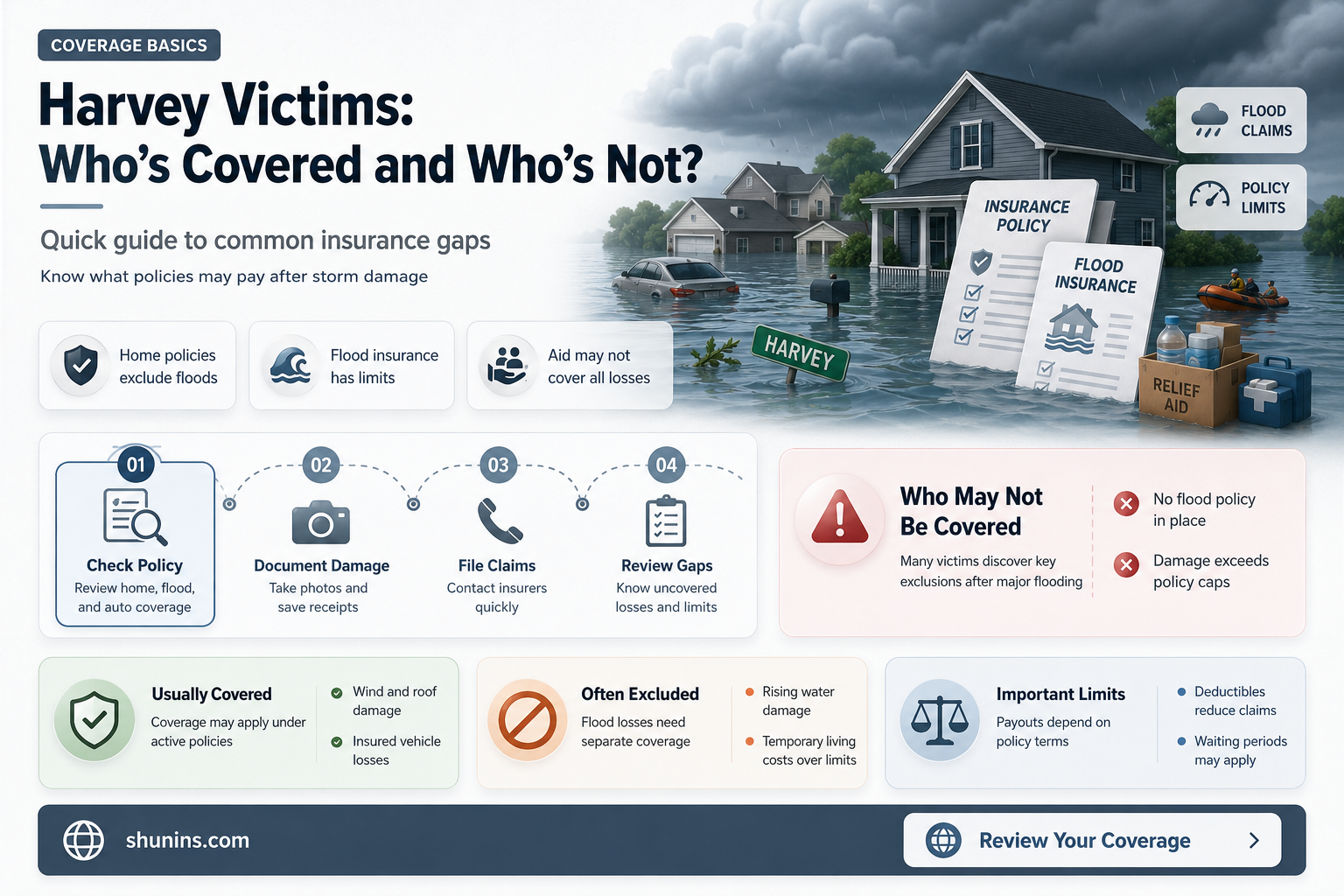

Hurricane Harvey wreaked havoc in Texas, causing unprecedented flooding and wind damage. The storm has resulted in billions of dollars in damage, and many victims are now dealing with insurance companies to recover their losses. However, it is estimated that most Harvey victims lack flood insurance, as personal insurance policies typically exclude flood coverage. This has left many victims facing significant financial burdens as they navigate the recovery process. To make matters worse, there are reports of insurance companies denying or underpaying claims to protect their profits. As a result, many victims are turning to attorneys for help in getting the compensation they deserve.

| Characteristics | Values |

|---|---|

| Deadline to file insurance claims | False claim that victims needed to file insurance claims before September 1, 2017 |

| Number of hail and wind claims involving attorneys and public adjusters | 900% increase |

| Estimated financial damage | $30 to $50 billion |

| Estimated insured losses | $10 to $20 billion |

| Number of people in affected areas with flood insurance | 15% to 20% |

| Estimated insurance payments for wind damage | $2 billion |

| Estimated insured flood claims | $5 billion |

Explore related products

What You'll Learn

![]()

Most Harvey victims lack flood insurance

Hurricane Harvey, which battered southeastern Texas in 2017, is likely to be one of the costliest storms in US history. The storm caused unprecedented flooding in the Houston area, and the total damage is expected to cost tens of billions of dollars.

However, most Harvey victims lack flood insurance. While most Texas homeowners have insurance that covers wind or hail damage, only 15-20% of people in areas affected by Harvey, such as Houston and Corpus Christi, are estimated to carry flood insurance. The Texas Windstorm Insurance Association (TWIA), a residential insurer of last resort, does not cover flood damage. As a result, many victims are likely to be uninsured.

The National Flood Insurance Program, which falls under the Federal Emergency Management Association (FEMA), is the only source of flood insurance for most people. The federal program is paid for by taxpayers and backs flood policies sold and serviced by private insurers. Despite the risks in flood-prone parts of Texas, many people have failed to buy coverage from the NFIP or have let their policies lapse.

The lack of flood insurance among Harvey victims could lead to significant financial challenges for those affected. The storm has caused widespread flooding, and the resulting damage is expected to be costly. Victims without flood insurance may struggle to cover the costs of repairs and rebuilding.

Insurance companies are expected to face substantial claims due to the storm. The Consumer Federation of America projected that insurance payments for wind damage from Hurricane Harvey would likely approach $2 billion, while insured flood claims would exceed $5 billion. The Texas Insurance Code has implemented changes to the claims process, extending deadlines and imposing additional requirements on insurers and insureds.

Hashimoto's Thyroiditis: Life Insurance Considerations and Impacts

You may want to see also

Explore related products

![]()

Victims misled by false insurance claims deadline

In the aftermath of Hurricane Harvey, victims were faced with the challenging task of navigating insurance claims to receive compensation for their losses. Unfortunately, misleading information spread on social media platforms, particularly Facebook and Twitter, claiming that there was a September 1 deadline for filing insurance claims. This misinformation caused confusion and concern among those affected by the hurricane.

It is important to clarify that the September 1 "deadline" referenced in these social media posts was not an official deadline for filing insurance claims related to Hurricane Harvey. The date pertained to a Texas law that came into effect on September 1, 2017, which affected the penalties insurers faced for late claim payments as a result of a lawsuit. Texas State Senator Kelly Hancock, chairman of the State Senate committee overseeing the property and casualty insurance industry, confirmed that the law had no impact on the insurance claims process and that there was no rush for victims to file their claims.

The spread of misinformation by trial lawyers and "storm-chasing attorneys" using scare tactics and taking advantage of vulnerable hurricane victims is unethical and unacceptable. These individuals urged victims to send their insurance claims by certified letter with a return receipt requested before the non-existent deadline, causing unnecessary stress and pressure. It is important for victims to know that they do not need to climb out of their boats or wade through floodwaters to submit their claims immediately.

To ensure that Hurricane Harvey victims receive the assistance they need, it is recommended that they seek help from reputable sources, such as insurance claim attorneys who have experience helping victims of hurricanes and extreme weather events. These attorneys can guide victims through the insurance claims process, protect their rights, and help them maximize their claim value. By seeking professional assistance, victims can avoid being misled by false deadlines and ensure they receive the compensation they deserve.

How Much of Life Flight Does Insurance Cover?

You may want to see also

Explore related products

![]()

Insurance companies profit from denying claims

Hurricane Harvey caused unprecedented flooding in Texas, with the Houston area being the worst hit. Most Harvey victims lacked flood insurance, and only 15-20% of people in affected areas carried flood insurance. The insurance industry has a business model that demands maximum profits, and honoring pledges to customers lowers those profits. Therefore, insurance companies may offer victims far less than they deserve, or their claims may be denied altogether.

In the aftermath of Hurricane Harvey, there was a 900% increase in the number of hail and wind claims involving attorneys and public adjusters. While some lawyers took advantage of the situation by exaggerating damages and suing innocent parties, insurance companies also attempted to mislead victims with carefully crafted statements. For example, some victims were falsely told that they needed to file their claims by a certain date or lose their rights under their insurance policy.

In general, insurance companies profit from denying claims because it lowers their costs and increases their net income. For instance, in the healthcare industry, the six largest private health insurers in the United States enjoyed combined profits of $41 billion in 2021. In the same year, these companies denied more than 42 million in-network claims from patients covered by Affordable Care Act (ACA) marketplace plans. While it is unclear exactly how much profit is made from denying claims, critics argue that the industry's behaviour leaves little doubt that private insurers are gouging patients and public healthcare programs.

Furthermore, denying claims is a "regular business practice" for insurance companies to increase their profits. Insurers are aware that most patients do not exercise their right to appeal when claims are denied and are often unsure how to do so. As a result, patients may delay necessary follow-up care until they can be certain that existing hospital bills will be paid. This results in longer hospital stays, which adds expense and risk to the healthcare system.

To conclude, insurance companies, including those involved in the aftermath of Hurricane Harvey, have been criticized for profiting from denying claims. While it is challenging to quantify the exact amount of profit generated from denied claims, the practice has significant financial implications for both individuals and the healthcare system as a whole.

Virtual Life Insurance Agents: Revolutionizing the Industry

You may want to see also

Explore related products

![]()

Victims may be eligible for federal disaster relief

Victims of Hurricane Harvey may be eligible for federal disaster relief. The storm caused unprecedented flooding in Texas, affecting both homeowners and businesses. While many victims lacked flood insurance, there are other sources of financial assistance available to them.

The National Flood Insurance Program, administered by the Federal Emergency Management Association (FEMA), is the primary source of flood insurance for most people. This federal program is funded by taxpayers and provides coverage for rising waters outside a home. However, only a small percentage of people in the affected areas, such as Houston and Corpus Christi, had flood insurance policies.

The Texas Windstorm Insurance Association (TWIA) provides wind and hail coverage to property owners in designated coastal areas who cannot obtain insurance elsewhere. While TWIA does not cover flood damage, it can provide protection from wind-driven rain and debris. Victims with windstorm damage can file claims with TWIA to receive compensation.

In addition to insurance claims, victims may also seek legal recourse to obtain fair compensation. Attorneys specialising in insurance claims can assist victims in navigating the complex legal landscape and maximising their claims. They can help victims understand their rights, document and assess damages, and negotiate with insurance companies.

It is important to note that deadlines and requirements for filing claims may vary. Victims should promptly notify their insurers and seek legal advice to preserve their rights and ensure they receive the assistance they need.

Child Life and AD&D Insurance: What Parents Need to Know

You may want to see also

Explore related products

![]()

Victims can take steps to protect their property

Victims of Hurricane Harvey can take several steps to protect their property and secure financial assistance. Firstly, it is crucial to contact your insurance company as soon as possible to initiate the claims process. Documenting the damage through photographs and videos can greatly aid in supporting your insurance claim. Additionally, creating a written list of damages, including furnishings and other personal property, can help in itemizing your losses. It is also advisable to retain all receipts and invoices related to repairs, travel, lodging, and other damage-related expenses for reimbursement purposes.

To further safeguard your interests, keep a meticulous record of all communications with your insurance company, adjusters, and other relevant parties. If you cannot locate your insurance policy, don't hesitate to request a copy from your provider. It is also important to verify that you have the appropriate type of coverage for flooding or storm damage, as certain policies may not cover all types of disaster-related losses.

In the aftermath of Hurricane Harvey, victims are encouraged to apply for disaster assistance through www.DisasterAssistance.gov or by calling 1-800-621-3362. Registering for FEMA assistance can provide crucial support during this challenging time. Additionally, contacting your mortgage servicer and utility companies is essential to discuss potential options for managing your financial obligations while dealing with property damage.

Unfortunately, there have been reports of unscrupulous attorneys and public adjusters taking advantage of victims by encouraging lawsuits and exaggerating damages. It is recommended to exercise caution and seek reliable legal counsel if needed. The Texas Windstorm Insurance Association (TWIA) is a valuable resource for property owners in designated coastal areas who may struggle to obtain insurance through private markets. They provide coverage for wind, wind-driven rain, and hail damage. However, it's important to note that TWIA does not cover storm surge or flood damage, and standard flood insurance policies also have limitations.

Life Insurance and Suicide: Payouts and Policies Explained

You may want to see also

Frequently asked questions

No, victims of Hurricane Harvey do not need to file insurance claims by September 1, 2017, as was claimed on social media.

Victims of Hurricane Harvey are likely to make flood and wind damage insurance claims.

Yes, flood damage insurance claims are common after hurricanes. For example, after Hurricane Katrina in 2005, the federal insurance program paid out $16 billion for flood damage.

Victims of Hurricane Harvey who are having issues with their insurance claims can contact a trusted attorney for help.