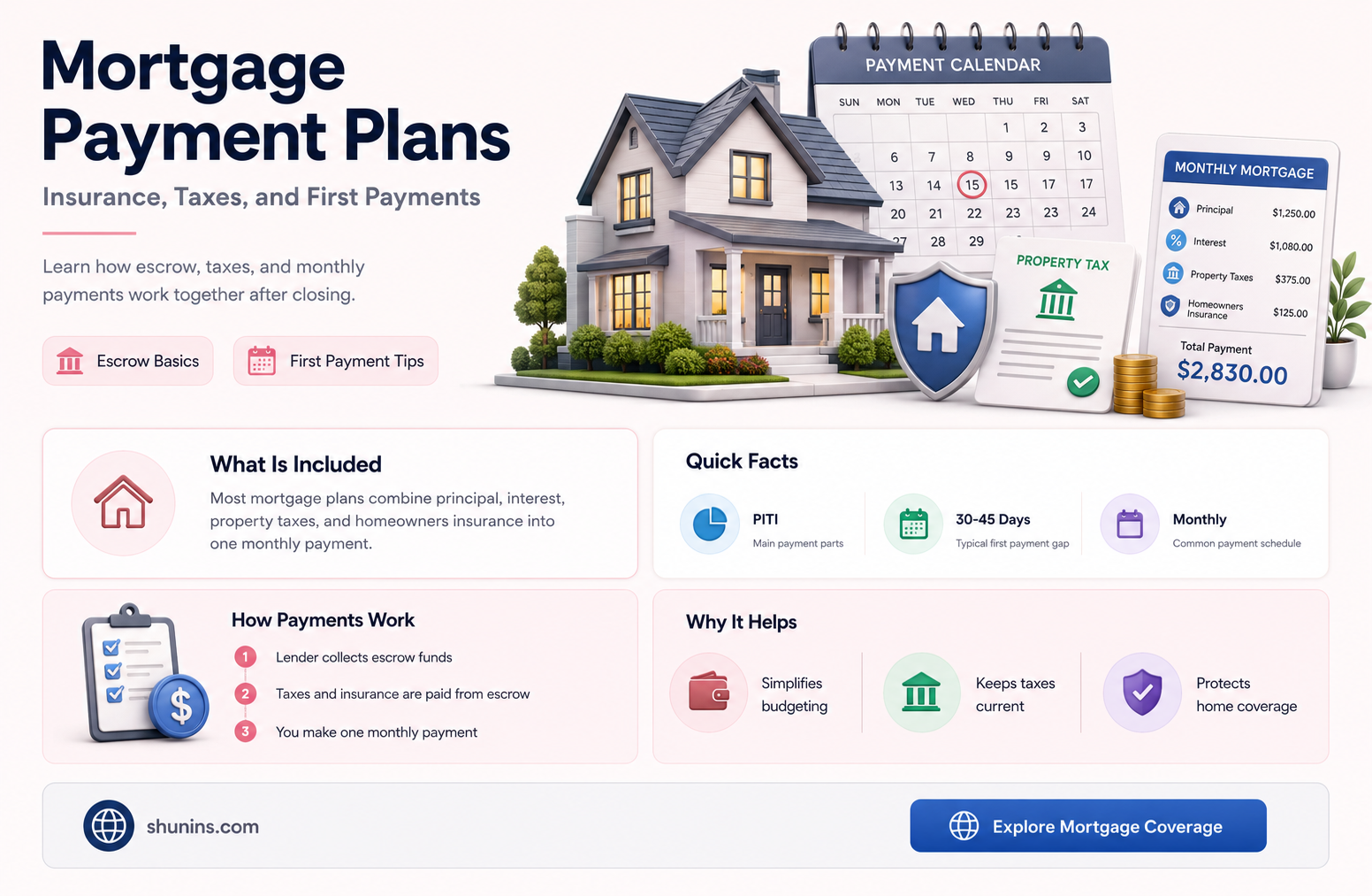

When it comes to mortgages, there are a variety of factors that can influence the size of your monthly payments. While many assume that mortgage payments consist solely of the principal and interest, there are often additional expenses such as property taxes and homeowners insurance included. These costs are typically managed through an escrow account set up by the lender, which helps to cover essential protections and local tax obligations. However, it is possible to separate tax and insurance payments from your mortgage through an escrow waiver, allowing you to pay these bills directly and choose your payment frequency.

| Characteristics | Values |

|---|---|

| Components of a mortgage payment | Principal, interest, taxes, homeowners insurance, and mortgage insurance |

| Factors that influence monthly payments | Property taxes, homeowners insurance, mortgage assistance payments, and mortgage insurance premiums |

| Escrow | A type of account that manages additional expenses like property taxes and homeowners insurance; can be waived under certain conditions |

| Tax deductions | Home mortgage interest, mortgage assistance payments for lower-income families, and mortgage insurance premiums (expired) |

Explore related products

What You'll Learn

![]()

Escrow accounts are used to manage property taxes and insurance costs

Escrow accounts are an essential part of the home-buying process, helping to manage property taxes and insurance costs. They are set up by lenders to cover essential protections and local tax obligations. Each month, homeowners contribute to their escrow account, and the funds are used to pay for property-related expenses when they are due. This includes property taxes, which are collected by local governments to fund community services, and homeowners insurance, which protects the property and assets against damage or loss.

The benefits of using an escrow account include having a dedicated fund to ensure that property tax and insurance payments stay up to date, helping homeowners avoid the financial and legal consequences of falling behind on these payments. Additionally, escrow accounts simplify budgeting by breaking down large expenses into smaller monthly payments. Instead of facing substantial insurance and tax bills, the cost is spread evenly across monthly mortgage payments.

When applying for a mortgage preapproval, lenders will estimate the monthly escrow payment based on the typical expenses of similar homes in the area. This estimate considers factors such as the previous owner's tax and insurance payments or the average taxes in the neighbourhood. However, it is important to remember that the actual insurance cost depends on the specific policy chosen, including the level of coverage, deductible amount, and insurance provider.

Escrow accounts are not mandatory for all mortgages, and there are instances where they can be waived. For example, private mortgages, those sold to Fannie Mae or Freddie Mac, and VA-backed mortgages do not require escrow accounts. However, FHA-backed loans mandate the use of escrow funds for tax and insurance payments. Additionally, lenders may waive escrow requirements for individual first mortgages if certain conditions are met, as outlined in their written policies.

In summary, escrow accounts serve as a valuable tool for managing property taxes and insurance costs, providing homeowners with a convenient way to budget for these expenses and ensuring that their payments stay current. While not compulsory in all cases, escrow accounts offer peace of mind and financial organisation during the home-buying journey.

Why You Need Pet Insurance: Is It Worth It?

You may want to see also

Explore related products

![]()

Property taxes are paid in advance for a full year

Property taxes are usually paid twice a year, in the spring and fall. However, there are other options. If you take on your own property tax payments, you can choose to pay them when they are due or pay in advance. Some people pay for the entire year at once and only pay once per year. This is done through an escrow account.

If your mortgage lender is paying your property taxes on your behalf, you may pay into an escrow account each month when you pay your mortgage payments. In this case, you won’t actively notice that you’re paying this tax as there will be no further action required from you. If your mortgage lender is making your property tax payments from an escrow account, you’ll usually set aside money with each mortgage payment that they will then apply to your taxes.

Escrow accounts are used to manage the costs of property taxes and homeowners insurance. Escrow waivers can take place on "private" mortgages (those made for a lender's own portfolio), for those sold to Fannie Mae or Freddie Mac, and on VA-backed mortgages. However, FHA-backed loans mandate that the lender escrow funds for the payment of taxes and insurance.

In some cases, homeowners are required to pay the first year of taxes as part of the closing costs. However, some property owners offer to pay taxes for the full year to make the property more attractive to prospective buyers.

It is important to note that property tax payments are based on the value of your house and the land it sits on. Therefore, if your neighbourhood becomes more desirable, your property taxes may increase. Similarly, if you take on home improvement projects or increase the size of your home, your property taxes may also rise.

Critical Illness Insurance: Unum's Worth and Value

You may want to see also

Explore related products

$9.99 $19.99

![]()

Homeowners insurance is required to protect against damage or theft

Homeowners insurance is not a legal requirement in any of the 50 states or Washington, D.C. However, if you have a mortgage, your lender will require it to protect your home. It is also important to understand that homeowners insurance is bundled with your property taxes and included in your monthly mortgage payment. This means that if you pay your property taxes separately, your monthly mortgage payments will not be affected by fluctuations.

Homeowners insurance offers financial protection against unexpected damage caused by disasters, theft, and accidents. It covers your dwelling, personal property, and liability. For example, if your home is damaged by a peril covered under your policy, you can file a claim with your insurance company. Once approved, you must pay your deductible before the insurance kicks in.

The specifics of what is covered vary depending on the policy. Most standard policies cover damage from fire, storms, theft, and liability claims. However, some disasters like floods and earthquakes are usually excluded. You can purchase separate policies or riders for these high-risk events.

Homeowners insurance premiums are highly individualized, and insurance companies consider many factors when determining your rate. The actual insurance cost depends on the specific policy you choose, including the level of coverage, deductible amount, and insurance provider. You may be able to qualify for a discount if you bundle your homeowners insurance with other policies, like auto insurance.

Collateral Protection Insurance: House Insurance Explained

You may want to see also

Explore related products

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UY218_.jpg)

![]()

Mortgage insurance may be needed for smaller down payments

When you take out a mortgage, your monthly payment will include more than just the principal and interest. Additional expenses like property taxes and homeowners insurance are also included. These costs are typically managed through an escrow account set up by your lender.

Private mortgage insurance (PMI) is a type of mortgage insurance that you may be required to purchase if you take out a conventional loan with a down payment of less than 20% of the purchase price. PMI protects the lender if you stop making payments on your loan. It's important to note that PMI does not protect you as the borrower, and you can still lose your home through foreclosure if you fall behind on payments. The cost of PMI ranges from 0.30% to 1.15% of your loan balance annually, and it is broken into 12 installments paid along with your monthly mortgage payment.

If you're a veteran or active-duty service member, you may be eligible for a VA loan, which does not require PMI and is guaranteed by the Department of Veterans Affairs. FHA loans are another option where mortgage insurance (MIP) is applied, but it cannot be canceled and borrowers pay MIP for the life of the loan.

Additionally, you may be able to avoid PMI by purchasing a less expensive home, making a 20% down payment, or choosing a property that is likely to appreciate in value. Once your home's value increases sufficiently to lower your loan-to-value ratio (LTV) below 80%, you may be able to request PMI cancellation.

Farmers Insurance: Exploring Coverage and Benefits for Nebraska's Agricultural Community

You may want to see also

Explore related products

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UY218_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UY218_.jpg)

![]()

Lenders may waive escrow accounts for first mortgages

Lenders may require borrowers to set up escrow accounts to cover property taxes and homeowners' insurance. This is because, if local taxing authorities force a tax sale due to delinquent property taxes, the lender could lose their investment in the home. Similarly, if a home is damaged or destroyed, the lender's collateral becomes much less valuable. By requiring homeowners' insurance and ensuring premiums are paid, the lender protects their investment.

Escrow accounts can make it more convenient for borrowers to save for these costs. By paying a little extra each month, they can avoid paying large amounts when tax or insurance bills are due. However, some borrowers may prefer to handle these payments themselves. In some cases, lenders may waive escrow accounts for first mortgages. This is because, while escrow accounts can make saving easier, they are ultimately interest-free loans to the servicer.

Escrow waivers can be granted for "private" mortgages, those sold to Fannie Mae or Freddie Mac, and VA-backed mortgages. FHA-backed loans, however, mandate that lenders escrow funds for the payment of taxes and insurance. Lenders cannot waive escrow accounts for certain refinance transactions or for the payment of premiums for borrower-purchased mortgage insurance. Additionally, if you have a conventional loan with private mortgage insurance (PMI), you must pay that through an escrow account. Borrowers who live in a flood zone and are required to have flood insurance may also be required to have an escrow account.

To qualify for an escrow waiver, you may need a good credit score and a history of no recent mortgage delinquencies, defaults, or loan modifications. Lenders must have a written policy governing the circumstances under which escrow accounts may be waived. When permitted, these waivers must not be based solely on the LTV ratio of a loan but also on whether the borrower can handle the lump-sum payments of taxes and insurance.

Insurance Interest: Where to Report on Your Tax Return

You may want to see also

Frequently asked questions

An escrow account is a way to manage your property taxes and homeowners insurance. This is typically set up by your lender and helps cover local tax obligations and essential protections. If you pay your homeowners insurance directly and not through an escrow account, you can choose to pay monthly, quarterly, semi-annually, or yearly.

Your monthly mortgage payment includes the loan principal, loan interest, taxes, and insurance. The loan principal is the amount of money borrowed to buy your house, and the interest is the cost of borrowing money from your lender. Taxes refer to property assessments collected by your local government. Insurance includes homeowners insurance, which is financial protection in the event of damage or theft, and mortgage insurance, which may be required if you need to make a smaller down payment.

You can separate tax and insurance payments from your mortgage payment through a process called an escrow waiver. Escrow waivers can be granted for "private" mortgages, those sold to Fannie Mae or Freddie Mac, and VA-backed mortgages. However, FHA-backed loans mandate that the lender escrow funds for the payment of taxes and insurance.

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UY218_.jpg)