Health insurance rates have been a topic of growing concern for many individuals and families, as recent trends indicate a steady increase in premiums across the board. Factors such as rising healthcare costs, inflation, and an aging population are contributing to this upward trajectory, leaving policyholders to wonder if relief is in sight. With the added complexities of policy changes and market dynamics, understanding the reasons behind these hikes and exploring potential solutions has become essential for those seeking affordable coverage in an increasingly expensive healthcare landscape.

| Characteristics | Values |

|---|---|

| Trend | Health insurance rates are generally increasing across the US. |

| Average Increase (2023) | Approximately 5-7% for individual market plans (varies by state and plan type). |

| Factors Driving Increases | * Medical Inflation: Rising costs of healthcare services, prescription drugs, and technology. * Post-Pandemic Costs: Increased demand for healthcare services and catching up on deferred care. < * Economic Factors: Inflation and labor shortages impacting healthcare providers. < * Policy Changes: Changes in government regulations and subsidies can influence rates. |

| State Variations | Increases vary significantly by state due to differences in regulations, market competition, and provider costs. |

| Impact on Consumers | Higher premiums, deductibles, and out-of-pocket costs for individuals and families. |

| Mitigation Efforts | * Government Subsidies: Premium tax credits through the Affordable Care Act (ACA) can offset costs for eligible individuals. * Employer-Sponsored Plans: Employers may absorb some cost increases, but employees may still see higher contributions. * Consumer Choices: Shopping around for plans, considering high-deductible plans with HSAs, or exploring alternative coverage options. |

| Future Outlook | Rates are expected to continue rising in the near future, though the pace may vary depending on economic conditions and policy changes. |

Explore related products

What You'll Learn

![]()

Economic Factors Driving Rate Increases

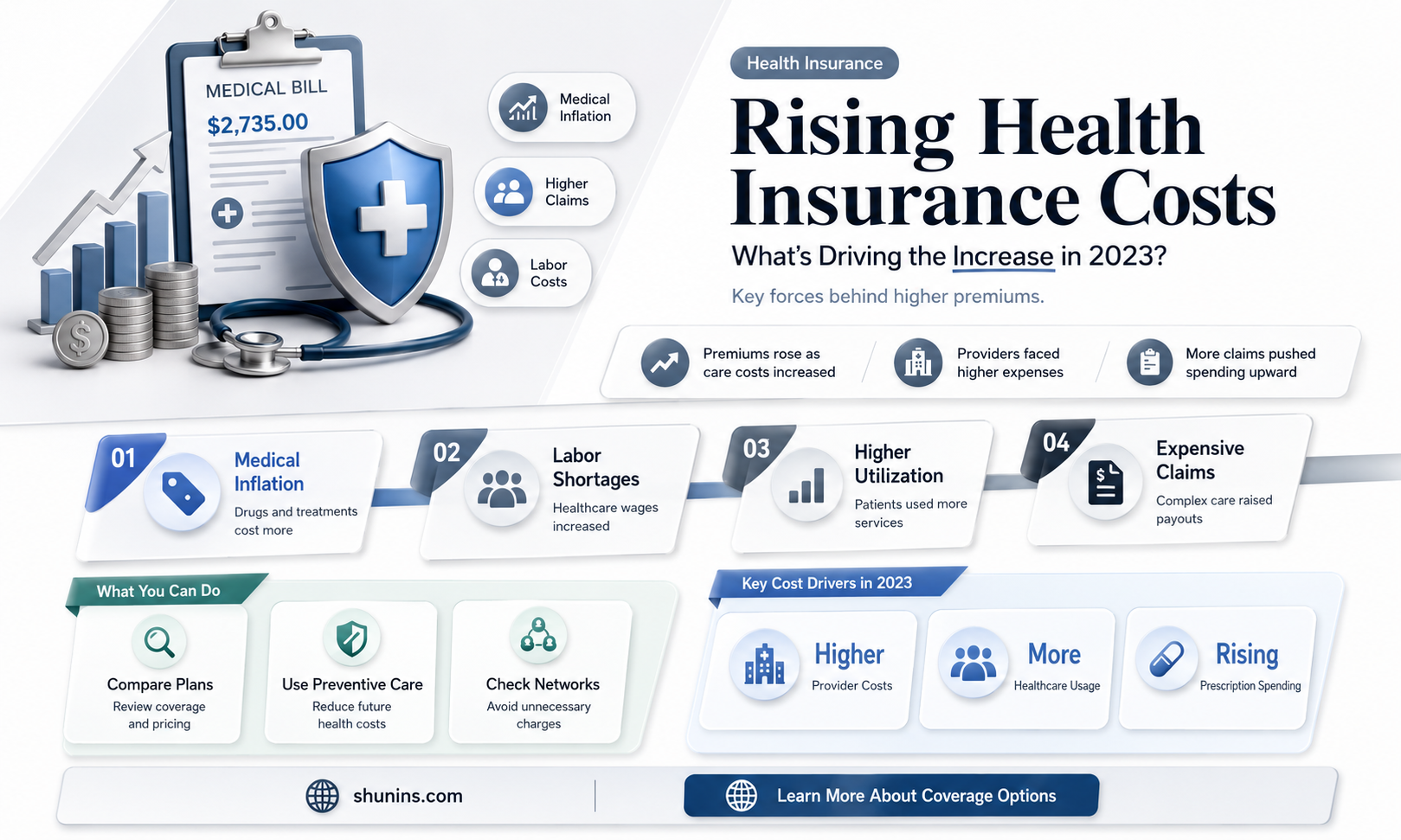

Health insurance rates are climbing, and economic forces are at the helm. One of the primary drivers is the relentless rise in healthcare costs. From 2010 to 2020, U.S. healthcare spending grew at an average annual rate of 4.3%, outpacing inflation. This surge is fueled by expensive medical technologies, high prescription drug prices, and an aging population requiring more intensive care. For instance, specialty drugs, which treat complex conditions like cancer and rheumatoid arthritis, can cost upwards of $100,000 annually per patient. Insurers, facing these escalating expenses, have little choice but to pass the burden onto policyholders through higher premiums.

Another economic factor is the impact of inflation on the broader economy. Inflation erodes the purchasing power of money, making goods and services more expensive. In the healthcare sector, this translates to higher wages for medical professionals, increased costs for medical supplies, and pricier facility maintenance. For example, the cost of personal protective equipment (PPE) skyrocketed during the COVID-19 pandemic, adding millions to healthcare providers’ operational expenses. Insurers must account for these inflationary pressures, further contributing to rate increases. Policyholders, particularly those on fixed incomes, feel the pinch as premiums consume a larger share of their budgets.

The labor market also plays a significant role in driving up health insurance rates. A tight job market, where unemployment is low, often leads to higher wages as employers compete for talent. While this benefits workers, it also increases the cost of employer-sponsored health insurance. Employers typically cover a portion of premiums, but as wages rise, so does the overall cost of providing benefits. For instance, a 5% increase in wages can translate to a 3-4% rise in insurance premiums. Small businesses, in particular, struggle to absorb these costs, sometimes opting to reduce coverage or shift more expenses to employees.

Lastly, economic uncertainty and policy changes create volatility in the insurance market. For example, shifts in government regulations, such as changes to the Affordable Care Act (ACA), can alter the risk pool and affect premiums. Insurers must anticipate these changes and adjust rates accordingly. Additionally, economic downturns can lead to more individuals relying on public insurance programs, reducing the number of healthier, privately insured individuals. This adverse selection further drives up costs for those remaining in the private market. To mitigate risk, insurers often raise rates preemptively, creating a cycle of increasing premiums even in uncertain economic times.

Practical steps can help individuals navigate these economic pressures. First, compare plans annually during open enrollment to find the best value. High-deductible health plans (HDHPs) paired with health savings accounts (HSAs) can lower premiums while offering tax advantages. Second, take advantage of employer-sponsored wellness programs, which may reduce insurance costs by promoting healthier lifestyles. Finally, stay informed about policy changes and economic trends that could impact rates. While economic factors driving rate increases are complex, proactive strategies can help mitigate their financial impact.

Medicaid and Medical Insurance: What's the Difference?

You may want to see also

Explore related products

![]()

Impact of Healthcare Inflation on Premiums

Healthcare costs have been rising steadily, outpacing general inflation for decades. This trend directly impacts health insurance premiums, as insurers must adjust rates to cover the increasing expenses of medical care. From 2010 to 2020, healthcare prices in the U.S. rose by 27%, compared to a 19% increase in the Consumer Price Index (CPI). Such disparities highlight the unique pressures healthcare inflation places on insurance markets.

Consider the mechanics of premium calculation. Insurers estimate future claims based on historical data and projected trends. When healthcare costs rise—due to factors like expensive new treatments, drug price hikes, or higher hospital fees—insurers must increase premiums to maintain solvency. For instance, a new cancer therapy costing $100,000 per patient forces insurers to spread this expense across their policyholders, raising premiums for all. This ripple effect demonstrates how innovation in healthcare, while beneficial, often comes with financial consequences.

Employers and individuals absorb these increases differently. Employers sponsoring health plans typically share premium costs with employees, but as rates rise, they may shift a larger portion to workers or reduce benefits to control expenses. For example, a 10% premium increase might lead an employer to raise employee contributions from 20% to 25% of the total cost. Individuals purchasing insurance independently face the full brunt of these hikes, often forcing difficult choices between coverage and affordability. A family plan that cost $1,200 monthly in 2020 could exceed $1,500 by 2025, straining household budgets.

Mitigating the impact of healthcare inflation requires proactive strategies. Policyholders can opt for high-deductible plans paired with health savings accounts (HSAs) to lower premiums while saving tax-free for medical expenses. For instance, a healthy 30-year-old might save $500 annually by choosing a $2,500 deductible plan over a $500 deductible option. Additionally, preventive care—such as annual check-ups or vaccinations—can reduce long-term costs by catching issues early. Employers can negotiate with insurers for value-based care models, tying payments to health outcomes rather than service volume, potentially slowing premium growth.

Ultimately, healthcare inflation’s impact on premiums is a complex interplay of medical advancements, market dynamics, and policy decisions. While insurers must adapt to rising costs, consumers and employers can take steps to manage their financial exposure. Understanding these forces empowers individuals to make informed choices, balancing coverage needs with budgetary constraints in an increasingly expensive healthcare landscape.

Navigating the Medical Insurance Maze: Getting Your Own Coverage

You may want to see also

Explore related products

![]()

Role of Policy Changes in Rate Hikes

Policy changes often serve as the catalyst for health insurance rate hikes, reshaping the financial landscape for both insurers and consumers. When governments introduce new mandates—such as expanding coverage for pre-existing conditions or requiring insurers to cover additional services like mental health or maternity care—insurers must adjust their pricing to account for the increased costs. For instance, the Affordable Care Act (ACA) mandated essential health benefits, leading to premium increases as insurers incorporated these services into their plans. While these changes aim to improve access and care quality, they directly contribute to higher rates, illustrating the delicate balance between policy goals and economic realities.

Consider the ripple effect of policy-driven rate hikes through a practical example: a 45-year-old individual in Texas saw their monthly premium rise by 12% in 2023 following state-level policy changes that expanded coverage for telehealth services. While telehealth improves accessibility, insurers argued that the increased utilization of virtual care drove up administrative and operational costs. This scenario highlights how even well-intentioned policies can inadvertently inflate premiums, underscoring the need for policymakers to anticipate and mitigate such financial impacts.

To navigate policy-induced rate hikes, consumers should proactively review their plans annually during open enrollment. Compare premiums, deductibles, and out-of-pocket maximums across different tiers (e.g., Bronze, Silver, Gold) to identify the best value. For example, a family of four earning $80,000 annually might save $2,400 by switching from a Gold plan to a Silver plan with a Health Savings Account (HSA), provided they don’t anticipate high medical expenses. Additionally, leveraging subsidies available through healthcare exchanges can offset costs for those earning up to 400% of the federal poverty level.

A comparative analysis reveals that policy changes in different regions yield varying rate impacts. In California, where state-level policies have imposed stricter regulations on insurer profit margins, premium increases have been moderated compared to states with fewer controls. Conversely, in Florida, where policy changes have focused on reducing insurer oversight, premiums have risen sharply. This contrast suggests that the structure and intent of policies—whether they prioritize consumer protection or market flexibility—play a pivotal role in determining the magnitude of rate hikes.

Ultimately, while policy changes are essential for shaping a more equitable healthcare system, their role in driving rate hikes cannot be overlooked. Consumers must stay informed about legislative updates and their potential financial implications, while policymakers should adopt a data-driven approach to balance accessibility with affordability. For instance, implementing phased rollouts of new mandates or pairing them with cost-containment measures, such as capping prescription drug prices, could mitigate premium increases. By fostering collaboration between stakeholders, the impact of policy changes on insurance rates can be managed more effectively, ensuring that healthcare remains both accessible and sustainable.

Seeley Medical: Insurance Coverage and Your Options

You may want to see also

Explore related products

![]()

Effect of Aging Population on Costs

The aging population is a significant driver of rising health insurance rates, and understanding this demographic shift is crucial for anyone navigating the complexities of healthcare costs. As life expectancy increases, the number of individuals aged 65 and older is projected to nearly double by 2050, according to the U.S. Census Bureau. This surge in seniors directly impacts healthcare demand, as older adults typically require more medical services, from chronic disease management to specialized care. For instance, Medicare spending per beneficiary increases dramatically with age, with those over 85 costing the system nearly three times as much as those aged 65 to 74. This heightened utilization translates into higher premiums for everyone, as insurers spread the escalating costs across their policyholders.

Consider the financial strain this places on both individuals and the healthcare system. Chronic conditions like diabetes, heart disease, and arthritis are more prevalent among older adults, often requiring ongoing medications, frequent doctor visits, and costly procedures. For example, the average annual prescription drug expenditure for seniors is over $3,000, compared to $1,000 for younger adults. Insurers must account for these expenses, leading to higher premiums and out-of-pocket costs. Additionally, the increased need for long-term care services, such as nursing homes or in-home assistance, further exacerbates the financial burden. Without proactive measures, this trend will continue to push insurance rates upward, making healthcare less affordable for all age groups.

To mitigate the impact of an aging population on health insurance costs, policymakers and individuals must take targeted actions. One effective strategy is promoting preventive care and wellness programs tailored to seniors. For instance, initiatives that encourage regular screenings, healthy diets, and physical activity can reduce the incidence of costly chronic diseases. Employers can also play a role by offering retirement health savings plans or partnering with insurers to provide age-specific coverage options. On a personal level, individuals approaching retirement should carefully evaluate Medicare plans, considering supplemental policies to cover gaps in traditional Medicare. By addressing the unique needs of older adults, society can work toward a more sustainable healthcare system.

A comparative analysis of countries with aging populations reveals varying approaches to managing healthcare costs. Japan, for example, has implemented a long-term care insurance system funded by premiums from all citizens, ensuring that the elderly receive necessary services without overwhelming the national budget. In contrast, the U.S. relies heavily on private insurance and out-of-pocket spending, leading to higher costs for individuals. Learning from such models, the U.S. could explore hybrid solutions that combine public and private funding to distribute the financial burden more equitably. Ultimately, the effect of an aging population on health insurance rates is a global challenge, but with innovative strategies, it can be managed to ensure affordability and accessibility for future generations.

Apply for Insurance Collection in Pennsylvania: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

How Medical Technology Advances Influence Rates

Medical technology advances are a double-edged sword for health insurance rates. On one hand, innovations like robotic surgery and precision medicine improve outcomes and reduce long-term costs. For instance, robotic-assisted knee replacements can shorten hospital stays from 3-5 days to just 24 hours, slashing recovery-related expenses by up to 40%. On the other hand, the initial cost of adopting these technologies—a single da Vinci surgical robot costs $2 million—often gets passed to consumers through higher premiums. Insurers must balance the promise of future savings against the immediate financial burden of integrating cutting-edge tools.

Consider the rise of wearable health monitors, such as smartwatches that track heart rhythms or glucose levels. While these devices empower individuals to manage chronic conditions proactively—potentially reducing emergency room visits by 25% for diabetics—insurers face a dilemma. Should they subsidize these tools, which can cost $300-$500 per unit, or risk higher claims from unmanaged conditions? Some providers, like UnitedHealthcare, now offer discounts for policyholders who use wearables, but this strategy shifts costs to those who opt out, exacerbating rate disparities.

The pace of technological adoption also complicates rate calculations. Gene therapies, for example, offer cures for previously untreatable diseases but come with staggering price tags—Zolgensma, a treatment for spinal muscular atrophy, costs $2.1 million per dose. Insurers must decide whether to cover such treatments, knowing they could bankrupt smaller plans or force premiums up for all members. A single high-cost claim can increase a group plan’s rates by 5-10% the following year, creating a ripple effect across the market.

To mitigate these challenges, insurers are experimenting with value-based care models tied to technology use. For instance, bundled payments for joint replacements incentivize hospitals to adopt cost-effective technologies like navigation systems, which reduce surgical errors by 60%. Similarly, telemedicine platforms, which cost providers $50-$150 per session to implement, have cut unnecessary office visits by 30%, lowering administrative costs for insurers. Such strategies demonstrate how technology, when paired with innovative payment models, can stabilize rates without sacrificing quality.

Ultimately, the relationship between medical technology and insurance rates hinges on alignment between innovation and affordability. Policymakers, providers, and insurers must collaborate to ensure that advancements like AI diagnostics or 3D-printed organs benefit all patients, not just those with premium plans. Until then, consumers should scrutinize their policies for coverage of emerging technologies and advocate for transparency in how these costs are distributed. After all, the future of healthcare isn’t just about what’s possible—it’s about what’s accessible.

Understanding Pre-Existing Conditions and Health Insurance Coverage

You may want to see also

Frequently asked questions

Yes, health insurance rates are expected to rise in the coming year due to factors like inflation, increased healthcare costs, and rising prescription drug prices.

The primary reasons include higher medical care costs, aging populations, advancements in medical technology, and increased demand for healthcare services.

No, premium increases vary based on factors like location, plan type, age, and changes in state or federal regulations.

Yes, you can shop around for more affordable plans, consider high-deductible health plans with Health Savings Accounts (HSAs), or explore employer-sponsored wellness programs to reduce costs.

Government policies, such as changes to the Affordable Care Act (ACA) or Medicaid, can influence rates by altering subsidies, mandates, or coverage requirements, either increasing or decreasing costs for consumers.