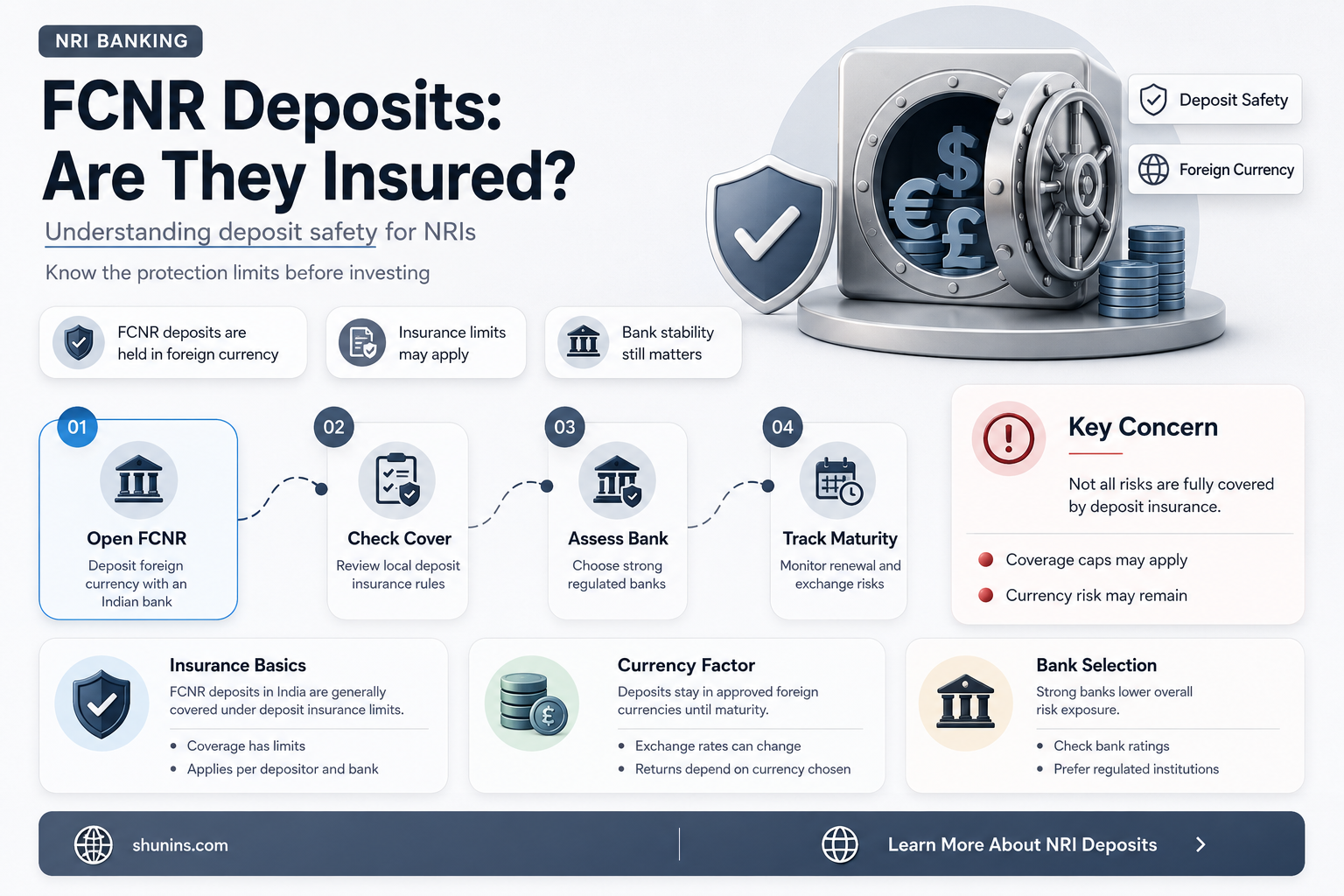

Foreign Currency Non-Resident (FCNR) accounts are a type of bank account offered to Non-Resident Indians (NRIs) that allow them to deposit their foreign earnings in India. These accounts are denominated in foreign currencies, protecting them from fluctuations in the value of the Indian rupee. One of the key concerns for NRIs is whether their FCNR deposits are insured in the event of a bank failure. Indeed, FCNR deposits are insured by India's Deposit Insurance and Credit Guarantee Corporation (DICGC), a subsidiary of the Reserve Bank of India (RBI). However, this insurance is subject to certain conditions and limits, with a maximum coverage of ₹5 lakh per depositor per bank.

| Characteristics | Values |

|---|---|

| Are FCNR deposits insured? | Yes, by the Deposit Insurance and Credit Guarantee Corporation (DICGC), a subsidiary of the Reserve Bank of India (RBI). |

| What is the coverage limit? | INR 5 lakh for the combined principal and interest per depositor per bank. |

| What is the currency of the deposit? | The insurance coverage is in INR. If the deposit is in a foreign currency, its equivalent value in INR will be calculated at the prevailing exchange rate. |

| What if I have multiple accounts? | The total coverage across all accounts (savings, current, fixed, or FCNR) is capped at INR 5 lakh. |

| Which banks offer this insurance? | Most commercial banks in India provide DICGC coverage for FCNR deposits, including Public Sector Banks (e.g., State Bank of India), Private Sector Banks (e.g., HDFC Bank, ICICI Bank), and some Foreign Banks. |

| Are there any risks to consider? | Yes, if the FCNR deposit is held with a weak bank, it may be unable to pay back upon maturity. Some experts believe that deposit insurance in India is almost non-existent due to the low coverage limit. |

| What are the benefits of FCNR deposits? | FCNR deposits are protected against forex rate risks, offer tax-free interest in India, allow seamless transfer of funds, and are denominated in major currencies like USD, GBP, EUR, and more. |

| Who can open an FCNR account? | Non-Resident Indians (NRIs), Persons of Indian Origin (POI), Overseas Citizens of India (OCI), and seafarers employed with foreign vessels. |

Explore related products

What You'll Learn

- FCNR deposits are insured by the DICGC, a subsidiary of the RBI

- The insurance covers the principal amount and interest up to ₹5 lakh per depositor per bank

- It's important to verify if your bank is eligible for DICGC coverage

- FCNR accounts are protected against forex rate risks

- Interest earned on FCNR deposits in India is tax-exempt

![]()

FCNR deposits are insured by the DICGC, a subsidiary of the RBI

FCNR (Foreign Currency Non-Resident) deposits are insured, but there are some important conditions and limits to this insurance. FCNR deposits are insured by the Deposit Insurance and Credit Guarantee Corporation (DICGC), a subsidiary of the Reserve Bank of India (RBI). The DICGC provides insurance coverage to all eligible bank deposits in India, including FCNR accounts. This insurance protects depositors against the risk of bank failure.

However, it's important to note that the coverage is limited to a maximum of ₹5 lakh per depositor per bank. This limit applies to the combined principal and interest of the deposit. For example, if you have an FCNR deposit in USD with a balance of USD 50,000, the DICGC insurance will only cover the equivalent of ₹5 lakh in INR, not the entire amount. This limit applies across all types of deposits held with a single bank, including savings, current, fixed, and FCNR accounts.

Most commercial banks in India provide DICGC coverage for FCNR deposits, but it is always a good idea to verify the eligibility of your specific bank. The coverage applies to all scheduled commercial banks in India, including public sector banks such as State Bank of India (SBI), private sector banks such as HDFC Bank and ICICI Bank, and some foreign banks operating in India.

FCNR accounts are a popular option for Non-Resident Indians (NRIs) as they allow them to retain their money in foreign currencies, protecting them from exchange rate risks. These accounts are also exempt from income tax on interest earned, and both the principal and interest are freely repatriable to the depositor's country of residence.

Life Insurance Underwriter: Getting Your Dream Job

You may want to see also

![]()

The insurance covers the principal amount and interest up to ₹5 lakh per depositor per bank

Foreign Currency Non-Resident (FCNR) deposits are insured by India's Deposit Insurance and Credit Guarantee Corporation (DICGC). The DICGC is a subsidiary of the Reserve Bank of India (RBI) and provides insurance coverage to all eligible bank deposits in India, including those held under FCNR accounts. The insurance covers the principal amount and interest up to ₹5 lakh per depositor per bank.

This means that if an FCNR account holder's bank fails, they are eligible for insurance coverage up to ₹5 lakh for the combined principal and interest. For example, if an individual holds an FCNR deposit in USD with a balance of USD 50,000, the DICGC insurance will only cover the equivalent of ₹5 lakh in INR, not the entire amount. It is important to note that this coverage limit of ₹5 lakh applies to all types of deposits (including FCNR deposits) held with a single bank.

The insurance coverage is provided in INR terms. If the deposit is in a foreign currency, its equivalent value in INR will be calculated at the prevailing exchange rate. Additionally, if an account holder has multiple deposits with the same bank, the total coverage across all accounts (savings, current, fixed, or FCNR) is still capped at ₹5 lakh.

While most commercial banks in India provide DICGC coverage for FCNR deposits, it is crucial to verify the eligibility of your bank for this insurance. The coverage applies to all scheduled commercial banks in India, including public sector banks such as State Bank of India (SBI), private sector banks like HDFC Bank and ICICI Bank, and some foreign banks operating in India.

FCNR accounts are a type of fixed deposit account that allows Non-Resident Indians (NRIs) to deposit their foreign earnings in India. These accounts are denominated in foreign currencies, protecting account holders from the risks associated with exchange rate fluctuations. While FCNR accounts offer various benefits, such as tax exemptions on interest earned and free repatriation of principal and interest, it is important for prospective account holders to carefully consider the eligibility and insurance coverage of their chosen bank to ensure their investments are adequately protected.

Incentive Life Insurance: Understanding the Basics

You may want to see also

![]()

It's important to verify if your bank is eligible for DICGC coverage

Foreign Currency Non-Resident (FCNR) deposits are insured by India's Deposit Insurance and Credit Guarantee Corporation (DICGC). The DICGC is a subsidiary of the Reserve Bank of India (RBI) and provides insurance coverage to all eligible bank deposits in India, including those held under FCNR accounts.

It is important to verify if your bank is eligible for DICGC coverage to ensure that your FCNR deposit is protected under the deposit insurance scheme. Here are some reasons why:

- Protection against bank failure: The DICGC insurance coverage protects depositors against the risk of bank failure. In the event of a bank facing financial difficulties, the DICGC safeguards account holders by ensuring they receive their funds up to a specified limit.

- Security of your deposits: The DICGC insured banks list helps depositors ensure their money is protected. Verifying your bank's insurance coverage under the DICGC gives you confidence in the security of your bank deposits.

- Choosing a reliable bank: By confirming that your bank is covered under the DICGC scheme, you can choose a well-established and reputable bank that prioritises deposit security.

- Peace of mind: Knowing that your FCNR deposit is insured provides peace of mind and assurance that your hard-earned money is safe.

- Adherence to regulations: As per the DICGC Act, 1961, all new commercial and cooperative banks must register with the DICGC after obtaining their banking license. Checking if your bank is on the DICGC insured banks list ensures that they are adhering to the regulatory requirements.

You can verify if your bank is eligible for DICGC coverage by checking the official DICGC website or by directly asking your bank. This will help you make informed decisions about your FCNR deposits and ensure that your investments are protected.

Understanding Life Insurance Underwriting: The Basics

You may want to see also

![]()

FCNR accounts are protected against forex rate risks

Foreign Currency Non-Resident (FCNR) accounts are a great option for Non-Resident Indians (NRIs) who want to retain their money in foreign currencies. These accounts are insured under the Deposit Insurance and Credit Guarantee Corporation (DICGC) and protect against the risk of bank failure. However, the coverage is limited to ₹5 lakh per depositor per bank, and it's important to verify that your bank is eligible for this insurance.

FCNR accounts offer protection against forex rate risks due to their denomination in foreign currencies. This means that the principal amount and interest earned are maintained in the chosen currency, insulating depositors from currency conversion and foreign exchange rate fluctuations. The interest earned is also free of taxes in India, and both the principal and interest are fully repatriable.

The ability to hold deposits in foreign currencies such as USD, GBP, EUR, JPY, AUD, and CAD is a significant advantage of FCNR accounts. This feature protects customers' funds from exchange rate variations and ensures stable returns at low risk. FCNR accounts also provide flexibility, with a minimum deposit period of one year and the option to renew within 14 days after maturity.

While FCNR accounts offer protection against forex rate risks, it's important to consider other factors. The choice of a reputable bank is essential, as weak banks may struggle to repay upon maturity. Additionally, the upper limit on credit guarantees in India is relatively low, at approximately Rs. 100,000 or 1600 USD, which has led to concerns about the effectiveness of deposit insurance in the country.

In summary, FCNR accounts offer NRIs protection against forex rate risks by allowing them to hold and earn interest on their deposits in foreign currencies. However, it is crucial to carefully select a reputable bank and stay informed about any applicable insurance conditions to ensure the safety of your funds.

Life Insurance and HIPAA: What's the Connection?

You may want to see also

![]()

Interest earned on FCNR deposits in India is tax-exempt

Foreign Currency Non-Resident (FCNR) accounts allow Non-Resident Indians (NRIs) to hold fixed deposits in foreign currencies. These accounts are a great way for NRIs to save money in foreign currencies while enjoying tax-free interest in India.

While FCNR deposits are insured by the Deposit Insurance and Credit Guarantee Corporation (DICGC), a subsidiary of the Reserve Bank of India (RBI), it is important to note that the coverage is limited. The DICGC covers the principal amount and interest of bank deposits, including FCNR deposits, up to a maximum of ₹5 lakh per depositor per bank. This means that in the event of a bank failure, you are eligible for insurance coverage up to ₹5 lakh for the combined principal and interest.

It is worth mentioning that while the interest earned on FCNR accounts is tax-exempt in India, it may still be subject to taxation in the country where the NRI resides, depending on the local tax laws and regulations. Therefore, it is advisable for NRIs to consult tax professionals in their country of residence to understand the specific tax implications on their FCNR deposits.

Life Insurance Conversion: Understanding Policy Transformations

You may want to see also

Frequently asked questions

Yes, FCNR deposits are insured, but only up to ₹5 lakh per depositor per bank. This insurance is provided by the Deposit Insurance and Credit Guarantee Corporation (DICGC), a subsidiary of the Reserve Bank of India (RBI).

The DICGC insurance covers the principal amount and interest of bank deposits, including FCNR deposits. This coverage protects depositors against the risk of bank failure, but it is essential to verify the eligibility of your bank for this insurance.

FCNR (Foreign Currency Non-Resident) deposits are fixed deposit accounts that allow Non-Resident Indians (NRIs) to hold and earn interest on their money in foreign currencies. These accounts are protected against forex rate risks and are exempt from income tax in India.