insurance: Can It Be Cancelled?

You may want to see also

Explore related products

![]()

Flood insurance is not included in standard homeowners, condo, or renters insurance

Flood insurance is a separate policy from standard homeowners, condo, or renters insurance. It is not included in the standard insurance packages listed above because it is a specialised type of insurance that covers a specific risk.

Flood insurance is provided by the National Flood Insurance Program (NFIP) and administered by FEMA. The NFIP was established by Congress in 1968 with the passage of the National Flood Insurance Act (NFIA). The program offers flood insurance to property owners, renters, and businesses, helping them recover faster when floods occur.

The NFIP provides insurance to anyone living in one of the 22,600 participating communities. This insurance covers buildings, the contents within a building, or both. For homeowners, this typically includes coverage for the structure and personal belongings. Structure coverage includes damage to the building's foundation, walls, and electrical systems, as well as appliances. Personal belongings coverage protects items such as furniture, clothing, and electronics, but there are limits on high-value items like artwork or jewellery. Condo owners should be aware that their flood insurance usually covers the unit's interior (drywall, flooring, cabinets) rather than the building's exterior or shared spaces.

The cost of flood insurance depends on various factors, including the property's location, elevation, characteristics, and cost to rebuild. FEMA's Risk Rating 2.0 system, introduced in 2021, considers new datasets, third-party software, home value, rebuild costs, flood history, flood type, and other factors to determine rates. The goal of this system is to have NFIP flood insurance costs increase each year to match the new, more accurate risk-based cost of insurance. As a result, many policyholders have seen their flood insurance rates increase as FEMA identifies properties at risk, even outside of designated flood zones.

State Farm Auto Insurance: Filing a Claim Made Easy

You may want to see also

Explore related products

![]()

The cost of flood insurance depends on the home's value and how it was built

The cost of flood insurance is influenced by a combination of factors, including the value of a home and its construction. While flood insurance is not mandated by law, its necessity often arises from the location of the property and the terms of the mortgage. Residences in high-risk flood areas may be required to obtain flood insurance by lenders as a condition of the loan agreement.

The National Flood Insurance Program (NFIP) calculates flood insurance rates using a unique set of rating variables for each property to assess its flood risk. These variables include the property's replacement value, the likelihood of flash floods or other flood types, and the cost to rebuild. Older homes constructed with outdated materials and techniques may be more susceptible to flood damage and could entail higher repair costs, influencing the overall flood insurance cost.

The elevation of a home plays a crucial role in determining flood insurance rates. Elevating a house above the base flood elevation can significantly reduce the premium. Obtaining an elevation certificate and comparing the home's elevation to the expected height of floodwaters can help lower insurance costs. Additionally, moving utilities, such as water heaters, to higher locations can decrease the likelihood of damage during a flood and result in insurance discounts.

The presence of a basement can also impact flood insurance rates. Homes with basements in high-risk flood zones may face higher insurance costs. Filling in basements or crawl spaces can be a prudent financial decision, as it reduces the potential for severe flood damage. Implementing flood openings or vents can facilitate water drainage, mitigating structural damage and potentially lowering insurance premiums.

The deductible amount selected for the flood insurance policy also influences the cost. A higher deductible generally leads to lower premiums, as the policyholder agrees to cover a larger portion of the repair costs in the event of a claim. According to FEMA, setting the deductible at the maximum amount of $10,000 can result in a discount of up to 40% on flood insurance rates.

Understanding CPI Auto Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Flood insurance rates are higher in areas with a higher flood risk

Flood insurance rates are not the same across the board. The National Flood Insurance Program (NFIP) calculates flood insurance rates based on a unique combination of rating variables for each property to reflect its flood risk.

The Federal Emergency Management Agency (FEMA) uses Risk Rating 2.0 to set flood insurance rates, which considers new datasets, third-party software, home value, rebuild costs, flood history, flood type, and other factors. The goal of Risk Rating 2.0 is to increase NFIP flood insurance costs each year to align with the new, more accurate risk-based cost of insurance. This means that properties with a higher flood risk will have higher insurance rates.

The cost of flood insurance varies depending on several factors, including the location of the property, its elevation, and the characteristics of the building. For example, homes in high-risk flood zones may pay up to 20% more for flood insurance, especially if they have a basement. Additionally, older homes built with outdated construction materials and techniques may be more vulnerable to flood damage and could incur higher repair costs.

To lower your flood insurance rates, you can take steps to protect your home from flood damage. This includes floodproofing your house by elevating it, moving utilities to higher ground, and installing flood openings or barriers. You can also increase your policy deductible and take advantage of community-wide discounts if your community is enrolled in the NFIP's Community Rating System.

It is important to note that flood insurance is not included in standard home, condo, or renters insurance policies, and it is a separate financial protection that individuals can purchase.

Auto Insurance and Leaking Sunroofs: What's Covered?

You may want to see also

Frequently asked questions

The average cost of flood insurance is $888 per year, according to 2023 FEMA pricing data. However, rates differ across states, with the lowest being $658 per year in Utah and the highest being $1,450 per year in West Virginia.

Flood insurance rates depend on several factors, including the home's location, elevation, characteristics, and cost to rebuild. The likelihood of flooding, based on the proximity to a large body of water or flood source, is also considered.

You can lower your flood insurance rates by taking steps to reduce the risk of flood damage to your home. This includes floodproofing your house by elevating it, moving utilities to higher ground, and installing flood openings or barriers. Additionally, increasing your policy deductible and taking advantage of community-wide discounts can also reduce your rates.

No, flood insurance rates can vary across insurance companies. However, the National Flood Insurance Program (NFIP) works with private insurance companies to offer the same rates and coverage, regardless of the company chosen.

While it is not mandatory to have flood insurance if you live in a low-to-moderate flood-risk area, it is still recommended. Approximately 40% of all flood insurance claims originate from these lower-risk zones, and standard homeowners or renters insurance typically does not cover flood damage.