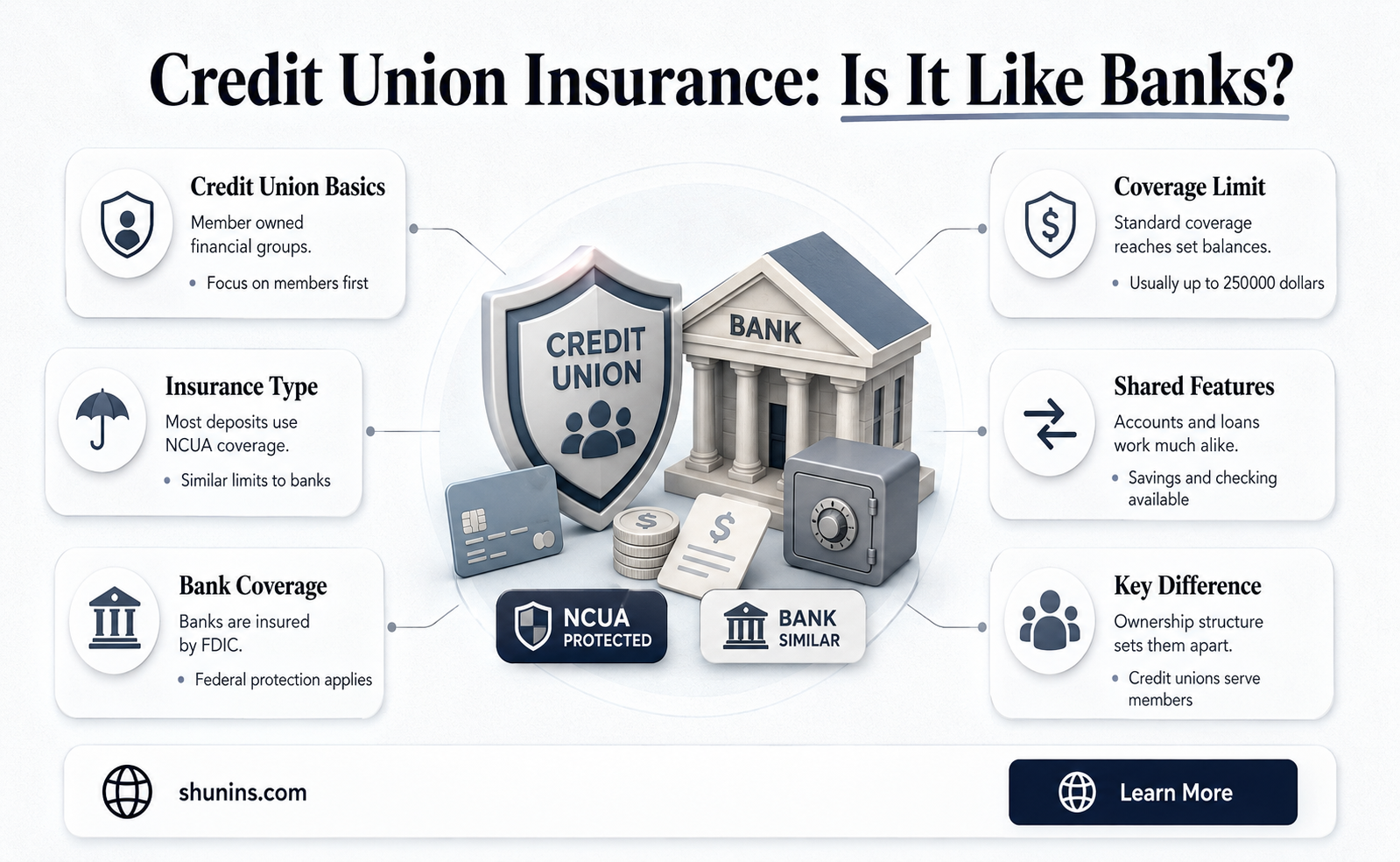

Credit unions are not-for-profit organisations that are owned by their members. While banks are insured by the Federal Deposit Insurance Corporation (FDIC), credit unions are insured by the National Credit Union Administration (NCUA). The NCUA is an independent federal agency that manages the National Credit Union Share Insurance Fund, which insures the deposits of over 135 million account holders in federal credit unions and most state-chartered credit unions. The NCUA and FDIC have the same insurance coverage limit of $250,000 per depositor, per account.

| Characteristics | Values |

|---|---|

| Insurer of credit unions | National Credit Union Administration (NCUA) |

| Insurer of banks | Federal Deposit Insurance Corporation (FDIC) |

| Cap on insurance coverage | $250,000 per depositor, per account |

| Number of accounts insured by NCUA | More than 135 million |

| NCUA's counterpart | FDIC |

Explore related products

What You'll Learn

![]()

Credit unions are insured by the NCUA, not the FDIC

Credit unions are not insured by the Federal Deposit Insurance Corporation (FDIC). Instead, they are insured by the National Credit Union Administration (NCUA), an independent federal agency that Congress created to regulate, charter, and supervise federal credit unions. The NCUA manages the National Credit Union Share Insurance Fund (NCUSIF), which guarantees that money in a credit union account is backed by the full faith and credit of the US government.

The NCUSIF provides up to $250,000 in coverage for each single ownership account in all federal credit unions and most state-chartered credit unions. Credit union members can calculate the amount of insured funds at a federally insured credit union using the NCUA's Share Insurance Estimator. While the NCUA and FDIC have different roles, their insurance coverage is quite similar. Both protect the cash in eligible deposit accounts up to $250,000, and neither covers stocks, bonds, mutual funds, or cryptocurrency investments.

The FDIC was established in 1933 in response to a series of bank failures during the Great Depression, which caused a national financial crisis and resulted in many Americans losing their life savings. The FDIC now monitors banks for financial soundness and compliance with consumer protection laws, providing insurance for deposits at banks. The NCUA, on the other hand, was created to provide stability and encourage public confidence in the nation's banking system, specifically for credit unions.

While credit unions are not insured by the FDIC, they are still safe places to store your money. Credit union members have never lost insured savings at a federally insured credit union. With the backing of the US government, the NCUA ensures the safety of deposits in federally insured credit unions, making them just as safe as FDIC-insured banks.

Flood Insurance: Private Options Absent Amidst Natural Disasters

You may want to see also

Explore related products

![]()

The NCUA is the National Credit Union Administration

Credit unions are insured by the National Credit Union Administration (NCUA), while banks are insured by the Federal Deposit Insurance Corporation (FDIC). The NCUA is an independent federal agency created by the United States Congress to regulate, charter, and supervise federal credit unions. It is administered through three regional offices, each responsible for specific states and territories.

The NCUA manages the National Credit Union Share Insurance Fund (NCUSIF), which insures the deposits of more than 124 million account holders in all federal credit unions and most state-chartered credit unions. The NCUSIF was created in 1970 without the use of any tax dollars and is capitalized solely by credit unions. It guarantees that money in a credit union account is backed by the full faith and credit of the US government, with deposits insured for up to $250,000 per individual depositor.

The NCUA also operates three other funds: the NCUA Operating Fund, the Central Liquidity Facility (CLF), and the Community Development Revolving Loan Fund (CDRLF). In addition to its role in deposit insurance, the NCUA also protects consumers and educates the public on consumer protection and financial literacy issues.

The NCUA has implemented measures to protect against the failure of credit unions, such as a 12-month examination cycle for federally insured credit unions to detect problems early on. As a result of these efforts, by the end of 2009, over 96% of credit unions were considered "well capitalized".

Blue Cross Blue Shield: Private Insurance and Tax Forms

You may want to see also

Explore related products

![]()

The NCUA insures deposits up to $250,000

Credit unions are insured differently from banks. While the Federal Deposit Insurance Corporation (FDIC) insures bank accounts, the National Credit Union Administration (NCUA) insures credit union accounts. The NCUA is a government agency that manages the National Credit Union Share Insurance Fund (NCUSIF). This fund guarantees that money in a credit union account is backed by the full faith and credit of the US government.

The NCUA's insurance coverage is automatic, so there is no need to opt in to receive it. The NCUA covers various common account types, including free checking accounts and high-yield savings accounts. It is important to note that the NCUA does not cover stocks, bonds, mutual funds, or cryptocurrency investments.

The NCUA and FDIC have similar rules and processes, and both agencies have the same cap on insurance coverage. Credit union members can have peace of mind knowing that their deposits are safe and insured by the NCUA, just as bank customers' deposits are protected by the FDIC.

Regence Insurance: Private or Public? Understanding the Difference

You may want to see also

Explore related products

![]()

The NCUA covers most federal and state-chartered credit unions

Credit unions are insured differently from banks. While banks are insured by the Federal Deposit Insurance Corporation (FDIC), credit unions are insured by the National Credit Union Administration (NCUA). The NCUA is an independent federal agency that manages the National Credit Union Share Insurance Fund (NCUSIF). The NCUSIF guarantees that money in a credit union account is backed by the full faith and credit of the US government.

The NCUA provides federal insurance for deposits at credit unions, protecting the cash kept in eligible deposit accounts up to $250,000 per individual depositor. Credit union members can calculate the amount of insured funds at a federally insured credit union using the NCUA's Share Insurance Estimator.

The NCUA and FDIC have similar rules and processes, and both have the same cap on how much of a depositor's funds are insured. The NCUA also protects consumers and educates the public on consumer protection and financial literacy issues. Both agencies were created by Congress to provide stability and encourage public confidence in the nation's banking system.

Elizabeth Warren's Stance on Private Insurers: Keep or Toss?

You may want to see also

Explore related products

![]()

The NCUA is an independent federal agency

The National Credit Union Administration (NCUA) is an independent federal agency that was created by the US Congress in 1970. It is a government-backed insurer of credit unions in the United States. The NCUA exclusively insures credit unions, while commercial banks and savings institutions are insured by the Federal Deposit Insurance Corporation (FDIC). The NCUA operates and manages the National Credit Union Share Insurance Fund (NCUSIF), which guarantees that money in a credit union account is backed by the full faith and credit of the US government. The fund provides up to $250,000 in coverage for each single ownership account.

The NCUA is governed by a three-member board, appointed by the US president and confirmed by the Senate. No more than two members can be from the same political party, and each member serves a six-year term. The NCUA's mission is to "provide, through regulation and supervision, a safe and sound credit union system, which promotes confidence in the national system of cooperative credit". The agency plays a role in ensuring broader financial stability as a member of the Federal Financial Institutions Examination Council and the Financial Stability Oversight Council.

The NCUA has three regional offices, each responsible for specific states and territories. The agency's headquarters are in Alexandria, Virginia, and it also operates an Asset Management and Assistance Center in Austin, Texas, to liquidate credit unions and recover assets. The NCUA provides targeted regulatory flexibility to federally insured credit unions, allowing them to manage their operational and financial risks effectively. During the COVID-19 pandemic, the NCUA worked to enhance the Central Liquidity Facility's ability to serve as a liquidity backstop for the system.

The NCUA is committed to protecting consumer rights and member deposits. It offers a Share Insurance Estimator to help consumers, credit unions, and their members understand how its share insurance rules apply to member share accounts and what portion, if any, exceeds coverage limits. The NCUA also reminds individuals to remain vigilant against scams, especially those related to the coronavirus pandemic.

Arvest Bank Accounts: Are They Insured?

You may want to see also

Frequently asked questions

Credit unions are not insured by the FDIC, but they are insured by the NCUA. The NCUA is the National Credit Union Administration, a federal agency that provides federal insurance for deposits at credit unions. The FDIC is the Federal Deposit Insurance Corporation, which provides federal insurance for deposits at banks. Both agencies have the same insurance coverage limit of \$250,000 per depositor, per account.

Congress created the NCUA to help provide stability and encourage public confidence in the nation's banking system. The NCUA manages the National Credit Union Share Insurance Fund (NCUSIF), which guarantees that money in a credit union account is backed by the full faith and credit of the U.S. government.

The NCUA provides an online tool to check if a credit union is an NCUA-insured financial institution. Additionally, federally insured credit unions are required to disclose their membership on their websites and at teller stations.