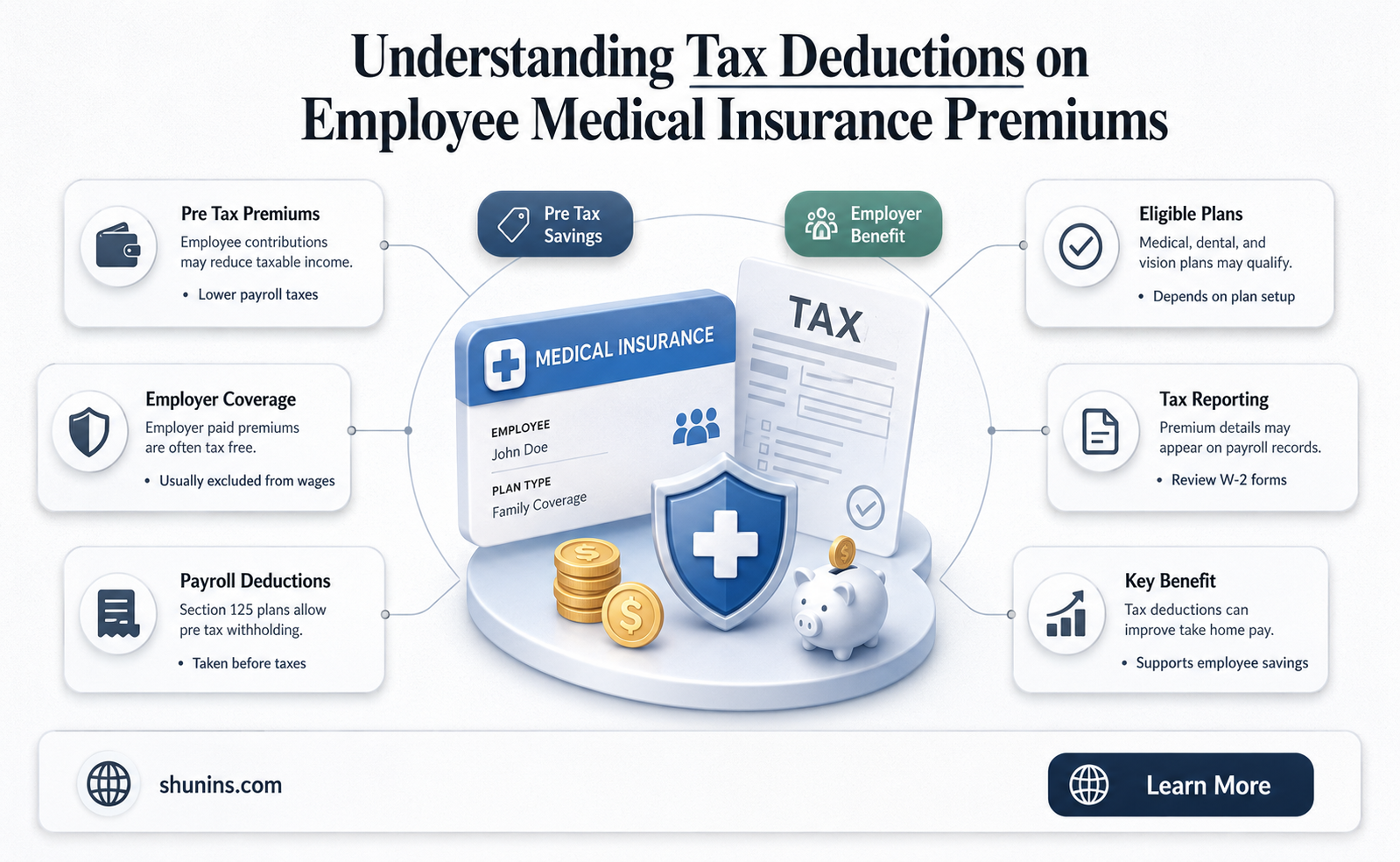

Health insurance premiums are the upfront cost of having medical insurance. In the context of employer-paid insurance premiums, it is important to understand the tax exclusion for employer-sponsored health insurance. The exclusion lowers the after-tax cost of health insurance for most Americans, as employer-paid premiums for health insurance are exempt from federal income and payroll taxes. This also reduces the after-tax cost of coverage for most workers. However, it is important to note that if you pay for health insurance coverage before taxes are deducted from your paycheck, you cannot deduct your health insurance premiums. On the other hand, if you pay for health insurance coverage after taxes, you may be able to deduct your medical expenses.

| Characteristics | Values |

|---|---|

| Are employee medical insurance premiums paid by the employer deductible? | No, they are not deductible. |

| Who can deduct health insurance premiums? | Self-employed people can deduct health insurance premiums. |

| What is the tax exclusion for employer-sponsored health insurance? | Employer-paid premiums for health insurance are exempt from federal income and payroll taxes. |

| What is the impact of the tax exclusion on workers' tax bills? | The exclusion of premiums lowers most workers' tax bills and thus reduces their after-tax cost of coverage. |

| How does the tax exclusion affect the cost of health insurance for workers in different income tax brackets? | The exclusion is worth more to taxpayers in higher tax brackets than to those in lower brackets. |

| What is the estimated cost of the ESI exclusion to the federal government in 2022? | The ESI exclusion is estimated to cost the federal government $299 billion in income and payroll taxes in 2022. |

| What is a Qualified Small Employer Health Reimbursement Arrangement (QSEHRA) | A QSEHRA is a standalone plan available for small employers with fewer than 50 full-time equivalent (FTE) employees who are not required to purchase company health insurance under the Affordable Care Act (ACA). |

Explore related products

$19.99 $19.99

What You'll Learn

- Self-employed people can deduct health insurance premiums

- Employer-paid premiums are exempt from federal income and payroll taxes

- Employees can have post-tax premium payments

- Pre-tax health insurance plans include Health Reimbursement Arrangements (HRAs)

- Health insurance premiums are usually deducted from paychecks

![]()

Self-employed people can deduct health insurance premiums

On the other hand, if a self-employed individual is a business partner or a member of an LLC and is treated as a partner for tax purposes, they can deduct the health insurance premiums they pay directly. Even if the partnership or LLC pays the premiums, special tax reporting rules allow them to still claim the deduction for premiums paid for their coverage. This deduction is beneficial as it lowers the adjusted gross income (AGI), reducing the likelihood of being affected by unfavourable phase-out rules that can cut back or eliminate various tax breaks.

The self-employed health insurance deduction is applied on a month-to-month basis. It is claimed as an adjustment to gross income on Schedule 1 of Form 1040. For a sole proprietorship, the premiums paid to provide health coverage to employees are deducted on Schedule C. This deduction is a valuable tax break, especially with the rising cost of health insurance.

It is important to note that expenses that are not deductible include the portion of insurance premiums treated as paid by the employer, funeral or burial expenses, amounts paid for non-prescription medicines, toothpaste, toiletries, cosmetics, health improvement programs, most cosmetic surgery, and nicotine products that don't require a prescription.

The Impact of the Individual Mandate Penalty on Americans

You may want to see also

Explore related products

![]()

Employer-paid premiums are exempt from federal income and payroll taxes

In the United States, employer-paid premiums for health insurance are exempt from federal income and payroll taxes. This means that if an employer pays $1000 towards an employee's insurance premium, their taxes will be $254 less than if that $1000 was paid as taxable compensation. This exclusion of premiums lowers most workers' tax bills and reduces their after-tax cost of coverage. This tax subsidy is a significant factor in why most American families have health insurance coverage through their employers.

The exclusion of employer-paid premiums from federal income and payroll taxes is a tax benefit for employees. It is worth noting that the portion of premiums employees pay is typically excluded from taxable income. This means that employees can benefit from pre-tax deductions on their health insurance premiums. Pre-tax health insurance plans include health reimbursement arrangements (HRAs) and Section 125 cafeteria plans.

It is important to distinguish between pre-tax and post-tax health insurance plans. Pre-tax plans are those where the employer deducts the cost of the premium from the employee's gross pay. In contrast, post-tax plans are when the employee pays for coverage through an insurance company without enrolling in an employer-sponsored plan. If an employee pays for health insurance coverage before taxes are taken out of their paycheck, they cannot deduct their health insurance premiums. However, if they pay for coverage after taxes, they may qualify for the medical expense deduction.

The tax exclusion for employer-sponsored health insurance is a significant policy issue. It is estimated that this exclusion will cost the federal government $299 billion in income and payroll taxes in 2022, making it the single largest tax expenditure. Some have suggested making the credit refundable to extend the benefit to those with lower tax liability. However, removing the link between the subsidy and employment status may reduce firms' incentive to provide health insurance coverage.

What Medical Insurance Do I Have?

You may want to see also

Explore related products

![]()

Employees can have post-tax premium payments

Employees can choose to have more money taken out of their paycheck to cover the cost of various benefits. These are known as voluntary payroll deductions and can be withheld on a pre-tax or post-tax basis. While pre-tax deductions are usually more advantageous, post-tax benefits can result in tax savings in the future.

Pre-tax deductions are made before federal income and employment taxes are applied, providing an immediate tax break. However, they impact the employee's taxable income. On the other hand, post-tax deductions are made after taxes have been withheld, and while they do not provide immediate tax relief, they will not be taxed when the benefits are used.

An example of a post-tax deduction is wage garnishment, which is when a court orders an employer to deduct an employee's earnings due to a debt. This is a post-tax deduction regardless of the reason. Additionally, if an employee purchases disability insurance through their company's group medical plan, they can choose to pay for the premium with post-tax dollars.

It is important to note that employers must obtain written consent from employees before withholding insurance premiums or any other benefit from their pay.

Understanding Your Medical Insurance Coverage: What's Included?

You may want to see also

Explore related products

![]()

Pre-tax health insurance plans include Health Reimbursement Arrangements (HRAs)

In the United States, employer-paid premiums for health insurance are exempt from federal income and payroll taxes. This exclusion lowers the after-tax cost of health insurance for most Americans. For example, if an employer-paid insurance premium is $1000, the taxes are $254 less than they would be if the $1000 were paid as taxable compensation.

Health Reimbursement Arrangements (HRAs) are a type of pre-tax health insurance plan. They are account-based group health plans that allow employers to provide defined non-taxed reimbursements to employees for qualified medical expenses, including monthly premiums and out-of-pocket costs like copayments and deductibles. Employees must be enrolled in individual health insurance coverage to use the funds. HRAs are only for employees, not self-employed individuals.

The IRS, the Department of the Treasury, the Department of Labor, and the Department of Health and Human Services have issued rules regarding HRAs and other account-based group health plans. These rules allow HRAs to be integrated with individual health insurance coverage or Medicare if certain conditions are satisfied. The rules also set forth conditions under which HRAs will be recognized as limited excepted benefits.

Affordability calculations for employer-sponsored coverage, including an individual coverage HRA offer, are based on the lowest-cost silver plan for self-only coverage provided for the residence of an employee. An additional safe harbor allows an employer to determine the affordability of an individual coverage HRA using the lowest-cost silver plan for self-only coverage for January of the prior year.

Renewing Medical Insurance: A Step-by-Step Guide for Beginners

You may want to see also

Explore related products

![]()

Health insurance premiums are usually deducted from paychecks

Health insurance premiums are usually deducted from an employee's paycheck. This is because the cost of health insurance is often covered by employers, who may choose to deduct the employee-paid portion of the insurance premiums from their gross pay before withholding any taxes. This is known as a pre-tax deduction, and it offers considerable cost savings for both the employer and the employee. By offering health insurance benefits, employers can attract and retain talent, while employees benefit from the cost savings of pre-tax deductions.

Pre-tax deductions are excluded from gross pay for taxation purposes, which means they reduce taxable income and the amount of money owed to the government. They also lower an employee's Federal Unemployment Tax (FUTA) and state unemployment insurance dues. While employees are not required to participate in pre-tax deductions, it is usually in their best interest to do so. Pre-tax contributions can save employees a significant amount of money compared to what they would pay for benefits and other services post-tax.

However, it is important to note that there are usually caps on how much employees can contribute on a pre-tax basis. For example, the IRS regulates the total amount that can be deferred pre-tax to a 401(k) retirement plan each year. Additionally, in some states, a pre-tax health premium may not be considered pre-tax for certain taxes, such as state unemployment tax. For example, in Pennsylvania, a pre-tax health premium is not pre-tax for state unemployment tax purposes.

Furthermore, if an employee pays for health insurance coverage before taxes are taken out of their paycheck, they cannot deduct their health insurance premiums as a medical expense. This is because, generally speaking, qualified medical expenses can only be claimed as a post-tax deduction if they were paid for with after-tax earnings. On the other hand, if an employee pays for health insurance coverage after taxes are taken out of their paycheck, they may qualify for the medical expense deduction.

Overall, while health insurance premiums are usually deducted from paychecks, the tax implications can vary depending on the specific circumstances and state regulations. It is always a good idea to consult with a tax professional or seek specific guidance from the Internal Revenue Service (IRS) to understand the tax consequences of health insurance premiums and deductions fully.

Medicaid Sign-Up: A Step-by-Step Guide for Beginners

You may want to see also

Frequently asked questions

Yes, employee medical insurance premiums paid by the employer are deductible. They are considered a cost to the business, similar to salary, rent, or supplies.

If an employer pays for an employee's medical insurance, it lowers the employee's after-tax cost of health insurance. This is because the portion of premiums paid by the employee is typically excluded from taxable income.

Yes, self-employed individuals can deduct health insurance premiums, including for long-term care, on their tax returns. However, they cannot claim the deduction for months when they were eligible to participate in an employer-subsidized health plan.

Payroll deductions for health insurance can be either pre-tax or post-tax. In most cases, employers deduct the employee-paid portion of the insurance premiums before withholding any taxes. Pre-tax plans can save employees tax dollars by decreasing their tax liability.