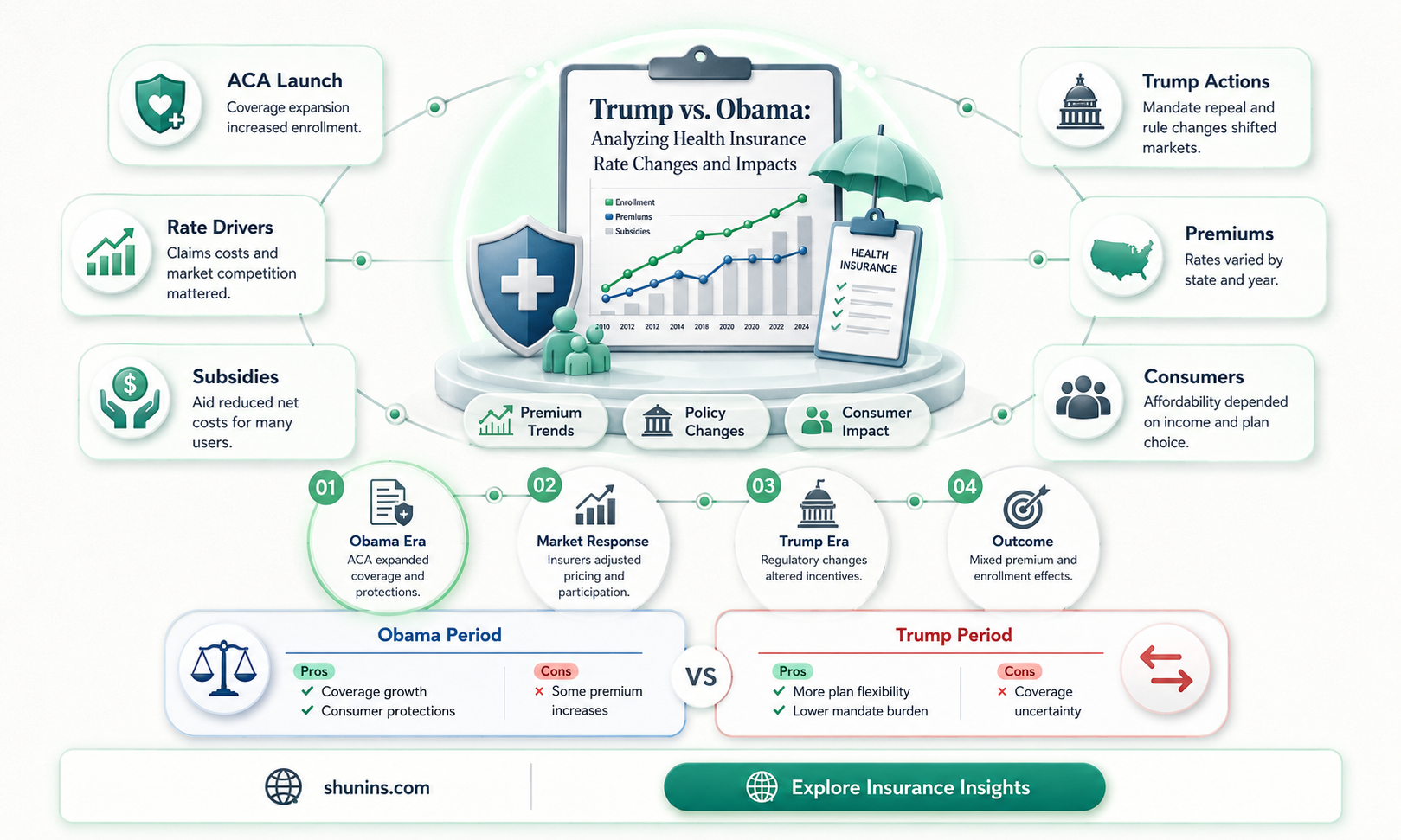

The question of whether health insurance rates are higher under Trump than Obama is a complex and contentious issue, shaped by policy changes, market dynamics, and political rhetoric. During the Obama administration, the Affordable Care Act (ACA) aimed to expand coverage and regulate premiums, though rates fluctuated due to factors like insurer participation and healthcare costs. Under Trump, efforts to repeal the ACA, reduce subsidies, and implement policies like short-term health plans were criticized for destabilizing markets and potentially increasing costs for some consumers. While premium trends varied by state and plan type, data suggests that average ACA marketplace premiums initially rose sharply in Trump’s early years before stabilizing, partly due to insurers adjusting to policy uncertainty. Ultimately, comparing the two administrations requires considering both legislative actions and broader economic and healthcare trends.

Explore related products

What You'll Learn

![]()

ACA vs Trump policies impact

The Affordable Care Act (ACA), often referred to as Obamacare, and the Trump administration’s policies on healthcare represent fundamentally different approaches to health insurance regulation, each with distinct impacts on premiums and coverage. Under the ACA, implemented during the Obama administration, several key provisions aimed to stabilize insurance markets and expand access. These included the individual mandate, which required most Americans to have health insurance or pay a penalty, and the establishment of health insurance marketplaces offering subsidized plans. These measures helped reduce the uninsured rate but also led to initial premium increases as insurers adjusted to new regulations and a sicker risk pool.

In contrast, the Trump administration sought to dismantle or weaken many ACA provisions, arguing they were overly burdensome and contributed to rising costs. One of the most significant changes was the elimination of the individual mandate penalty in 2019, which removed the financial incentive for healthy individuals to enroll in insurance. This shift, combined with efforts to expand short-term and association health plans (which often excluded pre-existing conditions and offered limited benefits), disrupted the ACA’s risk pool. While these changes initially lowered premiums for some, they also led to higher rates for those relying on ACA-compliant plans, as the pool became less healthy and more expensive to insure.

To illustrate the impact, consider the following example: In 2017, the average premium for a benchmark ACA plan increased by 37% due to market uncertainty caused by Trump’s policies. However, by 2020, premiums began to stabilize as insurers adapted to the new landscape and federal subsidies were expanded under the Biden administration. This volatility highlights the delicate balance between access and affordability, with Trump’s policies often prioritizing deregulation over market stability.

A critical takeaway is that while Trump’s policies may have offered short-term relief for some, they exacerbated long-term challenges for the ACA’s individual market. For instance, the expansion of short-term plans, which can last up to 36 months under Trump’s rules, attracted healthier individuals but left those with pre-existing conditions facing higher premiums in ACA-compliant plans. This segmentation of the market underscores the trade-offs between flexibility and comprehensive coverage.

Practical advice for consumers navigating these changes includes carefully reviewing plan details, as short-term and association plans may exclude essential health benefits like maternity care or prescription drugs. Additionally, individuals with pre-existing conditions should prioritize ACA-compliant plans, even if premiums are higher, to ensure comprehensive coverage. Finally, staying informed about policy changes and subsidy eligibility can help mitigate the financial impact of fluctuating premiums. The ACA vs. Trump policies debate ultimately reveals the complexities of balancing affordability, access, and regulation in the U.S. healthcare system.

Medical Insurance in LA: Signing Up Simplified

You may want to see also

Explore related products

$15

![]()

Premium changes 2016-2020 analysis

Health insurance premiums experienced notable fluctuations between 2016 and 2020, a period marked by significant policy shifts under the Obama and Trump administrations. Data from the Kaiser Family Foundation reveals that average premiums for benchmark Affordable Care Act (ACA) plans increased by 25% from 2016 to 2017, a trend often attributed to market uncertainty and insurer exits. However, this spike was followed by more modest increases in subsequent years, with premiums rising by an average of 4% in 2018 and 0% in 2019. This stabilization suggests that initial volatility was partly a response to policy changes rather than a sustained upward trajectory.

To understand these changes, consider the policy actions taken during this period. The Trump administration’s decision to eliminate the individual mandate penalty in 2019 and reduce funding for ACA outreach likely contributed to higher premiums in the short term, as healthier individuals opted out of coverage, leaving a sicker risk pool. Conversely, the expansion of short-term health plans and association health plans introduced more affordable but less comprehensive options, which may have alleviated premium growth for some consumers. These actions highlight the complex interplay between regulatory changes and market dynamics.

A comparative analysis of premium trends across states provides further insight. States that embraced ACA policies, such as California and New York, saw slower premium growth due to stronger risk pools and reinsurance programs. In contrast, states like Georgia and Florida, which did not expand Medicaid and had fewer insurer options, experienced higher premium increases. This disparity underscores the importance of state-level policies in mitigating federal-level changes. For example, in 2018, California’s premiums rose by only 3.2%, while Florida’s increased by 8.4%, illustrating the impact of localized strategies.

For consumers navigating these changes, practical steps can help manage costs. First, annually review plan options during open enrollment, as premiums and subsidies fluctuate. Second, consider short-term plans if you’re healthy and need temporary coverage, but be aware of their limited benefits. Third, leverage state-based marketplaces, which often offer additional subsidies or reinsurance programs. For instance, a 40-year-old earning $40,000 annually in California could save up to $200 monthly through state-specific subsidies compared to federal marketplace rates.

In conclusion, the 2016–2020 premium changes reflect a mix of federal policy shifts, state-level interventions, and market responses. While initial increases were steep, stabilization followed as insurers adapted to new regulations. Consumers can mitigate costs by staying informed and exploring all available options, emphasizing the need for proactive decision-making in a dynamic health insurance landscape.

Checking Medical Insurance in Saudi Arabia: A Step-by-Step Guide

You may want to see also

Explore related products

![A comparison of the costs of major national health insurance proposals by Gordon R. Trapnell Consulting Actuaries. 1976 [Leather Bound]](https://m.media-amazon.com/images/I/81nNKsF6dYL._AC_UY218_.jpg)

![]()

Subsidy adjustments under both administrations

Subsidy adjustments under the Obama and Trump administrations played a pivotal role in shaping health insurance affordability for millions of Americans. The Affordable Care Act (ACA), signed into law by President Obama, introduced premium tax credits to offset the cost of marketplace plans for individuals and families earning between 100% and 400% of the federal poverty level (FPL). These subsidies were designed to cap premiums at a percentage of income, ensuring that coverage remained affordable for lower- and middle-income households. For example, a family of four earning $50,000 annually (approximately 200% FPL) could limit their premium contribution to around 6.3% of their income, significantly reducing out-of-pocket costs.

Under the Trump administration, subsidy adjustments were less about expanding access and more about reevaluating the structure of financial assistance. While the ACA’s subsidy framework remained largely intact due to its statutory protections, the Trump administration introduced changes that indirectly affected subsidy eligibility and amounts. For instance, the decision to shorten the open enrollment period and reduce funding for outreach and advertising led to fewer individuals signing up for marketplace plans. This decline in enrollment skewed the risk pool toward sicker, costlier enrollees, prompting insurers to raise premiums. As a result, while subsidy amounts increased to keep pace with rising premiums, the overall affordability of coverage became less predictable for many consumers.

One critical difference in subsidy adjustments between the two administrations was their approach to cost-sharing reductions (CSRs). The Obama administration implemented CSRs to lower out-of-pocket costs like deductibles and copayments for individuals earning up to 250% FPL. However, the Trump administration discontinued federal funding for CSRs in 2017, forcing insurers to absorb these costs or pass them on to consumers. Many insurers responded by increasing silver-tier plan premiums, which triggered a paradoxical outcome: higher subsidies for those eligible, as premium tax credits are tied to the cost of the second-lowest silver plan. This adjustment effectively shielded subsidy recipients from premium hikes but left unsubsidized enrollees facing steep rate increases.

Practical takeaways for consumers navigating these subsidy adjustments include understanding how income fluctuations impact eligibility and staying informed about annual changes to subsidy calculations. For example, a household earning just above 400% FPL might find itself ineligible for subsidies, facing the full brunt of premium increases. Conversely, individuals nearing retirement or experiencing income reductions should reassess their subsidy eligibility annually, as even small changes in income can qualify them for financial assistance. Utilizing tools like the Healthcare.gov subsidy calculator can help estimate potential savings and ensure enrollment in the most cost-effective plan.

In conclusion, subsidy adjustments under both administrations reflect differing priorities: the Obama administration focused on expanding access and affordability through robust financial assistance, while the Trump administration’s changes, though less direct, had significant implications for the stability and predictability of health insurance costs. For consumers, understanding these nuances is essential to maximizing the benefits of available subsidies and mitigating the impact of premium fluctuations.

Florida Insurance Crisis: Why Companies Are Dropping Customers

You may want to see also

Explore related products

![]()

Market stability comparisons pre/post 2017

The Affordable Care Act (ACA), implemented under the Obama administration, aimed to stabilize health insurance markets by expanding coverage and regulating premiums. Pre-2017, the individual market saw initial volatility as insurers adjusted to new rules, but by 2016, markets in many states had begun to stabilize. Premiums increased significantly in 2017, but this trend was largely a continuation of adjustments insurers made under Obama-era policies, not a direct result of Trump’s actions. For example, benchmark silver plan premiums rose by an average of 25% in 2017, but this increase was attributed to insurers accounting for the uncertainty of cost-sharing reduction (CSR) payments, which the Trump administration later discontinued.

Post-2017, the Trump administration’s policies introduced new uncertainties that impacted market stability. The elimination of the individual mandate penalty in 2019, for instance, was projected to reduce enrollment by 4.3 million individuals by 2020, according to the Congressional Budget Office. This change, combined with the expansion of short-term health plans and association health plans, fragmented the risk pool, leading to higher premiums for ACA-compliant plans. In 2018, average premiums for benchmark silver plans increased by 32%, reflecting insurers’ responses to policy changes and market uncertainty.

A comparative analysis reveals that while premium increases were steep in 2017, they began to moderate in subsequent years. By 2019, premium increases slowed to an average of 0.2% for benchmark plans, as insurers adapted to the new regulatory environment. However, this stability came at a cost: reduced enrollment and a shift toward less comprehensive coverage options. For example, short-term plans, which are exempt from ACA regulations, saw enrollment grow from 182,000 in 2016 to 805,000 in 2019, according to the Kaiser Family Foundation.

To navigate these changes, consumers should focus on understanding their coverage options. For those under age 30 or with short-term health needs, short-term plans may offer lower premiums but lack essential health benefits. Families and individuals with pre-existing conditions should prioritize ACA-compliant plans, which guarantee coverage regardless of health status. Practical tips include using premium tax credits, available to those earning up to 400% of the federal poverty level, to offset costs. Additionally, enrolling during the annual open enrollment period ensures access to comprehensive coverage without facing penalties or coverage gaps.

In conclusion, market stability pre- and post-2017 reflects a complex interplay of policy changes and insurer adjustments. While premiums initially surged under both administrations, the Trump-era policies introduced new challenges, including reduced enrollment and increased reliance on non-ACA plans. Consumers must remain informed and proactive in selecting coverage that balances cost and comprehensiveness, leveraging available subsidies to mitigate financial burdens.

Indemnity Plans: Major Medical Insurance or Not?

You may want to see also

Explore related products

![]()

State-level rate trend variations

Health insurance rate trends under the Trump and Obama administrations varied significantly across states, influenced by factors like state policies, market dynamics, and regulatory environments. For instance, states that expanded Medicaid under the Affordable Care Act (ACA) during Obama’s tenure generally saw lower uninsured rates and more stable premiums, as the expansion reduced the number of high-risk individuals in the individual market. In contrast, states that opted out of Medicaid expansion often experienced higher premiums, as insurers faced a sicker risk pool. Under Trump, efforts to dismantle the ACA, such as eliminating the individual mandate penalty, led to increased uncertainty in some states, causing insurers to raise rates to account for potential market instability.

Consider the case of California versus Texas. California, a state that embraced ACA provisions and established a robust state-run marketplace, saw relatively modest premium increases during both administrations. In 2018, for example, California’s premiums rose by an average of 8.7%, but this was offset by state-funded subsidies that kept costs manageable for many residents. Texas, which did not expand Medicaid and has a less regulated market, experienced steeper premium hikes. In 2017, some Texas counties saw rate increases of over 30%, as insurers struggled with higher medical costs and reduced federal support. These examples illustrate how state-level decisions amplified or mitigated national trends.

Analyzing these variations requires examining state-specific policies and their interaction with federal changes. States with reinsurance programs, like Alaska and Minnesota, successfully lowered premiums by compensating insurers for high-cost claims, regardless of the federal administration. For example, Alaska’s reinsurance program reduced premiums by 20% in 2018, shielding consumers from broader market volatility. Conversely, states without such programs often faced double-digit premium increases, particularly after Trump’s policy shifts reduced federal funding for cost-sharing reductions (CSRs). This highlights the importance of state-level interventions in shaping rate trends.

Practical takeaways for consumers include researching state-specific programs and subsidies, as these can significantly offset premium increases. For example, in New Jersey, residents can access state-funded subsidies that lower costs for households earning up to 400% of the federal poverty level. Additionally, understanding the role of Medicaid expansion is crucial; in expansion states, individuals with incomes up to 138% of the poverty level may qualify for Medicaid, avoiding the individual market altogether. By focusing on state-level initiatives, consumers can navigate rate variations more effectively, regardless of broader federal policies.

In conclusion, state-level rate trend variations under Trump and Obama were driven by a combination of federal policy changes and state-specific actions. While national trends provide a broad framework, the real impact on premiums was often determined by how states responded to ACA provisions, Medicaid expansion, and market stabilization efforts. Consumers and policymakers alike must consider these nuances to understand why health insurance rates diverged so sharply across states during these administrations.

Medical Insurance and PrEP: What's Covered?

You may want to see also

Frequently asked questions

Health insurance rates generally increased under both Trump and Obama, but the rate of increase varied. Under Obama, premiums rose significantly in the early years of the Affordable Care Act (ACA), while under Trump, premiums continued to rise but at a slower pace due to factors like policy changes and market stabilization efforts.

Trump’s policies, such as eliminating the individual mandate penalty and expanding short-term health plans, were criticized for potentially destabilizing the ACA marketplace. However, other factors like rising healthcare costs and reduced insurer participation also contributed to rate increases.

Health insurance rates were not consistently lower under Obama. While the ACA expanded coverage, premiums spiked in some years, particularly in 2017, before Trump’s policies took full effect. Rates under Trump continued to rise but at a slower rate in later years.

Trump’s repeal of the individual mandate penalty in 2019 was expected to lead to higher premiums by reducing the number of healthy enrollees in the marketplace. However, the impact was mitigated by other factors, including increased federal subsidies and state-level stabilization efforts.

The ACA initially led to premium increases as insurers adjusted to new regulations and expanded coverage. Over time, rates stabilized, but they remained higher than pre-ACA levels. Trump’s changes to the ACA did not reverse this trend, and premiums continued to rise, albeit at a slower pace in some years.