The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the US government that protects and reimburses your deposits up to a legal limit of $250,000 if your FDIC-insured bank fails. FDIC deposit insurance covers checking accounts, savings accounts, money market deposit accounts (MMDAs), and certificates of deposit (CDs). However, it's important to note that not all financial products are covered by FDIC insurance, and customers should check with their bank to understand the specifics of their coverage.

| Characteristics | Values |

|---|---|

| Agency | Federal Deposit Insurance Corporation (FDIC) |

| Type of Agency | Independent government agency |

| Purpose | Protects against loss of deposit at many banks |

| Coverage | Up to $250,000 per depositor, per FDIC-insured bank, per ownership category |

| Coverage Calculation | Dollar-for-dollar, principal plus any interest accrued or due to the depositor |

| Coverage for Joint Accounts | Up to $500,000 for the same shared account ($250,000 per co-owner) |

| Coverage for Prepaid Cards | Up to $250,000 if certain FDIC requirements are met |

| Coverage for Investment Accounts | Not covered by FDIC insurance |

| Coverage for Credit Unions | Not covered by FDIC; insured by the National Credit Union Administration (NCUA) |

| Coverage for U.S. Treasury Bills, Notes, and Bonds | Covered by FDIC when purchased through an insured institution |

| Checking Accounts Coverage | Most checking accounts are covered by FDIC insurance |

| Banks Offering FDIC Insurance | Wells Fargo, Capital One Bank, Ally Bank, Goldman Sachs Bank USA |

Explore related products

What You'll Learn

![]()

The Federal Deposit Insurance Corporation (FDIC)

The FDIC protects bank account holders against loss, up to a certain amount, if their bank or thrift institution fails. The FDIC does not insure all banking institutions or types of financial accounts. Eligible bank accounts like checking accounts, savings accounts, negotiable orders of withdrawal (NOW), money market deposit accounts (MMDA), and certificates of deposit (CD) are insured up to $250,000 for principal and interest. The FDIC insurance limit was initially $2,500 per ownership category and has been increased several times over the years. Since the enactment of the Dodd-Frank Wall Street Reform and Consumer Protection Act in 2010, the FDIC insures deposits in member banks up to $250,000 per ownership category.

Deposit insurance is calculated dollar-for-dollar, including principal and any interest accrued or due to the depositor, through the date of default. For example, if a customer had a CD account in her name with a principal balance of $195,000 and $3,000 in accrued interest, the full $198,000 would be insured. In the unlikely event of a bank failure, the FDIC responds in two ways. First, as the insurer of the bank's deposits, the FDIC pays insurance to depositors up to the insurance limit. Typically, the FDIC pays insurance within a few days after a bank closing, usually by either providing each depositor with a new account at another insured bank for an amount equal to the insured balance of their account at the failed bank or issuing a check for the insured balance. Second, the FDIC acts as a receiver tasked with protecting the depositors and maximizing the recoveries for the creditors of the failed institution.

The FDIC is managed by a five-member Board of Directors, including a Chairman, Vice Chairman, Appointive Director, the Comptroller of the Currency, and the Director of the Bureau of Consumer Financial Protection. No more than three members of the Board can be from the same political party.

Schwab Accounts: Are They Federally Insured?

You may want to see also

Explore related products

![]()

FDIC insurance covers up to $250,000

The Federal Deposit Insurance Corporation (FDIC) is an independent government agency that protects customers against loss of deposit if their bank fails. FDIC insurance covers depositors' accounts at each insured bank, dollar-for-dollar, including principal and any accrued interest through the date of the insured bank's closing, up to the insurance limit. The standard maximum deposit insurance amount is $250,000 per depositor, per insured bank, for each account ownership category. This means that if a person has a certificate of deposit at Bank A and a certificate of deposit at Bank B, each account would be insured separately up to $250,000.

FDIC insurance covers checking, savings, and other deposit accounts up to $250,000. This includes money market deposit accounts (MMDAs) and certificates of deposit (CDs). The $250,000 limit is per account owner, not per account. For example, a couple with a joint checking account that's FDIC-insured can receive insurance for up to $500,000 for the same shared account ($250,000 per co-owner). FDIC insurance also covers retirement accounts, with the total amount insured up to a maximum of $250,000.

It's important to note that FDIC insurance does not cover all types of accounts or financial products. Investment options, such as stocks, bonds, mutual funds, annuities, and life insurance policies, are not insured by the FDIC. Additionally, the FDIC does not insure regular shares and share draft accounts held at credit unions; these are typically insured by the National Credit Union Administration (NCUA).

To check if your accounts are fully covered, you can use the FDIC's Electronic Deposit Insurance Estimator (EDIE) by entering information about your accounts. You can also look for the FDIC insurance logo on a bank's website or use the FDIC's BankFind tool to determine if a banking institution is insured.

Are Your CDs Insured?

You may want to see also

Explore related products

![]()

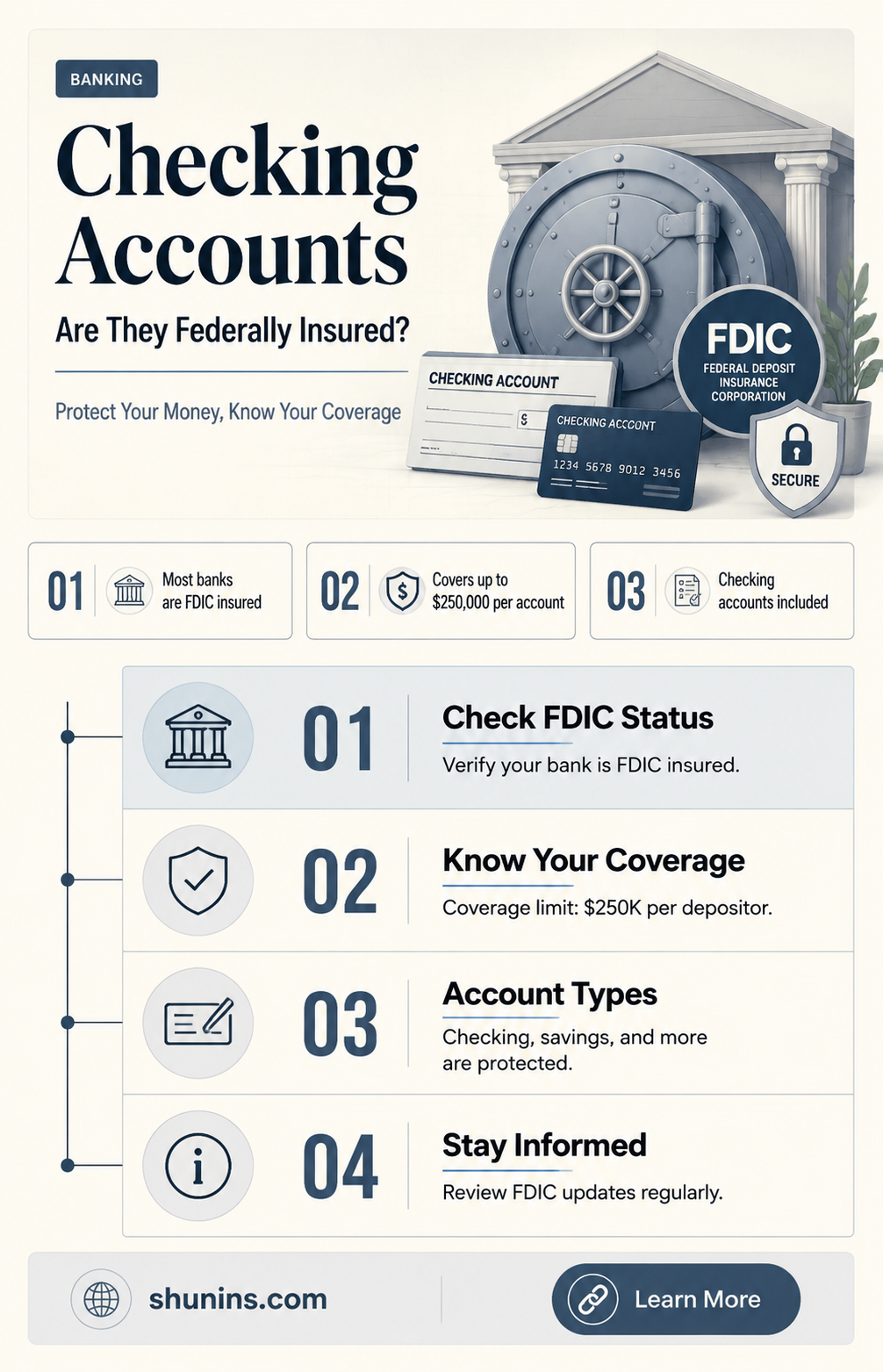

Checking accounts are insured by the FDIC

Checking accounts are insured by the Federal Deposit Insurance Corporation (FDIC), an independent agency of the US government. The FDIC was created by the federal government during the Depression in 1933 to protect customers against losses and maintain public confidence in the banking system.

The FDIC insures checking accounts and other deposit accounts, such as savings accounts, money market deposit accounts (MMDAs), and certificates of deposit (CDs). It does not cover investment accounts or losses due to fraud and theft. When you open a checking account, you may see a notice stating that the account is FDIC-insured. Banks will usually advertise this protection to their customers.

The FDIC insures deposits up to a standard maximum of $250,000 per depositor, per bank, per ownership category. This includes the principal amount and any interest accrued. For example, if a customer had a checking account with a principal balance of $195,000 and $3,000 in accrued interest, the full $198,000 would be insured. In the unlikely event of a bank failure, the FDIC will respond by paying insurance to depositors up to the insured amount.

You can check if your accounts are fully covered by accessing the FDIC's Electronic Deposit Insurance Estimator (EDIE) and entering information about your accounts. It is important to note that not all banks are FDIC-insured, and you can refer to the FDIC's website to determine if your bank is insured and how the coverage applies to your account(s).

US Bank Insurance: Is Your Money Safe?

You may want to see also

Explore related products

![]()

FDIC doesn't cover all banks

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government that protects bank depositors against the loss of their insured deposits in the event of an FDIC-insured bank or savings association failing. FDIC insurance is backed by the full faith and credit of the United States government. However, the FDIC does not cover all banks and financial products.

FDIC deposit insurance only covers certain deposit products, such as checking and savings accounts, money market deposit accounts (MMDAs), and certificates of deposit (CDs). Investment options, such as stocks, bonds, and mutual funds, are not insured by the FDIC. Additionally, the FDIC does not insure regular shares and share draft accounts held at credit unions; these are insured by the National Credit Union Share Insurance Fund, run by the National Credit Union Administration (NCUA).

The FDIC also does not insure all types of financial accounts. Eligible bank accounts like savings accounts, CDs, and checking accounts are insured up to $250,000 for principal and interest. This limit applies per depositor, per FDIC-insured bank, and per ownership category. Deposits held in different ownership categories are separately insured, even if held at the same bank. For example, a revocable trust account with one owner naming three unique beneficiaries can be insured up to $750,000.

To calculate your specific deposit insurance coverage, you can use the FDIC's Electronic Deposit Insurance Estimator (EDIE). This tool will show your deposit insurance coverage once you input your account details.

Certificates of Deposit: Are They Federally Insured?

You may want to see also

![]()

FDIC doesn't cover all types of accounts

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the US government that protects bank depositors against the loss of their insured deposits in the event that an FDIC-insured bank or savings association fails. FDIC insurance is backed by the full faith and credit of the US government.

FDIC insurance covers traditional deposit accounts, and depositors do not need to apply for it. Coverage is automatic whenever a deposit account is opened at an FDIC-insured bank or financial institution. However, not all products offered by banks are covered by FDIC insurance. FDIC deposit insurance only covers certain deposit products, such as checking and savings accounts, money market deposit accounts (MMDAs), and certificates of deposit (CDs).

The FDIC does not insure all banking institutions or types of financial accounts. For example, it does not insure regular shares and share draft accounts held at credit unions. Instead, these are insured by the National Credit Union Share Insurance Fund, run by the National Credit Union Administration (NCUA).

The FDIC also does not cover investment products that are not deposits, such as mutual funds, annuities, life insurance policies, stocks, bonds, and municipal securities. Additionally, the contents of a safe deposit box housed at a bank are not covered by FDIC insurance.

To calculate your specific deposit insurance coverage, you can use the FDIC's Electronic Deposit Insurance Estimator (EDIE) and enter information about your accounts. This tool can help you determine if all your cash is insured and provide you with detailed information about your specific deposit insurance coverage.

Chase Bank: Is Your Money Federally Insured?

You may want to see also

Frequently asked questions

The FDIC is an independent government agency that protects and reimburses your deposits up to a legal limit of $250,000 if your bank fails.

Banks will usually advertise this protection for their customers, or you can ask a banker when considering opening a new account. You can also check the FDIC's website for more information.

The FDIC insures up to $250,000 per depositor, per FDIC-insured bank, per ownership category. For example, a couple with a joint checking account can receive insurance for up to $500,000 for the same shared account.