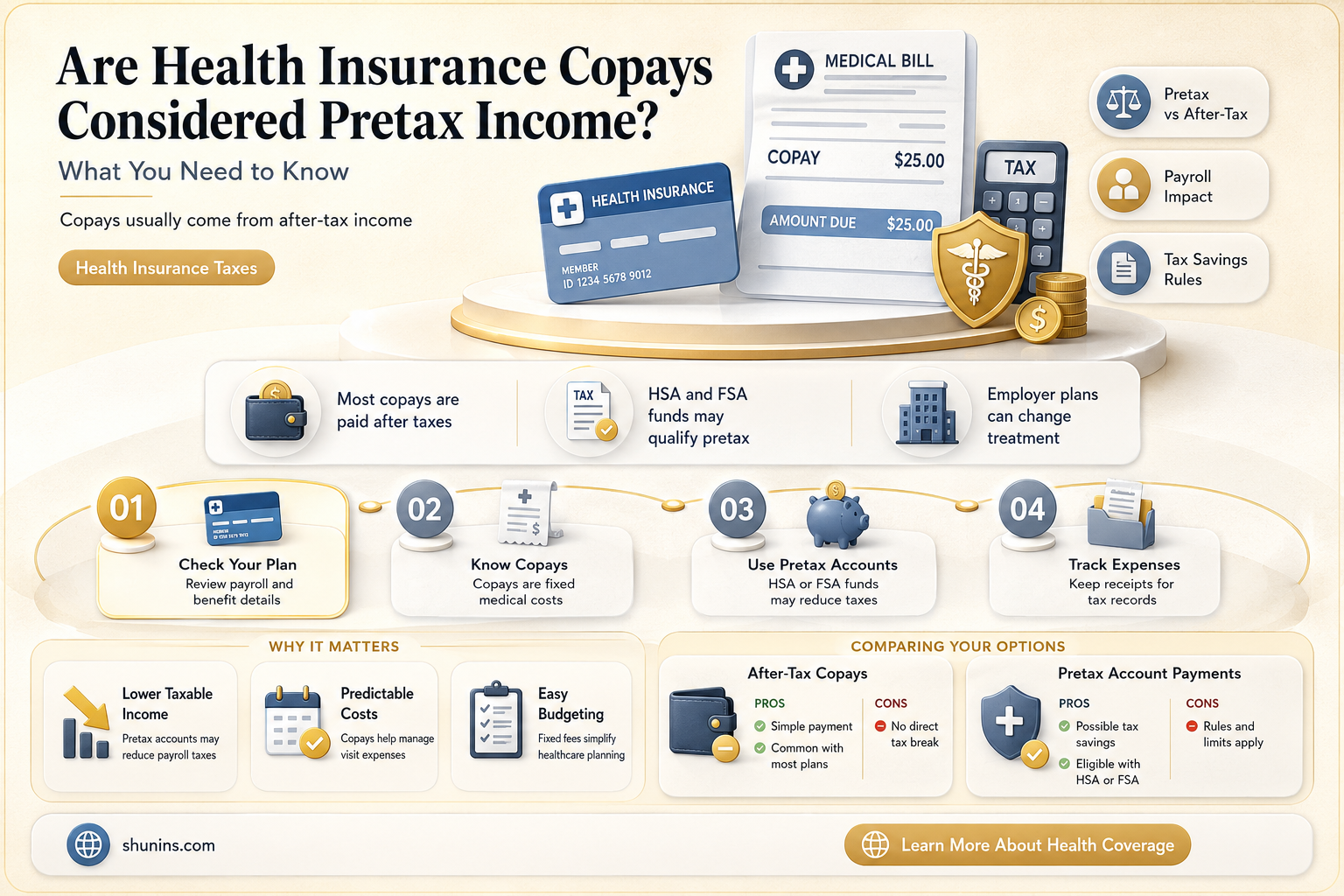

Health insurance copays are a common feature of many health insurance plans, requiring policyholders to pay a fixed amount for covered services at the time of care. A frequent question among employees and individuals is whether these copays are considered pretax income, which could impact their taxable earnings and overall financial planning. Understanding the tax treatment of copays is essential, as it can affect take-home pay, tax liabilities, and the overall value of employer-sponsored health benefits. While premiums paid for health insurance through employer-sponsored plans are often deducted from pretax income, copays typically do not qualify for the same treatment, as they are considered an out-of-pocket expense rather than a premium payment. This distinction highlights the importance of carefully reviewing tax regulations and consulting with a financial advisor or tax professional to fully grasp the implications of health insurance copays on one's financial situation.

| Characteristics | Values |

|---|---|

| Definition of Copay | A fixed amount paid by the insured at the time of service. |

| Tax Treatment of Copays | Generally not considered pretax income. |

| Reason for Non-Pretax Status | Copays are paid with after-tax dollars from personal funds. |

| Pretax Options for Healthcare Costs | Health Savings Accounts (HSAs), Flexible Spending Accounts (FSAs). |

| IRS Stance | Copays are not deductible as medical expenses unless exceed 7.5% of AGI. |

| Employer-Sponsored Plans | Copays in employer plans are typically not pretax. |

| Exceptions | No known exceptions; copays remain post-tax. |

| Reimbursement Eligibility | Copays cannot be reimbursed through HSAs or FSAs. |

| Impact on Taxable Income | Copays do not affect taxable income as they are post-tax expenses. |

| Latest Update (as of 2023) | No changes in tax treatment of copays under current IRS regulations. |

Explore related products

What You'll Learn

![]()

IRS Guidelines on Copayments

Copayments, those fixed amounts you pay for healthcare services, often leave people wondering about their tax implications. The IRS provides clear guidelines on whether these out-of-pocket expenses qualify as pretax income. Understanding these rules is crucial for maximizing your tax benefits and avoiding potential pitfalls.

IRS Publication 502: Your Roadmap

The Internal Revenue Service (IRS) Publication 502, "Medical and Dental Expenses," is the definitive guide to understanding which healthcare costs are deductible. It explicitly states that copayments for medical care are considered eligible expenses for the medical expense deduction. This means you can potentially deduct copayments from your taxable income, reducing your overall tax liability.

Deductibility Thresholds: A Numbers Game

It's important to note that not all copayments automatically qualify for deduction. The IRS imposes a threshold: only medical expenses exceeding 7.5% of your adjusted gross income (AGI) are deductible. This means you need to track all your eligible medical expenses, including copayments, throughout the year to see if you meet this threshold.

Documentation is Key: Keep Those Receipts

To claim copayments as deductions, meticulous record-keeping is essential. Retain receipts, Explanation of Benefits (EOB) statements, and any other documentation that verifies the amount and nature of each copayment. This documentation will be crucial if the IRS requests proof of your deductions.

FSAs and HSAs: A Pretax Advantage

While copayments themselves aren't directly considered pretax income, utilizing Flexible Spending Accounts (FSAs) or Health Savings Accounts (HSAs) can effectively make them so. Contributions to these accounts are made with pretax dollars, allowing you to pay for copayments and other eligible medical expenses with tax-free funds. This strategy can significantly reduce your taxable income and overall healthcare costs.

Dental and Medical Insurance: Overhead and Understood

You may want to see also

Explore related products

![]()

Pretax vs. Post-tax Copay Deductions

Health insurance copays can be deducted from your income either pre-tax or post-tax, and understanding the difference is crucial for maximizing your financial benefits. Pre-tax deductions are taken from your income before taxes are calculated, effectively lowering your taxable income and potentially reducing your overall tax liability. Post-tax deductions, on the other hand, are taken from your income after taxes have been applied, meaning they don't directly impact your taxable income.

Analytical Perspective:

Let's consider an example to illustrate the impact of pre-tax vs. post-tax copay deductions. Suppose you have a monthly health insurance copay of $200, and your annual income is $50,000. If your copay is deducted pre-tax, your taxable income would be reduced by $2,400 (200 x 12), resulting in a lower tax liability. Assuming a marginal tax rate of 22%, this could save you approximately $528 in taxes annually. In contrast, if your copay is deducted post-tax, your taxable income remains at $50,000, and you wouldn't receive any tax benefits from your copay contributions.

Instructive Approach:

To determine whether your health insurance copay is deducted pre-tax or post-tax, review your pay stub or consult your employer's benefits administrator. Look for terms like "pre-tax deductions," "Section 125 plan," or "cafeteria plan," which typically indicate pre-tax treatment. If your copay is currently deducted post-tax, consider discussing with your employer the possibility of switching to a pre-tax arrangement, such as a Flexible Spending Account (FSA) or Health Savings Account (HSA). These accounts allow you to contribute pre-tax dollars towards eligible medical expenses, including copays.

Comparative Analysis:

While pre-tax copay deductions offer clear tax advantages, there are some limitations to consider. For instance, FSAs have a "use-it-or-lose-it" provision, meaning any unused funds at the end of the plan year may be forfeited. HSAs, on the other hand, allow funds to roll over indefinitely, but they're only available to individuals with high-deductible health plans. Post-tax deductions, while not offering direct tax benefits, provide more flexibility in terms of fund usage and may be preferable for individuals who prioritize simplicity over tax savings.

Practical Tips:

To optimize your copay deductions, consider the following strategies:

- If you have predictable medical expenses, such as regular prescriptions or specialist visits, estimate your annual copay costs and contribute accordingly to a pre-tax FSA or HSA.

- For individuals aged 55 or older, consider "catch-up contributions" to an HSA, which allow for additional pre-tax contributions of up to $1,000 per year.

- Keep detailed records of your medical expenses, including copays, to ensure you're maximizing your pre-tax contributions and to facilitate reimbursement claims if necessary.

- Review your health insurance plan's coverage and copay structure annually, as changes to your plan or tax laws may impact the most advantageous deduction strategy.

By understanding the nuances of pre-tax vs. post-tax copay deductions and implementing strategic contributions, you can minimize your tax liability and maximize the value of your health insurance benefits. Remember to consult with a tax professional or financial advisor to determine the best approach for your individual circumstances.

Will Insurance Cover Riot Damage? Understanding Your Policy's Limits

You may want to see also

Explore related products

![]()

Health Savings Accounts (HSAs) Role

Health Savings Accounts (HSAs) serve as a triple tax-advantaged tool for managing healthcare expenses, but their role in relation to copays is often misunderstood. HSAs are not directly used to pay copays under most high-deductible health plans (HDHPs), which are required to pair with an HSA. Instead, HSAs function as a long-term savings vehicle for qualified medical expenses, including deductibles, coinsurance, and certain over-the-counter medications. While copays are typically paid out-of-pocket at the time of service, the funds in an HSA grow tax-free and can be used to reimburse yourself for these expenses later, effectively reducing their after-tax cost.

To maximize the benefits of an HSA, consider a strategic approach to paying copays. For instance, if you have a $30 copay for a doctor’s visit, pay it upfront with non-HSA funds. Later, when you face larger, qualified expenses like prescription costs or lab fees, use your HSA to cover those instead. This preserves the tax-advantaged funds for higher-impact expenses while allowing your HSA balance to grow over time. For example, a 35-year-old contributing the maximum $3,850 annually to an HSA could accumulate over $100,000 by age 65, assuming a 7% annual return, providing a substantial cushion for future healthcare needs.

One common misconception is that HSAs are only for immediate medical expenses. In reality, they are a powerful retirement savings tool. Unlike Flexible Spending Accounts (FSAs), HSAs have no "use-it-or-lose-it" rule, and unused funds roll over indefinitely. For retirees, HSAs offer tax-free withdrawals for Medicare premiums and out-of-pocket medical costs, making them a critical component of retirement planning. For example, a retiree could use HSA funds to cover the $1,800 annual Medicare Part B premium without incurring taxes, effectively lowering their overall healthcare burden.

When evaluating the role of HSAs in managing copays and other expenses, it’s essential to consider your overall financial strategy. If you’re in a lower tax bracket, paying copays out-of-pocket and saving HSA funds for future expenses may yield greater long-term benefits. Conversely, if you’re in a higher tax bracket, using HSA funds for immediate expenses can provide immediate tax relief. For instance, a taxpayer in the 24% bracket could save $240 in taxes on a $1,000 medical expense by using HSA funds instead of taxable income.

Incorporating an HSA into your healthcare financial plan requires careful coordination with your insurance coverage. For families, contributing to an HSA while maintaining a separate emergency fund for unexpected copays and deductibles can provide both flexibility and security. For example, a family of four with an HDHP might allocate $2,000 annually to an HSA while keeping $1,000 in a checking account for immediate copay needs. This dual approach ensures readiness for both routine and unforeseen medical costs while optimizing tax advantages.

Will Major Insurers Cover the Iconic G-Wagen? Exploring Options

You may want to see also

Explore related products

![]()

Employer-Sponsored Plan Rules

Employer-sponsored health insurance plans often allow employees to pay premiums on a pre-tax basis, reducing taxable income and increasing take-home pay. However, copays—fixed amounts paid at the time of service—are typically not considered pre-tax expenses. This distinction arises because copays are classified as out-of-pocket costs rather than premiums. Understanding this rule is crucial for employees to accurately plan their healthcare expenses and tax liabilities.

From a practical standpoint, employees should recognize that while premiums deducted from their paychecks lower their taxable income, copays do not offer the same tax advantage. For example, if an employee pays a $30 copay for a doctor’s visit, that $30 is paid with after-tax dollars. In contrast, if their monthly premium is $200 and deducted pre-tax, their taxable income is reduced by $2,400 annually. This difference highlights the importance of budgeting for both pre-tax and post-tax healthcare costs.

Employers play a key role in clarifying these rules for their workforce. They should provide detailed explanations of how pre-tax deductions work for premiums and why copays fall outside this category. Additionally, employers can offer tools like Flexible Spending Accounts (FSAs) or Health Savings Accounts (HSAs) to help employees manage out-of-pocket costs more effectively. For instance, funds from an HSA can be used to pay copays tax-free, though contributions to such accounts are also pre-tax.

A comparative analysis reveals that while copays are not pre-tax, other out-of-pocket expenses, such as deductibles and coinsurance, may be reimbursed through pre-tax accounts like HSAs or FSAs. This creates an opportunity for employees to strategize their healthcare spending. For example, an employee with a high-deductible health plan (HDHP) paired with an HSA can use pre-tax dollars to cover copays indirectly by saving for larger expenses. This approach maximizes tax benefits while addressing the limitation of copays being post-tax.

In conclusion, employer-sponsored plan rules clearly differentiate between pre-tax premiums and post-tax copays. Employees should leverage available tools like HSAs or FSAs to offset the lack of pre-tax treatment for copays. Employers, meanwhile, should educate their staff on these distinctions and encourage proactive financial planning for healthcare expenses. By doing so, both parties can optimize the value of their health insurance benefits within the constraints of current tax regulations.

Understanding Medical Necessity: Insurance Company Definitions and Criteria

You may want to see also

Explore related products

![]()

Tax Implications for Employees

Health insurance copays, those fixed amounts employees pay for medical services, are not considered pretax income. This distinction is crucial for understanding the tax implications employees face. Unlike premiums paid through employer-sponsored plans, which are often deducted from gross income on a pretax basis, copays are paid with after-tax dollars. This means employees have already paid taxes on the income used to cover these expenses, and they cannot deduct copays as a pretax benefit.

Understanding this difference is essential for employees to accurately assess their taxable income and plan their finances accordingly.

While copays themselves are not pretax, employees can leverage other tax-advantaged accounts to offset out-of-pocket medical expenses. Flexible Spending Accounts (FSAs) and Health Savings Accounts (HSAs) allow employees to set aside pretax dollars for qualified medical expenses, including copays. FSAs are typically employer-sponsored and have a "use-it-or-lose-it" rule, meaning funds must be spent within the plan year. HSAs, on the other hand, are available to those with high-deductible health plans and offer more flexibility, as funds roll over annually and can grow tax-free. By contributing to these accounts, employees can effectively reduce their taxable income while preparing for copay and other medical costs.

It’s important to note that not all medical expenses qualify for reimbursement through FSAs or HSAs. Generally, copays for preventive care, prescription medications, and certain treatments are eligible, but cosmetic procedures or over-the-counter medications without a prescription may not be. Employees should review the IRS guidelines or consult their plan administrator to ensure their expenses qualify. Additionally, keeping detailed records of medical expenses is crucial for substantiating claims and avoiding potential tax issues.

For employees with significant medical needs, understanding the interplay between copays, pretax accounts, and tax deductions can lead to substantial savings. For instance, if an employee anticipates frequent doctor visits or ongoing prescriptions, maximizing contributions to an FSA or HSA can reduce their overall tax burden. However, employees should be cautious not to overcontribute to FSAs, as unused funds are forfeited at the end of the year. Strategic planning, such as estimating annual medical expenses and adjusting contributions accordingly, can help employees optimize their tax benefits while managing copay costs effectively.

In summary, while health insurance copays are not pretax income, employees have tools at their disposal to mitigate the financial impact of these expenses. By utilizing FSAs, HSAs, and careful planning, employees can reduce their taxable income, save on medical costs, and ensure they are making the most of available tax-advantaged options. Proactive management of these resources is key to navigating the complexities of healthcare expenses in a tax-efficient manner.

Travel Vaccines: Medical Insurance Coverage Explained

You may want to see also

Frequently asked questions

No, health insurance copays are not considered pretax income. They are paid with after-tax dollars and are not deductible from your taxable income.

Yes, you can use pretax dollars from a Flexible Spending Account (FSA) or Health Savings Account (HSA) to pay for eligible copays, effectively reducing your taxable income.

No, copays are separate from premiums. Premiums paid with pretax dollars (e.g., through employer-sponsored plans) are pretax, but copays are paid with after-tax dollars.

Copays alone are not tax-deductible. However, they may contribute to your total medical expenses, which could be deductible if they exceed 7.5% of your adjusted gross income (AGI).

No, using pretax FSA or HSA funds to pay copays does not affect your taxable income, as these funds are already excluded from taxation.