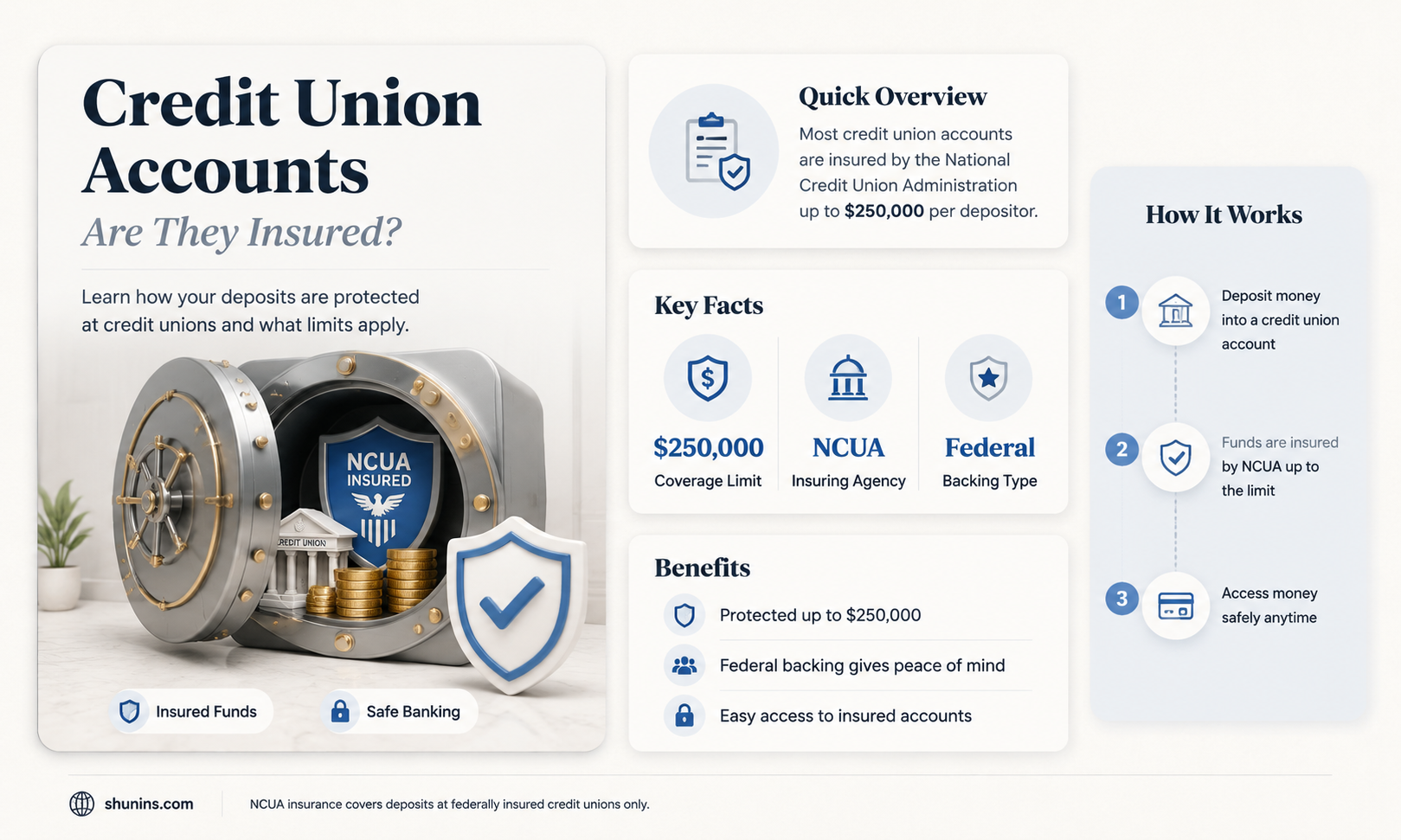

Credit unions are insured by the National Credit Union Administration (NCUA), a US government agency. The NCUA provides credit union members with coverage of up to $250,000 on deposit accounts, including checking, savings, and money market accounts. This insurance is similar to the Federal Deposit Insurance Corporation (FDIC) coverage provided to customers of traditional banks, ensuring that members' deposits are protected in the event of a credit union failure. While deposits up to $250,000 are insured, investment losses and contents of safe deposit boxes are not covered by the NCUA.

| Characteristics | Values |

|---|---|

| Credit union accounts insured by | The National Credit Union Association (NCUA) |

| NCUA insured amount | Up to $250,000 per depositor, per institution, per ownership category |

| NCUA insured accounts | Checking, savings, certificates of deposit, trust accounts, custodial accounts, traditional and Roth IRAs without an investment component |

| NCUA insured deposits | 100% of the amount, including principal and any accrued dividend |

| NCUA insurance estimator | Available on the NCUA website to help understand insurance coverage |

| NCUA-insured credit union identification | Display the official NCUA insurance sign in their advertising and on their website |

Explore related products

What You'll Learn

- The National Credit Union Association (NCUA) insures credit union deposits

- NCUA insurance covers up to $250,000 per depositor

- NCUA insurance covers checking, savings, and money market accounts

- NCUA insurance does not cover investment losses or safe deposit box contents

- NCUA-insured credit unions display the official NCUA insurance sign

![]()

The National Credit Union Association (NCUA) insures credit union deposits

The National Credit Union Administration (NCUA) insures credit union deposits, providing peace of mind to members. This insurance coverage is similar to that offered by the Federal Deposit Insurance Corporation (FDIC) for traditional bank customers. The NCUA, like the FDIC, is an independent branch of the federal government, ensuring that your deposits are protected.

The NCUA provides insurance coverage of up to $250,000 per depositor, per institution, and per ownership category. This means that if you have both single and joint accounts at the same credit union, each type of account is insured up to the $250,000 limit. Ownership categories include common types such as individual, joint, retirement, and trust accounts. It's important to note that deposits beyond $250,000 are not insured, even in eligible accounts. However, you can distribute your funds across different institutions to maximize coverage.

The NCUA insurance covers various deposit accounts, including checking, savings, money market accounts, and certificates of deposit. It also covers some retirement and employee benefit plans. The coverage extends to federally insured credit unions, and you can use the NCUA's credit union locator to confirm if a particular institution is NCUA-backed. Additionally, federally insured credit unions will display the official NCUA insurance sign in their advertising and on their websites.

In the unlikely event that a credit union fails, the NCUA will attempt to sell its deposits and loans to another credit union. If the sale is successful, customers' accounts are seamlessly transferred. If not, the NCUA will promptly send customers a check for the insured balance of their deposits. This process ensures that credit union members receive their entitled funds, even in the event of their credit union's closure.

The NCUA insurance provides a sense of security for those with credit union accounts, knowing that their deposits are protected by the federal government. It is important to understand the coverage limits and ownership categories to maximize the benefits of NCUA insurance.

Is Your Money Safe on GDAX?

You may want to see also

Explore related products

![]()

NCUA insurance covers up to $250,000 per depositor

Credit unions are insured by the National Credit Union Association (NCUA), an independent branch of the federal government. The NCUA provides credit union members with coverage of up to $250,000 on deposit accounts, which includes checking, savings, and money market accounts, as well as certificates of deposit. This coverage is similar to what the Federal Deposit Insurance Corporation (FDIC) provides to customers of traditional banks. The NCUA's insurance covers each depositor, per institution, per ownership category, and the cost of this insurance is covered by the credit unions themselves, not the customers.

The ownership category refers to the type of account, such as single or joint accounts. If a customer has both a single and a joint account at the same institution, each account is insured up to the $250,000 limit. Additionally, retirement plans and employee benefit plans are covered as separate ownership categories. It is important to note that investment losses are not covered, even if the investments were made through an insured credit union, and neither are the contents of safe deposit boxes.

In the event that a credit union fails, the NCUA will attempt to sell its deposits and loans to another credit union. If this sale is successful, customers' accounts are simply transferred. If the sale is unsuccessful, the NCUA will send customers a cheque for the insured balance of their deposits, typically within a few days of the credit union's closing.

While the standard insurance coverage amount is $250,000 per owner for each individual account, there may be additional insurance coverage for deposits in certain types of accounts, such as Payable-on-Death (POD) and Trust accounts, depending on the number of qualifying named beneficiaries. To help members understand their insurance coverage, the NCUA provides a share insurance estimator on its website.

In summary, NCUA insurance provides peace of mind for credit union members, ensuring that their deposits are protected up to $250,000 per depositor, with certain account types and ownership categories potentially qualifying for additional coverage.

Usaa's Commercial Property Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

NCUA insurance covers checking, savings, and money market accounts

Credit union members' deposits are insured by the National Credit Union Administration (NCUA), an independent branch of the federal government. The NCUA's insurance coverage extends to deposit accounts, including checking, savings, and money market accounts. This means that if a credit union fails, NCUA insurance guarantees that customers will receive the money they are entitled to from their deposit accounts.

The NCUA insurance coverage limit is $250,000 per member-owner for Single Ownership Accounts, Joint Ownership Accounts, and certain retirement accounts like IRAs. The coverage also applies to non-member deposits when permitted by law. Credit union members can use the NCUA's Share Insurance Estimator to calculate the amount of coverage their insured funds have at a federally insured credit union.

It is important to note that NCUA insurance does not cover investment losses, even if the investments were made through an insured credit union. Similarly, the contents of safe deposit boxes are not covered by NCUA insurance. However, some retirement plans and employee benefit plans are covered under NCUA insurance, counting as separate ownership categories.

To confirm if a credit union is NCUA-insured, individuals can use the NCUA's credit union locator tool or look for the official NCUA insurance sign displayed at teller stations and branches of federally insured credit unions. The NCUA website also offers resources and assistance to help members understand their insurance coverage.

Edward Jones Money Market Accounts: Are They Insured?

You may want to see also

Explore related products

![]()

NCUA insurance does not cover investment losses or safe deposit box contents

The National Credit Union Administration (NCUA) is a federal agency that insures credit union depositors. The NCUA's insurance covers many types of share deposits received at a federally insured credit union, including deposits in a share draft account, share savings account, or time deposit such as a share certificate. The insurance covers members' accounts at each federally insured credit union, dollar-for-dollar, including principal and any accrued dividend through the date of the insured credit union's closing, up to the insurance limit.

The insurance limit for NCUA is $250,000 per person, per ownership category, per financial institution. The NCUA also separately protects IRA and KEOGH retirement accounts up to $250,000. However, it's important to note that NCUA insurance does not cover investment losses or safe deposit box contents.

Investment risks, including the possible loss of the principal invested, are not covered by NCUA insurance. This means that if you invest money in stocks, bonds, mutual funds, life insurance policies, annuities, or municipal securities, even if these investment products are sold by a federal credit union, any losses incurred are not insured by the NCUA.

Additionally, the NCUA does not insure the contents of safe deposit boxes. Safe deposit boxes are typically used to store valuable items or important documents, but in the event of theft, damage, or loss, the NCUA will not provide coverage for the contents of these boxes. It is important for credit union members to understand the limitations of NCUA insurance and take appropriate measures to protect their investments and valuable possessions.

Leasing a Vehicle? Prepare for Higher Insurance Costs

You may want to see also

Explore related products

![]()

NCUA-insured credit unions display the official NCUA insurance sign

Credit unions are insured by the National Credit Union Administration (NCUA), an independent branch of the federal government. The NCUA provides credit union members with coverage of up to $250,000 on deposit accounts, including checking, savings, certificates of deposit, trust accounts, custodial accounts, and traditional and Roth IRAs without investment components. This is similar to the Federal Deposit Insurance Corporation (FDIC), which insures deposits in traditional banks.

The NCUA's Share Insurance Fund insures individual accounts at federally insured credit unions up to $250,000, and a member's combined interest in all joint accounts is also insured up to $250,000. The Share Insurance Fund also separately protects IRA and KEOGH retirement accounts up to $250,000. It is important to note that the NCUA does not insure money invested in stocks, bonds, mutual funds, life insurance policies, annuities, cryptocurrencies, or municipal securities, even if these investment or insurance products are sold at a federally insured credit union.

To ensure members can easily identify federally insured credit unions, all such institutions are required to display the official NCUA insurance sign at each teller station, where insured account deposits are usually received in their principal place of business and in all branches. Additionally, they must display the sign on their website and wherever they accept share deposits or open accounts. Credit union members can confirm their credit union's federal insurance status using the NCUA's Credit Union Locator tool.

The NCUA's Share Insurance Estimator helps consumers, credit unions, and their members understand how its share insurance rules apply to their accounts, clarifying what is insured and what portion, if any, exceeds coverage limits. This tool is available on the NCUA's consumer website, MyCreditUnion.gov, and can be used for personal, business, or government accounts. Members with questions about their share insurance coverage can also call 1.800.755.1030, select option 1, and speak to a representative Monday through Friday, 8 a.m. to 5 p.m. Eastern, or send an email inquiry to [email protected].

Death Insurance: Taxable Money or Not?

You may want to see also

Frequently asked questions

It means that the federal government ensures that you receive the money you're entitled to from your deposits in the unlikely event that something causes your credit union to go out of business.

The NCUA insures up to $250,000 per depositor, per institution, per ownership category. The most common ownership categories are Individual, Joint, Retirement, Revocable Trust, and Irrevocable Trust Accounts.

Federally insured credit unions display the official NCUA insurance sign in their advertising and on their websites where they accept deposits or open accounts. You can also use the NCUA's credit union locator or its share insurance estimator to better understand your insurance coverage.