The Consolidated Omnibus Budget Reconciliation Act, or COBRA, allows individuals to remain on their employer's health insurance plan for a limited period after they lose their job. While COBRA can be a great option for maintaining health coverage, the premiums can be expensive, as individuals are responsible for paying the original premiums plus the amount previously covered by their employer. This has led many to question whether these COBRA insurance premiums are tax-deductible.

| Characteristics | Values |

|---|---|

| COBRA insurance | Stands for Consolidated Omnibus Budget Reconciliation Act |

| Allows you to remain on your employer's group policy when you lose your job | |

| Coverage ranges from 18 to 36 months | |

| You have 60 days to make the election | |

| You are responsible for paying your original premiums plus the amount your employer previously paid | |

| You can deduct your COBRA costs if you itemize deductions on your federal income tax return | |

| You can pay COBRA premiums out of a health savings account | |

| You can only deduct costs that were not reimbursed or paid for on your behalf | |

| You are no longer eligible for the COBRA premium subsidy once you become eligible for other group health coverage or Medicare | |

| The premium subsidy is not included in the individual's income |

Explore related products

What You'll Learn

- COBRA insurance costs may be tax-deductible if you itemize deductions

- You can't deduct COBRA premiums if you're self-employed

- You can deduct COBRA costs from a health savings account

- COBRA coverage lasts 18-36 months after losing your job

- You must notify your plan when you're no longer eligible for the COBRA subsidy

![]()

COBRA insurance costs may be tax-deductible if you itemize deductions

The Consolidated Omnibus Budget Reconciliation Act, or COBRA, allows you to remain on your employer's group health insurance policy when you lose your job, face a reduction in work hours, or experience other life events. While COBRA can provide valuable peace of mind during periods of transition, it's no secret that the premiums can be expensive. After all, you are now responsible for covering the cost of premiums that your employer previously paid.

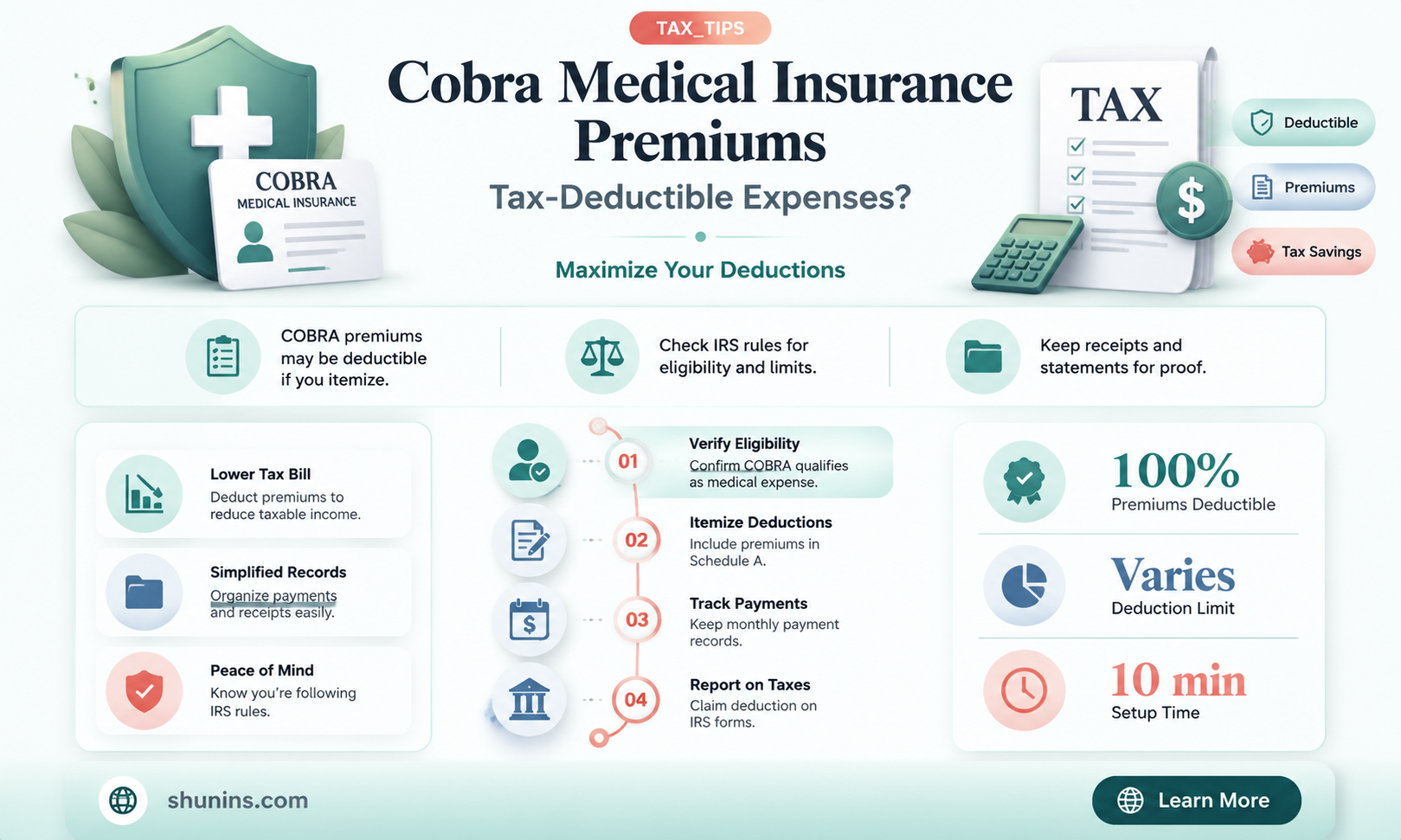

The good news is that you may be able to offset the financial burden of COBRA insurance costs by itemizing your deductions. According to federal tax laws, unreimbursed COBRA payments are deductible as medical expenses on your 1040 tax return. This means that you can deduct the cost of COBRA premiums in the same way you would deduct unreimbursed payments for legal medical services provided by healthcare professionals.

However, it's important to note that you can only deduct the portion of your medical expenses that exceeds 7.5% of your adjusted gross income (AGI). Therefore, keeping accurate records of the total amounts you've paid for medical and dental care for yourself, your spouse, and your dependents is crucial to ensure you claim the maximum deduction. Additionally, you cannot include any COBRA premiums paid by someone else or covered by the COBRA premium assistance credit under the American Rescue Plan Act of 2021 in your deduction calculations.

If itemizing deductions doesn't make sense for your situation, and your total medical and dental expenses don't reach 7.5% of your AGI, there may be another option for a slight tax break on COBRA premiums. If you have a health savings account (HSA), you could use those tax-exempt funds to pay your COBRA premiums. This strategy allows you to lower your overall healthcare costs by setting aside pretax dollars and using them tax-free on qualifying medical expenses.

Private Insurance vs. Medicaid: Which Offers Better Healthcare Coverage?

You may want to see also

Explore related products

![]()

You can't deduct COBRA premiums if you're self-employed

COBRA, or the Consolidated Omnibus Budget Reconciliation Act, allows individuals to remain on their employer's group health insurance policy after they are no longer employed by that company. This coverage can range from 18 to 36 months, and individuals have 60 days to make the election. However, COBRA premiums can be expensive, as individuals are responsible for paying their original premiums plus the amount previously covered by their employer.

While health insurance premiums are typically tax-deductible if you are not receiving reimbursement elsewhere, this does not apply to COBRA if you are self-employed. This is because, for self-employed individuals, the insurance plan must be established under their name or their business's name, and COBRA policies are set up under the name of the previous employer. Therefore, COBRA premiums do not qualify for the self-employed health insurance deduction.

It is important to note that the rules for tax deductions can be complex and may change annually. While COBRA premiums cannot be deducted as self-employed health insurance, they may be deductible as itemized medical expense deductions on Schedule A. This is applicable if your total out-of-pocket medical expenses exceed 7.5% of your Adjusted Gross Income (AGI) and your total itemized deductions are greater than your standard deduction.

Additionally, there are other opportunities for tax deductions that self-employed individuals may be able to take advantage of, such as deductions for medical, dental, and long-term care insurance premiums. These deductions can help offset the rising costs of healthcare and save money.

Aetna Insurance: Understanding Its Role in Medicaid Coverage

You may want to see also

Explore related products

$24.5

![]()

You can deduct COBRA costs from a health savings account

Losing your job can be scary, especially when it comes to the loss of income and health coverage. If you have a Health Savings Account (HSA), you may be wondering how job loss affects your HSA and whether you can use your HSA funds to help pay the premiums for COBRA continuation coverage.

Firstly, it's important to know that HSAs are portable. This means that you own the account regardless of termination, whether it is voluntary or involuntary. HSA funds are yours to spend on eligible healthcare expenses, even if you are no longer enrolled in an HSA-qualified high-deductible health plan (HDHP). After age 65, you can also use your HSA funds to pay for other expenses without penalty.

Now, can you deduct COBRA costs from your HSA? Generally, insurance premiums are not on the IRS-approved list of eligible HSA expenses. However, there is an exception for COBRA. According to IRS Publication 969, "You can't treat insurance premiums as qualified medical expenses unless the premiums are for: Long-term care insurance or COBRA continuation coverage premiums". Therefore, you can deduct COBRA continuation coverage premiums from your HSA. Additionally, if you are unemployed and receiving unemployment compensation, you can purchase other healthcare insurance with your HSA.

It is important to note that you cannot pay COBRA premiums with a Flexible Spending Account (FSA). However, depending on the plan setup, you may be able to pay for COBRA with a Health Reimbursement Arrangement (HRA). Contact your benefits administrator for more information. Remember, enrollment in a qualified HDHP is always required to open or contribute to an HSA.

Village Medical at Walgreens: Insurance Options and Coverage

You may want to see also

Explore related products

![]()

COBRA coverage lasts 18-36 months after losing your job

If you've lost your job, the Consolidated Omnibus Budget Reconciliation Act, or COBRA, allows you to maintain your employer-provided health insurance for a limited time. This is helpful if you want to continue seeing the same doctors and receiving the same health plan benefits.

COBRA coverage lets you stay on your job-based health insurance for a period ranging from 18 to 36 months after your employment ends. This duration is typically 18 months, but it can be longer in certain cases, such as if you experience another qualifying event during this period. It's important to note that you usually have to pay the full premium yourself, plus a small administrative fee, and these premiums can be expensive.

The length of your COBRA coverage depends on several factors. Firstly, it can last until 36 months after the date that benefits under the policy would have otherwise terminated. Secondly, it can end if you fail to make timely premium payments. Lastly, it can terminate on the date the group contract is terminated or when your employer ends their participation in the group contract.

To ensure you receive your full benefits, it's important to notify your employer or plan administrator of your election to continue coverage within 60 days of the qualifying event. This qualifying event could be your job loss, a reduction in hours, or another specified life change. Once you've made this election, your coverage must be provided from the date your previous coverage ended.

Dental Implants: Are They Covered by Medical Insurance?

You may want to see also

Explore related products

![]()

You must notify your plan when you're no longer eligible for the COBRA subsidy

If you become eligible for other group health coverage or Medicare, you lose eligibility for the COBRA premium subsidy. In such cases, you must notify your health plan provider in writing that you are no longer eligible for the COBRA subsidy. This notification must be made even if you continue to receive COBRA coverage and have to pay the full premium without the subsidy.

Failing to notify your health plan provider and continuing to receive the COBRA subsidy after becoming eligible for other group health coverage or Medicare may result in a penalty under IRC § 6720C. This penalty is equal to 110% of the subsidy provided after becoming eligible for other coverage. Therefore, it is important to inform your plan promptly when you are no longer eligible for the COBRA subsidy.

If you fail to notify your plan about the change in eligibility, you should self-report and inform the IRS that you are subject to the penalty. This can be done by calling the IRS toll-free customer helpline at 800-8. Additionally, anyone who suspects that an individual may be receiving the COBRA subsidy after becoming eligible for other group coverage or Medicare can report this suspected tax fraud activity to the IRS. This can be done by completing Form 3949-A, which is available on the IRS website. The form should be printed and mailed to the IRS, along with any relevant information about the individual in question.

It is important to note that the COBRA premium subsidy is not considered part of an individual's income. However, there is a phase-out of eligibility for the subsidy, which can increase the tax liability for high-income individuals. This phase-out applies to individuals with a modified adjusted gross income exceeding $125,000, or $250,000 for those filing joint returns.

Understanding Medical Insurance Fraud: Scams and Schemes

You may want to see also

Frequently asked questions

COBRA stands for Consolidated Omnibus Budget Reconciliation Act, which allows you to remain on your employer's group health insurance policy for up to 18 months after losing your job.

Yes, COBRA insurance premiums are tax-deductible as medical expenses on your tax return. However, you can only deduct the premiums you paid out of pocket and not any amounts reimbursed by your employer or other sources.

If you lose your job, are laid off, or experience a reduction in work hours, resulting in losing eligibility for employer-provided health insurance, you may qualify for COBRA. You must have been enrolled in the health coverage before losing eligibility, and the coverage must still be available to other employees.

Typically, COBRA coverage lasts for up to 18 months, but it can be extended to 29 months in certain situations, such as if you become disabled within 60 days of enrolling.

Yes, you can explore other options, such as buying a private health plan or taking advantage of tax subsidies and deductions offered under the Affordable Care Act (ACA). Additionally, if you are self-employed or a small business owner, you may be eligible for specific health insurance deductions.