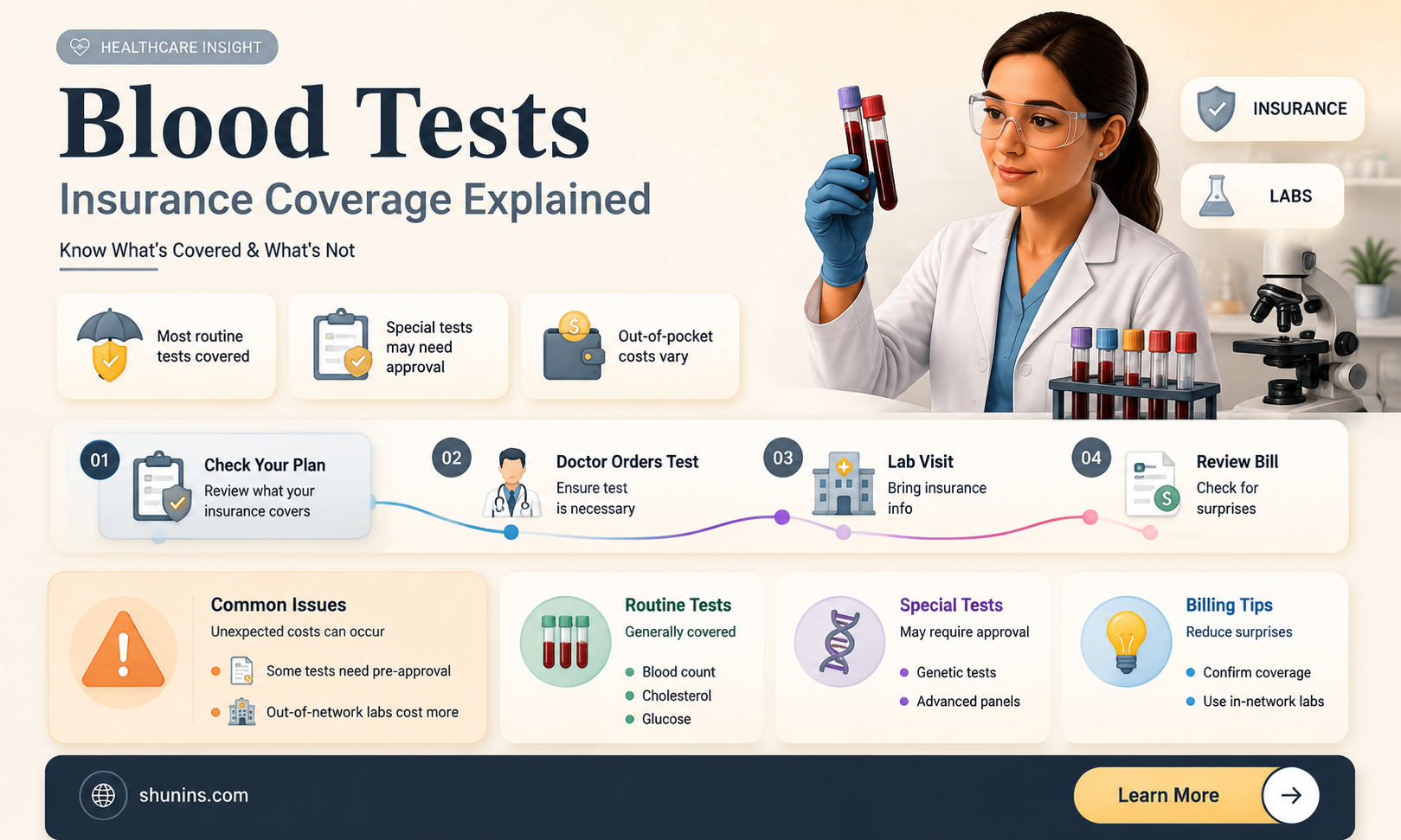

Blood tests are a crucial diagnostic tool, aiding in the identification and monitoring of diseases. They are also important for preventive healthcare and the management of ongoing illnesses. While insurance coverage for blood tests can vary depending on the insurance plan and provider, most insurance plans cover blood tests that are considered medically necessary or ordered by a healthcare provider. However, there may be certain restrictions or requirements that need to be met for the test to be covered. It is always recommended to check with the insurance provider and healthcare provider to understand the coverage and any associated out-of-pocket costs.

| Characteristics | Values |

|---|---|

| Blood tests covered by insurance | Annual routine tests (complete blood count and comprehensive metabolic panel) |

| Diagnostic tests ordered to investigate specific symptoms (e.g. thyroid tests or vitamin D) | |

| Tests required to monitor chronic conditions (e.g. HbA1c for diabetes, and liver function tests) | |

| Preventive screenings (e.g. colon cancer screening test Cologuard) | |

| Blood tests not covered by insurance | Preventive care blood tests |

| Diagnostic blood tests | |

| Blood tests for monitoring chronic illnesses | |

| Blood tests from out-of-network doctors or labs | |

| Blood tests with specific diagnosis codes not deemed preventive by insurance companies | |

| Blood tests not deemed medically necessary by insurance companies |

Explore related products

What You'll Learn

![]()

Blood tests during annual checkups

Blood tests are a basic tool used by physicians to screen for and diagnose diseases. They can also be used to monitor chronic conditions and spot risk factors, such as high cholesterol or elevated organ-health markers. Despite their importance, not all blood tests are covered by insurance.

Whether or not blood tests are covered by insurance during annual checkups depends on the insurance plan and the insurance company. Some insurance companies, such as Anthem Blue Cross & Blue Shield, may not cover blood tests as part of an annual checkup, while others, like United Health Care, do cover these costs.

It is important to note that insurance companies generally cover labs that are deemed medically necessary by medical professional groups. Many health insurance plans offer, at least in part, coverage for additional laboratory tests beyond the mandatory coverage of preventive screenings. These can include diagnostic tests ordered to investigate specific symptoms or tests required to monitor chronic conditions.

To avoid unexpected costs, patients should confirm coverage with their insurer before undergoing any blood tests. It is also worth noting that the cost of blood tests can vary depending on where they are performed, with hospital outpatient departments typically charging more than stand-alone labs or direct-to-consumer testing companies. Some insurance plans may also offer discounted fees for patients who are uninsured or whose plans do not cover clinical laboratory testing.

In summary, while blood tests during annual checkups may not always be covered by insurance, it is important to verify coverage with your specific insurance provider and understand the potential costs associated with these tests.

Who Gets the Life Insurance Payout in Delaware?

You may want to see also

Explore related products

![]()

Insurance plan and company differences

Blood tests are a basic tool used by physicians to diagnose diseases and monitor chronic conditions. However, not all blood tests are covered by insurance, and the coverage varies depending on the insurance plan and company. Some insurance companies may consider certain blood tests as diagnostic rather than preventive, and therefore may not cover them.

Secondly, the type of insurance plan can also impact coverage. For instance, ACA-compliant insurance plans typically cover preventive care without any out-of-pocket expenses. In contrast, non-ACA-compliant plans may not include preventive medicine in their coverage. Additionally, the specific terms of your insurance plan, such as coinsurance and deductible amounts, will influence how much you pay out of pocket for blood tests.

Thirdly, the location where the blood test is conducted can affect coverage and cost. Hospital outpatient departments (HOPDs) usually charge the most for lab services, while stand-alone labs like Labcorp or Quest may offer lower prices. Direct-to-consumer testing companies often provide testing packages at a discounted rate compared to individual lab tests.

Lastly, the specific laboratory tests ordered by the physician can impact coverage. Insurance companies generally cover tests deemed medically necessary by medical professional groups for preventing, managing, or treating diseases. However, even if a test is considered necessary by a doctor, insurance coverage may vary, and patients may need to pay some expenses out of pocket.

To avoid unexpected costs, patients should confirm coverage with their insurer and understand their insurance plan's specific terms and conditions. It is also essential to review the Explanation of Benefits (EOB) provided by the insurance company, detailing the services covered and denied.

Germans and Insurance: Who's Covered?

You may want to see also

Explore related products

![]()

Preventative vs diagnostic tests

Preventative tests are often part of annual physical examinations or wellness visits, which are usually covered by health insurance plans. These tests are considered essential for maintaining good health and can help detect potential issues early on, making them easier to manage or treat. For example, a mammogram can be a preventative screening tool for breast cancer, offered to patients at certain ages. However, the same mammogram can be considered diagnostic if there is a specific concern, such as a detected lump or pain in the breast.

Diagnostic tests are typically ordered by a doctor when a patient presents with specific symptoms or health concerns. These tests aim to identify the underlying cause of the symptoms and guide treatment decisions. For example, if a patient experiences chest pain, the doctor may order various diagnostic tests to determine the cause. While some insurance plans cover diagnostic tests, particularly those deemed medically necessary, patients may still need to pay out of pocket, depending on their specific plan and coverage limits.

The distinction between preventative and diagnostic tests can impact insurance coverage and billing. Preventative services are often covered at no cost to the patient under their health plan. In contrast, diagnostic services may incur separate charges, and insurance may not always cover them. It is important for patients to understand the reason for their medical appointments and the types of tests being performed to avoid unexpected medical bills. Patients can contact their insurance providers directly or utilise online tools to determine their coverage for specific tests.

In summary, preventative tests are used to proactively screen for potential health issues, while diagnostic tests are employed to identify the specific cause of symptoms or conditions. Preventative tests are typically covered by insurance plans, while diagnostic tests may or may not be covered, depending on the patient's plan and the nature of the test. Understanding the difference between these types of tests and their insurance implications is crucial for patients to manage their health and finances effectively.

Life Insurance: Their Doctors, Your Health

You may want to see also

Explore related products

![]()

Test costs and locations

The cost of blood tests varies depending on several factors, such as the type of test, the location, and the facility where the test is conducted. Basic tests like blood glucose or cholesterol checks typically cost between $20 and $40, while more specialized tests can range from $108 to $1,139. The mean cash price for lab tests without insurance is between $116 and $142. However, prices can vary significantly, with some tests costing as little as $6 in certain states and over $35 in others. Hospital outpatient departments (HOPDs) tend to charge the highest rates for lab services, while stand-alone labs like Labcorp or Quest usually offer lower prices. Direct-to-consumer testing companies, such as Levels or Function Health, often provide testing packages at discounted rates compared to individual tests.

To save costs, it is recommended to explore independent testing facilities, which generally offer lower prices than hospitals. Additionally, some facilities provide financial assistance programs, payment plans, and discounts for individuals facing financial challenges. It is also worth noting that insurance coverage for blood tests depends on the specific plan and company. While some insurance plans cover annual routine tests and medically necessary diagnostic tests, others may require out-of-pocket expenses or have different coverage criteria. Therefore, it is advisable to confirm coverage with your insurer and understand the specifics of your plan.

Life Insurance: Uninsurable? Strategies for the Uninsured

You may want to see also

Explore related products

![]()

Confirming coverage with insurers

To confirm coverage for blood tests with your insurer, it is important to understand the nuances of insurance plans and the specific context of your situation. Here are some detailed steps and considerations to help you navigate the process effectively:

Understanding Insurance Plan Variations

Insurance plans can vary significantly, and it is crucial to recognize that not all plans provide the same coverage for blood tests. Some insurers may cover a broader range of tests, while others may have more limitations. It is your responsibility to understand the specifics of your chosen plan.

Preventative vs. Diagnostic Testing

A key distinction in insurance coverage relates to the purpose of the blood test. Preventative testing, which is often part of annual health check-ups, may be covered by certain insurance plans. These tests are typically recommended for everyone, regardless of their health status, to detect potential issues early on. On the other hand, diagnostic testing is used to investigate specific symptoms or monitor chronic conditions and may not always be covered.

Necessary vs. Elective Testing

Insurance companies generally cover laboratory tests that the medical establishment has deemed necessary for preventing, managing, or treating diseases. However, even if your doctor considers a test "necessary," you may still need to pay out of pocket, depending on your specific insurance plan's provisions for coinsurance or deductibles. It is important to understand your plan's definition of "necessary" and whether it aligns with your medical provider's recommendations.

In-Network Laboratories

Your insurance plan may have a network of preferred laboratories, and using these in-network facilities can significantly reduce your out-of-pocket expenses. Before choosing a laboratory for your blood tests, confirm with your insurer which facilities are in your plan's network to ensure cost-effective testing.

At-Home Testing

Direct-to-consumer or at-home testing kits may or may not be covered by your insurance. If you opt for at-home blood collection, you will likely need to pay for the collection service yourself, but your insurance plan may cover the cost of the actual tests. Always check with your insurance provider to confirm coverage for at-home testing options.

Reading the Fine Print

Insurance policies can be complex, and understanding the fine print is essential. Review your insurance plan's documentation to identify any specific provisions, exclusions, or eligibility criteria related to blood tests. This will help you make informed decisions and avoid unexpected costs.

Contacting Your Insurer

Ultimately, the best way to confirm coverage is to contact your insurance provider directly. They can provide you with specific details about your plan's coverage for blood tests, including any limitations or requirements. Ask about the types of tests covered, the frequency of coverage, and any associated costs you may be responsible for.

Life Insurance, Annuities, and CDs: Are They Federally Protected?

You may want to see also

Frequently asked questions

It depends on the insurance plan and/or the insurance company. Some insurance companies cover blood tests as part of an annual physical examination, while others do not.

If your insurance company doesn't cover blood tests, you can contact the testing company and your insurance company to understand your particular situation. You can also look into getting free or low-cost tests at community health centres.

Yes, some testing companies offer in-home blood collection services. You will have to pay for the in-home collection service, but your insurance plan may cover the actual test.