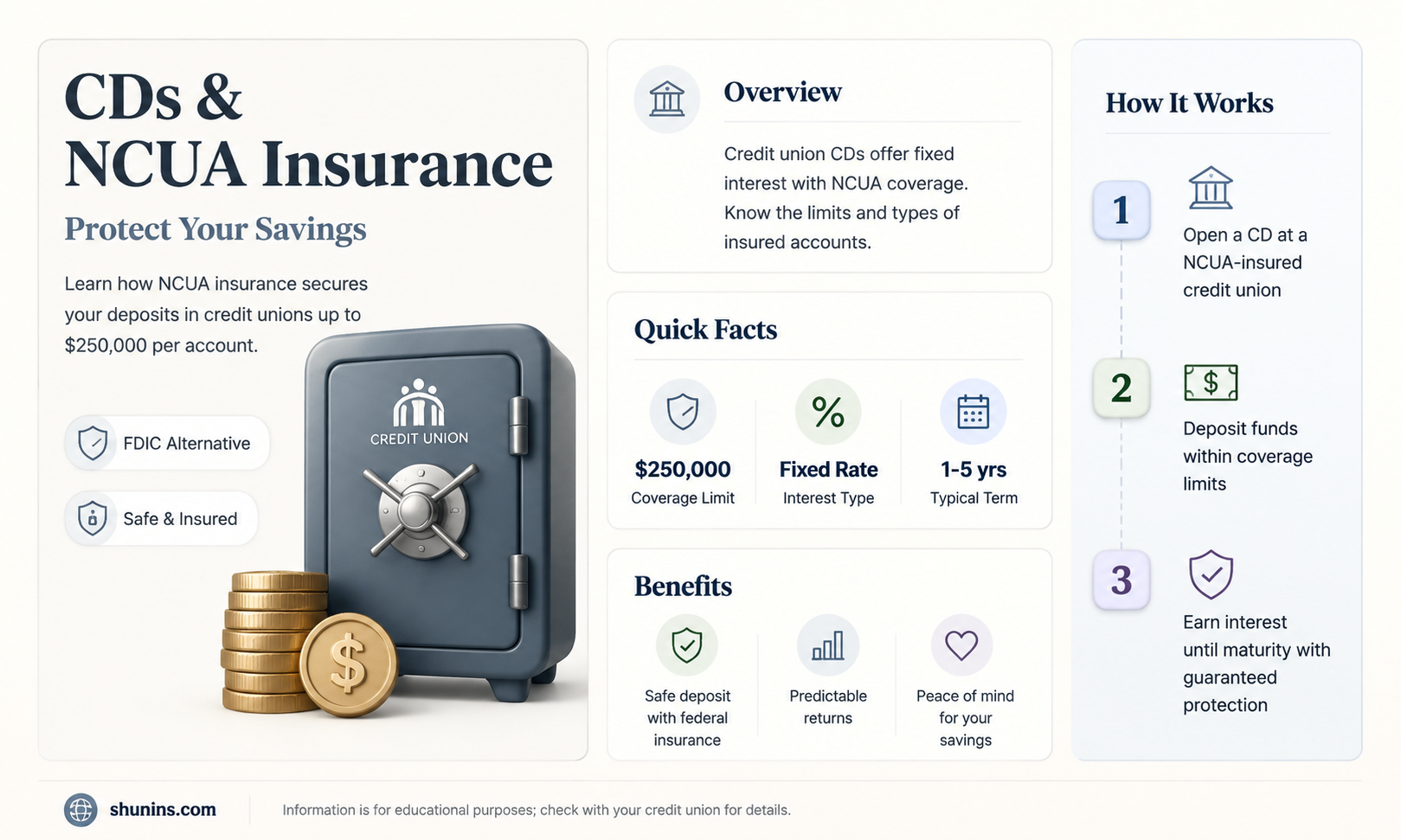

Certificates of deposit are considered one of the safest and lowest-risk investments due to their insurance protection. They are insured by the National Credit Union Administration (NCUA) or the Federal Deposit Insurance Corporation (FDIC). This means that even if the bank or credit union fails, your investment is protected up to $250,000 per depositor, per institution. The NCUA was established by Congress in 1970 to provide federal insurance for deposits at credit unions, while the FDIC was created in 1933 to insure deposits at banks. Both organizations offer similar coverage, protecting cash in eligible deposit accounts up to $250,000 and providing security and stability for depositors.

| Characteristics | Values |

|---|---|

| Type of Account | Certificates of Deposit (CDs) |

| Issuing Authority | Banks or Credit Unions |

| Insurer | National Credit Union Administration (NCUA) or Federal Deposit Insurance Corporation (FDIC) |

| Insurance Coverage | Up to $250,000 per depositor, per institution |

| Risk Profile | Low-risk |

| Investment Returns | Guaranteed returns with higher interest rates than regular savings accounts |

| Access to Funds | Limited during the term |

| Format | Electronic or Paper |

| Safety | Insured and protected even if the financial institution fails |

Explore related products

What You'll Learn

- CDs are insured by the National Credit Union Administration (NCUA) or Federal Deposit Insurance Corporation (FDIC)

- The NCUA provides federal insurance for deposits at credit unions

- The FDIC provides federal insurance for deposits at banks

- CDs are considered low-risk investments with guaranteed returns

- CDs are insured up to \$250,000 per depositor, per institution

![]()

CDs are insured by the National Credit Union Administration (NCUA) or Federal Deposit Insurance Corporation (FDIC)

Certificates of Deposit (CDs) are considered one of the safest and easiest investment options due to their insurance protection. They are insured by the National Credit Union Administration (NCUA) or the Federal Deposit Insurance Corporation (FDIC). The NCUA and FDIC are independent federal agencies that provide government-backed deposit account insurance for consumers in the United States.

The NCUA provides federal insurance for deposits at credit unions, while the FDIC provides federal insurance for deposits at banks. Both organizations protect individual accounts up to a limit of $250,000 per depositor, per institution. This means that even if the financial institution fails, your investment is protected up to the insurance limit. For example, a $250,000 CD in a single-owner account would be fully insured in the event of a bank failure.

The insurance coverage provided by the NCUA and FDIC is automatic. Credit union members do not need to apply for share insurance coverage as it is provided when they join a federally insured credit union. Similarly, most CD accounts at FDIC-insured banks are automatically covered. However, it is important to note that some CD accounts, such as those investing in foreign banks, may not carry deposit insurance even when held at an FDIC member bank.

The NCUA and FDIC cover a variety of common account types, including free checking accounts and high-yield savings accounts. The NCUA also insures retirement accounts, such as IRA and KEOGH accounts, up to $250,000. Additionally, the NCUA provides an online tool to check if a credit union is an NCUA-insured institution, while the FDIC offers the BankFind Suite tool to verify if a bank is FDIC-insured.

Changing Life Insurance Tax Laws: Who Benefits?

You may want to see also

Explore related products

![]()

The NCUA provides federal insurance for deposits at credit unions

The National Credit Union Administration (NCUA) is an independent federal agency established by Congress in 1970 to regulate, charter and supervise federal credit unions. The NCUA operates and manages the National Credit Union Share Insurance Fund, which insures deposits of over 143 million account holders in all federal credit unions and most state-chartered credit unions.

The Share Insurance Fund is similar to deposit insurance coverage provided by the Federal Deposit Insurance Corporation. Credit union members are automatically covered by the Share Insurance Fund when they join a federally insured credit union. The fund insures individual accounts at federally insured credit unions up to $250,000, and a member's interest in all joint accounts combined is insured up to the same amount. The fund also separately protects IRA and KEOGH retirement accounts up to $250,000.

The NCUA does not insure money invested in stocks, bonds, mutual funds, life insurance policies, annuities, or municipal securities, even if these investment or insurance products are sold at a federally insured credit union. Credit unions are required to disclose that these products are not deposits or other obligations of the credit union and are not guaranteed by the credit union. The NCUA also does not insure safe deposit boxes or their contents and does not insure digital assets such as cryptocurrencies.

Credit union members can use the NCUA's Share Insurance Estimator to calculate the amount of insured funds at a federally insured credit union. The NCUA provides several resources to help credit union members understand their share insurance coverage, including brochures, pamphlets, and booklets available in English and Spanish.

Life Insurance: Free Sources and Where to Find Them

You may want to see also

Explore related products

![]()

The FDIC provides federal insurance for deposits at banks

The Federal Deposit Insurance Corporation (FDIC) provides federal insurance for deposits at banks. This insurance covers deposits in all types of accounts at FDIC-insured banks, including Certificates of Deposit (CDs). FDIC deposit insurance protects your money in the event of a bank failure, and coverage is automatic when you open one of these account types. Your deposits are insured for up to $250,000 per depositor, per FDIC-insured bank, and per account ownership category.

The FDIC deposit insurance does not cover non-deposit investment products, even if they are offered by FDIC-insured banks. It also does not cover the default or bankruptcy of any non-FDIC-insured institution. To determine if your bank is FDIC-insured, you can use the BankFind Suite search tool.

Certificates of Deposit (CDs) are considered one of the safest and easiest investments due to their insurance protection. They are a type of time deposit offered by banks and are insured by either the National Credit Union Administration (NCUA) or the FDIC. This means that even if the bank or credit union fails, your investment is protected up to the insurance limit of $250,000. CDs are generally viewed as low-risk because they are insured, guaranteeing your money up to the specified limit.

The NCUA, established by Congress in 1970, provides insurance for member share accounts at federally insured credit unions. The insurance is automatic when one joins a federally insured credit union, covering individual accounts for up to $250,000. The NCUA also separately protects IRA and KEOGH retirement accounts for up to $250,000.

Evangelistic Center: Was Truman's Insurance Enough?

You may want to see also

Explore related products

![]()

CDs are considered low-risk investments with guaranteed returns

Certificates of Deposit (CDs) are insured by the National Credit Union Administration (NCUA) or the Federal Deposit Insurance Corporation (FDIC). This insurance covers up to \$250,000 per depositor, per institution, in the event of a bank failure. This means that even if the bank or credit union fails, your investment is protected up to the insurance limit. As a result, CDs are considered a safe and low-risk investment option.

CDs are considered low-risk investments because they offer guaranteed returns. When you open a CD account, you can choose the term, which can range from a few months to several years. During this time, your deposit earns a guaranteed interest rate, which is fixed, meaning that overall volatility will not impact the performance of your savings. At the end of the term, you receive your initial deposit back, along with the interest accrued. This guaranteed return is in contrast to other investments, such as stocks, which can offer higher returns but also carry a higher risk of loss.

The longer you save with a CD and the more you deposit, the greater your interest accrual will be. The interest rate attached to a CD typically increases with the length of the term, with longer-term CDs offering higher interest rates than shorter-term ones. This incentivizes savers to invest for longer periods. Additionally, CDs usually offer higher interest rates than regular savings accounts, allowing for a modest return on investment with minimal risk.

While CDs are considered low-risk, it is important to note that they may not be suitable for every situation. CDs are best suited for short- to medium-term financial goals, typically within a timeframe of less than five years. For long-term goals, such as retirement planning, other investments like stocks and mutual funds may offer better returns over time. Additionally, CDs have limited access to funds during the term, and there may be penalties for early withdrawal. Therefore, it is important to consider your financial goals and time horizon before investing in CDs.

In summary, CDs are considered low-risk investments due to the guaranteed returns they offer, backed by federal insurance. They provide a stable option for building savings, particularly for short- to medium-term financial goals. However, it is important to weigh the benefits against the potential limitations before investing in CDs.

Life Insurance Proceeds: What Taxes Are Imposed?

You may want to see also

![]()

CDs are insured up to \$250,000 per depositor, per institution

Certificates of Deposit (CDs) are considered one of the safest investment options due to their insurance protection. The Federal Deposit Insurance Corporation (FDIC) and the National Credit Union Administration (NCUA) insure CDs. These organisations protect your deposits up to a limit of $250,000 per depositor, per institution. This means that even if the financial institution fails, your investment is protected.

The FDIC was created in 1933 after a series of bank failures in the 1920s and early 1930s, during the Great Depression. Since the introduction of FDIC insurance in 1934, no depositor has lost their insured deposits. The NCUA was established later, in 1970, to insure member share accounts at federally insured credit unions. Like the FDIC, the NCUA also has a perfect record, and no one has lost insured deposits at a federally insured credit union.

Both organisations insure individual accounts at federally insured credit unions up to $250,000, and a member's interest in all joint accounts combined is insured up to $500,000. The NCUA also separately protects IRA and KEOGH retirement accounts up to $250,000. The NCUA and FDIC cover a variety of common account types at member institutions, including free checking accounts and high-yield savings accounts.

It is important to note that not all CDs are insured. Some types of CDs don't carry deposit insurance, even when held at an FDIC or NCUA-insured bank. For example, CDs that involve investing money in foreign banks are uninsured. CDs purchased through a non-bank institution, such as a brokerage firm, may also be uninsured.

Benefit Term Life Insurance: What's the Deal?

You may want to see also

Frequently asked questions

Yes, they are insured by the National Credit Union Administration (NCUA).

The NCUA provides federal insurance for up to $250,000 per depositor, per account ownership category.

The NCUA covers a variety of common account types, including free checking accounts, retirement accounts, and high-yield savings accounts.

Yes, CDs are considered one of the safest and easiest investments due to their insurance protection. They are typically low-risk and provide guaranteed returns.

The NCUA provides an online tool to check if a credit union is an NCUA-insured financial institution. Additionally, federally insured credit unions are required to disclose their membership on their websites and at teller stations.