Life insurance is often seen as a reliable way to provide for loved ones after you're gone, and one of its biggest advantages is the tax relief it offers. Typically, the death benefit your beneficiaries receive isn't taxed as income, meaning they get the full amount to use for expenses like paying off debts, covering funeral costs or securing their future. However, there are some situations where taxes could come into play, and it's important to know when that might happen.

Explore related products

What You'll Learn

![]()

Interest on life insurance payouts

Life insurance death benefits are typically tax-free, but there are exceptions. If the beneficiary of a life insurance policy chooses to receive the payout in installments instead of a lump sum, any interest that accrues on those payments is taxable. This interest is considered taxable income, even though the original death benefit is not.

The IRS considers the interest on life insurance payouts to be taxable income. This means that if you receive a life insurance payout in installments, you must report the interest portion as income on your tax return. The death benefit itself is generally not taxable and does not need to be reported.

It is important to note that the rules and regulations regarding life insurance and taxes can be complex and may vary depending on your location. It is always recommended to consult with a tax professional or financial advisor to understand your specific situation and obligations.

In addition to the interest on life insurance payouts, there are other situations where taxes may apply to life insurance proceeds. For example, if the policy owner leaves the death benefit to their estate instead of directly naming a person as the beneficiary, the proceeds may be subject to estate taxes if the estate's total value exceeds certain thresholds.

Furthermore, if the life insurance policy involves three different people - the insured, the policy owner, and the beneficiary - the death benefit may be subject to gift tax if it exceeds the annual exclusion limit. In such cases, careful planning and consultation with a tax professional are crucial to minimize potential tax liabilities.

Life Insurance: Pyramid Scheme or Legit Business?

You may want to see also

Explore related products

![]()

Life insurance and estate taxes

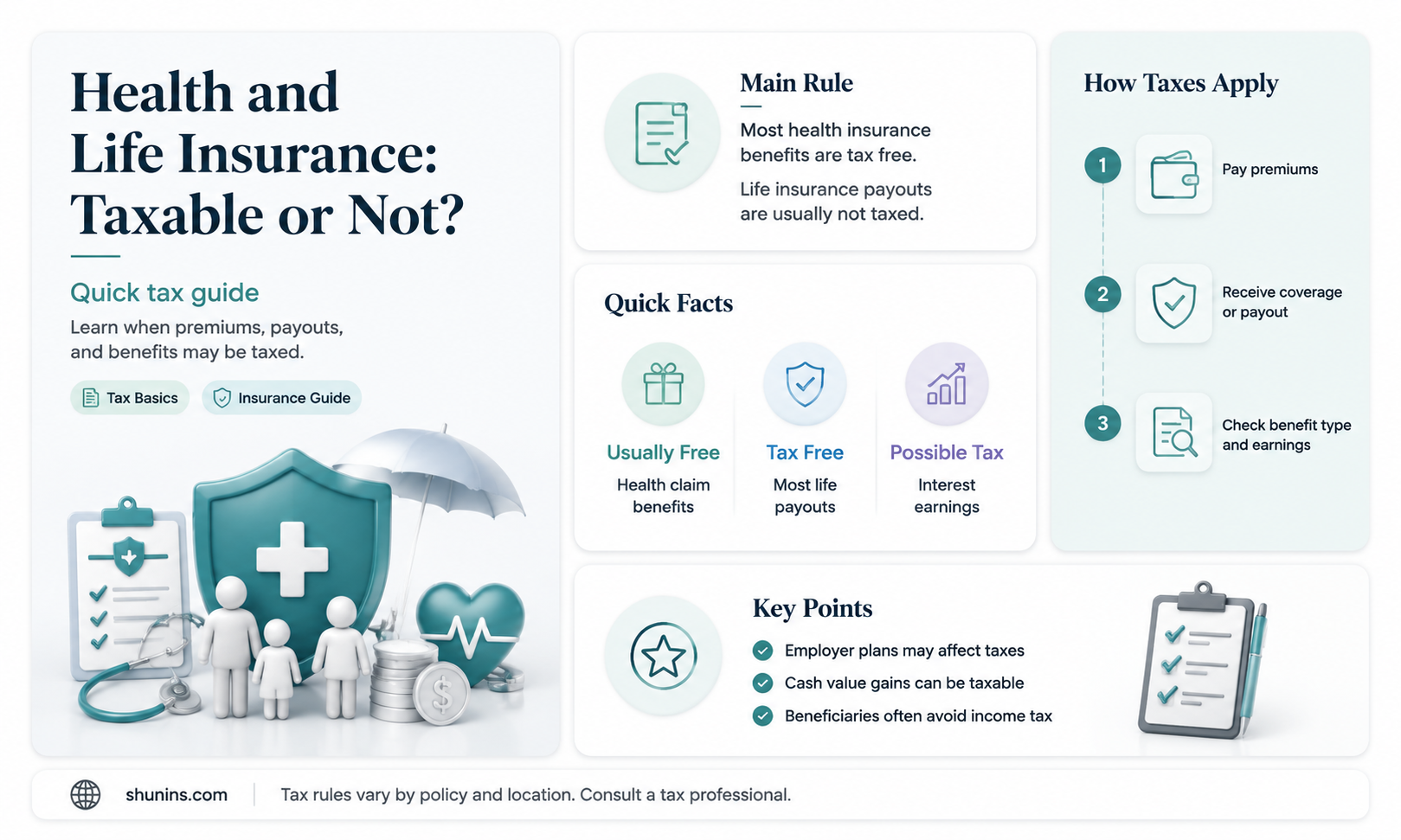

Life insurance proceeds are generally not subject to income or estate taxes. However, there are exceptions to this rule.

If the payout from a life insurance policy is structured to be paid in multiple instalments, these payments may be taxable. This is because the insurer typically holds the principal amount in an interest-bearing account, and so the interest that accumulates on the death benefit is subject to income tax.

If the payout from a life insurance policy becomes part of your estate, it may also be taxed. In 2024, the federal estate tax exemption limit is $13.61 million for an individual. This means that if the total taxable value of your assets exceeds this amount, the IRS will levy an estate tax. If you die while holding a life insurance policy, the IRS will count the payout in the value of your estate, regardless of whether you name a beneficiary.

If you have a will or trust in place and name your estate as the beneficiary of your policy, the life insurance payout can be used to pay estate taxes. However, if you choose one or more individuals as beneficiaries, they won't be held liable for estate tax. They will receive the life insurance payout tax-free, and estate taxes will be paid from other assets you owned.

In addition to the federal estate tax, some states levy their own estate or inheritance taxes. Exemption limits vary among states. For example, in New York, the estate tax threshold is $6.94 million.

To avoid estate taxes, you can transfer ownership of your life insurance policy to another person or entity. Alternatively, you can set up an irrevocable life insurance trust (ILIT). The three-year rule applies to both options, meaning that if you die within three years of the transfer, the full amount of the proceeds will be included in your estate and taxed accordingly.

Life Insurance and Scuba Diving: What's Covered?

You may want to see also

Explore related products

![]()

Cash value withdrawals

It's important to note that different types of life insurance policies have distinct rules regarding cash value withdrawals. For example, with a whole life insurance policy, the cash value grows tax-free, and you can withdraw up to the total premium payments without incurring taxes. On the other hand, a universal life insurance policy's cash value component grows based on market rates, offering more flexibility in adjusting premiums and death benefits.

When considering cash value withdrawals, it's essential to be mindful of potential tax implications. Consulting a tax advisor or a financial professional can help you navigate the complexities of your specific situation and make informed decisions about your life insurance policy.

Additionally, it's worth noting that the rules and regulations regarding life insurance and taxation may vary based on your location. Therefore, seeking guidance from a professional familiar with the laws and regulations in your area is always advisable.

Life Insurance: Maturing and Your Benefits

You may want to see also

Explore related products

![]()

Policy loans

While policy loans can provide quick access to funds, there are some disadvantages to consider. Interest can accumulate over time, potentially draining the policy's cash value. This could lead to a reduction in the cash value growth and the death benefit if the loan remains unpaid. It is crucial to weigh the advantages and disadvantages before deciding to borrow from a life insurance policy, as it may impact the long-term financial security of loved ones.

Life Insurance and Cirrhosis: What Coverage is Offered?

You may want to see also

Explore related products

![TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![]()

Group term life insurance

While group term life insurance provides financial security and peace of mind for employees, it is important to note that it is not always a portable benefit. This means that if an employee leaves their job, they may not be able to take their group term life insurance policy with them.

In terms of taxation, group term life insurance has some nuances. According to the Internal Revenue Service (IRS), employers can provide employees with up to $50,000 of tax-free group term life insurance coverage as a benefit. Any amount of coverage above $50,000 that is paid for by an employer must be recognized as a taxable benefit and included on the employee's W-2 form. This is because the IRS considers the life insurance premiums paid by the employer to be part of the employee's compensation.

It is worth noting that if employees pay the premiums themselves for life insurance purchased through their employer, no income tax is due.

Life Insurance Proceeds: Are Trusts Taxable?

You may want to see also

![TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

![TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UL320_.jpg)

![[Old Version] TurboTax Deluxe 2023, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/719rCYQpjdL._AC_UL320_.jpg)