The cost of insuring an SUV varies depending on several factors, including the SUV's make and model, its safety features, and the driver's history. Insurers often view SUVs as safer due to their robust construction and advanced safety features, which can result in lower insurance rates compared to other vehicle types. However, certain SUVs may be more expensive to insure than others. Repair costs, vehicle size, and theft rates are also factors that influence insurance premiums. It is essential to compare rates from different insurance companies and consider various SUV models to find the most affordable option.

| Characteristics | Values |

|---|---|

| Average insurance cost for SUVs | $1,935 per year |

| Cheapest SUV insurance | Honda HR-V, $1,673 per year |

| Most expensive SUV insurance | Toyota Sequoia, $2,536 per year |

| Average insurance cost for medium sedan | $1,694 per year |

| Average insurance cost for medium SUV | $1,529 per year |

| Average insurance cost for subcompact SUV | $1,298 per year |

| Average insurance cost for compact SUV | $1,292 per year |

| Average insurance cost for small sedan | $1,353 per year |

| Average insurance cost for medium sedan | $1,403 per year |

| Average insurance cost for SUV in Maine | Lowest in the US |

| Factors that affect insurance rates | Age, gender, location, driving history, vehicle model, year of manufacture, safety features, level of insurance coverage |

| Cheaper SUV insurance options | Chevrolet Equinox, Subaru Forester |

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

What You'll Learn

![]()

Insurers' perception of SUVs as safer vehicles

The insurance rates for SUVs vary depending on the model, with some being cheaper to insure than others. However, it is worth noting that SUVs are generally considered safer than sedans due to their robust construction, advanced safety features, and elevated driving position, resulting in lower insurance rates.

SUVs have a higher driving position, offering better visibility of the road and a perception of improved control and awareness of surroundings. Many are equipped with advanced safety technologies like lane-keeping assist, adaptive cruise control, and collision detection systems. This perception of safety may lead to a false sense of security, influencing driving behaviour and reliance on the vehicle's perceived safety rather than the driver's skills and caution.

Insurers often view SUVs as safer vehicles, which contributes to their lower insurance rates compared to other car types. The average insurance cost for SUVs is $1,935 per year, which is almost 9% less than the cost of insuring a sedan. However, it is important to note that within the category of SUVs, insurance rates vary, with smaller SUVs generally being cheaper to insure than larger ones.

The safety differences between SUVs and sedans are influenced by various factors, including design features, crash test performance, and visibility. While SUVs offer advantages in certain crash scenarios, their higher centre of gravity makes them more prone to rollovers, a significant concern for taller vehicles. In contrast, sedans prioritise a lower centre of gravity, enhancing handling and reducing rollover risk.

When determining insurance rates, insurers consider factors such as safety ratings, historical accident data, and repair costs. SUVs, due to their size and weight, can lead to higher claims and increased liability in collisions. Understanding local laws and their impact on liability assessments is crucial when considering insurance coverage.

Understanding Auto Insurance: The Three Key Components

You may want to see also

Explore related products

![]()

SUV insurance rates vary by model and insurer

When it comes to insuring an SUV, it's important to know that rates can vary depending on the specific model and insurer. While SUVs generally have lower insurance rates compared to sedans and trucks due to their safety features, there are several factors that can influence the cost of insurance for these vehicles.

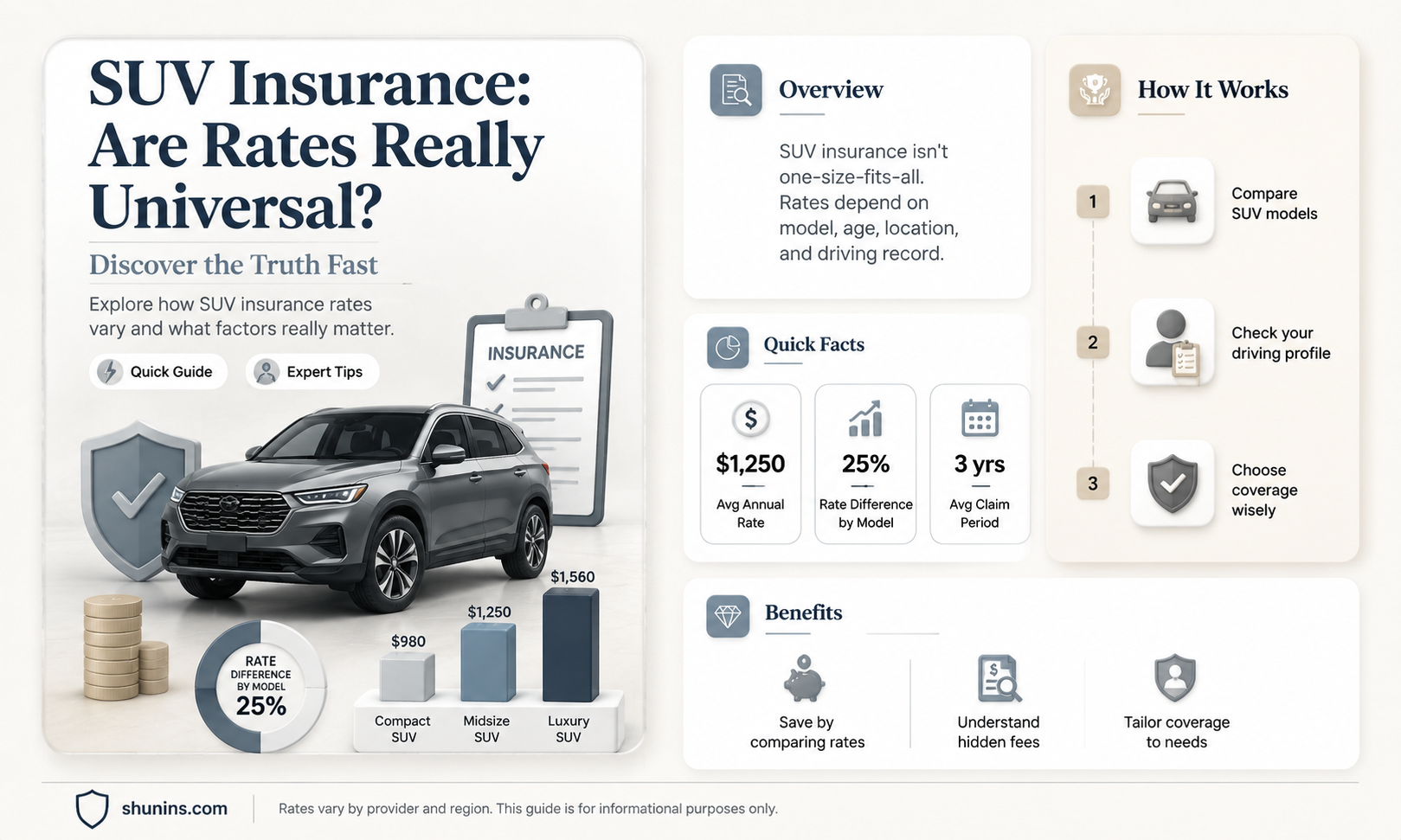

One factor is the size of the SUV. Larger SUVs tend to have higher insurance rates than smaller ones. For example, the average insurance cost for a subcompact SUV is $1,298 per year, while a compact SUV is $1,292, and a medium-sized SUV is $1,296. The cost increases for larger SUVs, with some of the most expensive models costing over $2,200 per year to insure.

The make and model of the SUV also play a significant role in determining insurance rates. Certain models are cheaper to insure due to their safety features and lower theft rates. For instance, the Honda HR-V is one of the most affordable SUVs to insure, with an average annual cost of $1,673. On the other hand, the Toyota Sequoia is one of the most expensive models, with an average insurance cost of $2,536 per year.

Additionally, the age, gender, location, and driving history of the driver can impact the insurance rates for an SUV. Insurance companies may offer lower rates to drivers with a clean driving record and charge higher rates in areas with high theft rates.

It's worth noting that electric SUVs may also have higher insurance rates than their gasoline-powered counterparts. However, as electric vehicles become more common, insurance costs for these SUVs are expected to decrease over time.

To find the best insurance rates for an SUV, it's recommended to compare quotes from different insurers, especially if you have a specific make and model in mind. By considering all these factors, SUV owners can make informed decisions and choose the most suitable insurance policy for their vehicles.

Mercury Insurance: Who's Driving?

You may want to see also

Explore related products

![]()

Electric SUVs are an exception and may cost more

SUVs are generally considered safer than other vehicles due to their sturdy construction and advanced safety features. This perception of safety often results in lower insurance rates for SUVs compared to other car types. However, this rule does not seem to apply to electric SUVs, which often cost more to insure.

Electric SUVs, like other electric vehicles, tend to be more expensive to insure than their gas-powered counterparts. This is mainly due to the higher cost of specialised parts required for repairs or replacement after an accident. Electric vehicle batteries, for example, can cost between $4,000 and $20,000 to replace, compared to $100-$200 for a traditional car battery. Repairing damaged battery packs can also require additional safety protocols and disposal fees, further increasing the cost.

The limited availability of repair shops with technicians qualified to work on electric vehicles is another contributing factor to the higher insurance costs. This scarcity of specialised repair facilities may result in higher repair charges, which are passed on to policyholders. Additionally, the higher purchase price of electric vehicles can lead to increased insurance rates, as the cost to replace them in the event of a total loss is higher.

However, it's important to note that the insurance costs for electric vehicles can vary depending on the make and model. For instance, insuring a Nissan Leaf will likely be significantly cheaper than insuring a Tesla Model X due to the lower cost of repairs for the former. Additionally, some insurance companies offer discounts and incentives specifically for electric vehicles, which can help offset the higher insurance rates.

While electric SUVs may currently attract higher insurance rates, this trend may not persist in the long run. As electric vehicles become more prevalent, the availability of specialised repair shops and parts is expected to increase, driving down the cost of repairs and, consequently, insurance rates.

Canceling Liberty Mutual Auto Insurance: A Guide

You may want to see also

Explore related products

![]()

The level of insurance coverage affects the cost

The level of insurance coverage is a significant factor in determining the cost of insurance for any vehicle, including SUVs. While it is challenging to generalize about insurance rates for all SUVs due to various factors, it is safe to say that the chosen level of insurance coverage will affect the overall cost.

The cost of insurance for an SUV can vary depending on the specific model, with some SUVs being significantly more expensive to insure than others. For example, the Toyota Sequoia is one of the most expensive SUVs to insure, with an average annual cost of $2,536. In contrast, the Honda HR-V is one of the most affordable options, with an average annual insurance cost of $1,673. These differences in insurance costs are influenced by factors such as the vehicle's safety features, repair costs, and theft rates, which are considered when determining insurance rates.

The level of coverage chosen will directly impact the overall cost of insurance. For example, a basic liability policy will typically be less expensive than a comprehensive policy that includes additional coverages such as collision, personal injury protection, or uninsured motorist protection. The deductible amount chosen will also affect the cost, as a higher deductible usually results in a lower premium, while a lower deductible leads to a higher premium.

Another critical factor influencing the cost of insurance for SUVs is the location of the insured. Urban areas tend to have higher insurance rates due to increased risks of vandalism, theft, and accidents. Additionally, factors such as the age and gender of the driver, as well as their driving history, can impact the cost of insurance. Mature drivers and women tend to benefit from lower insurance rates due to statistical differences in accident rates and severity.

It is worth noting that electric SUVs may also face higher insurance costs due to their higher purchase price. However, as electric vehicles become more prevalent, the cost to insure them is expected to decrease over time. Overall, while the level of coverage is a significant factor in determining insurance costs, it interacts with various other factors, making it essential to compare rates and consider multiple aspects when insuring an SUV.

Auto Glass Claims: Understanding the Impact on Your Insurance

You may want to see also

Explore related products

![]()

Location and driving history influence insurance rates

Several factors influence premium rates for SUVs. Insurers consider the driver's history and the vehicle they are planning to insure. SUVs are typically $314 per year cheaper to insure than sedans. However, one exception is that electric SUVs tend to be more expensive to insure.

Location is a key factor in determining insurance rates. Urban drivers pay higher auto insurance prices than those in small towns or rural areas due to higher rates of theft, vandalism, and accidents. The cost of medical care, car repair, and the frequency of auto accident lawsuits also vary by location and impact premium prices. For example, Maine residents enjoy the lowest average insurance premiums for SUVs.

Age is another significant factor in insurance rates, with young and inexperienced drivers paying higher premiums as they pose a higher risk for accidents. Insurance companies classify teen drivers as high-risk due to data showing they engage in riskier driving behaviors and have higher accident rates than other age groups. As drivers gain experience, their premiums decrease, with the lowest rates typically seen in drivers in their mid-50s.

A driver's history, including moving traffic violations and at-fault accidents, is one of the most important factors in determining insurance rates. Insurance companies view frequent claims as a red flag and may increase rates for several years after a claim is paid out. The more experience a driver has, the less likely they are to make mistakes, resulting in lower insurance prices.

In summary, location and driving history significantly influence insurance rates for SUVs. Urban residents and drivers with a history of claims or violations will likely pay higher premiums, while those in rural areas and experienced drivers with a clean record will benefit from lower rates.

Parents, Passengers, and Premiums: Navigating Auto Insurance Coverage for Young Adults

You may want to see also

Frequently asked questions

No, the insurance rates for SUVs vary depending on the model, make, safety features, and other factors.

Some of the cheapest SUVs to insure include the Honda HR-V, Mazda CX-30, Chevrolet Trailblazer, Honda CR-V, and Subaru Outback.

SUVs are generally considered safer due to their robust construction and advanced safety features, which can result in lower insurance rates compared to other types of cars.

Yes, factors such as the vehicle's repair costs, luxury finishes, advanced technology, and safety ratings can impact the insurance rates for SUVs.

It is recommended to compare insurance rates from multiple providers and consider factors such as age, location, driving history, and vehicle model to find the best insurance rates for an SUV.