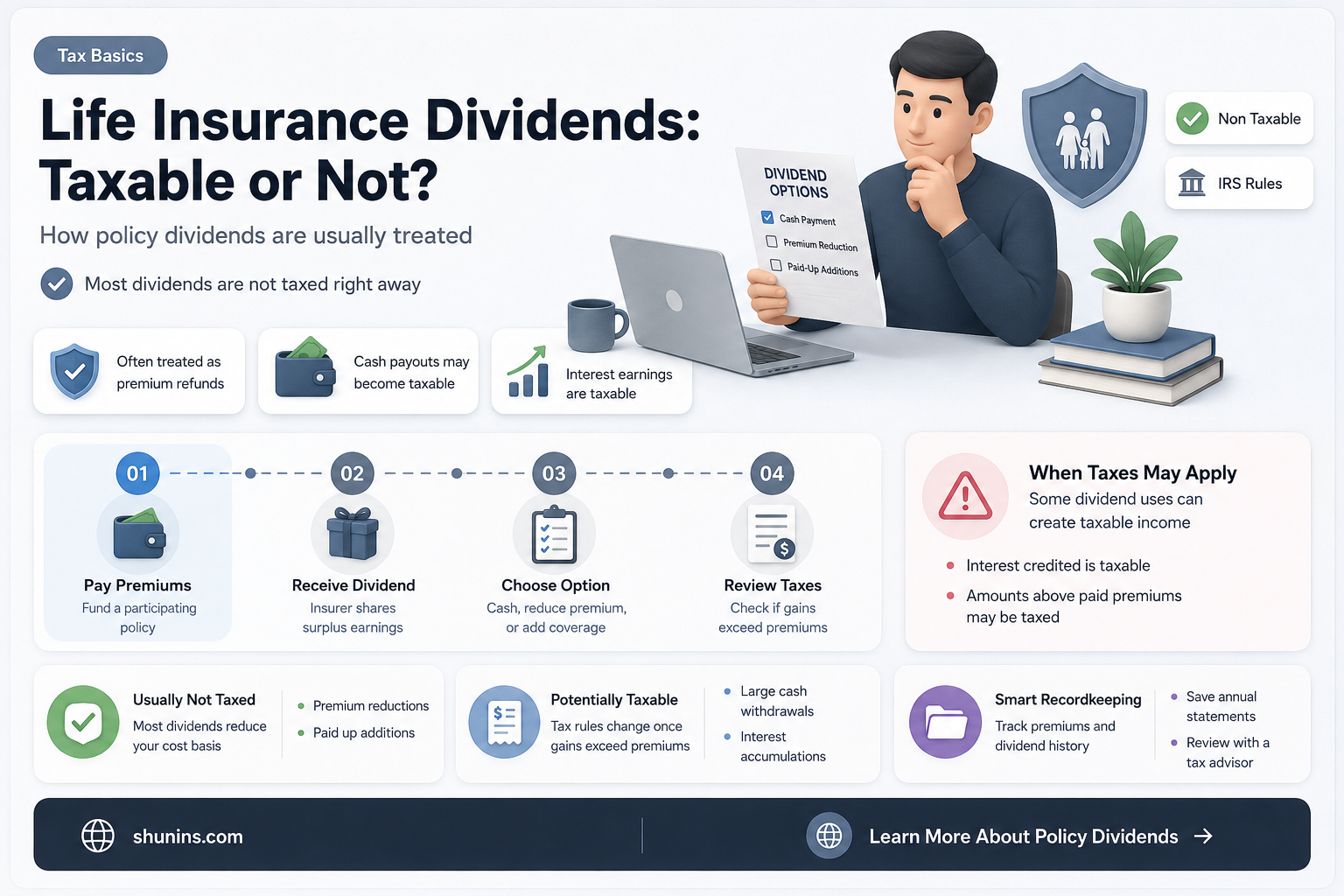

Life insurance dividends are generally not taxable. The Internal Revenue Service (IRS) considers life insurance dividends to be a return of funds that have already been taxed through federal and state income taxes. However, there are some exceptions. If your dividend returns exceed the amount of premiums you have paid, there may be income tax implications. Additionally, if you earn interest on your dividends, this interest income is typically subject to taxation. It is important to understand the specifics of your life insurance plan, as different policies have varying taxable measures of income when they are paid out. Working with a tax professional can help you effectively navigate the tax implications of your life insurance dividends.

Explore related products

$15.95

What You'll Learn

![]()

Dividends from life insurance are generally not taxable

The taxation of dividends also depends on the type of policy you have. If your policy is not a Modified Endowment Contract (MEC), dividends are typically considered a return of premium and are not taxable. However, if your policy is a MEC, dividends (except those used to purchase additional insurance or pay premiums on the same policy) may be taxable when earned, depending on the gain in the contract.

It's worth noting that while dividends from life insurance are generally not taxable, any interest earned on those dividends is usually taxable. This interest income may be subject to tax if it exceeds the amount you have paid in premiums. Therefore, it is always a good idea to consult with a tax professional to understand the tax implications of your specific situation and policy.

Additionally, it's important to understand the difference between participating and non-participating life insurance policies. Participating policies are eligible for dividends, while non-participating policies are not. With a participating policy, you are considered a stakeholder in the insurance company, and the company uses your premiums to invest and generate returns. On the other hand, a non-participating policy has a lower premium but does not offer the potential for dividends.

Personal Life Insurance: Protecting Your Family's Future

You may want to see also

Explore related products

![]()

Dividends are considered a return of premiums paid

Dividends from life insurance are generally not taxable. This is because the IRS considers them a return of premiums paid. In other words, when you receive dividends from your life insurance policy, it is treated as a refund of a portion of the premiums you have paid. This is because the insurance company invests the premium payments you make, and if they keep their expenses low and their investments perform well, they will distribute some of the profits back to policyholders in the form of dividends.

However, it is important to note that dividends from life insurance are not guaranteed. The insurance company determines the dividend amount based on their profits, expenses, and cash reserves, and there is no clear method for how they arrive at this amount. Additionally, while dividends are not taxable, if you earn interest on your dividends, that interest is usually taxable.

If your life insurance policy is classified as a Modified Endowment Contract (MEC), the rules regarding taxation of dividends may differ. In this case, dividends are generally taxable when earned to the extent of the gain in the contract, which is calculated as the difference between the cash value of the policy and the cost basis of the policy.

Cashing in on Mutual Savings: Life Insurance Options

You may want to see also

Explore related products

![]()

Dividends exceeding premiums paid may be taxable

Dividends from life insurance are generally not taxable. The IRS considers them a return of premiums paid. However, if your dividends exceed the premiums you have paid, the excess amount may be subject to income tax. This is because any dividends over the amount you paid are considered income rather than a return of premium. For example, if you pay $1,000 in premiums and receive a dividend of $1,250, you may owe taxes on the excess $250.

In addition, if you earn interest on your dividends by leaving them in your policy, this interest income may also be taxable if it exceeds the premiums you have paid. It is important to note that the taxability of dividends may depend on the type of life insurance policy you have and how it is structured. Working with a tax professional can help you understand the tax implications of your specific situation.

It is worth noting that life insurance dividends are not guaranteed. They are determined by the insurance company's board of directors, who consider factors such as the company's financial performance, expenses, and cash reserves. Dividends are typically paid out on a set schedule, such as quarterly or annually, and policyholders have several options for using their dividends, including taking them as cash, applying them to future premium payments, or using them to purchase additional insurance coverage.

Life Insurance and Suicidal Death: What Employers Cover

You may want to see also

Explore related products

![]()

Interest earned on dividends left in a policy may be taxable

The taxation of dividends depends on whether your policy is classified as a Modified Endowment Contract (MEC). If your policy is not a MEC, dividends are considered a return of premium and are generally not taxable. However, if the dividends you receive over the life of the policy exceed the premiums you have paid, the excess amount may be taxable as income.

On the other hand, if your policy is a MEC, dividends are generally taxable when earned to the extent of the gain in the contract. The gain is calculated as the difference between the cash value of your policy and the cost basis of the policy (premiums paid less any amounts previously received tax-free).

It is important to note that the interest you earn on dividends left in your policy is fully taxable as soon as you have the right to withdraw it, regardless of whether you actually withdraw it or not. This interest income is treated as ordinary income and must be reported on your tax return.

To determine if you need to pay taxes on the interest earned, you can refer to IRS Topic No. 403, Interest Received, or consult with a tax professional. They can help you understand the specific rules and regulations regarding the taxation of interest earned on life insurance dividends and ensure that you are compliant with the tax laws.

Suicid and Life Insurance: What's the Verdict?

You may want to see also

Explore related products

![]()

Consult a tax professional to understand your specific situation

The taxability of dividends from life insurance can depend on several factors, and it is important to consult a tax professional to understand your specific situation. A tax advisor can help you navigate the complexities of tax regulations and ensure you are compliant with the relevant laws. Here are some reasons why consulting a tax professional is essential:

- Variations in Tax Laws: Tax laws can vary by jurisdiction, and a tax professional will be able to advise you based on the specific tax laws in your area. They will be up to date with any changes or updates to these laws, ensuring accurate guidance.

- Individual Circumstances: Your specific circumstances, such as the type of life insurance policy you hold, the amount of dividends received, and how you intend to use those dividends, will impact their taxability. A tax professional can help you understand how these factors interact and affect your tax obligations.

- Tax Treatment of Dividends: Life insurance dividends are generally treated as a return of premiums and are not taxable. However, there are exceptions to this rule. For example, if your dividends exceed the total premiums you have paid, the excess may be subject to tax. A tax professional can help you navigate these nuances and determine if your dividends are taxable in your specific situation.

- Interest on Dividends: If you choose to leave your dividends in your policy to earn interest, the interest income may be taxable. A tax advisor can help you understand the tax implications of this decision and advise you on how to report and pay taxes on this income if necessary.

- Policy Details and Structures: Different types of life insurance policies have varying tax treatments. For example, whole life insurance policies, including participating and non-participating policies, have distinct tax considerations. A tax professional can help you understand the tax implications of your specific policy type and any associated dividends.

- Tax Planning: Consulting a tax professional can help you make informed decisions about your life insurance dividends and their impact on your overall tax liability. They can advise you on strategies to minimize taxes, such as using dividends to pay future premiums or investing them back into the policy.

While online resources can provide general information, consulting a qualified tax professional will give you personalized advice tailored to your unique circumstances. They can help you navigate the complexities of tax laws, ensure compliance, and make informed decisions about your life insurance dividends and overall financial planning.

Kentucky Farm Bureau Life Insurance: Competitive Rates?

You may want to see also

Frequently asked questions

Life insurance dividends are generally not taxable. The IRS considers them a return of premiums paid. However, if your dividends exceed the total premiums paid, the excess may be taxable.

Life insurance dividends may be taxable if they exceed the total premiums paid. In this case, the excess amount is considered income. Additionally, if you earn interest on your dividends, this interest income may be taxable.

Dividends are a share of profits or a return on investment, while interest is money earned over time on borrowed or lent funds. Dividends are typically not taxable, while interest is taxable.

A death benefit is a predetermined amount paid to the beneficiaries upon the death of the policyholder. It is part of the insurance policy. A life insurance dividend, on the other hand, is a return on the insurance company's investment performance and is only available to those with participating whole life insurance policies.

The main advantage of life insurance dividends is the potential for tax-free or tax-deferred returns. This can help offset future premium costs or increase the cash value of the policy. However, the main disadvantage is the higher monthly premium associated with a participating policy eligible for dividends.