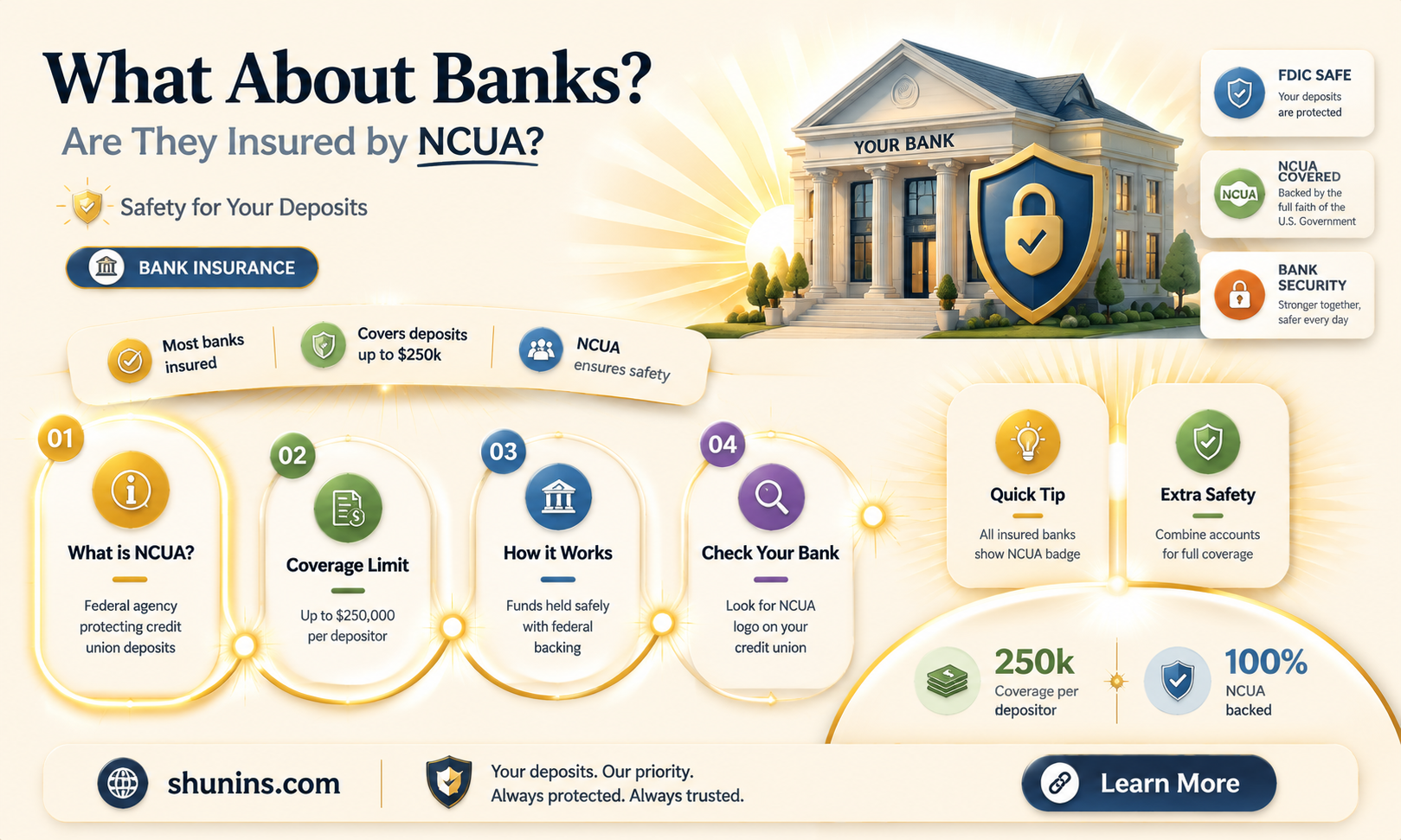

Banks are insured by the Federal Deposit Insurance Corporation (FDIC), whereas credit unions are insured by the National Credit Union Administration (NCUA). Both the FDIC and the NCUA provide federal insurance for deposits up to $250,000 per depositor, per account ownership category. The NCUA and FDIC were established by Congress to stabilise the nation's banking system and encourage public confidence in financial institutions.

| Characteristics | Values |

|---|---|

| Institution | National Credit Union Administration (NCUA) |

| Insured Deposits | Up to $250,000 per depositor, per federally insured credit union, per ownership category |

| Insured Accounts | Checking accounts, savings accounts, free checking accounts, and high-yield savings accounts |

| Non-Insured Deposits | Stocks, bonds, mutual funds, life insurance policies, annuities, municipal securities, safe deposit boxes, cryptocurrencies |

| Insured Institutions | Credit unions |

| Non-Insured Institutions | Banks |

Explore related products

What You'll Learn

![]()

The NCUA insures credit unions, not banks

The NCUA (National Credit Union Administration) is a federal agency created by Congress to regulate credit unions and insure deposits at member credit unions. It manages the National Credit Union Share Insurance Fund (NCUSIF), which guarantees that money in a credit union's account is backed with the full faith and credit of the US government.

The NCUA provides federal insurance for deposits at credit unions, protecting cash in eligible deposit accounts up to $250,000 per depositor, per federally insured credit union, per ownership category. This includes various account types, such as checking and savings accounts, share draft accounts, share savings accounts, and time deposits. Credit union members can use the NCUA's Share Insurance Estimator on MyCreditUnion.gov to calculate their specific coverage amount.

It is important to note that the NCUA does not insure all types of investments, such as stocks, bonds, mutual funds, life insurance policies, annuities, cryptocurrencies, or safe deposit boxes and their contents.

While the NCUA insures credit unions, banks are insured by the Federal Deposit Insurance Corporation (FDIC). Both the NCUA and FDIC offer similar coverage amounts and types, providing stability and confidence in the nation's banking system. The FDIC insures banks, protecting deposit accounts up to $250,000 per depositor, per bank, per ownership category.

In summary, the key difference between the NCUA and FDIC is the type of institution they insure, with the NCUA focusing on credit unions and the FDIC on banks.

ACA Private Insurance Enrollees: How Many?

You may want to see also

Explore related products

![]()

The NCUA offers $250,000 of protection per depositor

The National Credit Union Administration (NCUA) offers up to $250,000 of protection per depositor, per federally insured credit union, per ownership category. This means that if you have a single and a joint account at the same institution, both are insured up to the $250,000 limit. The NCUA's insurance coverage extends to various deposit accounts, including checking, savings, and money market accounts, as well as certificates of deposit and certain retirement plans. It's important to note that this coverage is provided automatically when individuals join a federally insured credit union, and no one has lost insured deposits at such institutions.

The NCUA's $250,000 limit may impact some members with larger deposits, but there are ways to maximize coverage. One strategy is to distribute funds across different institutions or ownership categories to ensure complete insurance. For example, having single-owned CDs at one credit union and joint checking and savings accounts at another can provide coverage beyond $250,000. Additionally, the NCUA's Share Insurance Estimator tool helps members calculate their coverage amount for personal, business, or government accounts.

It is worth noting that the NCUA's insurance coverage does not extend to investment losses, safe deposit box contents, or deposits exceeding the $250,000 limit. In the event of a credit union closure, the NCUA will send customers a check for the insured balance of their deposits, typically within a few days. The NCUA's insurance is backed by the full faith and credit of the United States government, providing assurance that insured deposits are protected.

The NCUA's insurance coverage is similar to that of its counterpart for banks, the Federal Deposit Insurance Corporation (FDIC). Both agencies offer the same amount of coverage ($250,000) for similar types of deposit accounts, providing stability and confidence in the nation's banking system. While the decision between a credit union and a bank should not be based solely on insurance, it is essential to verify that the chosen institution is a member of either the NCUA or FDIC to ensure deposit protection.

Blue Cross Insurance: Private or Public Option?

You may want to see also

Explore related products

![]()

The FDIC is the NCUA's counterpart for banks

The Federal Deposit Insurance Corporation (FDIC) is an independent federal agency that was created by Congress in 1933 to maintain stability and public confidence in the nation's financial system. The FDIC insures deposits at banks, while its counterpart, the National Credit Union Administration (NCUA), insures deposits at credit unions. Both agencies provide government-backed deposit account insurance for consumers throughout the United States, protecting cash deposits of up to $250,000 per depositor, per account ownership category.

The FDIC and NCUA have similar roles and offer comparable coverage for different types of institutions. The FDIC provides insurance for a wide range of common account types at member banks, including checking and savings accounts, while the NCUA offers the same level of protection for similar account types at credit unions. Both agencies require their member institutions to display their affiliation, making it easy for customers to identify them. Additionally, the FDIC and NCUA offer lookup tools on their websites, allowing individuals to verify if a bank or credit union is a member.

While the FDIC and NCUA have the same cap on deposit insurance, the specific rules and processes for bank and credit union accounts may differ. For example, in the event of a bank or credit union collapse, the FDIC has committed to repaying all depositors, regardless of their insured status. However, the NCUA may not necessarily follow the same course of action due to varying factors involved in the collapse of a credit union. Therefore, it is essential to understand the specific guidelines and protections offered by each agency.

Both the FDIC and NCUA play a crucial role in safeguarding consumers' deposits and maintaining stability in the financial system. By providing insurance coverage, they inspire confidence in the banking and credit union industries, allowing individuals to choose the financial institution that best suits their needs without worrying about the safety of their funds.

Insurers' Testing: What Private Insurers Test and Why

You may want to see also

Explore related products

![]()

NCUA insurance covers various account types

The National Credit Union Administration (NCUA) is a federal agency created by Congress in 1970 to regulate credit unions and insure deposits at federally insured credit unions. The NCUA's counterpart for banks is the Federal Deposit Insurance Corporation (FDIC). While accounts at credit unions and banks are insured differently, both federal agencies have similar rules and processes, and even have the same cap on how much of a depositor's funds are insured.

The NCUA's insurance coverage is automatic for members of federally insured credit unions, and there is no need to apply for it separately. The insurance covers up to $250,000 per depositor, per federally insured credit union, per ownership category. This means that if a credit union fails, the NCUA guarantees that depositors will receive their money up to this limit.

It is important to note that NCUA insurance does not cover all types of investments, such as stocks, bonds, mutual funds, life insurance policies, annuities, or municipal securities, even if these products are sold by a federally insured credit union. Additionally, the contents of safe deposit boxes are also not covered by NCUA insurance.

Vanguard Insurance: Federal or Private Protection?

You may want to see also

![]()

NCUA insurance is automatic for depositors

The NCUA operates and manages the National Credit Union Share Insurance Fund, which insures deposits at federal credit unions and most state-chartered credit unions. This fund is backed by the full faith and credit of the United States government. The NCUA requires federally insured credit unions to prominently display the official NCUA insurance sign at each teller station, as well as on their websites and wherever they accept share deposits or open accounts.

The NCUA insurance limit is $250,000 per individual depositor, per federally insured credit union, per ownership category. This includes various types of accounts, such as checking and savings accounts, share draft accounts, share savings accounts, and time deposits. Credit union members can use the NCUA's Share Insurance Estimator on MyCreditUnion.gov to calculate the amount of coverage their insured funds have.

It is important to note that not all credit unions are federally insured. Some state-chartered credit unions are insured by private insurers, which provide non-federal share insurance coverage that is not backed by the full faith and credit of the United States government. Therefore, members should confirm that their credit union is federally insured by using the NCUA's Credit Union Locator tool.

How Pharmacy Gag Clauses Profit Private Insurers

You may want to see also

Frequently asked questions

The FDIC, or Federal Deposit Insurance Corporation, insures banks, while the NCUA, or National Credit Union Administration, insures credit unions. Both protect deposit accounts and offer the same amount of coverage ($250,000) for similar types of deposit accounts.

NCUA insurance covers share deposits received at a federally insured credit union, including deposits in a share draft account, share savings account, or time deposit such as a share certificate. It also covers non-member deposits when permitted by law. NCUA insurance does not cover stocks, bonds, mutual funds, cryptocurrencies, or other investments, life insurance policies, annuities, municipal securities, safe deposit boxes, or digital assets like cryptocurrencies.

You can use the NCUA's Credit Union Locator tool to find out if your credit union is federally insured. Credit unions are also required to display the official NCUA insurance sign at each teller station and in all branches.