Health departments play a crucial role in public health by overseeing community wellness initiatives, disease prevention, and healthcare regulations. However, their relationship with network health insurance is often misunderstood. While health departments are not directly part of insurance networks, they collaborate with insurers to ensure access to essential services, promote preventive care, and address public health disparities. This partnership helps align insurance coverage with community health needs, fostering a more integrated approach to healthcare delivery. Understanding this dynamic is key to appreciating how health departments and insurance networks work together to improve population health.

Explore related products

What You'll Learn

![]()

Role of Health Departments in Insurance Networks

Health departments play a pivotal role in shaping the landscape of insurance networks by ensuring that healthcare services are accessible, affordable, and aligned with public health goals. Their involvement often begins with regulatory oversight, where they establish standards for network adequacy, requiring insurers to include a sufficient number of providers within geographic regions. For instance, in California, health departments mandate that insurance networks have at least 85% of enrollees within a 15-mile radius of a primary care provider, ensuring rural and urban populations alike have equitable access. This regulatory function is critical in preventing network narrowness, a common issue where insurers limit provider options to cut costs, often at the expense of patient care.

Beyond regulation, health departments actively collaborate with insurance networks to address public health priorities. During the COVID-19 pandemic, many departments partnered with insurers to waive out-of-pocket costs for testing and vaccination, ensuring widespread access. Similarly, in states like New York, health departments have worked with Medicaid managed care organizations to integrate preventive services, such as diabetes screenings and mental health counseling, into network benefits. These partnerships not only improve health outcomes but also reduce long-term healthcare costs by focusing on early intervention and chronic disease management.

A less obvious but equally important role of health departments is data sharing and analytics. By providing insurers with anonymized health data, departments enable networks to identify high-risk populations and tailor services accordingly. For example, in Florida, health departments shared data on opioid overdose hotspots, prompting insurers to expand access to addiction treatment centers within their networks. This data-driven approach ensures that resources are allocated efficiently, addressing the most pressing health needs of the community.

However, the relationship between health departments and insurance networks is not without challenges. One significant issue is the tension between cost containment and comprehensive care. Insurers often prioritize profitability, leading to disputes over reimbursement rates and covered services. Health departments must balance advocating for patient needs with fostering a sustainable healthcare ecosystem. For instance, in Texas, a health department intervened when an insurer proposed reducing coverage for prenatal care, citing the potential long-term costs of untreated maternal health issues.

To maximize the impact of health departments within insurance networks, stakeholders should adopt a multi-faceted strategy. First, departments should leverage their regulatory authority to enforce stricter network adequacy standards, particularly in underserved areas. Second, they should expand collaborative initiatives, such as joint funding for preventive care programs. Finally, health departments must invest in robust data infrastructure to provide insurers with actionable insights. By taking these steps, health departments can ensure that insurance networks not only meet regulatory requirements but also contribute to the broader goal of improving public health.

Why Insurance Companies Seek Your DNA: Privacy Risks Explained

You may want to see also

Explore related products

$19.99

$9.99 $19.99

![]()

Network Health Insurance Policy Regulations

Health departments play a pivotal role in shaping network health insurance policies, ensuring they align with public health goals and regulatory standards. These departments often act as gatekeepers, reviewing and approving insurance networks to guarantee adequate provider access and quality care for policyholders. For instance, in many states, health departments mandate that insurance networks include a minimum number of primary care physicians, specialists, and mental health providers within a specified geographic radius. This regulatory oversight helps prevent "narrow networks" that limit patient choice and access to essential services.

Consider the regulatory framework in California, where the Department of Managed Health Care requires network adequacy reports from insurers, detailing provider availability and wait times for appointments. These reports are scrutinized to ensure compliance with state standards, such as a maximum 15-day wait for non-urgent specialist appointments. Failure to meet these benchmarks can result in fines or network expansion mandates. Such regulations underscore the health department’s role in balancing insurer profitability with consumer protection, ensuring that network health insurance policies serve the public interest.

From a practical standpoint, policyholders should scrutinize their network health insurance plans for compliance with local health department regulations. For example, if you’re in New York, verify that your plan meets the state’s requirement for at least 30% of providers to be primary care physicians. Additionally, check if mental health services are covered at parity with physical health services, as mandated by federal and state laws. Proactively reviewing these details can prevent unexpected out-of-network costs and ensure access to necessary care.

A comparative analysis reveals that health department regulations vary significantly across states, creating a patchwork of network adequacy standards. For instance, Texas has more lenient requirements, allowing insurers greater flexibility in network design, while Massachusetts enforces stricter provider-to-patient ratios. These disparities highlight the need for federal guidelines to standardize network adequacy, ensuring consistent access to care nationwide. Until such standards emerge, consumers must navigate state-specific regulations to make informed insurance choices.

In conclusion, health departments are instrumental in regulating network health insurance policies, ensuring they meet public health standards and provide adequate access to care. By enforcing network adequacy requirements, these departments protect consumers from limited provider options and subpar services. Policyholders should familiarize themselves with local regulations to maximize their insurance benefits and advocate for better coverage when needed. As the healthcare landscape evolves, the role of health departments in shaping network insurance policies will remain critical to achieving equitable and accessible care.

Riverside County's Top Medical Insurance Options

You may want to see also

Explore related products

$26.04 $35.95

![]()

Health Department Oversight of Insurance Providers

Health departments play a pivotal role in ensuring that insurance providers adhere to regulatory standards, safeguarding the interests of policyholders. Their oversight extends to monitoring network adequacy, which ensures that insurers maintain a sufficient number of healthcare providers within their networks. For instance, in California, the Department of Managed Health Care (DMHC) requires insurers to meet specific provider-to-enrollee ratios, such as one primary care physician per 1,000 enrollees in urban areas. This regulatory measure prevents insurers from offering plans with inadequate access to care, a common issue in rural or underserved regions.

Analyzing the impact of health department oversight reveals a dual benefit: it protects consumers while fostering accountability among insurers. When health departments audit network directories, they often uncover discrepancies, such as providers listed as in-network who are no longer accepting new patients. A 2021 audit by the New York State Department of Financial Services found that 42% of provider directories contained inaccuracies, leading to stricter enforcement and fines for non-compliant insurers. These actions not only correct immediate issues but also deter future violations, ensuring long-term compliance.

To navigate this regulatory landscape, insurance providers must adopt proactive strategies. First, they should conduct regular internal audits of their provider networks, verifying accuracy and updating directories in real time. Second, insurers should invest in technology that streamlines provider credentialing and network management, reducing the likelihood of errors. For example, platforms like BetterDoctor use AI to verify provider information, ensuring compliance with health department standards. Third, insurers should establish clear communication channels with health departments, facilitating transparency and swift resolution of issues.

A comparative analysis highlights the varying degrees of oversight across states. While some states, like Massachusetts, have robust health department frameworks that actively monitor insurer performance, others rely on federal guidelines with minimal state-level intervention. This disparity underscores the need for standardized oversight practices nationwide. For instance, the federal government could mandate uniform network adequacy standards, ensuring consistent consumer protection regardless of location. Such a measure would level the playing field for insurers while enhancing access to care for all enrollees.

In conclusion, health department oversight of insurance providers is a critical mechanism for ensuring network integrity and consumer protection. By enforcing regulatory standards, conducting audits, and promoting transparency, health departments hold insurers accountable while safeguarding policyholders’ access to care. Insurers, in turn, must embrace proactive compliance strategies to navigate this regulatory environment effectively. As the healthcare landscape evolves, strengthening oversight mechanisms will remain essential to addressing emerging challenges and upholding the principles of equitable access and quality care.

Medical and Dental Insurance: Choosing the Best Coverage

You may want to see also

Explore related products

$72.21 $179.99

![]()

Public Health Impact of Network Insurance

Network insurance models, where health departments collaborate with insurers, can significantly amplify public health initiatives by leveraging shared resources and data. For instance, in regions where local health departments partner with network insurers, vaccination rates for preventable diseases like influenza and measles have shown a 15-20% increase compared to non-network areas. This synergy allows health departments to use insurer networks to disseminate health education materials, schedule screenings, and track outcomes more efficiently. By integrating public health goals into insurance provider networks, these partnerships create a structured pathway to reach underserved populations, ensuring that preventive care becomes a routine part of healthcare delivery rather than an afterthought.

One critical mechanism through which network insurance impacts public health is by reducing barriers to care for chronic disease management. Insurers often incentivize providers within their networks to follow evidence-based protocols for conditions like diabetes or hypertension, while health departments contribute population-level data to identify high-risk areas. For example, a collaborative program in California combined insurer-funded telehealth services with health department-led community workshops, resulting in a 30% improvement in blood sugar control among diabetic patients aged 45-65. Such initiatives demonstrate how network insurance can bridge the gap between individual care and population health, turning fragmented efforts into cohesive strategies.

However, the success of these partnerships hinges on addressing potential pitfalls, such as misaligned priorities between insurers and health departments. While insurers focus on cost containment, health departments prioritize disease prevention and health equity. A case study from Texas highlights how a network insurance program initially failed to improve maternal health outcomes because insurers prioritized short-term cost savings over long-term preventive measures. To avoid this, stakeholders must establish clear, shared metrics—such as reduced hospital readmissions or increased prenatal care access—and ensure transparency in data sharing and decision-making processes.

To maximize the public health impact of network insurance, health departments should adopt a proactive role in shaping network policies. This includes advocating for expanded coverage of preventive services, such as mental health screenings for adolescents or cancer screenings for adults over 50, and negotiating contracts that reward providers for achieving population health milestones. For example, a pilot program in New York incentivized network providers with a 10% reimbursement bonus for reducing smoking rates in their patient populations, leading to a 12% decline in smoking-related hospitalizations. By embedding public health objectives into the financial and operational frameworks of network insurance, health departments can drive systemic change that benefits entire communities.

The Right Time: Medical Insurance for Seniors Over 70

You may want to see also

Explore related products

$91.95 $87.95

$24.99 $24.99

$9.97 $19.99

![]()

Challenges in Health Department-Insurance Collaboration

Health departments and insurance networks often struggle to align their goals, creating friction in collaboration. Health departments prioritize population health, focusing on preventive measures and community well-being, while insurers emphasize cost containment and individual policyholder outcomes. This misalignment can lead to conflicting priorities, such as when a health department pushes for widespread vaccination campaigns, but insurers hesitate to cover costs unless directly tied to individual claims. Bridging this gap requires clear communication and shared metrics that value both population health and financial sustainability.

One practical challenge arises in data sharing and privacy regulations. Health departments rely on aggregate data to identify health trends and plan interventions, but insurers are bound by HIPAA and other privacy laws that restrict data sharing. For instance, a health department might need access to claims data to track chronic disease prevalence, but insurers may only share de-identified data, limiting its utility. Establishing secure data-sharing agreements and investing in interoperable systems can mitigate this issue, though it requires significant time and resources.

Financial incentives further complicate collaboration. Insurers operate on a profit-driven model, often avoiding investments in preventive services that yield long-term benefits but lack immediate returns. Health departments, funded by taxpayer dollars, may propose initiatives like smoking cessation programs or mental health screenings that insurers view as costly. To overcome this, health departments can structure programs to demonstrate return on investment, such as by quantifying reduced emergency room visits or hospitalizations. Pilot programs with measurable outcomes can also build trust and encourage insurer participation.

Another hurdle is the fragmented nature of insurance networks. Health departments often work with multiple insurers, each with its own policies, coverage criteria, and administrative processes. This fragmentation can delay or derail collaborative efforts, as seen in initiatives like flu shot campaigns where insurers vary in reimbursement rates or covered locations. Standardizing certain processes across insurers, such as prior authorization requirements for preventive services, could streamline collaboration. Health departments can advocate for policy changes at the state level to encourage uniformity.

Finally, workforce capacity and expertise differences pose challenges. Health department staff are trained in public health strategies, while insurance professionals focus on claims processing and risk management. This knowledge gap can lead to misunderstandings or inefficiencies. Cross-training initiatives, such as workshops on public health principles for insurers or seminars on insurance operations for health department staff, can foster mutual understanding. Collaborative projects should also include diverse teams to ensure all perspectives are considered from the outset.

By addressing these challenges through strategic planning, policy advocacy, and relationship-building, health departments and insurance networks can create more effective partnerships that improve health outcomes for individuals and communities alike.

Insurance Companies Mandating RBT Certification for Behavioral Therapists

You may want to see also

Frequently asked questions

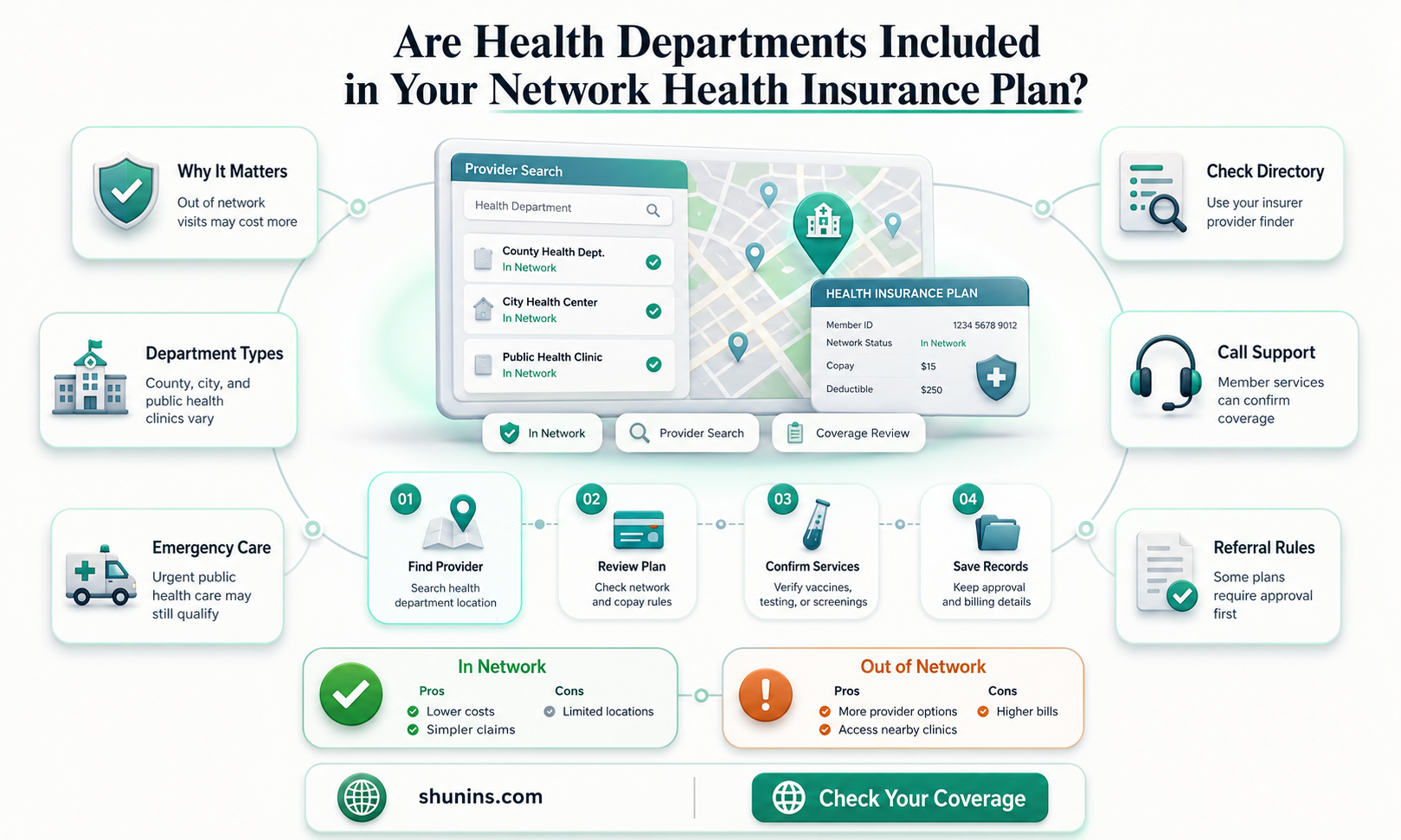

When a health department is in-network with your health insurance, it means they have a contract with your insurance provider to offer services at pre-negotiated rates, typically resulting in lower out-of-pocket costs for you.

Check your insurance provider’s website or call their customer service to verify if your local health department is included in their network of providers.

Yes, using an in-network health department usually means lower copays, coinsurance, and deductibles compared to out-of-network providers.

Covered services vary by insurance plan but often include preventive care, immunizations, screenings, and certain public health programs. Check your plan details for specifics.

Yes, but out-of-network services typically cost more since they are not subject to pre-negotiated rates, and your insurance may cover a smaller portion or none of the expenses.