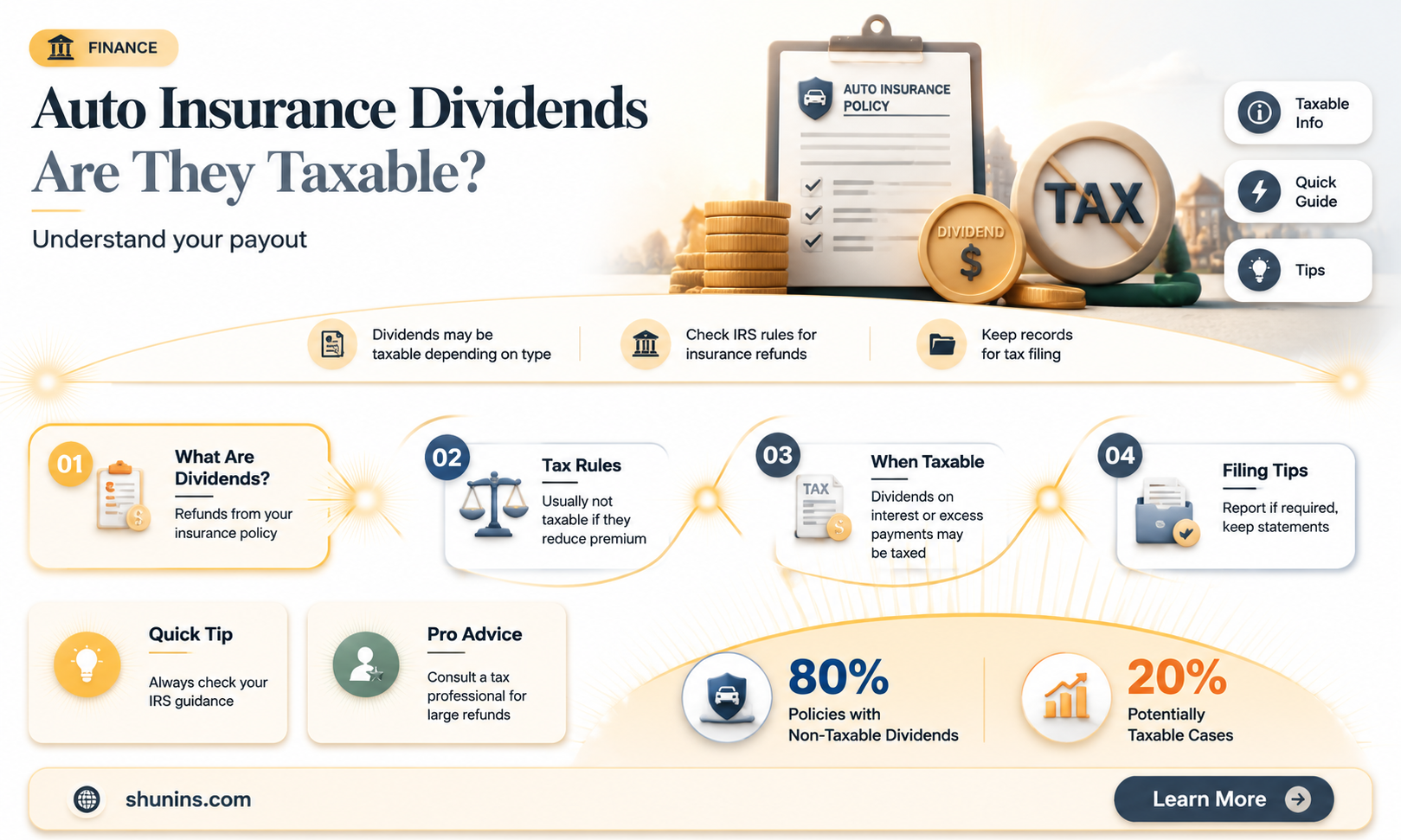

Auto insurance dividends are a return of premium paid to policyholders when a company performs better than expected. They are typically not taxable, as they are considered a return of the premium paid for the insurance policy. However, if the dividends exceed the total premiums paid, the excess amount may be subject to taxation as it is considered income. Additionally, interest earned on dividends left in the policy may also be taxable if it exceeds the premiums paid.

Explore related products

What You'll Learn

![]()

Dividends are generally not taxable

Dividends from insurance policies are generally not taxable. This is because the IRS considers them to be a return of premiums paid. However, there are certain situations in which dividends may be taxable.

Firstly, if the amount of dividend you receive is greater than the total amount of premiums you have paid into the policy, the excess may be taxable. In this case, any dividends over the amount you paid are considered income rather than a return of premium. For example, if you pay $1,000 in premiums and receive a $1,250 dividend, you may owe taxes on the excess $250.

Secondly, if you earn interest on dividends by leaving them in your policy, this interest income may be taxable if it is more than the amount you have paid in premiums.

It is important to note that these rules specifically apply to life insurance dividends and may not apply to dividends from other types of insurance policies, such as auto insurance. Additionally, tax laws can be complex and subject to change, so it is always a good idea to consult with a tax professional to determine your specific tax obligations.

In summary, while dividends from insurance policies are generally not taxable, there are certain exceptions to this rule. To ensure compliance with tax regulations, it is important to carefully review your specific circumstances and seek professional advice if needed.

Leasing a Subaru: Is GAP Insurance Included?

You may want to see also

Explore related products

![]()

Dividends exceeding premiums are taxable

Dividends from auto insurance are generally not taxable. This is because the IRS considers them to be a refund or return of premiums paid. However, if your dividends exceed the total premiums paid, the excess amount may be subject to tax. This is because any dividends that surpass the amount you paid are considered income rather than a return of premium.

For example, if you pay $1,000 in annual premiums and receive a dividend of $1,250, you may be required to pay taxes on the excess $250. In this case, consulting a tax professional is advisable to determine your specific tax obligations.

It is worth noting that any interest earned on dividends left in your policy to accumulate may also be taxable if it exceeds the total premiums paid. Therefore, it is important to carefully consider your options for receiving dividends, such as cash payments, purchasing additional insurance, or reducing future premiums.

While auto insurance dividends are typically tax-free, it is always a good idea to consult with a financial advisor or tax professional to understand the specific tax implications for your situation. They can provide valuable insights and guidance to help you make informed decisions regarding your auto insurance dividends and overall financial management.

Auto Insurance: Scratches Covered?

You may want to see also

Explore related products

![]()

Interest on dividends is taxable

Dividends are generally considered to be a "return of premium" and are therefore not taxable. However, interest earned on dividends is taxable. This is because any interest earned in excess of the amount paid is considered income, not a return of premium. For example, if you pay $1000 in life insurance premiums and receive a dividend of $1250, you may owe taxes on the $250 excess.

The IRS considers dividends to be taxable income if they exceed the total amount of premiums paid. In this case, the excess amount is considered income rather than a return of premium. This means that if you receive dividends that are greater than the total amount you have paid in premiums, you may need to pay taxes on the excess amount.

Interest earned on dividends can also be left in the policy to earn interest. This interest income may be taxable if it exceeds the amount paid in premiums. It's important to note that different types of dividends have different tax implications. For example, dividends from permanent life insurance policies, such as whole life insurance, are generally taxed differently from term life insurance dividends.

Additionally, the method of receiving dividends can also impact their taxability. For instance, if you choose to receive your dividends as a cash payment, it may be considered taxable income. On the other hand, if you apply your dividends towards future premium payments or let them accumulate interest within the policy, the tax implications may vary.

Gap Insurance: Credit Score Impact

You may want to see also

Explore related products

![]()

Dividends are a return of premium

Dividends are a return of a portion of the premiums paid for a life insurance policy. They are considered an annual fee paid by an insurance company to its whole life policyholders. Dividends are not guaranteed and are declared by the insurance company based on its earnings. The key components that determine a dividend payout are the dividend interest rate, mortality credits, and company expense debits.

Whole life insurance policies, particularly those issued by mutual companies, are the most common type of policy that pays dividends. Mutual companies are owned by their policyholders, so it is customary for them to pay dividends annually back to their policyholders. However, not all mutual companies pay dividends, and among those that do, the dividend amounts can vary significantly.

When an insurance company performs better than expected, it may choose to pay some or all of its profits back to shareholders and policyholders in the form of a dividend. Dividends can be used in several ways, such as growing your life insurance, paying premiums, or taking them as cash.

Life insurance dividends are generally not taxable because they are considered a return of premium. However, if the dividends exceed the total amount of premiums paid, the excess may be taxable as income. Additionally, if policyholders choose to accumulate their dividends with the insurance company and earn interest, that interest income may also be taxable.

To avoid taxation on dividends, policyholders can choose to receive their dividends in cash up to the amount of premiums paid and then borrow against their policy, as loans are typically tax-exempt. Alternatively, policyholders can use their dividends to purchase "paid-up additions," which provide tax-sheltered growth and dividends within the tax sanctuary of the life insurance policy.

Calculating Vehicle Insurance Costs

You may want to see also

Explore related products

![]()

Dividends can be reinvested

DRIPs are dividend reinvestment plans offered by hundreds of publicly traded companies. They automatically reinvest your dividends into new shares of their stock at each quarterly dividend payout, without any ongoing cost to you. The shares are purchased directly from the company, rather than through a broker. Some companies offer flexible options, like full or partial reinvestment, and investors can often purchase fractional shares. DRIPs may also be a good option for those who are uncomfortable with investing online or who want to invest in individual stocks. However, DRIPs only invest in their own stock, and plans may vary, so it's important to research the specifics of each company's plan.

Alternatively, you can use your brokerage account to reinvest your dividends. Many brokers offer dividend reinvestment programs that automate the purchase of new shares in the same stock, exchange-traded fund (ETF), or mutual fund. This option provides access to multiple investment types, making it easier to diversify your holdings. While brokers typically don't offer stock at a discount, reinvesting dividends through a brokerage account is generally simpler and more flexible than DRIPs.

Regardless of the method chosen, reinvesting dividends can be a powerful way to boost your returns over the long term. However, it's important to keep in mind that you may still owe taxes on reinvested dividends, and you'll need to pull money from other accounts to pay the tax bill.

Auto Insurance Settlements: Taxable?

You may want to see also

Frequently asked questions

No, auto insurance dividends are not always taxable. They are considered a "return of premium" and are usually tax-free.

Auto insurance dividends may be taxable if they exceed the total premiums paid. In this case, the excess amount may be considered income and therefore taxable.

You should receive a Form 1099-DIV by January 31st if the amount of dividends you received is $10 or more and needs to be included in your taxable income.

Auto insurance dividends are a sum of money that an insurer pays to policyholders when the company performs better than expected. They are typically paid annually and can be received in cash or applied as a discount on future premium payments.