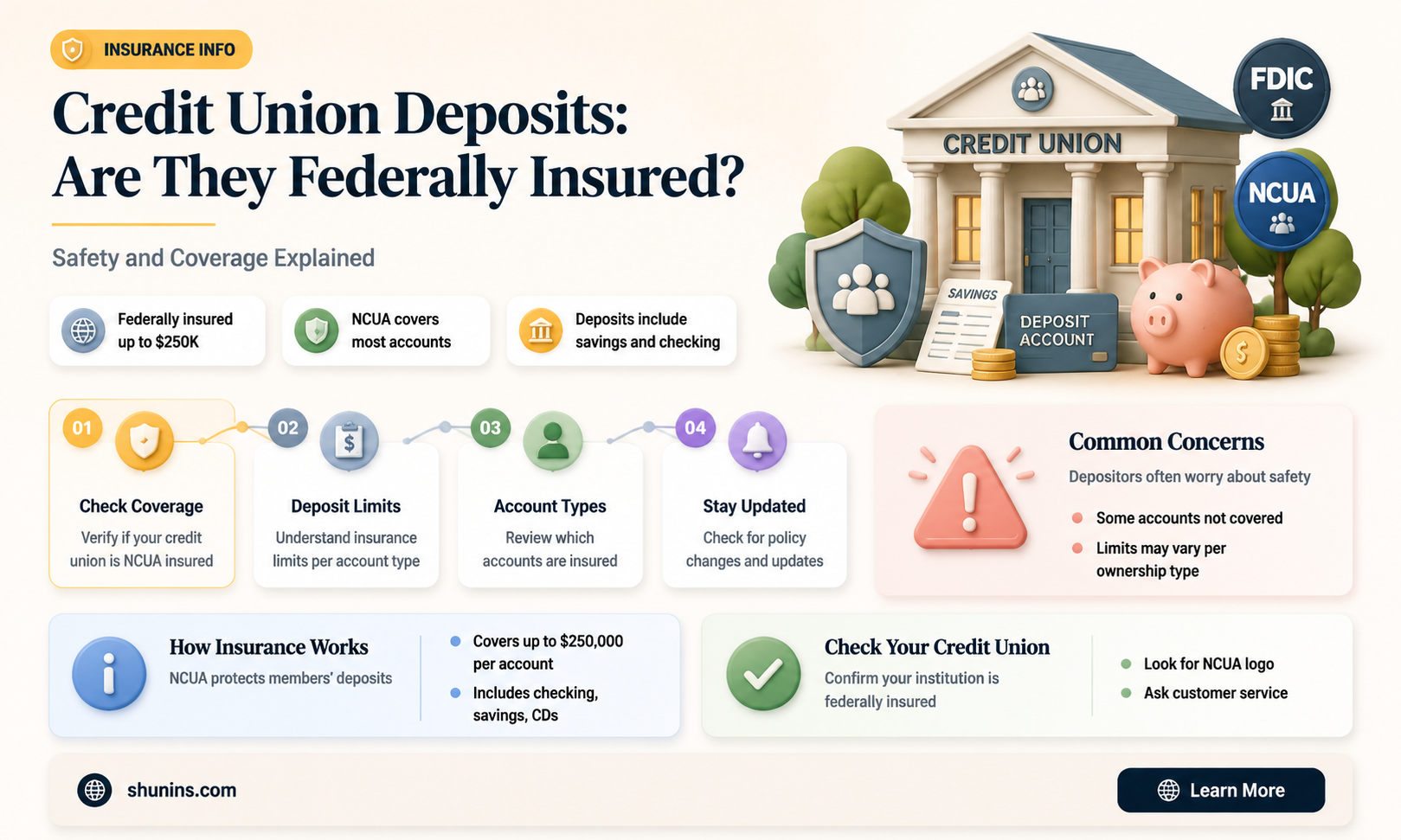

Credit unions are not-for-profit financial institutions that accept deposits, make loans, and provide other financial services. They are owned and controlled by their members, who elect a volunteer board of directors to manage the union. Members share a common bond, and profits are returned to them in the form of reduced fees, higher savings rates, and lower loan rates. When it comes to deposits, credit unions are federally insured by the National Credit Union Administration (NCUA), which was established by Congress in 1970. The NCUA provides federal insurance for deposits at credit unions, guaranteeing that members' money is protected up to $250,000 per depositor, per federally insured credit union, and per ownership category. This insurance is similar to the deposit insurance provided by the Federal Deposit Insurance Corporation (FDIC) for banks.

| Characteristics | Values |

|---|---|

| Credit union deposits federally insured by | The National Credit Union Administration (NCUA) |

| NCUA's counterpart for banks | The Federal Deposit Insurance Corporation (FDIC) |

| NCUA's insurance limit | $250,000 per depositor, per federally insured credit union, per ownership category |

| NCUA's role | Managing the National Credit Union Share Insurance Fund (NCUSIF) |

| NCUA's establishment | Congress in 1970 |

| NCUA's function | Regulating federal credit unions |

| NCUA insurance coverage | Automatic |

| NCUA insured deposits | Cash in eligible deposit accounts, share draft accounts, share savings accounts, single ownership accounts, joint ownership accounts, IRAs and other certain retirement accounts, revocable trust accounts, and irrevocable trust accounts |

| NCUA non-insured deposits | Stocks, bonds, mutual funds, life insurance policies, annuities, municipal securities, safe deposit boxes, and digital assets like cryptocurrencies |

Explore related products

What You'll Learn

![]()

The National Credit Union Share Insurance Fund

The NCUSIF is similar to the deposit insurance coverage provided by the Federal Deposit Insurance Corporation (FDIC). The NCUSIF guarantees that money in a credit union's account is backed by the full faith and credit of the US government. For all federal credit unions and most state-chartered credit unions, the NCUSIF provides up to $250,000 in coverage for each single ownership account. This limit refers to the total of all shares that account owners have at each federally insured credit union.

The NCUSIF insures individual accounts at federally insured credit unions up to $250,000, and a member's interest in all joint accounts combined is insured up to $250,000. The fund also separately protects IRA and KEOGH retirement accounts up to $250,000. Credit union members do not need to apply for this insurance coverage as it is provided automatically when they join a federally insured credit union.

The NCUSIF is funded entirely by participating credit unions, with contributed capital being one percent of insured shares deposited by each federal credit union and all federally insured, state-chartered credit unions. The fund is approximately $13 billion in total, with $2.8 billion in retained earnings and approximately $10 billion in contributed capital from credit unions. The majority of the fund is invested in United States treasury securities, with a portion of the earnings being used to fund NCUA's operations.

Ally Bank: Is Your Money Safe and Federally Insured?

You may want to see also

Explore related products

![]()

Federal Deposit Insurance Corporation

The Federal Deposit Insurance Corporation (FDIC) is a United States government corporation that supplies deposit insurance to depositors in American commercial banks and savings banks. The FDIC was established under the Banking Act of 1933 in response to numerous bank failures during the Great Depression. The FDIC began insuring banks on January 1, 1934, and has since averted bank runs and restored trust in the American banking system. The FDIC's income is derived from insurance premiums on deposits held by insured banks and savings associations, and from interest on the required investment of the premiums in US government securities. The FDIC does not operate on funds appropriated by Congress.

The FDIC provides deposit insurance coverage to depositors in American commercial banks and savings banks. The FDIC insurance limit was initially US$2,500 per ownership category, and this has been increased several times over the years to accommodate inflation. Since the enactment of the Dodd-Frank Wall Street Reform and Consumer Protection Act in 2010, the FDIC insures deposits in member banks up to $250,000 per ownership category. FDIC insurance is backed by the full faith and credit of the government of the United States.

The FDIC is also responsible for examining and supervising financial institutions for safety and soundness and consumer protection, making large and complex financial institutions resolvable, and managing the resolution of failed banks. In its role as a receiver, the FDIC is tasked with protecting the depositors and maximizing the recoveries for the creditors of the failed institution. The FDIC as a receiver is functionally and legally separate from the FDIC acting in its corporate role as a deposit insurer.

The FDIC's counterpart for credit unions is the National Credit Union Administration (NCUA), which provides deposit insurance coverage for credit union members. The NCUA was established by Congress in 1970 to insure member share accounts at federally-insured credit unions. The NCUA manages the National Credit Union Share Insurance Fund (NCUSIF), which guarantees money in a credit union's account, backed by the full faith and credit of the US government. The NCUSIF provides up to $250,000 in coverage for each single ownership account.

Is Your 401(k) Safe? Federal Insurance and Your Retirement

You may want to see also

Explore related products

![]()

NCUA insurance limits

The National Credit Union Administration (NCUA) is a government agency that insures deposits at member credit unions. The NCUA insures deposits at federally insured credit unions through the National Credit Union Share Insurance Fund (NCUSIF). The NCUSIF is similar to the Federal Deposit Insurance Corporation's (FDIC) deposit insurance coverage. The fund is administered by the NCUA and is backed by the full faith and credit of the United States government.

The NCUA provides insurance coverage for various types of accounts, including Single Ownership Accounts, Joint Ownership Accounts, IRAs and other retirement accounts, Revocable Trust Accounts, and Irrevocable Trust Accounts. The insurance limit for each of these accounts is $250,000 per account owner, with certain requirements and structures in place. This limit applies to the total of all shares that account owners have at each federally insured credit union.

It is important to note that the NCUA does not insure all types of investments and assets. For example, money invested in stocks, bonds, mutual funds, life insurance policies, annuities, or municipal securities is not insured by the NCUA, even if these products are sold at a federally insured credit union. Additionally, safe deposit boxes and their contents, as well as digital assets like cryptocurrencies, are not insured by the NCUA.

The NCUA insurance limits provide protection for depositors' funds in the event of a credit union failure. These limits are designed to ensure that members' accounts are covered dollar-for-dollar, including principal and any accrued dividends, up to the specified limit of $250,000. This coverage is automatic for members of federally insured credit unions, and no separate application is required.

Is Your Money Safe? SECU and Federal Insurance

You may want to see also

Explore related products

![]()

Non-member deposits

The NCUA offers share insurance coverage through the National Credit Union Share Insurance Fund (NCUSIF), which is similar to the coverage provided by the Federal Deposit Insurance Corporation (FDIC). The NCUSIF covers up to $250,000 of the total balance of individuals' credit union accounts. For jointly owned accounts, the NCUSIF provides an additional $250,000 for each account holder. The NCUA also insures traditional and Roth IRA, as well as Keogh retirement accounts, up to $250,000 in aggregate.

It is important to note that credit unions must prominently display the official NCUA insurance sign at each teller station and where insured account deposits are normally received. This includes their principal place of business, all branches, and their website if they have one. Credit unions are also required to disclose that certain investment and insurance products are not deposits or obligations of the credit union and are not guaranteed or insured by the credit union.

To determine if a credit union is federally insured, individuals can use the NCUA's Credit Union Locator tool or visit the NCUA website to look up members. The NCUA's Share Insurance Estimator can also help calculate the amount of coverage provided for insured funds at a federally insured credit union.

Fifth Third Bank: Is Your Money Safe?

You may want to see also

Explore related products

![]()

What the NCUA sign indicates

The National Credit Union Administration (NCUA) is a government agency that insures deposits at member credit unions. The NCUA sign indicates that a credit union is federally insured. The sign must be displayed prominently at each teller station, where insured account deposits are usually received, in the credit union's principal place of business and in all its branches. The NCUA sign must also be displayed on the credit union's website and where they accept share deposits or open accounts.

The NCUA sign indicates to members that their accounts are insured and protected. The NCUA's National Credit Union Share Insurance Fund (NCUSIF) guarantees that money in a credit union's account is backed by the full faith and credit of the US government. The fund insures individual accounts at federally insured credit unions up to $250,000, and a member's interest in all joint accounts combined is insured up to the same amount.

The NCUA sign is an important indication of a credit union's insured status. Credit unions are required to include either the official advertising statement or the NCUA official sign on all their advertisements and on their main internet page. The NCUA sign can be downloaded from the NCUA website, and credit unions can also purchase or develop their own signs, as long as they comply with the NCUA's rules and regulations.

The NCUA sign is a crucial indicator of a credit union's financial security and stability. It provides members with peace of mind, knowing that their deposits are insured and protected by the US government. The sign also helps to maintain trust and confidence in the credit union system, as members can be assured that their money is safe and guaranteed, even in the event of a credit union failure.

Chime's FDIC Insurance: Your Money Is Safe

You may want to see also

Frequently asked questions

The NCUA is the government agency that insures deposits at member credit unions. It was created by Congress to help provide stability and encourage public confidence in the nation's banking system.

The NCUA provides federal insurance for up to $250,000 per depositor, per federally insured credit union, per ownership category. This includes Single Ownership Accounts, Joint Ownership Accounts, IRAs and Other Certain Retirement Accounts, Revocable Trust Accounts, and Irrevocable Trust Accounts.

The NCUA does not insure money invested in stocks, bonds, mutual funds, life insurance policies, annuities, or municipal securities. It also does not insure safe deposit boxes or their contents and does not cover digital assets such as cryptocurrencies.