When considering investments in Exchange-Traded Funds (ETFs), one common question is whether ETFs are insured. Unlike traditional bank deposits, which are often insured by government agencies like the FDIC in the United States, ETFs themselves are not directly insured. However, ETFs are regulated financial products, and investors may have certain protections depending on the jurisdiction and the type of ETF. For instance, in the U.S., ETFs are subject to oversight by the Securities and Exchange Commission (SEC), and investors may be covered by the Securities Investor Protection Corporation (SIPC) in the event of brokerage failure, though this does not protect against market losses. Additionally, some ETFs may hold assets that are insured, such as government bonds or insured money market funds, but this varies by fund. It’s essential for investors to understand the specific protections and risks associated with the ETFs they invest in, as insurance coverage is not a universal feature of these investment vehicles.

Explore related products

What You'll Learn

![]()

SIPC Coverage Limits for ETFs

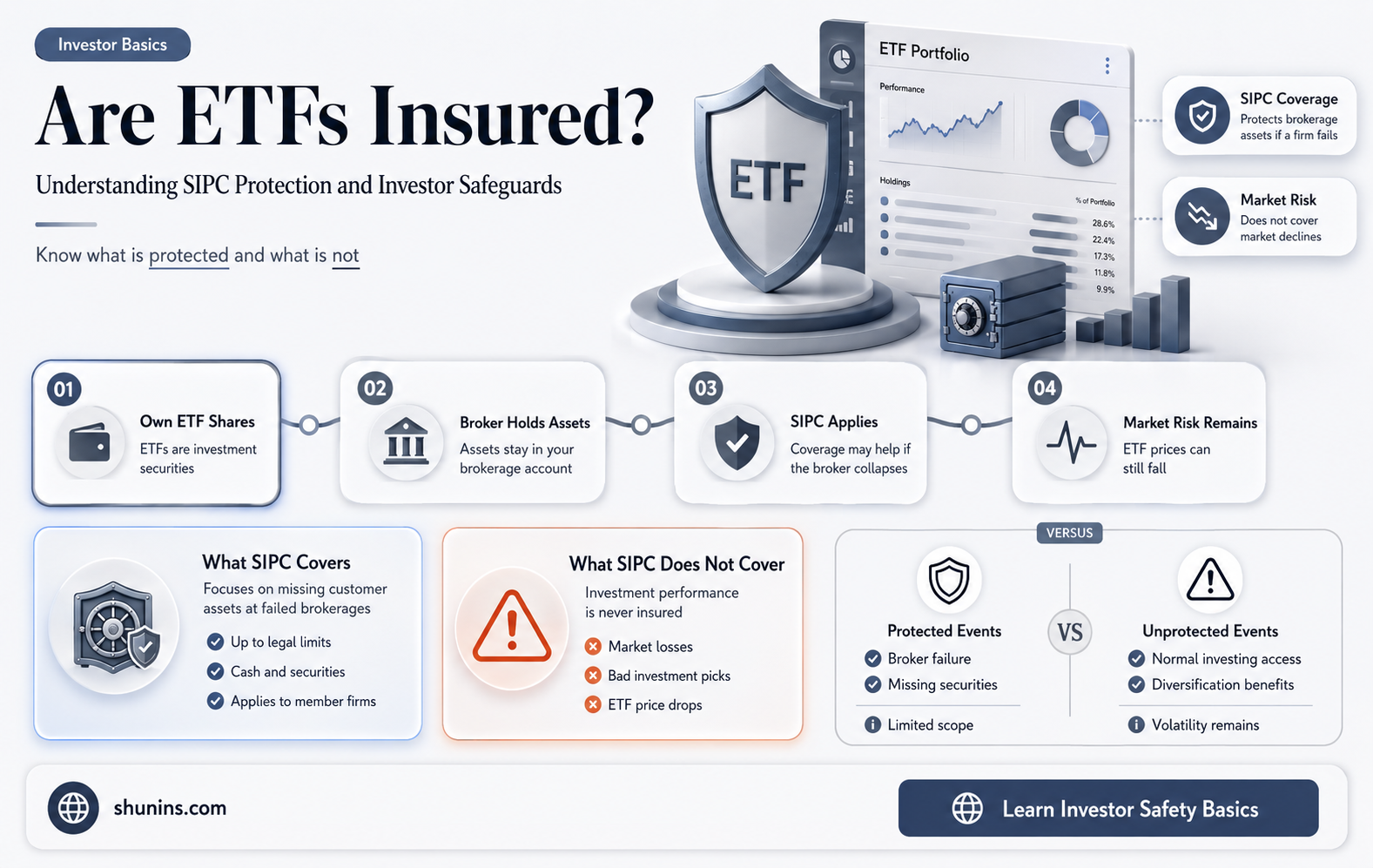

Exchange-Traded Funds (ETFs) have become a popular investment vehicle due to their flexibility, diversification, and liquidity. However, investors often wonder about the protections available for their ETF investments. One key protection is provided by the Securities Investor Protection Corporation (SIPC), a nonprofit membership corporation that insures investors against the loss of cash and securities in the event a brokerage firm fails. Understanding SIPC coverage limits for ETFs is essential for investors to gauge the extent of their protection.

SIPC coverage applies to ETFs held in brokerage accounts, as ETFs are considered securities. Under SIPC protection, investors are covered up to $500,000 per customer, including a maximum of $250,000 for cash claims. This coverage is designed to protect investors if their brokerage firm goes bankrupt or fails to return their assets. For ETF investors, this means that the shares of the ETFs held in their account are protected up to the SIPC limits. It’s important to note that SIPC coverage does not protect against market losses or investment declines; it solely safeguards against the failure of the brokerage firm itself.

When considering SIPC coverage for ETFs, investors should be aware that the protection applies to the brokerage account as a whole, not to individual securities like ETFs. For example, if an investor holds multiple ETFs and other securities in their account, the total value of these assets is considered for SIPC coverage, not each ETF separately. Additionally, SIPC coverage is supplementary to any insurance provided by the brokerage firm itself, which may offer additional protection beyond the SIPC limits.

It’s also crucial to distinguish SIPC coverage from FDIC insurance, which protects bank deposits. ETFs are not FDIC-insured because they are securities, not cash deposits. Therefore, investors relying on SIPC coverage should ensure their brokerage firm is a member of SIPC, as not all financial institutions are covered. Investors can verify this by checking the SIPC membership list or confirming with their brokerage firm directly.

Lastly, while SIPC coverage provides a safety net for ETF investors, it is not a guarantee against all risks. Investors should diversify their holdings and conduct thorough research to minimize potential losses. Understanding the SIPC coverage limits for ETFs empowers investors to make informed decisions and ensures they are aware of the protections available in the event of a brokerage firm failure. By staying informed, investors can navigate the ETF market with greater confidence and security.

Understanding Life Events: Impact on Health Insurance Options

You may want to see also

Explore related products

![]()

FDIC Insurance Applicability to ETFs

When considering whether Exchange-Traded Funds (ETFs) are insured, it’s crucial to understand the role of the Federal Deposit Insurance Corporation (FDIC) and its limitations. The FDIC is a government agency that provides insurance for bank deposits, such as checking and savings accounts, up to $250,000 per depositor, per insured bank, per ownership category. However, FDIC insurance does not apply to ETFs. ETFs are investment funds that trade on stock exchanges and hold assets such as stocks, bonds, or commodities. They are not bank deposits and therefore fall outside the scope of FDIC coverage.

The confusion about FDIC insurance and ETFs often arises because some financial products, like money market funds or bank-issued ETFs, might be mistakenly associated with FDIC protection. However, even if an ETF holds cash or cash equivalents, it is not a bank deposit. For example, a money market ETF invests in short-term debt securities and does not qualify for FDIC insurance. Investors should carefully review the prospectus or fund documentation to understand the specific risks and protections associated with any ETF.

Instead of FDIC insurance, ETFs are subject to other forms of protection. For instance, ETFs registered with the Securities and Exchange Commission (SEC) are regulated under the Investment Company Act of 1940, which provides oversight to ensure transparency and fair practices. Additionally, many ETFs are structured as open-end funds, which means they are required to hold assets in custody with a qualified custodian, often a bank or trust company. While the custodian may offer some safeguards, these do not equate to FDIC insurance.

Another layer of protection for ETF investors comes from the Securities Investor Protection Corporation (SIPC). SIPC insurance covers investors against the loss of cash and securities held by a failed brokerage firm, up to $500,000 (including a $250,000 limit for cash). However, SIPC protection does not shield against market losses or the underperformance of an ETF. It only applies if the brokerage firm holding the ETF shares goes bankrupt and customer assets are missing.

In summary, FDIC insurance does not apply to ETFs because they are not bank deposits. Investors in ETFs rely on other regulatory frameworks, such as SEC oversight and SIPC protection, for safeguards. It is essential for investors to distinguish between the types of insurance available and to recognize that ETFs carry investment risks that are not mitigated by FDIC coverage. Always consult with a financial advisor to fully understand the protections and risks associated with ETF investments.

General Insurance: What You Need to Know

You may want to see also

![]()

ETF Broker Protection Plans

When considering whether ETFs (Exchange-Traded Funds) are insured, it’s essential to understand the role of ETF Broker Protection Plans. Unlike traditional bank accounts, which are insured by the FDIC (Federal Deposit Insurance Corporation) in the U.S., ETFs themselves are not directly insured. However, investors who purchase ETFs through a brokerage account may benefit from certain protections offered by the broker. These protections are designed to safeguard investors’ assets in the event of broker insolvency or other financial failures.

One of the primary ETF Broker Protection Plans is the Securities Investor Protection Corporation (SIPC) insurance. SIPC is a nonprofit membership corporation in the U.S. that protects investors against the loss of cash and securities held by a broker-dealer that fails financially. If a brokerage firm goes bankrupt, SIPC insurance covers up to $500,000 per customer, including a maximum of $250,000 for cash claims. This means that if you hold ETFs through a SIPC-insured broker, your investments are protected up to these limits, though it’s important to note that SIPC does not protect against market losses.

In addition to SIPC, many brokers offer additional insurance coverage through private insurers. This supplemental coverage, often referred to as "excess SIPC," provides an extra layer of protection beyond the SIPC limits. For example, some brokers insure accounts for millions of dollars in securities and cash, ensuring that even large ETF portfolios are safeguarded. Investors should carefully review their broker’s protection plan to understand the extent of this additional coverage.

Another aspect of ETF Broker Protection Plans is the custodial safeguards implemented by brokers. Reputable brokers hold investor assets in segregated accounts, separate from the firm’s operational funds. This segregation ensures that client assets, including ETFs, are not used to cover the broker’s debts or liabilities. In the event of broker failure, these segregated assets are more easily recoverable, providing an additional layer of security for ETF investors.

Lastly, investors should be aware of diversification as a form of protection. While not an insurance plan per se, diversifying ETF holdings across multiple brokers or accounts can mitigate risk. By spreading investments, investors reduce the likelihood of exceeding SIPC coverage limits with a single broker. This strategy complements the protections offered by ETF Broker Protection Plans and enhances overall portfolio safety.

In summary, while ETFs themselves are not insured, investors can rely on ETF Broker Protection Plans such as SIPC insurance, excess SIPC coverage, custodial safeguards, and diversification strategies to protect their investments. Understanding these protections is crucial for ETF investors to ensure their assets are safeguarded against broker insolvency and other financial risks. Always verify your broker’s specific protection plans and consider diversifying your holdings for added security.

Child Riders: Life Insurance's Extra Protection for Your Children

You may want to see also

![]()

Risks Not Covered by Insurance

Exchange-Traded Funds (ETFs) are popular investment vehicles that offer diversification and liquidity, but it’s crucial to understand that not all risks associated with ETFs are covered by insurance. While ETFs themselves are not directly insured by the Federal Deposit Insurance Corporation (FDIC) or the Securities Investor Protection Corporation (SIPC), the underlying assets held by the ETF may have certain protections. However, there are significant risks that remain uncovered, and investors must be aware of these to make informed decisions.

One of the primary risks not covered by insurance is market risk. ETFs are subject to fluctuations in the value of the securities they hold, and insurance does not protect against losses resulting from market declines. For example, if the stock market crashes and the ETF’s holdings lose value, investors bear the full brunt of those losses. Insurance mechanisms like SIPC protect against brokerage firm failures, not against market volatility or poor investment performance.

Another risk not covered is counterparty risk in certain types of ETFs, such as those using derivatives or synthetic structures. If a counterparty (e.g., a bank or financial institution) fails to meet its obligations, the ETF and its investors could suffer losses. While some ETFs may have collateralization measures in place, there is no insurance to guarantee recovery in such scenarios. This risk is particularly relevant for leveraged or inverse ETFs, which rely heavily on derivatives and counterparty agreements.

Tracking error is another uncovered risk. ETFs aim to replicate the performance of an index or asset class, but factors like fees, rebalancing, or sampling methodologies can cause the ETF’s returns to deviate from its benchmark. Insurance does not protect against these discrepancies, and investors must accept the possibility that the ETF may underperform its target index.

Lastly, liquidity risk is not covered by insurance. While ETFs are generally liquid, certain market conditions or specific ETFs (e.g., those tracking niche markets) may experience reduced liquidity. If investors cannot buy or sell shares at desired prices, they may face losses, and insurance does not mitigate this risk. Additionally, in extreme cases, an ETF could delist or close, leaving investors with limited options, and such events are not insured.

In summary, while ETFs offer certain protections through the underlying assets and regulatory frameworks, investors must recognize that market risk, counterparty risk, tracking error, and liquidity risk are not covered by insurance. Understanding these uncovered risks is essential for managing expectations and building a resilient investment strategy.

Canceling Life Insurance: Over the Phone Possible?

You may want to see also

![]()

Insurance for ETF Cash Holdings

Exchange-Traded Funds (ETFs) are popular investment vehicles that pool money from multiple investors to purchase a basket of assets, such as stocks, bonds, or commodities. While ETFs themselves are not directly insured, certain aspects of their operations, including cash holdings, may be protected under specific insurance schemes. Insurance for ETF Cash Holdings is a critical component of investor protection, ensuring that cash balances held by ETFs are safeguarded against loss, theft, or insolvency of the custodian bank.

ETF cash holdings typically arise from dividends, interest payments, or proceeds from the creation and redemption process. These cash balances are usually held in custodian banks, which are financial institutions responsible for safeguarding the assets of the ETF. To protect these cash holdings, many custodian banks participate in insurance programs such as the Securities Investor Protection Corporation (SIPC) in the United States. SIPC insurance covers up to $250,000 per customer, including up to $250,000 for cash, in case the custodian bank fails. This protection ensures that ETF investors have a safety net for their cash balances, though it does not cover investment losses due to market fluctuations.

In addition to SIPC coverage, some custodian banks may provide additional insurance through private insurers to supplement the SIPC limits. This excess insurance can extend coverage beyond the $250,000 SIPC limit, offering greater protection for larger cash balances held by ETFs. However, it is important for investors to verify the extent of this coverage, as not all custodian banks offer excess insurance, and the terms can vary widely. ETF providers often disclose details about cash holdings insurance in their prospectuses or on their websites, allowing investors to assess the level of protection.

Another layer of protection for ETF cash holdings comes from the regulatory oversight of custodian banks. These institutions are subject to strict regulations and regular audits to ensure they maintain adequate capital and operational integrity. While not insurance per se, this oversight reduces the likelihood of custodian bank failure, thereby indirectly protecting ETF cash holdings. Investors should also consider the creditworthiness and reputation of the custodian bank when evaluating the safety of their ETF investments.

Lastly, it is worth noting that money market funds, which some ETFs may use to manage cash holdings, often have their own insurance mechanisms. These funds may provide coverage through private insurers or self-insurance pools to protect against losses. However, ETFs that hold cash directly in custodian accounts rely primarily on SIPC and excess insurance for protection. Investors should carefully review the ETF’s structure and cash management practices to understand the specific insurance provisions in place.

In summary, Insurance for ETF Cash Holdings is a multifaceted system that includes SIPC coverage, excess insurance, regulatory oversight, and, in some cases, money market fund protections. While these measures provide a safety net for cash balances, they do not guarantee against market risks or investment losses. Investors should conduct thorough due diligence to understand the insurance protections offered by their ETF and its custodian bank, ensuring their cash holdings are adequately safeguarded.

Starting a Life Insurance Business: Steps to Success

You may want to see also

Frequently asked questions

No, ETFs (Exchange-Traded Funds) are not insured by the FDIC (Federal Deposit Insurance Corporation). The FDIC insures bank deposits, not investments like ETFs.

ETFs themselves are not insured, but some may hold assets that are protected by other forms of insurance, such as SIPC (Securities Investor Protection Corporation) coverage for brokerage accounts, which protects against broker failure, not market losses.

No, ETF investors are not protected against market losses. ETFs are subject to market risk, and their value can fluctuate based on the performance of the underlying assets. Investors bear the risk of loss.