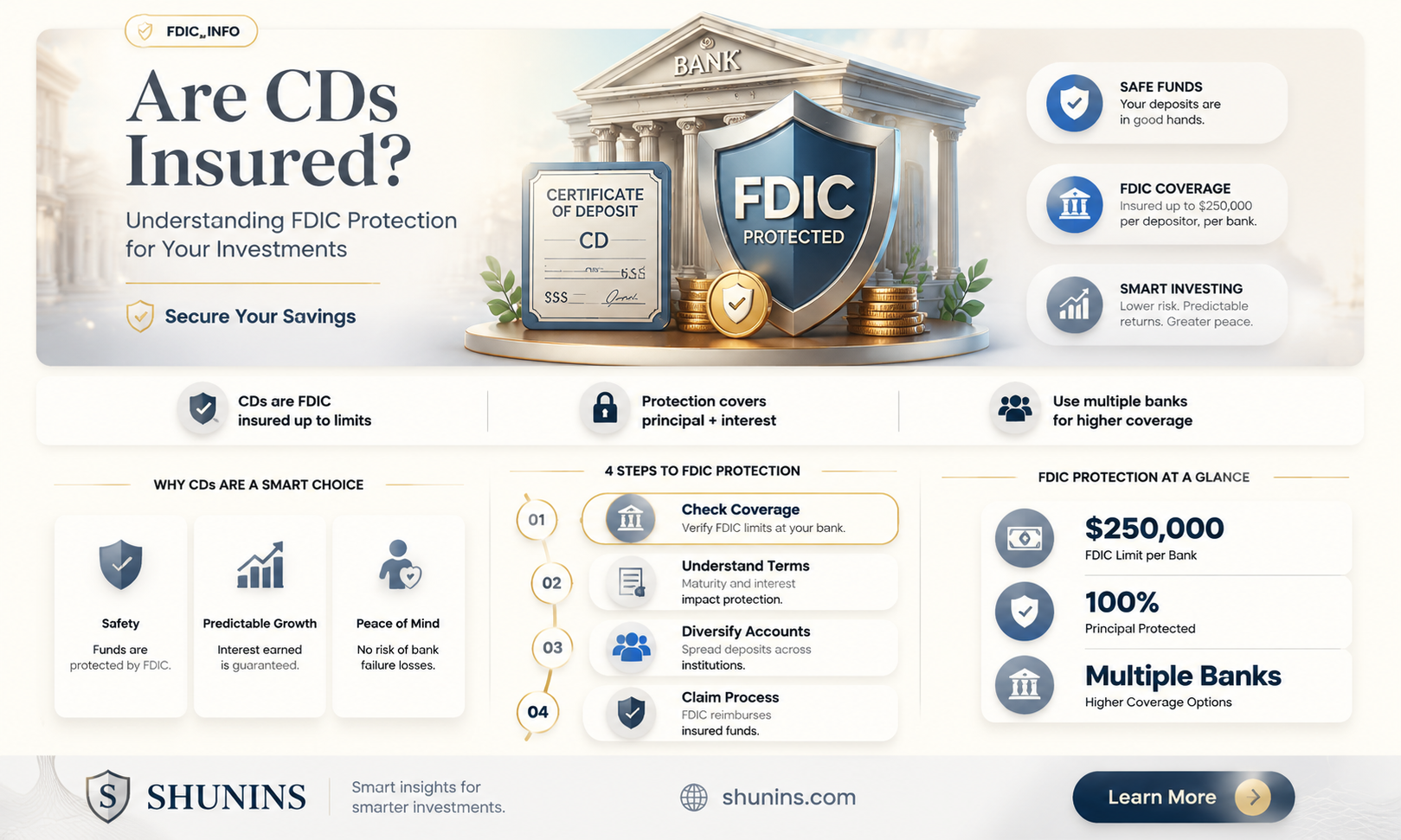

When considering the safety of your investments, it’s important to understand whether CDs (Certificates of Deposit) are insured. CDs are a type of time deposit account offered by banks and credit unions, and in the United States, they are typically insured by the Federal Deposit Insurance Corporation (FDIC) for banks and the National Credit Union Administration (NCUA) for credit unions. This insurance protects your principal and interest up to $250,000 per depositor, per insured bank, for each account ownership category, providing a layer of security for your savings. However, it’s crucial to verify the insurance status of the institution where you purchase the CD, as not all financial institutions are FDIC or NCUA insured. Understanding this protection can help you make informed decisions about where to invest your money.

| Characteristics | Values |

|---|---|

| FDIC Insurance Coverage | CDs purchased from FDIC-insured banks are insured up to $250,000 per depositor, per ownership category, per bank. |

| NCUA Insurance Coverage | CDs from NCUA-insured credit unions are insured up to $250,000 per depositor, per ownership category, per institution. |

| Coverage Limits | Insurance covers principal and accrued interest up to the limit. |

| Eligibility | Applies to CDs held in single accounts, joint accounts, trusts, and certain retirement accounts. |

| Non-Covered Entities | CDs from non-FDIC/NCUA-insured institutions, foreign banks, or investment products (e.g., CD-indexed annuities) are not insured. |

| Early Withdrawal Penalty | FDIC/NCUA insurance does not protect against penalties for early withdrawal. |

| Brokered CDs | Brokered CDs are insured, but the coverage is based on the issuing bank, not the brokerage firm. |

| Duration of Coverage | Coverage lasts for the entire term of the CD, including renewal periods. |

| Claim Process | In case of bank failure, the FDIC/NCUA typically pays insured depositors within a few days. |

| Alternative Insurance | Some CDs may be backed by private insurance, but this is less common and not as secure as FDIC/NCUA insurance. |

Explore related products

What You'll Learn

![]()

FDIC Insurance Coverage Limits

The Federal Deposit Insurance Corporation (FDIC) provides insurance coverage for deposit accounts, including certificates of deposit (CDs), held at insured banks and savings associations. Understanding the FDIC insurance coverage limits is crucial for anyone looking to safeguard their investments in CDs. As of the most recent guidelines, the standard insurance amount is $250,000 per depositor, per insured bank, for each account ownership category. This means that if you have multiple CDs or other deposit accounts at the same bank, the total amount insured across all accounts is capped at $250,000. However, the way accounts are titled can significantly impact your coverage.

For individuals with CDs in their own name, the $250,000 limit applies to the aggregate of all single-owner accounts at that bank. Joint accounts, where two or more individuals have equal rights to the funds, are insured separately from individually owned accounts. Each co-owner of a joint account is insured up to $250,000 for their share, meaning a joint account with two owners can be insured for up to $500,000. This allows couples or family members to maximize their FDIC coverage by strategically titling their CD accounts.

Certain types of accounts, such as retirement accounts (e.g., IRAs) or revocable trust accounts, also qualify for separate insurance coverage. Retirement accounts are insured up to $250,000 per owner, regardless of the number of accounts or beneficiaries. Revocable trust accounts can receive additional coverage depending on the number of beneficiaries named in the trust. For example, if a revocable trust names five beneficiaries, the account can be insured for up to $1,250,000 ($250,000 per beneficiary). Understanding these ownership categories is essential for optimizing FDIC insurance coverage for your CDs.

It’s important to note that FDIC insurance covers the principal amount deposited in the CD plus any accrued interest, up to the coverage limit. However, investments in stocks, bonds, mutual funds, or other non-deposit products are not insured by the FDIC, even if purchased through an insured bank. Additionally, CDs held at different banks are insured separately, allowing depositors to spread their funds across multiple institutions to increase their total insured amount. For example, if you have a $250,000 CD at Bank A and another $250,000 CD at Bank B, both are fully insured.

To ensure your CDs are fully covered, regularly review your account ownership structure and the total amount held at each bank. The FDIC provides an Electronic Deposit Insurance Estimator (EDIE) tool on its website, which can help you calculate your insurance coverage based on your account types and balances. By staying informed about FDIC insurance coverage limits and strategically managing your CD accounts, you can protect your investments and have peace of mind knowing your funds are secure.

Life Insurance for Navy Reserves: What's on Offer?

You may want to see also

Explore related products

$50.85 $63.99

![]()

NCUA Insurance for Credit Unions

When considering the safety of your deposits, particularly in certificates of deposits (CDs), understanding the insurance coverage provided by the National Credit Union Administration (NCUA) is crucial. The NCUA is an independent federal agency that insures deposits in federally insured credit unions, similar to how the FDIC insures deposits in banks. For credit union members, this means that their funds, including those in CDs, are protected up to certain limits, providing peace of mind and financial security.

NCUA insurance covers various types of accounts, including share accounts, money market accounts, and, importantly, CDs. The standard insurance coverage is $250,000 per depositor, per insured credit union, for each account ownership category. This means that if you have multiple CDs or other accounts in the same credit union, they are aggregated and insured up to the $250,000 limit. However, you can maximize your coverage by structuring your accounts in different ownership categories, such as individual accounts, joint accounts, retirement accounts, and trust accounts, each of which is insured separately.

For CD holders, understanding how NCUA insurance applies is essential. If you have a CD in a federally insured credit union, it is automatically covered by NCUA insurance up to the $250,000 limit. This coverage extends to both regular CDs and IRA CDs, ensuring that your retirement savings are also protected. It’s important to note that the insurance covers the principal amount deposited and any accrued interest, so even if your CD earns interest that pushes the balance above $250,000, the full amount remains insured.

To ensure your CDs are fully insured, verify that your credit union is federally insured by the NCUA. You can do this by looking for the official NCUA insurance sign at the credit union or by checking the NCUA’s online database. Additionally, regularly review your account structure to ensure you are maximizing your insurance coverage, especially if you have multiple accounts or CDs. Proper planning can help you take full advantage of NCUA insurance limits and protect your savings effectively.

Lastly, it’s worth noting that NCUA insurance is backed by the full faith and credit of the U.S. government, providing a high level of reliability. This means that even in the unlikely event of a credit union failure, your insured deposits, including those in CDs, are safe and will be reimbursed up to the coverage limits. This federal guarantee makes credit union CDs a secure investment option, comparable to FDIC-insured CDs in banks. By understanding and utilizing NCUA insurance, credit union members can confidently invest in CDs, knowing their funds are protected.

Life Insurance Proceeds: Virginia's Tax Laws Explained

You may want to see also

Explore related products

![]()

Joint Account Insurance Rules

When considering the insurance coverage for joint accounts holding certificates of deposit (CDs), it's essential to understand the specific rules governing these accounts. Joint accounts, typically owned by two or more individuals, are subject to unique insurance regulations provided by the Federal Deposit Insurance Corporation (FDIC) in the United States. The FDIC insures deposits in joint accounts differently than individual accounts, offering coverage based on the ownership category rather than per co-owner. This means the insurance limit is not divided among the joint account holders but is applied collectively.

Under the FDIC's insurance rules, joint accounts are insured up to $250,000 per ownership category, the same limit as individual accounts. For example, if two people own a joint account, the entire account balance is insured up to $250,000, not $250,000 per person. This is because the account is considered a single ownership category. However, if the same individuals have other joint accounts at the same bank, each account is insured separately up to the $250,000 limit, provided the accounts are structured differently (e.g., one account is jointly owned with right of survivorship, and another is a payable-on-death account).

It's crucial to understand how the FDIC defines ownership categories for joint accounts. The corporation recognizes five ownership categories: single accounts, joint accounts, certain retirement accounts, revocable trust accounts, and irrevocable trust accounts. Joint accounts fall under the second category, and the insurance coverage applies to the total of all accounts in this category, not per individual. For instance, if two people jointly own multiple CDs at the same bank, the combined balance of all these CDs is insured up to $250,000 under the joint account ownership category.

To maximize insurance coverage for joint accounts, account holders should carefully structure their deposits. If two individuals each have $250,000 in separate individual accounts and also share a joint account with $250,000, the total insured amount would be $750,000 ($250,000 for each individual account and $250,000 for the joint account). However, if the joint account exceeds $250,000, the excess amount would not be insured. Therefore, it's advisable to distribute funds across different ownership categories or banks to ensure full coverage.

Lastly, beneficiaries of joint accounts also play a role in insurance coverage. In joint accounts with right of survivorship, the surviving account holder automatically inherits the funds upon the death of the other owner. The FDIC insurance continues to cover the account up to the $250,000 limit, regardless of the number of surviving owners. However, if the account is structured as a payable-on-death (POD) account, the beneficiary’s share is insured separately, potentially increasing the total insured amount. Understanding these nuances is vital for joint account holders to ensure their CDs are fully protected under FDIC insurance rules.

The Ultimate No-Lapse Guarantee Life Insurance Guide

You may want to see also

![]()

Uninsured CD Risks Explained

Certificates of Deposit (CDs) are generally considered a safe investment because they are insured by the Federal Deposit Insurance Corporation (FDIC) for banks or the National Credit Union Administration (NCUA) for credit unions, up to $250,000 per depositor, per insured institution, per ownership category. However, not all CDs are insured, and investing in uninsured CDs can expose you to significant risks. Uninsured CD risks arise when the CD is issued by an institution that is not FDIC or NCUA insured, or when the investment amount exceeds the insurance limits. Understanding these risks is crucial for any investor considering CDs as part of their portfolio.

One of the primary uninsured CD risks is the potential loss of principal if the issuing institution fails. Unlike insured CDs, where your money is protected up to the insured limit, uninsured CDs offer no such guarantee. If the bank or credit union goes bankrupt, you could lose all or part of your investment. This risk is particularly acute with smaller or less stable financial institutions that may offer higher interest rates to attract investors but lack the safety net of federal insurance. Always verify the insurance status of the institution before investing in a CD.

Another risk of uninsured CDs is the lack of liquidity. CDs typically require you to keep your money locked up for a fixed term, ranging from a few months to several years. If you need to access your funds before the maturity date, you may face steep penalties or lose a portion of the interest earned. While this is a risk with all CDs, it is more concerning with uninsured CDs because you also face the risk of losing your principal if the institution fails during the term. This double jeopardy makes uninsured CDs less attractive for risk-averse investors.

Uninsured CDs also expose investors to interest rate risk, especially in a rising rate environment. If you lock your money into a long-term uninsured CD and interest rates increase, you could miss out on higher returns available elsewhere. Additionally, if you need to withdraw funds early, you might not only face penalties but also lose the opportunity to reinvest at a higher rate. This risk is compounded by the lack of insurance, as you are essentially gambling on both the stability of the institution and the direction of interest rates.

Lastly, investing in uninsured CDs can lead to concentration risk, particularly if a significant portion of your portfolio is tied up in these products. Diversification is a key principle of prudent investing, and putting too much money into uninsured CDs from a single institution can leave you vulnerable to financial loss if that institution fails. Even if the CDs are from different banks, exceeding the FDIC or NCUA insurance limits means any amount over $250,000 is at risk. To mitigate this, consider spreading your investments across multiple insured institutions or asset classes.

In conclusion, while CDs are often touted as a safe investment, uninsured CD risks can significantly impact your financial security. From the potential loss of principal to liquidity issues, interest rate risk, and concentration risk, uninsured CDs require careful consideration. Always ensure your CDs are FDIC or NCUA insured and stay within the coverage limits to protect your investment. If you’re considering uninsured CDs, weigh the potential higher returns against the risks involved and consult a financial advisor to make an informed decision.

Life Insurance Payments: Are They Considered Income?

You may want to see also

![]()

Brokered CD Insurance Considerations

When considering brokered CDs, it's essential to understand the insurance protections available to investors. Unlike traditional bank CDs purchased directly from a financial institution, brokered CDs are bought and sold through brokerage firms, adding a layer of complexity to their insurance considerations. The primary insurance for brokered CDs is provided by the Federal Deposit Insurance Corporation (FDIC) or the National Credit Union Administration (NCUA), but there are important nuances to keep in mind.

First, FDIC or NCUA insurance covers brokered CDs up to the standard limit of $250,000 per depositor, per insured bank, for each account ownership category. However, because brokered CDs are often spread across multiple banks, investors must ensure they do not exceed this limit at any single institution. For example, if you purchase brokered CDs through a brokerage firm and they are placed in several banks, the total amount insured across all banks cannot exceed $250,000 per bank. This requires careful tracking to avoid gaps in coverage.

Second, the ownership structure of the brokered CD matters for insurance purposes. Joint accounts, trusts, and individual accounts are treated as separate categories for FDIC or NCUA coverage. Investors should diversify their brokered CDs across different ownership categories to maximize insurance protection. For instance, holding brokered CDs in both individual and joint accounts can effectively double the insured amount to $500,000 across the same bank.

Third, investors should be aware of the risks associated with non-FDIC-insured brokered CDs. While rare, some brokered CDs may not be FDIC-insured, particularly if they are issued by non-bank entities or structured as non-traditional products. Always verify the insurance status of a brokered CD before purchasing. Additionally, brokered CDs purchased on the secondary market may have different insurance considerations, as the original FDIC coverage may not transfer to the new owner.

Finally, working with a reputable brokerage firm is crucial for managing brokered CD insurance considerations. A trustworthy broker will provide transparency about the insurance status of each CD, help monitor coverage limits, and ensure compliance with FDIC or NCUA rules. Investors should also review their brokerage account statements regularly to confirm that their brokered CDs are properly insured and aligned with their financial goals. By staying informed and proactive, investors can fully leverage the safety and benefits of brokered CDs while minimizing risks.

Cigarette Impact: Life Insurance and Your Health

You may want to see also

Frequently asked questions

Yes, CDs (Certificates of Deposit) held at FDIC-insured banks are insured up to $250,000 per depositor, per insured bank, for each account ownership category.

No, credit unions are not insured by the FDIC. Instead, they are insured by the NCUA (National Credit Union Administration), which provides similar coverage of up to $250,000 per depositor.

Yes, if a bank fails, FDIC insurance protects your CD funds up to the insured limit, ensuring you do not lose your principal or accrued interest.

No, CDs held in brokerage accounts are not FDIC-insured. Only CDs held directly at FDIC-insured banks or NCUA-insured credit unions are covered.