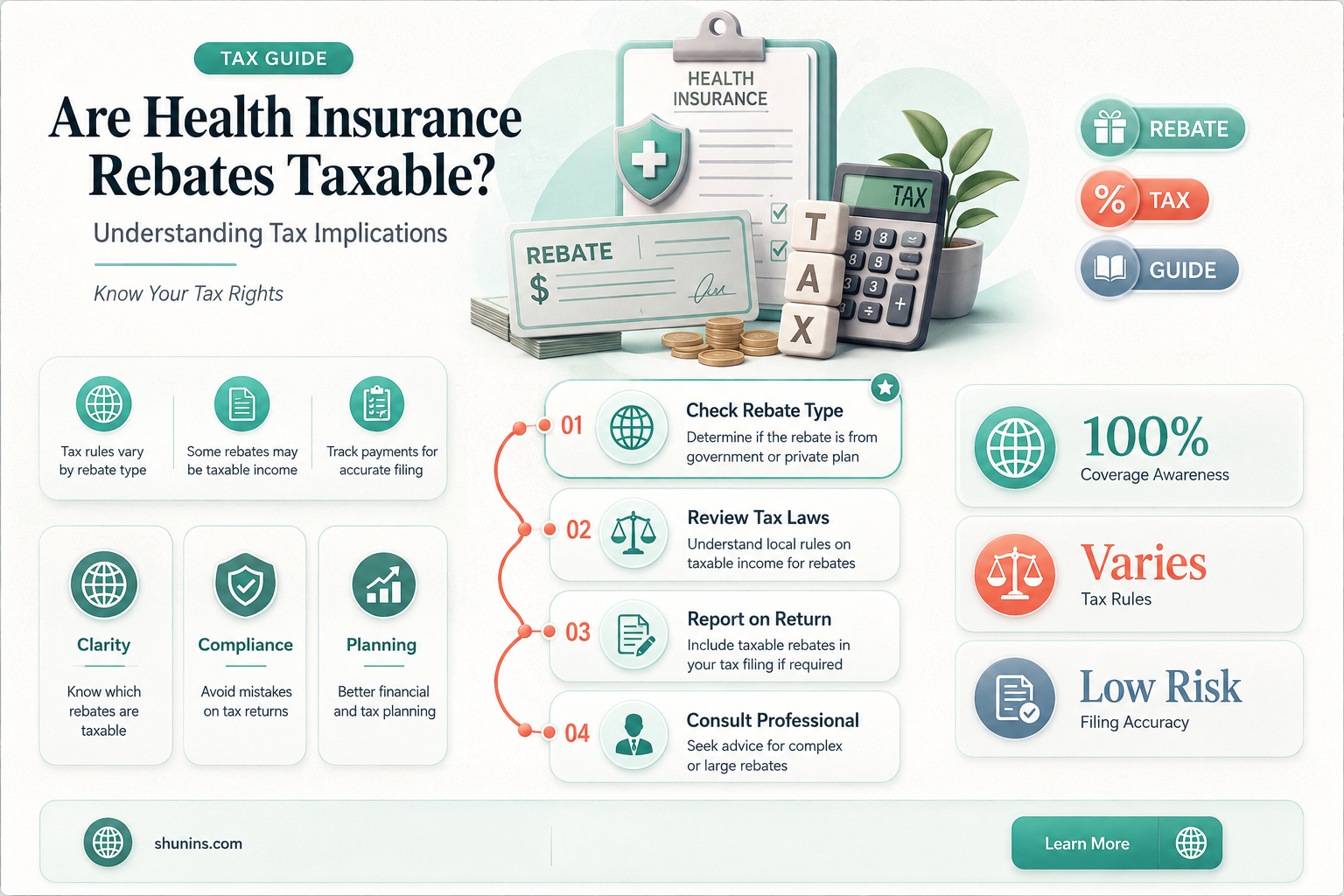

Health insurance rebates, which are often issued by insurance companies as a refund of premiums paid, can raise questions about their tax implications. Many individuals wonder whether these rebates are considered taxable income and how they should be reported to the IRS. The answer depends on various factors, including the type of health insurance plan, the reason for the rebate, and the tax laws in your jurisdiction. Generally, rebates related to employer-sponsored health insurance plans may be tax-free, while those from individual policies could be subject to taxation. Understanding the specific circumstances surrounding the rebate is crucial to determining its tax treatment and ensuring compliance with tax regulations.

| Characteristics | Values |

|---|---|

| Taxability of Health Insurance Rebates | Generally, health insurance rebates are not taxable in the United States. They are considered a reduction in premiums rather than taxable income. |

| Type of Rebate | Rebates issued under the Affordable Care Act (ACA) or by insurance companies as premium adjustments are typically tax-free. |

| IRS Guidance | The IRS treats health insurance rebates as nontaxable because they are not considered income but rather a return of premiums paid. |

| State-Specific Rules | Some states may have different rules, but federal tax guidelines generally apply. Check state-specific tax laws for variations. |

| Reporting Requirements | Health insurance rebates do not need to be reported on federal tax returns as income. |

| Exceptions | If a rebate is received for a policy paid with pre-tax dollars (e.g., through a Flexible Spending Account or Health Savings Account), it may have different tax implications. |

| ACA Premium Tax Credits | Advance Premium Tax Credits (APTC) are reconciled on tax returns, but rebates from insurance companies are separate and not taxable. |

| Employer-Sponsored Plans | Rebates for employer-sponsored health plans are generally not taxable for employees, as they are treated as a reduction in premiums. |

| Timing of Rebate | Whether the rebate is received in the same tax year or later does not affect its taxability; it remains nontaxable. |

| Documentation | Keep documentation of rebates received for record-keeping, though they do not need to be reported on tax returns. |

Explore related products

What You'll Learn

![]()

Federal Tax Treatment of Rebates

Health insurance rebates, often issued by insurers to policyholders, can be a financial boon, but their tax implications are not always clear. Under federal tax law, the treatment of these rebates hinges on their classification: are they a reduction in premiums or a reimbursement of expenses? This distinction is crucial because it determines whether the rebate is taxable as income or excluded from taxation. For instance, rebates issued under the Affordable Care Act’s Medical Loss Ratio (MLR) provision are generally considered a return of premium payments, making them nontaxable for most individuals. However, rebates tied to specific claims or services may be treated differently, particularly if they resemble reimbursements for deductible medical expenses.

To navigate this complexity, consider the source and purpose of the rebate. If the rebate is issued because an insurer failed to meet the MLR threshold—spending less than 80-85% of premiums on healthcare—it is typically treated as a refund of premiums. Since premiums are usually paid with after-tax dollars, the rebate is not taxable. For example, if a family paid $12,000 in annual premiums and received a $300 rebate, they would not owe taxes on that $300. However, if the rebate is tied to a specific claim or service, such as a reimbursement for overpaid copays, it may need to be reported as income unless it qualifies as a medical expense reimbursement under Section 105 of the Internal Revenue Code.

Practical steps can help policyholders avoid tax surprises. First, review the insurer’s explanation of the rebate, which often clarifies its purpose. If unclear, contact the insurer directly for documentation. Second, consult IRS Publication 502, which outlines the tax treatment of medical expenses, and Form 1099-R, which may be issued if the rebate is taxable. For those using Health Savings Accounts (HSAs), rebates related to HSA-qualified plans may have additional considerations, as they could affect contribution limits or deductions. Finally, consider consulting a tax professional, especially if the rebate amount is substantial or if you’re unsure of its classification.

A comparative analysis highlights the contrast between federal and state tax treatments. While federal law generally excludes MLR rebates from taxation, some states may tax them as income or subject them to different rules. For example, California treats MLR rebates as nontaxable, aligning with federal guidelines, but other states may vary. This discrepancy underscores the importance of checking state-specific regulations. Additionally, employer-sponsored plans may handle rebates differently, with some employers distributing them directly to employees or applying them to future premiums, further complicating tax implications.

In conclusion, understanding the federal tax treatment of health insurance rebates requires a nuanced approach. By focusing on the rebate’s source, purpose, and classification, individuals can determine whether it is taxable or excluded from income. Proactive steps, such as reviewing documentation and consulting resources, can prevent unexpected tax liabilities. While federal guidelines provide a framework, state laws and employer policies may introduce additional layers of complexity, making it essential to stay informed and seek professional advice when needed.

Conservative Health Insurance Providers: A Guide to Traditional Coverage Options

You may want to see also

Explore related products

![]()

State-Specific Tax Rules for Rebates

Health insurance rebates, often issued by insurers to policyholders, can be a financial boon, but their tax implications vary widely across states. While federal guidelines provide a baseline, state-specific tax rules introduce layers of complexity that demand attention. For instance, California treats health insurance rebates as nontaxable income if they are directly related to premium overpayments, whereas New York considers them taxable unless explicitly excluded by state law. Understanding these nuances is crucial for accurate tax reporting and financial planning.

Consider the example of a family in Texas receiving a $500 rebate from their health insurer. Texas, which does not impose a state income tax, exempts this rebate from taxation entirely. In contrast, a similar rebate in Massachusetts, a state with its own income tax, may be subject to state taxes unless it qualifies under specific exemptions, such as those tied to Affordable Care Act (ACA) compliance. This disparity highlights the importance of consulting state tax codes or a tax professional to avoid unexpected liabilities.

For those navigating state-specific rules, a proactive approach is essential. Start by identifying whether your state classifies health insurance rebates as taxable income. States like Pennsylvania and Ohio generally follow federal guidelines, treating rebates as nontaxable if they are returned premiums. However, states like Minnesota and Wisconsin may tax rebates unless they meet certain criteria, such as being issued under a state-regulated program. Reviewing your state’s Department of Revenue website or tax publications can provide clarity.

Practical tips can further simplify compliance. Keep detailed records of all rebates received, including the insurer’s explanation of the rebate’s purpose. For example, if a rebate is labeled as a "premium refund" rather than a "discount," it may be more likely to be nontaxable in some states. Additionally, consider timing: if a rebate is issued in a different tax year than the premiums were paid, state rules may differ on how to report it. For instance, Illinois allows taxpayers to adjust their income in the year the rebate is received, while other states may require reporting in the year the premiums were overpaid.

In conclusion, state-specific tax rules for health insurance rebates are a patchwork of regulations that require careful navigation. By understanding your state’s stance, maintaining thorough records, and staying informed about exemptions, you can ensure compliance and maximize the financial benefit of these rebates. Whether you’re in a no-income-tax state like Florida or a high-tax state like Oregon, the key is to treat each rebate as a unique case, guided by local laws and expert advice.

Top Homeowner Insurance Companies for Efficient and Fair Claims Handling

You may want to see also

Explore related products

![TurboTax Desktop Deluxe 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71uOJaU7UvL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UL320_.jpg)

![]()

Rebates vs. Premium Reductions

Health insurance rebates and premium reductions serve similar purposes—lowering out-of-pocket costs—but their tax implications and mechanisms differ significantly. Rebates are typically refunds issued after a policy period, often tied to overpaid premiums or insurer profits exceeding regulatory limits. Premium reductions, on the other hand, lower the cost of coverage upfront, directly reducing the amount policyholders pay each month. Understanding these distinctions is crucial for navigating their tax treatment and financial impact.

Consider a scenario where a family of four receives a $500 rebate from their health insurer due to lower-than-expected medical claims in their plan’s pool. This rebate, classified as a reduction in premium costs, is generally not taxable under IRS guidelines. However, if the rebate is tied to a government subsidy or advance premium tax credit (APTC), the rules shift. For instance, if the family’s income fluctuates mid-year, triggering an APTC reconciliation, the rebate might offset overclaimed credits, effectively becoming a tax adjustment rather than taxable income.

Premium reductions, such as those offered through employer-sponsored plans or marketplace subsidies, operate differently. For example, a 35-year-old individual earning $40,000 annually might qualify for a $200 monthly premium reduction through the Affordable Care Act’s cost-sharing reductions. This reduction is applied directly to their premium, lowering their monthly payment from $400 to $200. Unlike rebates, these reductions are not taxable because they are considered part of the premium structure, not a refund or additional income.

A key takeaway is that rebates and premium reductions are treated distinctly for tax purposes. Rebates are generally tax-free unless tied to government subsidies, while premium reductions are inherently non-taxable. Policyholders should review their insurer’s documentation to determine the source of any rebate—whether from overpaid premiums, insurer profits, or government programs—to ensure accurate tax reporting. For instance, a rebate issued under the Medical Loss Ratio (MLR) provision of the ACA is typically tax-free, whereas a rebate tied to an APTC reconciliation may require adjustments on Form 8962.

Practical tips include monitoring income changes throughout the year to avoid overclaiming subsidies, which can complicate rebate taxability. Additionally, individuals should retain all insurer communications regarding rebates and premium reductions for tax filing purposes. For those aged 65 and older or with complex financial situations, consulting a tax professional can clarify how these benefits interact with Medicare premiums or other deductions. By distinguishing between rebates and premium reductions, policyholders can maximize savings while staying compliant with tax laws.

Private Medical Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![TurboTax Desktop Premier 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71RgxnEm-tL._AC_UL320_.jpg)

![TurboTax Desktop Home & Business 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71KOcfYElCL._AC_UL320_.jpg)

![H&R Block Tax Software Premium 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51dMIAMHkkL._AC_UL320_.jpg)

![]()

Taxable Income Classification for Rebates

Health insurance rebates often blur the lines between taxable and nontaxable income, leaving policyholders uncertain about their financial obligations. The classification hinges on whether the rebate is considered a reduction in premium costs or a reimbursement of expenses. Generally, if a rebate is treated as an advance premium tax credit—a common scenario under the Affordable Care Act—it may not be taxable if properly reconciled on your tax return. However, if the rebate is viewed as a refund of previously deducted medical expenses, it could become taxable income, as it effectively reduces your prior deductions. Understanding this distinction is crucial for accurate tax reporting.

To navigate this complexity, consider the source and purpose of the rebate. For instance, employer-sponsored health insurance rebates are typically nontaxable if they are returned to the employer, who then uses them to offset future premiums. However, if the rebate is distributed directly to the employee, it may be classified as taxable wages. Similarly, rebates from individual health plans often depend on whether they are tied to premium adjustments or specific claims. A rebate for overpaid premiums usually remains nontaxable, while a reimbursement for out-of-pocket expenses might require tax reporting, especially if those expenses were previously deducted.

Practical steps can help clarify your situation. First, review the documentation provided by your insurer or employer, which often specifies whether the rebate is taxable. Second, consult IRS guidelines, particularly Publication 502 and Form 8885, for detailed instructions on reporting health insurance-related income. If you’re unsure, seek advice from a tax professional who can analyze your specific circumstances. For example, a family receiving a $500 rebate from their marketplace plan should verify if it was an advance premium tax credit, which would require reconciliation on Form 8962, or a separate refund, which might have different tax implications.

A comparative analysis reveals inconsistencies across jurisdictions. While federal tax rules generally govern health insurance rebates, state laws can introduce variations. For instance, some states exempt all health insurance rebates from taxation, while others align with federal guidelines. This disparity underscores the importance of checking local regulations. Additionally, international examples, such as Australia’s private health insurance rebate, are nontaxable but subject to income testing, highlighting how different systems handle similar issues. Such comparisons emphasize the need for context-specific understanding.

In conclusion, classifying health insurance rebates as taxable or nontaxable income requires a nuanced approach. By examining the rebate’s origin, purpose, and applicable laws, individuals can avoid costly mistakes. Proactive steps, such as reviewing documentation and consulting resources, ensure compliance and financial clarity. While the rules may seem intricate, a methodical evaluation can demystify this aspect of tax planning, ultimately saving time and reducing stress during tax season.

Dual Medical Insurance: Maximizing Your Coverage Benefits

You may want to see also

Explore related products

![TurboTax Desktop Deluxe 2025, Federal Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71zRbfw0RdL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51Mlng5FWYL._AC_UL320_.jpg)

![]()

Reporting Rebates on Tax Returns

Health insurance rebates can significantly reduce your out-of-pocket costs, but their tax implications often leave policyholders puzzled. When reporting rebates on your tax returns, the key is understanding whether the rebate is considered taxable income. Generally, rebates from health insurance premiums are not taxable if they are treated as a reduction in premiums rather than a reimbursement of expenses. However, if the rebate is tied to a specific claim or expense, it may need to be reported differently. This distinction is crucial because misreporting can lead to penalties or audits.

To report rebates accurately, start by identifying the nature of the rebate. If it’s a premium rebate issued by your insurer as part of a rate adjustment or overpayment, it’s typically not taxable. For example, if your insurer refunds $300 due to overestimated premiums, this amount doesn’t need to be included in your taxable income. However, if the rebate is a reimbursement for a specific medical expense you’ve already deducted on your taxes, you must adjust your deductions accordingly. Failing to do so could result in double-dipping, which is a red flag for the IRS.

The process of reporting taxable rebates involves careful documentation and calculation. If the rebate is taxable, it should be included in your gross income on Form 1040. For instance, if you received a $500 rebate for a medical expense you previously deducted, add this amount to your income to offset the earlier deduction. Keep detailed records of all rebates, including the insurer’s explanation of the rebate type, to support your reporting. This documentation is essential if the IRS requests verification.

One common mistake is assuming all rebates are tax-free. For example, rebates from Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs) may have different rules. HSA rebates are generally tax-free if used for qualified medical expenses, but FSA rebates could be taxable if not properly accounted for. Always consult the IRS guidelines or a tax professional if you’re unsure about the rebate’s classification. Proactive clarity can save you from complications during tax season.

In conclusion, reporting health insurance rebates on your tax returns requires a clear understanding of the rebate’s purpose and source. Non-taxable rebates, like premium adjustments, simplify the process, but taxable rebates demand meticulous attention to avoid errors. By distinguishing between types of rebates and maintaining thorough records, you can navigate this aspect of tax reporting with confidence. Remember, when in doubt, seek guidance to ensure compliance and peace of mind.

Understanding Your Medical Insurance Group

You may want to see also

Frequently asked questions

Health insurance rebates are generally not considered taxable income because they are treated as a reduction in premiums rather than income received.

Typically, health insurance rebates do not need to be reported on your tax return since they are not taxable income. However, consult a tax professional for specific situations.

A health insurance rebate may reduce the amount of premiums you claim for tax credits or deductions, as it lowers your actual premium expense. Always verify with the IRS guidelines or a tax advisor.

![H&R Block Tax Software Premium & Business 2025 Win [PC Online code]](https://m.media-amazon.com/images/I/618kxmZlTGL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![TurboTax Desktop Business 2025, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71UL+5xLOeL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UL320_.jpg)

![(Old Version) H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)