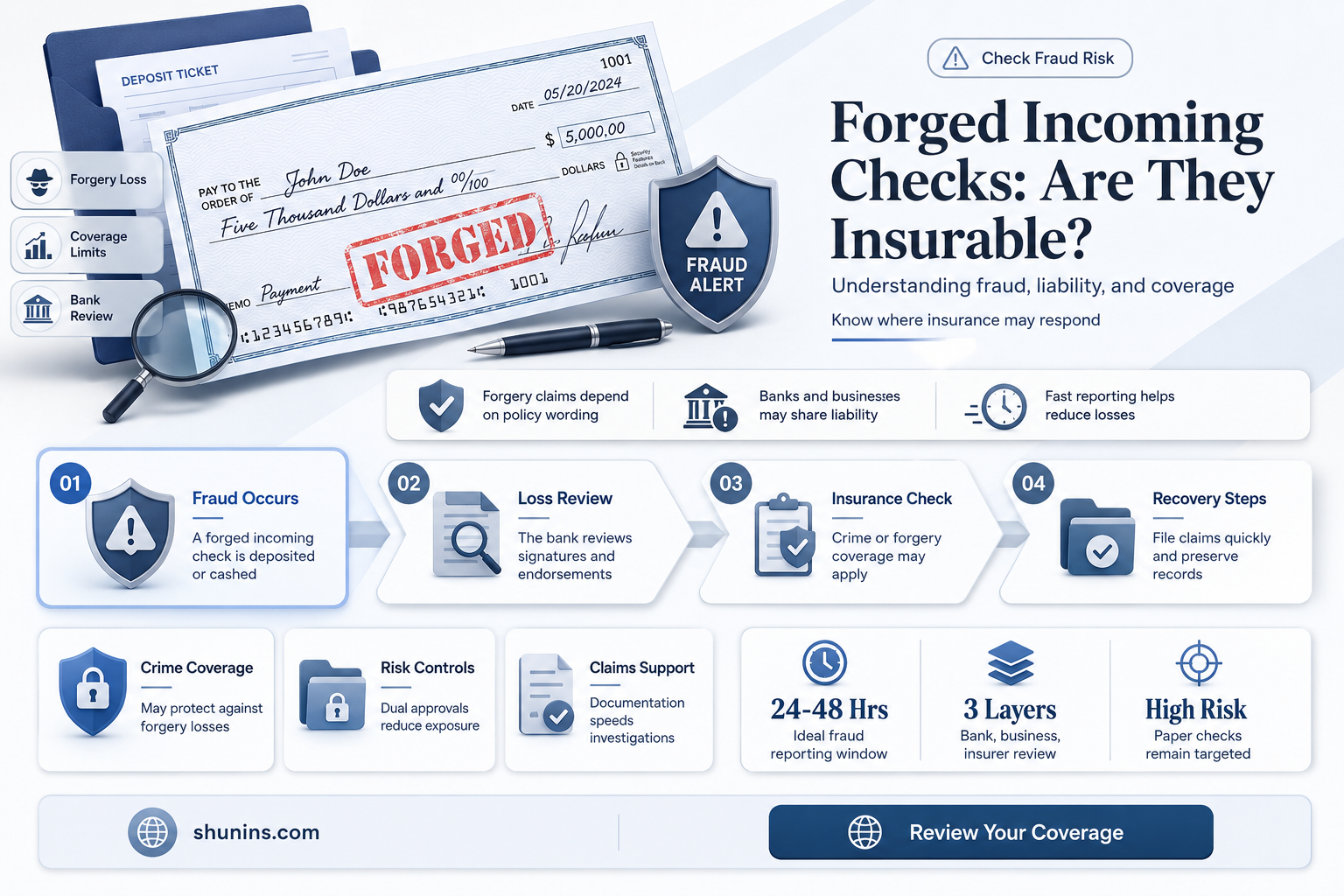

Forged incoming checks can have serious consequences on both the criminal and civil sides of the law. While the forger is liable as the signer of the instrument, the person who cashes or deposits the fraudulent check may also be held responsible depending on the circumstances and the state's laws. Generally, banks are required to reimburse customers for forged checks, but they can investigate to determine if the customer is entitled to reimbursement based on individual circumstances.

| Characteristics | Values |

|---|---|

| Who is liable for forged checks? | The forger is liable as a signer of the instrument. The bank that accepts the forged check is also liable and must cover the loss. |

| What happens if the bank misses a forged check? | The bank will be required to reimburse the customer if it is found to have failed to exercise ordinary care in handling the check. |

| What should you do if you suspect a forged check? | Contact the bank immediately and review your deposit account agreement. You may also need to file a police report. |

| What is the role of the prosecutor in check forgery cases? | The prosecutor charges the thief with a misdemeanor or felony, depending on the state's laws and the specific circumstances of the case. |

| What are the punishments for check fraud? | Punishments vary by state but typically include prison time, fines, and restitution to the bank. |

| How can a financial lawyer help in these situations? | A financial lawyer can assist in interpreting complex financial laws, determining the best course of action, and representing clients in legal proceedings. |

Explore related products

What You'll Learn

![]()

Bank liability and reimbursement

Banks are generally required to reimburse customers for forged checks and are liable for accepting a check that has been forged, altered, or improperly endorsed. However, the bank may not be liable if the customer's failure to exercise ordinary care substantially contributed to an alteration or forgery. If the actions of the customer—the way the check or checkbook was handled, issued, completed, or made payable—contributed to the forgery, the customer may be at least partially liable.

The bank's responsibility to the account holder is not a negligence standard. Instead, as a general rule, the UCC places a duty on the bank of the payor account to make its account holder whole in the event it pays on a charge made through a fraudulent check. The policy rationale behind placing the initial liability on the drawee bank rests on the belief that the relationship between the bank and the account holder is contractual, and the bank's paying a charge based on a fraudulent check violates its agreement with the account holder.

UCC Section 4-406 places a duty on the account holder to discover and notify the bank of a forgery or alteration. The UCC mandates that pursuant to this duty, an account holder must exercise reasonable promptness in discovering and reporting the unauthorized charge but does not define what is considered reasonable promptness. Further, the UCC requires that account holders exercise ordinary care in handling the checks. Under UCC Section 3-406, if a bank can show that the account holder failed to exercise ordinary care, and that failure substantially contributed to an alteration of a check or to the forgery of a signature on the check, that customer may be precluded from making a claim against the bank for reimbursement of that loss.

If you believe your bank has processed a check that has been clearly and wrongfully altered, you should contact a financial lawyer immediately. If you believe there is an error on your statement, contact the bank immediately, as there are required timeframes for notifying the bank of an error.

Federal Insurance: BCBS and Its Benefits

You may want to see also

Explore related products

![]()

Customer liability

When it comes to forged incoming checks, customer liability can be a complex issue that may depend on various factors, including the customer's actions, the bank's policies, and the applicable laws. Here are some key considerations regarding customer liability:

Customer's Actions

In certain situations, a customer's failure to exercise ordinary care in handling their checks may contribute to the forgery or alteration of a check. This could include the way the check or checkbook was handled, issued, or completed. If a bank can demonstrate that the customer's negligence substantially contributed to the forgery, the customer may bear at least partial liability. Therefore, it is essential for customers to take reasonable precautions to protect their checks and promptly notify their bank of any suspected fraud or unauthorized activity.

Bank's Policies and Procedures

Banks typically have policies and procedures in place to address forged or altered checks. These policies may outline the steps that customers need to take if they suspect forgery, such as completing an affidavit stating that they did not authorize the check and filing a police report. Banks are generally required to reimburse customers for forged checks, but they can also investigate the circumstances to determine if the customer's actions contributed to the forgery.

Applicable Laws and Regulations

The laws and regulations surrounding check forgery can vary depending on the jurisdiction. For example, the Uniform Commercial Code (UCC) in the United States imposes certain duties on account holders, such as the duty to discover and promptly notify the bank of any forgery or alteration under UCC Section 4-406. Additionally, under UCC Section 3-406, if a bank can prove that the customer failed to exercise ordinary care and that this failure substantially contributed to the forgery, the customer may be unable to claim reimbursement from the bank.

Time Limitations

It is important to note that there are typically time limitations for filing a claim or lawsuit related to forged checks. Depending on the state or jurisdiction, the depositor may have a limited window of one or two years to take legal action. Therefore, customers must act promptly and seek appropriate guidance if they suspect any fraudulent activity involving their checks.

Seeking Legal Assistance

Dealing with forged incoming checks can be a complex and stressful situation. If a customer believes that their bank has wrongfully processed a forged or altered check, it is advisable to seek legal assistance from a financial lawyer. A lawyer can help interpret the relevant laws, communicate with the bank, and determine the best course of action to protect the customer's rights and financial interests.

In summary, while banks generally bear the initial liability for accepting forged or altered checks, customers also have a responsibility to exercise reasonable care in handling their checks and accounts. By understanding their rights and obligations, customers can take appropriate steps to mitigate the risk of check forgery and resolve any issues that may arise.

Marcus Accounts: Are They Safe and Federally Insured?

You may want to see also

Explore related products

![]()

Criminal punishment

In Minnesota, the penalties are based on the value of the forged checks and the property or services obtained through fraud. Forging a check for $250 or less, with a previous conviction for a similar offense within five years, can result in up to 364 days of imprisonment and/or a fine of up to $3,000. If the forged check is used to obtain property or services worth more than $250 but not exceeding $2,500, the punishment can be up to five years of imprisonment and/or a fine of up to $10,000. For amounts exceeding $35,000, the penalty increases to a maximum of 20 years in prison and/or a fine of up to $100,000.

In Texas, check forgery is also a serious offense, and those accused should seek the help of a criminal defense attorney to navigate the legal complexities and minimize potential consequences. A conviction for check forgery results in a permanent criminal record, making it challenging to secure certain types of employment or obtain specific professional licenses.

It is important to note that the intent to defraud is usually a critical element in check forgery crimes. The accused may argue that they did not participate in the forgery or intend to defraud, even if they altered a real check to increase the amount. The level of the offense and the subsequent punishment can depend on various factors, including the type of document involved and the value of the fraud.

If you suspect that a check has been forged or altered, it is crucial to contact your bank and, if necessary, seek legal advice from a financial or criminal defense lawyer to understand your rights and options.

TD Bank Customers: Is Your Money Federally Insured?

You may want to see also

Explore related products

![]()

Civil consequences

The civil consequences of forged incoming checks can be complex and vary depending on the specific circumstances and applicable laws. Here are some key points to consider:

Forgery of a signature on a check typically imposes no liability on the victim of the forgery. The forger, however, is liable as the signer of the instrument, even if they sign in a name other than their own. The victim of the forgery may need to file a police report and initiate legal action to establish their non-liability and seek redress.

In general, banks are liable for accepting and processing forged, altered, or improperly endorsed checks. They are required to reimburse customers for forged checks and bear the resulting losses. However, if the customer's negligence substantially contributed to the forgery, the bank may not be held liable, and the customer may be partially liable.

The person who cashes or deposits a fraudulent check may also face civil consequences and be held responsible, depending on the circumstances and applicable state laws. It is important to review the bank's forged check policy, which is usually outlined in the account information packet. If the bank refuses to address the issue or provide relevant information, consulting a financial lawyer is advisable.

The statute of limitations for filing a claim or lawsuit against a bank for processing forged checks varies by state, typically ranging from one to two years. Additionally, intent to defraud is a critical element in defining check forgery and related offenses. While it may be challenging to determine intent, it is generally inferred from the defendant's actions, past conduct, or statements.

To summarize, the civil consequences of forged incoming checks can include financial losses, legal liabilities, and the potential for civil litigation. It is important for individuals and businesses to be vigilant in detecting and addressing forged checks promptly and to seek appropriate legal assistance when needed.

Payday Lenders: Are They Federally Insured?

You may want to see also

Explore related products

![]()

Signature forgery

Forgery of a signature on a check is a common form of check fraud, and it is usually quite severely punished. The intent to defraud is an important element in the crime of check forgery. This means that if there was no intention to defraud, the person is not guilty of a crime, even if they committed the overt acts constituting check forgery.

If you suspect you are a victim of signature forgery on a check, it is recommended to seek legal advice from an attorney immediately. A financial lawyer can help you navigate the complex legal process and determine the best course of action. The plaintiff (the person whose signature was forged) bears the burden of proof in these cases.

To prevent signature forgery, there are several technological solutions available, such as secure electronic signature solutions, which can authenticate and encrypt signatures. Additionally, maintaining detailed records of transactions and keeping sensitive documents in secure, access-controlled places can help mitigate the risk of forgery.

In terms of insurance, it is not entirely clear whether forged incoming checks are insurable. However, banks are generally required to reimburse customers for forged checks, unless it is found that the customer's negligence substantially contributed to the forgery. It is important to review your deposit account agreement and contact your bank to understand their specific policies and procedures regarding forged checks.

Deposits at Schools First Credit Union: Are They Insured?

You may want to see also

Frequently asked questions

If you believe a check has been forged, you should contact your bank immediately. You may also wish to consult a financial lawyer, particularly if your bank refuses to answer your questions.

Generally, yes. Banks are required to reimburse customers for forged checks, though they may investigate to determine if the customer is entitled to reimbursement. The bank that accepts the check must reimburse the customer's bank. However, the customer may be held partially liable if their actions contributed to the forgery.

If you are unable to resolve the issue with your bank, you can file a written complaint with the Office of the Comptroller of the Currency's (OCC) Customer Assistance Group. Alternatively, you can file a complaint with the appropriate regulator.

If you are being sued for altering a check, you should contact a financial lawyer immediately. This is a serious issue with potential criminal and civil consequences.