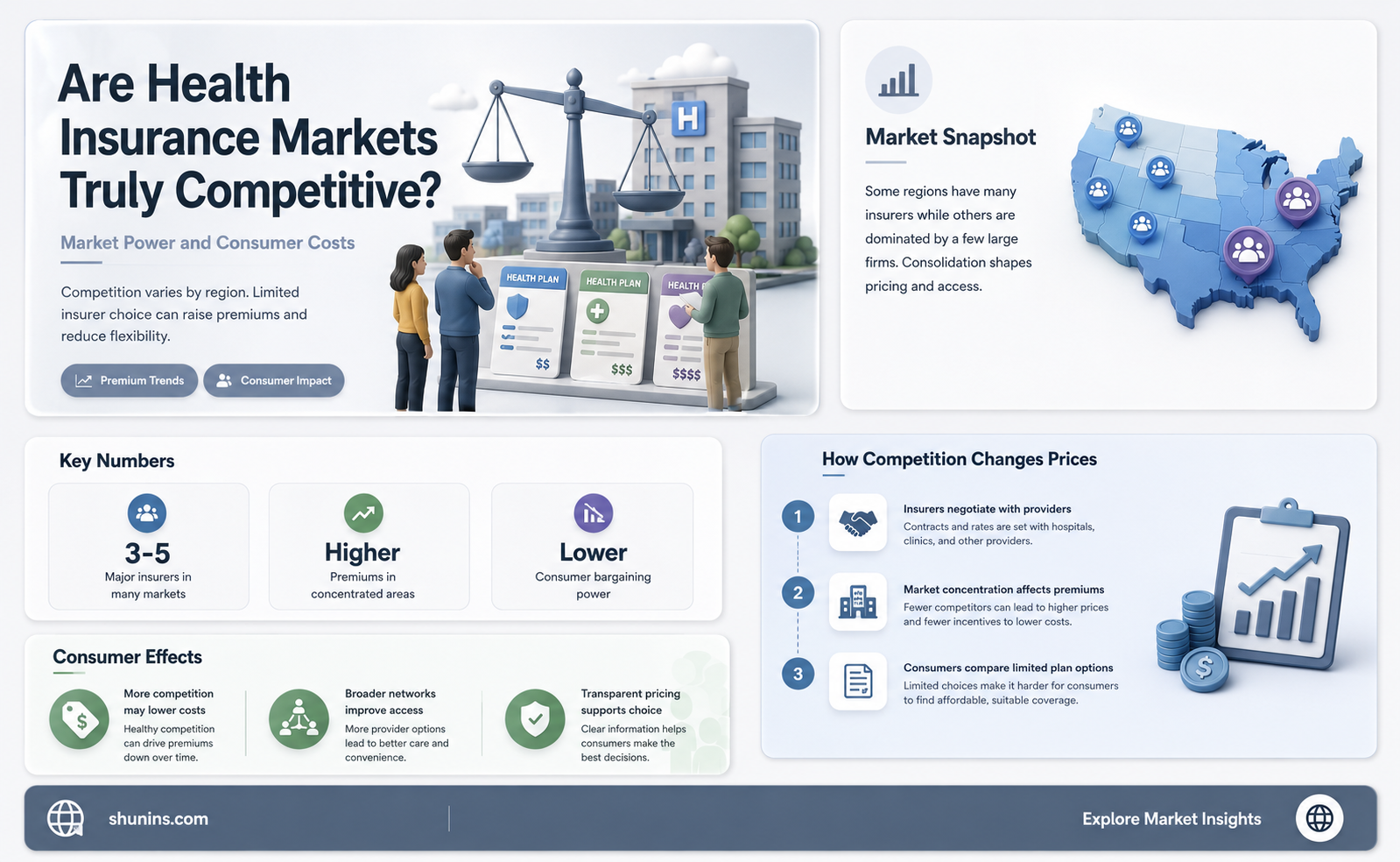

The question of whether health insurance markets are competitive is a critical issue in healthcare economics, as it directly impacts affordability, quality, and accessibility of care. While proponents argue that competition among insurers can drive down premiums and improve service offerings, critics highlight significant barriers to true competition, such as market consolidation, high entry barriers, and information asymmetry between insurers and consumers. Additionally, the complexity of health insurance products and regulatory frameworks often limits consumer choice, raising concerns about whether these markets function competitively or if they are dominated by a few large players, ultimately affecting the overall efficiency and equity of healthcare systems.

Explore related products

What You'll Learn

![]()

Market Concentration and Monopoly Power

Health insurance markets often exhibit high levels of market concentration, where a few large firms dominate the industry. This phenomenon raises concerns about monopoly power and its implications for competition, consumer choice, and pricing. For instance, in the United States, the top five health insurers control over 50% of the market, limiting options for consumers and providers alike. Such concentration can stifle innovation, reduce price competition, and lead to higher premiums, as dominant firms face less pressure to improve services or lower costs.

Analyzing market concentration requires examining metrics like the Herfindahl-Hirschman Index (HHI), which measures the size of firms in relation to the overall market. A high HHI score indicates a less competitive market, often prompting regulatory scrutiny. For example, mergers between large insurers are frequently reviewed by antitrust authorities to prevent further consolidation. However, even without mergers, dominant firms can exploit their market power through exclusive provider contracts, limiting access for smaller competitors and maintaining their stronghold.

To mitigate the effects of monopoly power, policymakers can implement targeted interventions. One approach is to encourage market entry by reducing regulatory barriers for new insurers, particularly in underserved areas. Another strategy is to strengthen antitrust enforcement, challenging anticompetitive practices such as price-fixing or market allocation. Additionally, promoting transparency in pricing and network adequacy can empower consumers to make informed choices, though this requires robust data collection and dissemination mechanisms.

A comparative analysis reveals that countries with more fragmented health insurance markets, such as Germany or the Netherlands, often experience greater competition and lower premiums. These nations typically have multiple insurers competing for consumers, coupled with strong regulatory frameworks that prevent monopolistic behavior. In contrast, highly concentrated markets like those in some U.S. states struggle with affordability and accessibility, highlighting the need for structural reforms to foster competition.

Practically, consumers can take steps to navigate concentrated markets more effectively. First, compare plans using state or federal health insurance marketplaces, which aggregate options for easier comparison. Second, consider provider networks carefully, as dominant insurers often have broader networks but may charge higher premiums. Finally, advocate for policy changes that promote competition, such as public options or expanded Medicaid programs, which can introduce new players and reduce reliance on monopolistic firms. By understanding market concentration and its consequences, stakeholders can work toward a more competitive and equitable health insurance landscape.

Top Mobile Insurance Providers: Which Company Offers the Best Coverage?

You may want to see also

Explore related products

![]()

Consumer Choice and Plan Diversity

Health insurance markets often tout consumer choice as a hallmark of competition, but the reality is more nuanced. While a plethora of plans may appear on exchanges or through employers, true diversity in coverage options remains elusive for many. For instance, in rural areas, consumers frequently face limited choices, with only one or two insurers dominating the market. This scarcity restricts not only the types of plans available but also the networks of providers, leaving individuals with fewer specialists or hospitals to choose from. Without genuine plan diversity, the promise of competition falters, as consumers are forced to settle for options that may not align with their health needs or financial situations.

Consider the role of plan design in shaping consumer choice. Insurers often offer tiered plans—bronze, silver, gold, and platinum—each with varying premiums, deductibles, and out-of-pocket maximums. While this structure appears to provide options, it can be misleading. For example, a bronze plan might have lower monthly premiums but higher deductibles, making it unsuitable for individuals with chronic conditions who require frequent medical care. Conversely, a platinum plan may offer lower out-of-pocket costs but come with a premium that is unaffordable for many. Without clear, standardized information about these trade-offs, consumers may struggle to make informed decisions, undermining the competitive ideal of choice.

To enhance plan diversity and empower consumers, policymakers and insurers must address two critical issues: transparency and customization. First, insurers should be required to provide clear, comparable information about plan benefits, costs, and provider networks. Tools like standardized summaries or online comparison platforms can help consumers navigate their options more effectively. Second, insurers could offer more customizable plans, allowing individuals to tailor coverage to their specific needs. For example, a young, healthy individual might opt for a plan with lower premiums and higher deductibles, while someone with a family history of cancer might prioritize broader specialist coverage. Such customization would not only increase diversity but also foster genuine competition by rewarding insurers that meet unique consumer demands.

A cautionary note: increasing plan diversity alone is insufficient if underlying market dynamics remain unchanged. In monopolistic or oligopolistic markets, where a few insurers dominate, even a wide array of plans may not translate into meaningful competition. For instance, if all available plans have narrow networks or exclude certain high-cost treatments, consumers are still constrained. Addressing this requires broader reforms, such as incentivizing new insurers to enter underserved markets or regulating anti-competitive practices like provider exclusivity contracts. Without such measures, plan diversity risks becoming a facade, masking deeper structural issues that limit consumer choice.

In conclusion, consumer choice and plan diversity are essential but fragile components of competitive health insurance markets. While offering multiple plans is a start, true competition requires transparency, customization, and structural reforms to ensure that options are meaningful and accessible. By focusing on these elements, stakeholders can move beyond superficial diversity and create a market that genuinely serves the needs of all consumers. Practical steps, such as implementing standardized plan comparisons or piloting customizable coverage models, can pave the way for a more competitive and consumer-friendly health insurance landscape.

Geisinger Gold: A Medicare Supplement Insurance Option?

You may want to see also

Explore related products

![]()

Price Transparency and Comparability

Price transparency in health insurance markets remains a critical yet elusive goal. Consumers often face a labyrinth of costs—premiums, deductibles, copays, and out-of-pocket maximums—that are difficult to decipher. A 2021 study by the Kaiser Family Foundation found that only 30% of respondents felt confident in their ability to compare health plan prices. This opacity hinders competition, as consumers cannot easily identify the best value for their needs. Without clear, standardized pricing information, insurers face less pressure to lower costs or improve services, perpetuating a market that favors providers over buyers.

To address this, policymakers and industry leaders must prioritize tools that enhance comparability. For instance, standardized cost-sharing metrics and user-friendly platforms could allow consumers to compare plans side by side. The implementation of the No Surprises Act in 2022, which protects patients from unexpected medical bills, is a step in the right direction. However, more is needed. Insurers should be required to provide personalized estimates for common procedures, such as MRIs or childbirth, based on a consumer’s specific plan and provider network. This would empower individuals to make informed decisions and drive insurers to compete on price and quality.

Consider the example of prescription drug pricing. Many health plans offer tiered formularies, but the actual cost of a medication can vary widely depending on the pharmacy or whether a generic is available. A 60-day supply of a brand-name cholesterol medication might cost $150 under one plan but only $50 under another. Without transparent pricing, consumers may unknowingly choose a plan that leaves them overpaying. Tools like GoodRx have emerged to fill this gap, but such solutions should be integrated directly into insurance platforms to ensure accessibility for all age groups, including older adults who may be less tech-savvy.

The lack of price transparency also disproportionately affects small businesses and individuals purchasing insurance on the marketplace. For example, a 45-year-old self-employed graphic designer might struggle to compare Bronze, Silver, and Gold plans without clear breakdowns of costs. A practical tip for such consumers is to use government-run marketplaces like Healthcare.gov, which offer standardized summaries of benefits and coverage. Additionally, reaching out to insurance brokers can provide personalized guidance, though this may come with additional fees.

Ultimately, achieving price transparency and comparability requires a collaborative effort. Regulators must enforce stricter disclosure requirements, while insurers should invest in technology that simplifies cost comparisons. Consumers, too, must advocate for their right to clear information. Until these changes are implemented, health insurance markets will remain less competitive than they could be, leaving many to navigate a system that prioritizes complexity over clarity.

BlueCross BlueShield: Understanding Your Medical Insurance Options

You may want to see also

Explore related products

![The Candlestick Trading Bible: [3 in 1] The Ultimate Guide to Mastering Candlestick Techniques, Chart Analysis, and Trader Psychology for Market Success](https://m.media-amazon.com/images/I/61eKxh-x7FL._AC_UY218_.jpg)

![]()

Regulatory Impact on Competition

Regulations shape the competitive landscape of health insurance markets by dictating how insurers operate, price, and innovate. For instance, the Affordable Care Act (ACA) mandated essential health benefits, preventing insurers from excluding pre-existing conditions. While this increased access, it also standardized plans, reducing product differentiation and potentially stiffing competition. Insurers now compete less on coverage scope and more on network breadth, customer service, and cost-sharing structures. This regulatory-driven shift highlights how well-intentioned rules can inadvertently homogenize offerings, leaving consumers with fewer unique choices.

Consider the impact of state-level regulations on market entry. States with stringent licensing requirements and rate review processes often limit the number of insurers willing to participate. For example, in states like Wyoming or West Virginia, fewer than five insurers dominate the individual market. This concentration reduces competitive pressure, allowing dominant players to raise premiums without fear of losing customers. Conversely, states like California or New York, with more lenient entry rules, boast over 10 active insurers, fostering price competition and innovation. Policymakers must balance consumer protections with barriers to entry to avoid creating oligopolies.

A persuasive argument emerges when examining the role of regulatory oversight in pricing. Rate review processes, mandated in 37 states, require insurers to justify premium increases. While this protects consumers from excessive hikes, it can also discourage insurers from entering volatile markets. For instance, in 2023, a proposed 15% premium increase in Florida was reduced to 8% after regulatory scrutiny, potentially deterring new entrants. This dynamic underscores the trade-off between affordability and competition. Regulators must strike a delicate balance, ensuring transparency without stifling the financial viability of insurers.

Comparing international models reveals the diverse effects of regulation. In Germany, a multi-payer system with strict price controls has led to over 100 competing insurers, as low administrative costs enable smaller players to thrive. Conversely, the UK’s National Health Service (NHS) limits private insurer involvement, reducing competition but ensuring universal access. These examples illustrate how regulatory frameworks can either foster or suppress competition based on their design. U.S. policymakers could draw lessons from such models, tailoring regulations to encourage innovation while maintaining affordability.

Finally, a practical takeaway for stakeholders is to monitor regulatory trends proactively. Insurers should invest in compliance teams to navigate evolving rules, while consumers can leverage tools like Healthcare.gov to compare standardized plans. Policymakers, meanwhile, must conduct regular impact assessments to ensure regulations achieve their intended goals without unintended consequences. By staying informed and adaptable, all parties can navigate the complex interplay between regulation and competition in health insurance markets.

Top Insurance Companies Rated by A.M. Best: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Provider Network Limitations and Access

Health insurance markets often tout competition as a driver of affordability and quality, but provider network limitations can undermine these benefits. Insurers negotiate contracts with specific healthcare providers to form networks, restricting policyholders to these in-network options for full coverage. While this strategy helps insurers control costs, it can severely limit patient access, especially in rural or underserved areas where network options are scarce. For instance, a 2021 study found that 40% of rural counties had access to only one insurer on the Affordable Care Act marketplace, effectively eliminating choice and competition.

Consider the case of a patient with a rare condition requiring a specialist. If that specialist is out-of-network, the patient faces higher out-of-pocket costs or must switch providers, potentially disrupting continuity of care. This scenario highlights the tension between insurer cost-control measures and patient access to necessary care. Narrow networks, which include fewer providers, are particularly problematic. A 2019 analysis revealed that 45% of silver-level ACA plans had narrow networks, often excluding top-tier hospitals and specialists.

To navigate these limitations, patients should scrutinize provider directories during open enrollment. Verify that preferred doctors, hospitals, and specialists are in-network, and confirm that the network includes providers with expertise in specific health needs. For example, a patient with diabetes should ensure the network includes endocrinologists and certified diabetes educators. Additionally, understand the appeals process for out-of-network care, as insurers may grant exceptions in cases where in-network options are inadequate.

Policymakers and insurers must address these limitations to foster genuine competition. Expanding network adequacy standards and increasing transparency about provider availability can empower consumers to make informed choices. For instance, requiring insurers to include at least one provider in each specialty within a 30-mile radius could improve access in rural areas. Until such reforms are implemented, patients must remain vigilant advocates for their own care, balancing cost and access within the constraints of their insurance networks.

Why Lease Companies Demand Higher Liability Insurance Coverage Explained

You may want to see also

Frequently asked questions

Health insurance markets vary in competitiveness depending on factors like the number of insurers, regulatory environments, and market concentration. In some regions, a few large insurers dominate, reducing competition, while others have more players, fostering competitive pricing and options.

Competition in health insurance markets can lead to lower premiums, improved coverage options, and better customer service as insurers strive to attract and retain policyholders. It also encourages innovation in plan designs and wellness programs.

Limited competition can result from high barriers to entry, such as regulatory hurdles, large capital requirements, and dominant market positions held by a few insurers. Additionally, provider consolidation and narrow networks can reduce consumer choice and stifle competition.