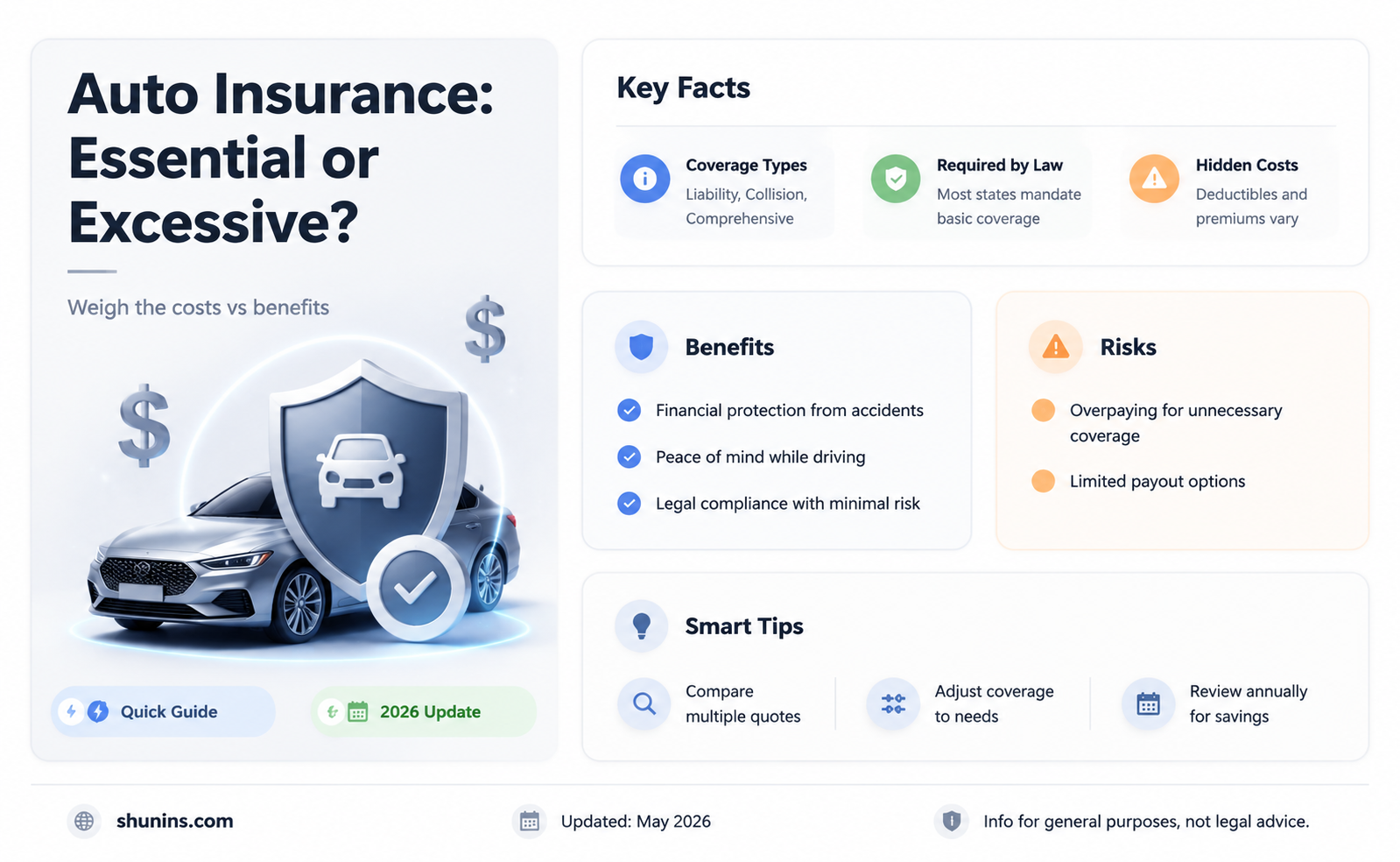

Auto insurance is an essential aspect of vehicle ownership, providing financial protection in the event of accidents and serving as a legal requirement in many places. While auto insurance is necessary, not all policies are created equal, and understanding what to look for in a policy is critical to ensuring suitable coverage.

Auto insurance offers financial peace of mind, covering vehicle repairs, medical bills, and legal fees, depending on the policy. It is also designed to protect against uninsured drivers and provide peace of mind while on the road.

When selecting auto insurance, it is crucial to consider factors such as liability coverage, collision coverage, comprehensive coverage, personal injury protection, and uninsured/underinsured motorist coverage. Additionally, insurance rates are influenced by driving history, vehicle type, location, coverage limits, deductibles, and available discounts.

Choosing the right auto insurance policy involves careful evaluation of individual circumstances, driving habits, and financial situation. It is essential to compare quotes, evaluate customer service, and periodically reassess coverage to ensure it aligns with changing needs.

| Characteristics | Values |

|---|---|

| Legal Requirement | Auto insurance is legally mandatory in most places. |

| Financial Protection | Accidents can be expensive. Auto insurance covers the cost of vehicle repairs, medical bills, and potential legal fees, depending on the coverage. |

| Protection from Uninsured Drivers | Auto insurance covers expenses if you're in an accident with an uninsured or underinsured driver. |

| Peace of Mind | Auto insurance provides peace of mind by offering financial protection and confidence while on the road. |

| Liability Coverage | Bodily Injury Liability and Property Damage Liability are the foundation of any auto insurance policy. |

| Collision Coverage | Collision coverage helps repair or replace a vehicle in an accident, regardless of fault. |

| Comprehensive Coverage | Comprehensive coverage protects against damages to a vehicle not related to collisions, such as theft, vandalism, and natural disasters. |

| Personal Injury Protection (PIP) | PIP is required in some states and covers medical expenses, lost wages, and other expenses for the policyholder and passengers, regardless of fault. |

| Uninsured/Underinsured Motorist Coverage | Uninsured/underinsured motorist coverage protects against expenses if involved in an accident with a driver who has insufficient or no insurance. |

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

What You'll Learn

- Auto insurance is a legal requirement in most places

- Auto insurance provides financial protection in the event of accidents

- Auto insurance policies consist of several components, including liability, collision, and comprehensive coverage

- Factors affecting auto insurance rates include driving history, vehicle type, location, coverage limits, and deductibles

- Discounts and bundling can help lower auto insurance premiums

![]()

Auto insurance is a legal requirement in most places

In the UK, for example, it is a legal requirement to have at least third-party insurance, which covers liability for injury to others and their property. This is the minimum cover required by law.

In the US, liability insurance is also required in all states when you buy auto insurance. This covers financial and medical expenses for others in the event of an accident.

Auto insurance is designed to provide financial peace of mind. It ensures that you are not left to cover the full cost of an accident on your own.

Auto Insurance Premium: What's Covered?

You may want to see also

Explore related products

![]()

Auto insurance provides financial protection in the event of accidents

Auto insurance is a contractual agreement between you and an insurance company. It provides financial protection in the event of accidents, covering the cost of vehicle repairs, medical bills, and potential legal fees, depending on your policy.

Understanding Auto Insurance

Auto insurance is designed to provide financial peace of mind. It ensures that when unexpected events occur, you’re not left to cover the full cost on your own. From minor fender benders to catastrophic accidents, auto insurance steps in to protect your finances and help you get back on the road.

The Importance of Auto Insurance

Auto insurance is vital for several reasons:

- Legal Requirement: In most places, it is legally mandatory to have auto insurance. Driving without it can result in fines, license suspension, or even legal action.

- Financial Protection: Accidents can be expensive. Auto insurance covers the cost of vehicle repairs, medical bills, and legal fees, depending on your coverage.

- Protection from Uninsured Drivers: If you’re in an accident with an uninsured or underinsured driver, your own policy can cover your expenses.

- Peace of Mind: Knowing you’re financially protected while on the road provides peace of mind. You can drive with confidence, assured that you have a safety net.

Components of an Auto Insurance Policy

Auto insurance policies have several components, each serving a unique purpose:

- Liability coverage is the foundation of any auto insurance policy. It includes bodily injury liability, which covers medical expenses, rehabilitation, and legal fees if you injure someone in an accident, and property damage liability, which covers damage to someone else’s property.

- Collision coverage helps repair or replace your vehicle if it’s damaged in an accident, regardless of who is at fault.

- Comprehensive coverage, often referred to as “comp,” provides protection for damages to your vehicle that are not related to collisions, such as theft, vandalism, natural disasters, and falling objects.

- Personal Injury Protection (PIP) is required in some states and covers medical expenses, lost wages, and other expenses for you and your passengers, regardless of who is at fault.

- Uninsured/Underinsured Motorist Coverage protects you if you’re involved in an accident with a driver who doesn’t have insurance or has insufficient coverage.

Choosing the Right Auto Insurance Policy

Selecting the right auto insurance policy involves careful consideration:

- Evaluate your circumstances, driving habits, and financial situation to determine the coverage types and limits that suit your needs.

- Obtain multiple quotes from different insurance companies to compare premiums, coverage options, and discounts.

- Look beyond the numbers and investigate the insurance company’s reputation for customer service and claims processing.

- Review the policy carefully to ensure you understand the coverage, limits, and deductibles.

- Periodically reassess your coverage as your auto insurance needs may change over time due to life events such as marriage or purchasing a new vehicle.

Behavioral Factors: Auto Insurance Premiums

You may want to see also

Explore related products

![]()

Auto insurance policies consist of several components, including liability, collision, and comprehensive coverage

Auto insurance is a necessity for vehicle owners, offering financial protection in the event of accidents and, in most places, being a legal requirement. Auto insurance policies are made up of several components, including liability, collision, and comprehensive coverage, each serving a distinct purpose.

Liability coverage forms the basis of any auto insurance policy, encompassing bodily injury liability and property damage liability. Bodily injury liability covers medical expenses, rehabilitation, legal fees, and compensation for pain and suffering if the insured individual injures someone in an accident. On the other hand, property damage liability covers damage to someone else's property, such as their vehicle or other personal property. Liability insurance is required in nearly all states.

Collision coverage assists in repairing or replacing the insured's vehicle if it is damaged in an accident, regardless of who is at fault. This coverage is particularly valuable for new or expensive vehicles. When selecting collision coverage, individuals must choose a deductible, which is the amount they are responsible for paying before the insurance company covers the rest. Higher deductibles generally lead to lower premiums but result in higher out-of-pocket expenses when making a claim.

Comprehensive coverage, often referred to as "comp," protects against damages to the insured's vehicle that are not collision-related. This includes damage from theft, vandalism, natural disasters, and falling objects. Similar to collision coverage, individuals must select a deductible for comprehensive coverage. It is a wise choice for those seeking full coverage for their vehicle.

In addition to these essential components, auto insurance policies may also include personal injury protection (PIP) and uninsured/underinsured motorist coverage. PIP is mandatory in some states and covers medical expenses, lost wages, and other expenses for the insured and their passengers, regardless of fault. Uninsured/underinsured motorist coverage, on the other hand, protects the insured if they are in an accident with a driver who has insufficient or no insurance.

Best Affordable Auto Insurance Options

You may want to see also

Explore related products

![]()

Factors affecting auto insurance rates include driving history, vehicle type, location, coverage limits, and deductibles

Driving history, vehicle type, location, coverage limits, and deductibles are some of the main factors that determine auto insurance rates.

Driving History

Insurance companies consider a driver's past as an accurate predictor of their future performance. A history of tickets, violations, accidents, or moving violations will increase the cost of current and future insurance premiums. The longer a driver goes without any incidents, the better their insurance rates will be.

Vehicle Type

The type of car one drives also plays a significant role in setting insurance rates. Insurance companies will look at past claims from similar models and evaluate repair costs, theft rates, and payments made for comprehensive claims. Brand-new sports cars are likely to come with higher premiums than older models since insurers will factor in potential replacement costs when determining rates.

Location

Location functions as a rating factor on two levels: state and zip code. Car insurance rates vary by state due to differing regulations and requirements. For example, some states require drivers to carry a certain liability coverage, while others do not. Additionally, rates are higher in areas with higher populations, as accidents and insurance claims are more prevalent.

Coverage Limits

The amount of coverage one chooses can significantly impact their policy costs. Opting for higher limits may cost more, but this extra protection could be invaluable in an emergency. On the other hand, purchasing only the minimum required coverage may leave one financially exposed.

Deductibles

The deductible is the amount one pays out-of-pocket before their insurance coverage kicks in. A higher deductible will result in a lower monthly payment, while a lower deductible will lead to a higher monthly payment.

Other factors that can affect auto insurance rates include age, gender, marital status, credit score, and annual mileage.

Gap Insurance: Vehicle Protection

You may want to see also

Explore related products

![]()

Discounts and bundling can help lower auto insurance premiums

Discounts and bundling can be effective ways to lower your auto insurance premiums.

Discounts

Many insurance companies offer a range of discounts that can help lower your premiums. These can include:

- Safe driver discounts: Insurers may offer discounts for maintaining a clean driving record with no accidents or violations.

- Multi-vehicle discounts: You may be eligible for a discount if you insure multiple vehicles with the same company.

- Bundling discounts: Insurers often provide discounts if you bundle your auto insurance with other types of insurance policies, such as home, renters, or life insurance.

- Good student discounts: Students who maintain a certain GPA in high school or college may be eligible for lower premiums.

- Defensive driving course discounts: Taking an accredited defensive driving course can sometimes lead to a discount on your insurance.

- Anti-theft system discounts: If your car has an anti-theft system, you may qualify for a discount on your comprehensive insurance coverage.

- Usage-based insurance discounts: Participating in a usage-based insurance program, where your driving habits are monitored, can lead to savings on your premiums if you drive safely and log low mileage.

- Pay-in-full discounts: Some insurers offer a discount if you pay your full 6- or 12-month premium upfront instead of paying monthly.

- Paperless or automatic payment discounts: Choosing to go paperless or enroll in automatic payments can sometimes result in a small discount on your premiums.

Bundling

Bundling your auto insurance with other types of insurance, such as home, renters, or life insurance, can often lead to significant savings. Insurance companies typically offer bundling discounts, which can range from 10% to 25% or more. By combining your auto insurance with another policy, you not only save money but also simplify your insurance management.

When considering bundling, it's important to compare quotes from multiple insurance companies. Even with a bundling discount, one insurer may offer lower base premiums than another. Additionally, not all insurers offer both home and auto insurance, so bundling may not be an option with your preferred auto insurance company. It's also worth noting that while you can bundle life insurance with other policies, discounts are not permitted on life insurance due to state regulations.

Gap Insurance: Keep or Toss?

You may want to see also

Frequently asked questions

Auto insurance is important for several reasons. Firstly, it is a legal requirement in most places, and driving without it can result in fines, license suspension, or legal action. Secondly, it provides financial protection in case of accidents, covering the cost of vehicle repairs, medical bills, and legal fees. It also protects you from uninsured or underinsured drivers and gives you peace of mind while driving.

The foundation of any auto insurance policy is liability coverage, which includes bodily injury liability and property damage liability. Collision coverage helps repair or replace your vehicle in an accident, regardless of fault. Comprehensive coverage protects against damages not related to collisions, such as theft, vandalism, or natural disasters. Personal Injury Protection (PIP) covers medical expenses and lost wages for you and your passengers, and uninsured/underinsured motorist coverage protects you if you're in an accident with a driver who has insufficient insurance.

Auto insurance rates are influenced by your driving history, the type of vehicle you drive, where you live, the coverage limits and deductibles you choose, and the discounts you qualify for. A clean driving record and a safe, reliable vehicle can result in lower premiums. Urban areas with high traffic and crime rates tend to have higher insurance costs, while rural areas usually have lower rates.