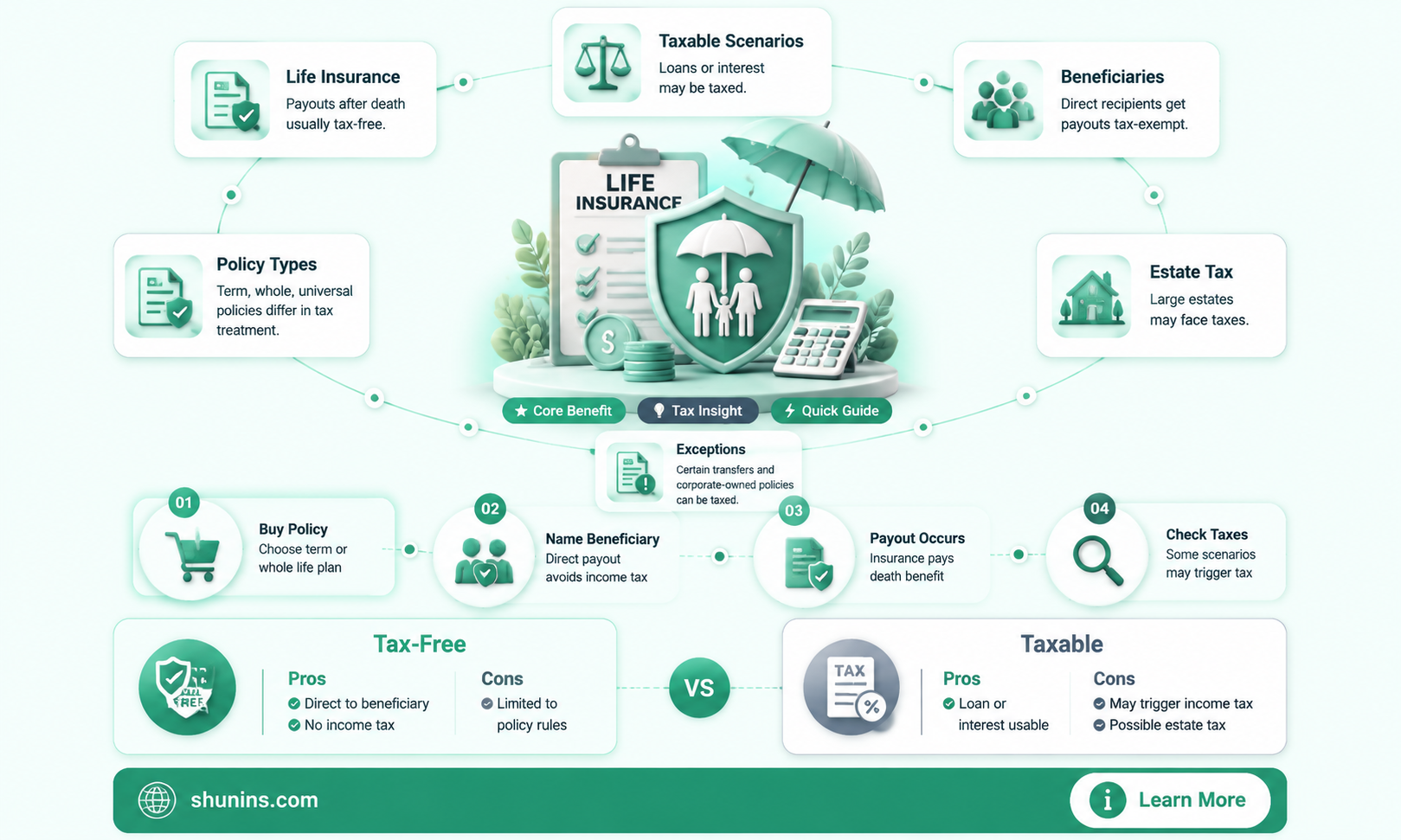

Life insurance is often taken out to provide peace of mind and financial security for loved ones after the policyholder's death. While the death benefit is typically tax-free, there are several situations in which taxes may be incurred. This is an important topic to understand to avoid unexpected tax complications and ensure beneficiaries receive the full benefit.

| Characteristics | Values |

|---|---|

| Are life insurance proceeds taxable as income? | No |

| Are there exceptions to the above? | Yes |

| What are the exceptions? | Interest on the proceeds is taxable, proceeds are paid in installments, proceeds are paid to the estate, proceeds are paid as part of an employer-paid group life insurance policy, proceeds are paid as part of a life insurance settlement, proceeds are paid after surrendering the policy, proceeds are paid to a beneficiary who is not the spouse |

| Are life insurance proceeds taxable as part of an estate? | Yes |

| What is the federal estate tax range? | 18% to 40% |

| What is the federal exemption limit? | $13.61 million |

| How many states impose an estate tax? | 12 |

| What is the exemption limit range for these states? | $1 million to $13.61 million |

| What is the highest state tax rate? | 20% |

Explore related products

What You'll Learn

![]()

Interest on life insurance proceeds is taxable

Life insurance proceeds are generally not taxable if you are the beneficiary receiving them due to the death of the insured person. However, any interest accrued on those proceeds is taxable and must be reported. This means that if you choose to receive the life insurance payout in installments instead of a lump sum, you will have to pay taxes on the interest that accumulates over time. This interest is considered taxable income, and you should report it as interest received.

The same rule applies to interest accrued on dividends from participating whole life insurance policies. While the dividends themselves are not taxed, the interest earned on those dividends is taxable income and must be reported.

It is important to note that the taxability of life insurance proceeds can depend on various factors, such as the type of policy, the relationship between the policy owner, the insured, and the beneficiary, and whether the policy was transferred for cash or other valuable consideration. Seeking advice from a tax professional or financial advisor is always recommended to understand your specific situation better.

Does Globe Life Insurance Offer Cash Value Benefits?

You may want to see also

Explore related products

$16.1 $16.95

![]()

Proceeds are not taxable if paid as a lump sum

Life insurance proceeds are typically not taxable as income. However, there are certain situations where taxes could come into play. If you receive a policy payout in installments rather than as a lump sum, any interest that accrues is taxable. The principal death benefit is still not taxed.

If you are the beneficiary of a life insurance policy, the payout, known as a death benefit, is typically tax-free. There are some exceptions, however. One such exception is when the beneficiary is an estate. If your estate is the beneficiary of your life insurance policy, the death benefit may be subject to estate taxes.

In 2024, the federal estate tax ranges from 18% to 40%, depending on how much of the estate is over $13.61 million, the exclusion limit. Without congressional action, the limit will revert to $5 million (indexed for inflation) at the start of 2026. In addition to the federal tax, twelve states and the District of Columbia impose an estate tax, with the exemption limit ranging from $1 million in Oregon to $13.61 million in Connecticut.

If you are receiving proceeds from an employer-paid life insurance policy, any death benefit beyond $50,000 is taxed as income, according to the IRS.

One way to avoid life insurance payouts being taxed as part of your estate is to set up an irrevocable life insurance trust (ILIT). You transfer ownership of the policy to the ILIT and cannot be the trustee. However, you can determine who you want as the trust beneficiary. While an ILIT is an effective way to ensure that your life insurance death benefit is not taxable as part of your estate, there are a couple of situations in which you may face a tax event.

When setting up the trust, if the life insurance policy's cash value is greater than the gift tax exemption, you may need to pay a gift tax when transferring ownership. The gift tax exemption for 2022 is $16,000. If you pass away within three years of transferring the life insurance policy to the trust, the policy will likely become part of your estate from a tax perspective. This is a policy meant to ensure you don't avoid having your heirs pay taxes by giving away assets as deathbed gifts.

Banks Accepting Life Insurance Collateral: Who and Why?

You may want to see also

Explore related products

![]()

Proceeds are taxable if paid in installments

Life insurance proceeds are generally not taxable if they are paid out as a lump sum. However, if the beneficiary chooses to receive the payout in installments, any interest accrued on those payments is typically taxed as regular income. This means that while the principal death benefit remains untaxed, the additional money generated from interest is considered taxable income. This situation often arises when parents request to have their life insurance death benefit paid in installments if their beneficiary is a young child or someone financially dependent on them.

The taxation of interest on installment payments is based on the idea that the death benefit is usually calculated from the date of the insured's death until the date the insurance company sends the check to the beneficiary. This delay results in the accumulation of interest, which is then taxable. Therefore, beneficiaries who opt for installment payments should be prepared to report and pay taxes on the interest portion.

It is important to note that the specific tax implications may vary depending on the state and country of residence, as well as the specific terms of the life insurance policy. Consulting with a tax professional or financial advisor can help individuals understand the tax consequences of their specific situation.

Understanding PA's Tax on Life Insurance Proceeds

You may want to see also

Explore related products

![]()

Proceeds are taxable if the beneficiary is an estate

Life insurance proceeds are generally not taxable as income. However, if your beneficiary is your estate, the proceeds may be taxed as part of it. This is because the proceeds will be added to the value of your estate. If the total value exceeds the exemption threshold, any amount over the exemption will be subject to estate and inheritance taxes.

In 2024, the federal estate tax ranges from 18% to 40%, depending on how much of the estate is over $13.61 million, the exclusion limit. The limit will revert to $5 million at the start of 2026 unless there is congressional action. Additionally, twelve states and the District of Columbia impose an estate tax, with exemption limits ranging from $1 million to $7 million.

To avoid this, you can set up an irrevocable life insurance trust (ILIT). By transferring ownership of the policy to an ILIT, you can keep the death benefit out of your taxable estate if certain rules are met. However, there are a couple of situations in which you may still face a tax event. Firstly, if the life insurance policy's cash value is greater than the gift tax exemption when setting up the trust, you may need to pay a gift tax when transferring ownership. Secondly, if you pass away within three years of transferring the policy to the trust, it will likely become part of your estate from a tax perspective.

Life Insurance for Billionaires: Do They Need It?

You may want to see also

![]()

Proceeds are taxable if the policy is surrendered

If you surrender your permanent life insurance policy, you may receive immediate cash, but this can come with tax implications. When you surrender the policy, you will receive the cash surrender value (CSV) after any fees are deducted. The CSV is the cash value of the policy minus any fees. While you don't have to pay taxes on the principal when it's returned, any cash value that the policy has accrued will be taxed as income.

For example, if you've paid $30,000 in premiums and the CSV of the policy is $45,000, the $15,000 difference would be taxed as ordinary income. This could push you into a higher tax bracket for that year.

Term life insurance policies do not have a cash value component, so there would be no taxes associated with surrendering the policy. However, you also wouldn't receive any money from the insurer.

If you have a whole or universal life insurance policy and cancel it before you pass away, you will typically receive the CSV, which is your policy's cash value minus any fees. If the CSV is higher than the amount of premiums you've paid into the policy (your cost basis), the excess is taxable as ordinary income.

Let's say you've paid $10,000 in premiums over the years that a permanent life insurance policy was in effect, and it resulted in $30,000 in proceeds. In this case, $20,000 would be taxable. The $30,000 will be reported on a Form 1099-R, with the $20,000 taxable portion shown.

Strategies to Avoid Taxes on Surrendered Policies

To avoid unexpected tax bills, it's important to carefully plan ahead and consider strategies to mitigate potential tax liabilities:

- Choose a lump-sum payout: Selecting a lump-sum payout over installments can keep the death benefit income tax-free.

- Avoid taxable interest: Opting for a lump-sum payout over installments can help you avoid taxable interest.

- Use an irrevocable life insurance trust (ILIT): Transferring ownership of the policy to an ILIT can keep the death benefit out of your taxable estate if certain rules are met. Ensure the policy is transferred to the ILIT at least three years before death.

- Keep policy loans in check: Monitoring your loan balance and ensuring your policy doesn't lapse can help prevent taxable income from policy loans.

- Transfer ownership early: Transferring policy ownership well in advance (more than three years before death) can keep the policy out of your taxable estate.

- Regularly review beneficiaries: Ensuring your estate isn't named as the beneficiary and naming a contingent beneficiary can help prevent estate taxes.

By implementing these strategies, you can minimize or avoid potential tax implications and safeguard your beneficiaries from avoidable tax complications.

Bankers Life Insurance: Colorado's Policy Changes and Their Impact

You may want to see also

Frequently asked questions

Life insurance proceeds are typically not taxable as income, but there are some exceptions. For example, if the beneficiary is an estate or if the payout is in installments, the proceeds may be taxed.

If you cancel a whole life or universal life insurance policy, you will typically receive the cash surrender value, which is your policy's cash value minus any fees. Any cash value accrued will be taxed as income.

If your estate is the beneficiary of your life insurance policy, the death benefit may be subject to estate taxes. In 2024, the federal estate tax ranges from 18% to 40% for estates valued over $13.61 million.

If the beneficiary receives the life insurance payout in installments rather than a lump sum, any interest that accrues is taxable. The principal death benefit is still not taxed.