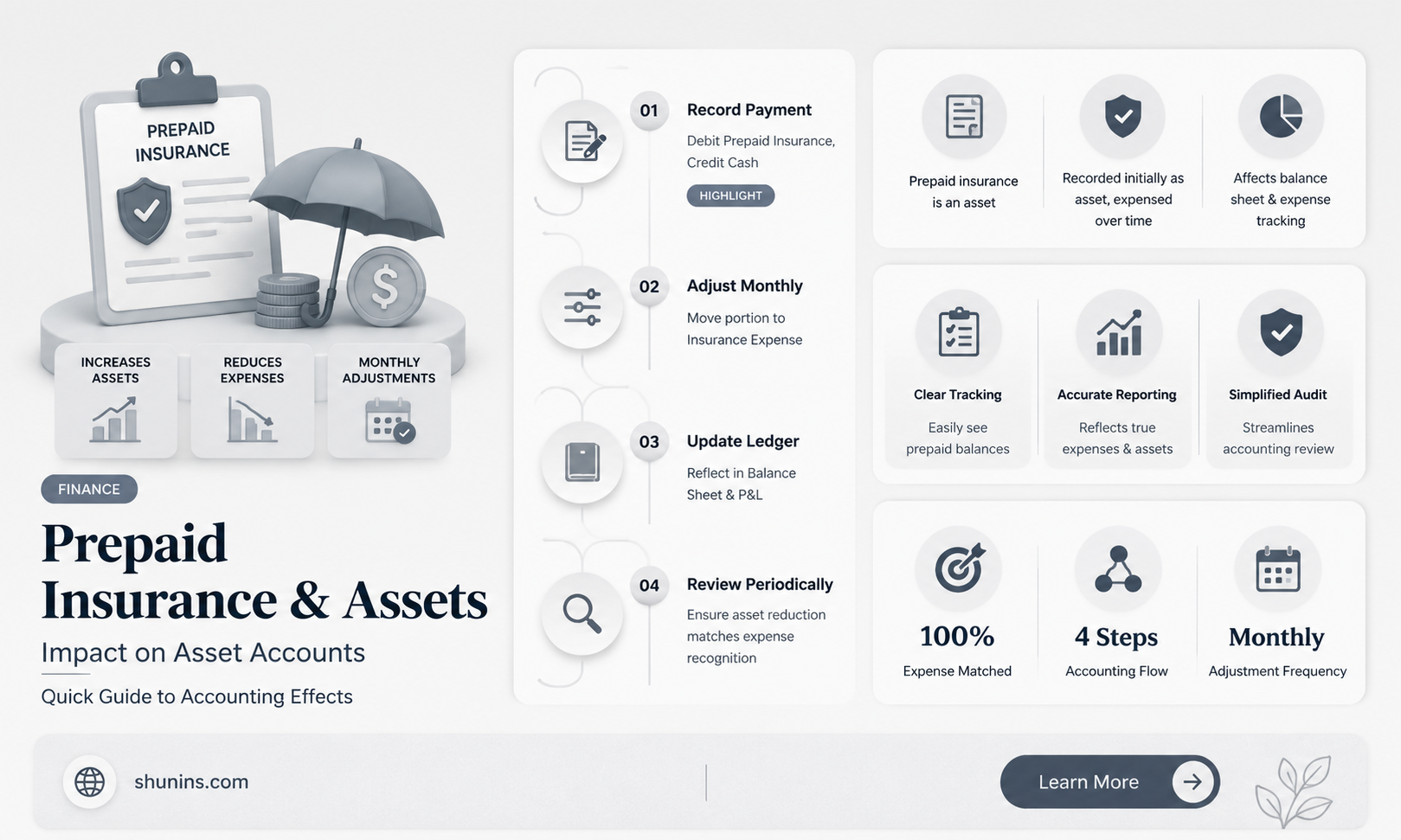

Prepaid insurance is a current asset if coverage is used within one year of payment. When a company pays in advance for goods or services it will receive in the future, these payments are recorded as assets on a company's balance sheet until the benefit of the good or service is realized. Prepaid insurance is a prepaid expense, which is a good or service that has been paid for in advance but not yet incurred. Prepaid expenses are considered assets because they provide future economic benefits to the company. When recording insurance premiums, you’ll debit prepaid insurance and credit cash, then systematically expense the amount over the coverage period through monthly adjusting entries.

| Characteristics | Values |

|---|---|

| Definition | Prepaid expense occurs when a company pays in advance for goods or services it will receive in the future. |

| Recording in balance sheet | Prepaid expenses are recorded as assets on a company's balance sheet. |

| Tracking | Prepaids are tracked in the accrual method of accounting, but not the cash method. |

| Amortization | The company amortizes the prepaid expense account with journal entries at the end of each period. |

| Adjusting entries | Adjusting entries are made each month to reflect the consumed portion of the prepaid expense. |

| Current asset | Prepaid insurance is a current asset if coverage is used within one year of payment. |

| Long-term asset | When coverage extends beyond the 12-month accounting period, the portion of insurance prepaid in the prior year and used in the following year is a long-term asset. |

| Impact on financial statements | Prepaid insurance impacts key financial metrics and ratios, including liquidity metrics such as the current ratio. |

| Asset conversion | The asset is converted to an expense for the period in which the prepaid is used. |

| Asset management | Effective asset management requires monitoring policy expiration dates and evaluating prepaid insurance to ensure alignment with business objectives. |

Explore related products

What You'll Learn

- Prepaid insurance is a current asset if coverage is used within a year of payment

- Prepaid insurance is considered a debit on the asset account

- Prepaid insurance is a financial asset representing future economic benefits

- Prepaid insurance is recorded as an asset and adjusted as the policy is consumed

- Prepaid insurance is important for accurate financial statements

![]()

Prepaid insurance is a current asset if coverage is used within a year of payment

Prepaid insurance is a current asset if the coverage is used within a year of payment. This is because prepaid expenses are considered assets on a company's balance sheet, as they represent future value. When a company makes an advance payment, it first records it as an asset, acknowledging that it has purchased something of future value. These assets turn into expenses as the company uses the service or product over time.

When a company uses the accrual method of accounting, the concept of prepaid expenses allows the accounting process to match the payment for expenses with the periods in which they are actually consumed. This enables the most accurate reflection of assets in the short term, as well as profit. The concept of prepaid is not used in the cash method of accounting, which is most often used by small businesses.

When insurance is prepaid, the accountant sets up an amortization worksheet. Initially, the total insurance premium paid is a debit to prepaid expense and a credit to cash. As each monthly portion of the prepaid asset amortizes or expires, it is expensed on the income statement, and the balance sheet is adjusted by recording a debit to insurance expense and a credit to prepaid expenses. These regular adjustments ensure financial statements accurately reflect how much of the prepaid expense remains as an asset and how much has been consumed.

Prepaid insurance is usually considered a current asset, as it becomes converted to cash or used within a short time. However, if a prepaid expense is not consumed within the year after payment, it becomes a long-term asset, which is not a very common occurrence.

Pursuing a Purr-fect Career: Navigating the Path to Becoming a Cat Insurance Adjuster

You may want to see also

Explore related products

![]()

Prepaid insurance is considered a debit on the asset account

Over time, as the insurance coverage is consumed, the prepaid expense is converted to an expense. This is reflected in the company's financial statements through adjusting journal entries, which are typically made each month. Each month, a portion of the prepaid insurance is moved from the asset account to the expense column, reflecting that month's portion of insurance coverage. This is recorded as a debit to insurance expenses and a credit to prepaid expenses.

The amount of the adjusting journal entry depends on the cost of the insurance and the period of coverage. For example, if a company pays $2,400 for six months of insurance coverage, each month of coverage would be worth $400. Therefore, at the end of the first month, an adjusting entry of $400 would be made, with a debit to insurance expense and a credit to prepaid insurance. This process is repeated each month until the prepaid insurance balance reaches zero, indicating that the full amount of the prepaid insurance has been consumed.

Prepaid insurance is typically considered a current asset, as it is usually converted to cash or used within a short period. However, in rare cases, an insurance policy may extend beyond the 12-month accounting period. In such cases, the portion of insurance prepaid in the prior year and used in the following year is considered a long-term asset.

General Insurance: Commercial Vehicles Covered?

You may want to see also

Explore related products

![]()

Prepaid insurance is a financial asset representing future economic benefits

Over time, as the coverage term progresses, the prepaid insurance account is gradually reduced. This is done through adjusting journal entries, which are typically made each month. These entries transfer a portion of the prepaid insurance to the expense column of the income statement, reflecting the expense incurred for that month. This process ensures that the financial statements accurately represent the matching principle, which states that expenses should be recorded in the same period in which the revenue is generated or the benefit is realised.

For example, if a company pays $60,000 for a year of liability insurance upfront, the full amount is initially recorded as an asset called "prepaid insurance". Each month, $5,000 is moved from the prepaid account to the expense column, reflecting that month's portion of insurance coverage. These regular adjustments ensure that the financial statements accurately reflect how much of the prepaid expense remains as an asset and how much has been consumed.

Prepaid insurance is of great importance to businesses as it helps manage cash flow and budget effectively. It ensures that there are no lapses in insurance coverage due to missed payments, providing protection against potential losses and obligations. Additionally, prepaid expenses can help businesses secure discounts and better rates, contributing to financial rewards and stability. However, it is crucial for companies to carefully manage their prepaid expenses to avoid straining their cash reserves.

Strategies for Passing the 60-Question Commercial Insurance Exam

You may want to see also

Explore related products

![]()

Prepaid insurance is recorded as an asset and adjusted as the policy is consumed

Prepaid insurance is a current asset if coverage is used within a year of payment. When a company makes advance payments, it initially records them as assets, acknowledging that it has purchased something of future value. These assets turn into expenses as the company uses the service or product over time. When a company uses the accrual method of accounting, the concept of prepaid expenses allows the accounting process to match the payment for expenses with the periods in which they are actually consumed. This enables the most accurate reflection of assets in the short term, as well as profit.

When insurance is prepaid, the accountant sets up an amortization worksheet. Initially, the total insurance premium paid is a debit to prepaid expense and a credit to cash. As each monthly portion of the prepaid asset amortizes or expires, it is expensed on the income statement, and the balance sheet is adjusted by recording a debit to insurance expense and a credit to prepaid expenses in an amount equal to the monthly portion until it has been fully realized and amortized. These regular adjustments ensure financial statements accurately reflect how much of the prepaid expense remains as an asset and how much has been consumed.

Adjusting journal entries are then needed each month so that the current month's expense is recorded on each month's income statement and the unexpired amount of the prepaid insurance is reduced each month in the asset account. The monthly adjusting journal entries will be shown on both the company's income statement and on the company's balance sheet as a reduction to the prepaid expense asset account. When the insurance coverage comes into effect, it is moved from an asset and charged to the expense side of the company's balance sheet. Insurance coverage is often consumed over several periods. In this case, the company's balance sheet may show corresponding charges recorded as expenses.

Prepaid expenses are considered an asset because they provide future economic benefits to the company. However, the adjusting journal entry for a prepaid expense affects both a company's income statement and balance sheet. The expense would show up on the income statement while the decrease in prepaid rent would reduce the assets on the balance sheet. When a prepaid expense is not consumed within the year after payment, it becomes a long-term asset, which is not a very common occurrence.

Weighing the Pros and Cons: W-2 vs. 1099 Insurance Adjusters

You may want to see also

Explore related products

![]()

Prepaid insurance is important for accurate financial statements

Prepaid insurance is a valuable tool for businesses to maintain financial stability, budgeting accuracy, and risk mitigation. It is a type of prepaid expense, which occurs when a company pays in advance for goods or services it will receive in the future. These advance payments are recorded as assets on a company's balance sheet, reflecting the future value they will bring. Prepaid insurance, specifically, is insurance paid in advance that has not yet expired on the date of the balance sheet.

When a company pays for a year of insurance upfront, the full amount is initially recorded as an asset called "prepaid insurance". Over time, as the insurance coverage is utilised, the relative insurance premium amount is transferred to expenses through adjusting journal entries. These regular adjustments are essential for accurate financial statements, as they ensure that the remaining prepaid expense and the consumed amount are correctly reflected.

For example, if a company pays $60,000 for a year of liability insurance in advance, the entire sum is initially recorded as an asset. Each month, $5,000 is moved from the prepaid account to the expense column, representing that month's insurance coverage. These monthly transfers are called "adjusting entries" and are crucial for investors and auditors to gauge the company's financial health and compliance with accounting standards.

The concept of prepaid expenses is particularly relevant in the accrual method of accounting, where it enables the matching of expenses with the periods in which they are consumed. This results in the most accurate reflection of assets and profits in the short term. Prepaid insurance, therefore, plays a vital role in maintaining accurate financial statements by providing a mechanism to allocate expenses accurately over the coverage period.

Commercial Plates: Impacting Your Insurance Rates?

You may want to see also

Frequently asked questions

A prepaid expense is a good or service that has been paid for in advance but not yet incurred. Companies make advance payments for practical reasons, such as securing a discount or because it is required.

Prepaid expenses are recorded as assets on a company's balance sheet. When a company pays for insurance coverage beyond the current accounting period, it creates what is known as prepaid insurance, a financial asset representing future economic benefits.

When recording insurance premiums, you’ll debit prepaid insurance and credit cash, then systematically expense the amount over the coverage period through monthly adjusting entries.