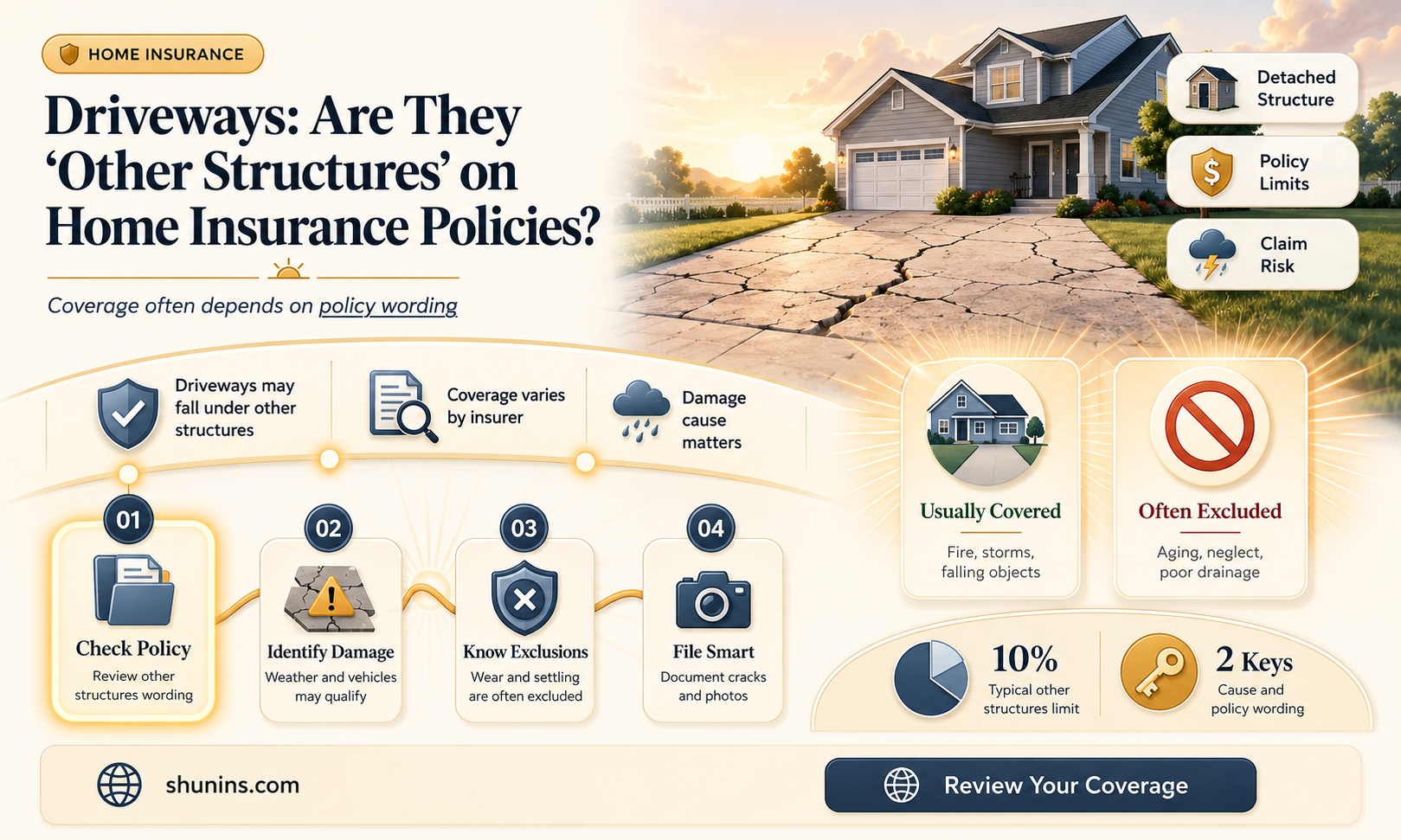

Homeowners insurance policies typically include coverage for the dwelling, personal property, and other structures. Other structures coverage, also known as Coverage B, applies to structures that are not directly attached to the home, such as sheds, fences, and detached garages. Driveways are also considered other structures and are usually covered on an actual cash value basis. This means that if a covered peril, such as a fallen tree, damages your driveway, your insurance policy may cover the repair or replacement costs, minus your deductible. However, it's important to note that standard homeowners insurance policies may not cover damage to your driveway from certain natural disasters or perils.

| Characteristics | Values |

|---|---|

| Driveways considered other structures | Yes |

| Other structures coverage | Covers structures that aren't attached to the home, such as sheds, fences, gazebos, and detached garages |

| Coverage limit | Typically 10% of the dwelling coverage limit |

| Coverage basis | Replacement cost basis or actual cash value basis |

| Exclusions | Structures used for business purposes |

Explore related products

What You'll Learn

![]()

Driveways are covered under 'other structures'

Homeowners insurance is not a one-size-fits-all policy. While some coverages are self-explanatory, others, like 'other structures coverage', are less straightforward. This coverage includes items on the property that aren't directly attached to the home, such as driveways, decks, patios, sheds, fences, and detached garages.

Driveways are often considered under 'other structures coverage' in homeowners insurance policies. This means that if your driveway is damaged by a covered peril, your insurance company may pay to repair or replace it, up to your policy's limits. For example, if a tree falls on your driveway and cracks it, your insurance company may cover the cost of repairs or replacement. Other covered perils may include fires, tornadoes, windstorms, or hail.

It's important to note that standard homeowners insurance policies may not cover damage to your driveway from certain natural disasters or perils. For instance, damage caused by hot asphalt sagging or cracking due to weight, or damage from changing seasonal temperatures, is typically not covered. Additionally, if you use your driveway for business purposes, such as storing work equipment, it may not be covered by your homeowners insurance and you may need separate business insurance.

The coverage limit for 'other structures' is typically set at a percentage of your dwelling coverage limit, commonly 10%. For example, if your home is insured for $300,000, your other structures coverage limit would be $30,000. You may be able to adjust this limit or purchase additional coverage if you have a large driveway or other valuable detached structures.

It's always a good idea to review your homeowners insurance policy carefully to understand what is and isn't covered. Communicating regularly with your insurance provider can help ensure you have the right coverage for your needs.

Farmers Insurance: Unveiling the Roadside Assistance Benefits

You may want to see also

Explore related products

![]()

Coverage for damage caused by natural disasters

A standard homeowners insurance policy typically covers your home's physical structure (dwelling coverage) and your personal belongings (personal property coverage). It also includes liability coverage and guest medical payment coverage. If your home is damaged by a covered peril and you cannot live in it, your policy may also include loss-of-use coverage, which pays for temporary housing, food, and transportation.

Homeowners insurance usually covers many disasters like wildfires and tornadoes. However, a standard policy won't cover damage from an earthquake or flood. You would need to purchase separate flood insurance or earthquake insurance. Home insurance companies in coastal areas sometimes exclude coverage for wind damage, and you may need to buy a separate policy for windstorm and hail damage.

Other structures coverage is part of your homeowners insurance that covers damage to structures that aren't attached to your house, such as sheds, fences, gazebos, and detached garages. Depending on your policy, other structures coverage typically provides coverage up to a percentage of the dwelling coverage, often 10%. For example, if a tree falls on your driveway during a storm and cracks it, the cost of repairing or replacing your driveway may be covered by your homeowners insurance policy. Your policy may also cover other perils, including fires, tornadoes, windstorms, or hail.

It is important to note that standard homeowners insurance policies won't cover damage to your driveway from certain natural disasters and perils. For instance, hot asphalt driveways are more vulnerable to sagging and cracking due to weight and changing seasonal temperatures. Homeowners insurance may not cover the cost of debris removal following a storm unless a tree falls due to a covered peril, such as a lightning strike, and blocks your driveway.

Arson for Insurance: Burning Down a House

You may want to see also

Explore related products

$14.37 $24.99

![]()

Coverage for damage caused by vehicles

A standard homeowners insurance policy typically covers the physical structure of your home, your personal belongings, liability coverage, and guest medical payment coverage. If your home is damaged by a covered peril and you cannot stay in it, your policy may also include loss-of-use coverage, which pays for temporary housing, food, and transportation.

Homeowners insurance does not cover vehicles, whether they are parked in your driveway or inside your garage. It also does not cover damage to vehicles, even if they are on your property. For instance, if you accidentally back into your garage door, homeowners insurance will not cover the damage. Auto insurance is required for comprehensive vehicle protection.

However, homeowners insurance may cover damage caused by your vehicle to other people's property. If you are responsible for injuring someone or damaging another person's property with your vehicle, your homeowners insurance may provide liability protection. This includes coverage for legal settlements if you are found liable for an incident on your property.

It is important to note that if a covered peril damages both your home and your vehicle, you will need to file two separate claims: one with your homeowners insurance for the damage to your home and another with your auto insurance for the damage to your vehicle. This is because each policy is designed to cover specific types of damage under its own terms and conditions.

Additionally, while homeowners insurance does not cover damage to your vehicle in your driveway, it may pay to replace personal belongings damaged or stolen from it. This includes coverage for belongings stolen from your car, up to the personal property coverage limits in your policy.

Windshield Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

Coverage for damage caused by mould and mildew

Driveways are considered 'other structures' in homeowners insurance. Other structures coverage is part of your homeowners insurance and covers damage to structures that are not attached to your house. This includes driveways, fences, pools, sheds, detached garages, tree houses, and so on. If any of these structures are damaged, your insurance can pay for the repairs.

Homeowners insurance typically does not cover mould damage due to flooding or a lack of home maintenance. However, if the mould is caused by a sudden and unexpected event, such as a bursting pipe, your insurance company will likely cover the cost of repairs.

If your insurance company denies your claim, you can either file an appeal or pay for the repairs yourself. If you choose to appeal, you must be able to prove that the damage was caused by a covered peril and that your insurer is wrong to deny the claim. If your appeal is still denied, you may need to seek legal advice.

If the mould damage is small (less than 3 feet by 3 feet), it may be safe to carry out the repairs yourself. To prevent mould, you must control and remove moisture by stopping the water flow and drying any wet areas. You should also move wet items to a dry area.

You can also purchase flood insurance, which may cover mould damage if it occurs after a flood. This is especially useful if you live in a flood-prone area.

ICBC Insurance Alternatives: Are They Worth the Switch?

You may want to see also

Explore related products

![]()

Coverage for damage caused by vandalism

Homeowners insurance policies typically include coverage for the dwelling, personal property, and other structures. Other structures coverage includes items on the property that are not directly attached to the home, such as driveways, decks, patios, sheds, fences, and detached garages. This coverage usually provides coverage up to a percentage of the dwelling coverage, often 10%.

Regarding vandalism, it is considered a "named peril" and is typically covered by homeowners insurance policies. Vandalism refers to intentional damage caused to one's property without their consent, such as slashed bike tires, broken windows, or spray paint on the exterior of the house. Most homeowners insurance policies cover damage sustained due to vandalism, including the primary dwelling and personal property. If the property damage is severe and the homeowner cannot reside in the home, additional living expenses (ALE) coverage may be included to cover temporary housing and other expenses.

However, it is important to note that vandalism losses are generally not covered if the property has been vacant for a consecutive period, typically 60 days, as per most state regulations. Additionally, vandalism caused to one's car is not covered under homeowners insurance and would require comprehensive coverage under a separate car insurance policy.

To ensure adequate coverage for your driveway and protection against vandalism, carefully review your homeowners insurance policy, including the coverage limits and exclusions. Consider consulting with your insurance provider to clarify any uncertainties and determine if additional coverage is necessary.

Justin Thomas' Participation in the Farmers Insurance Open: Will He Compete?

You may want to see also

Frequently asked questions

Yes, driveways are considered other structures and are covered by homeowners insurance. Other structures refer to items on the property that aren't directly attached to the home, such as sheds, fences, and detached garages.

Homeowners insurance typically covers damage to driveways caused by covered perils, such as fires, tornadoes, windstorms, or hail. It may also cover sudden and accidental damage, like a tree falling and cracking the driveway.

The coverage limit for other structures is usually about 10% of your dwelling coverage limit. For example, if your home is insured for $100,000, your other structures limit would be $10,000. You may need to purchase additional coverage if you have a larger driveway or want more comprehensive protection.

No, homeowners insurance typically covers the driveway itself but not the contents or items stored on it. It also does not cover damage caused by certain exclusions listed in your policy, such as damage from specific natural disasters or wear and tear due to a lack of maintenance.