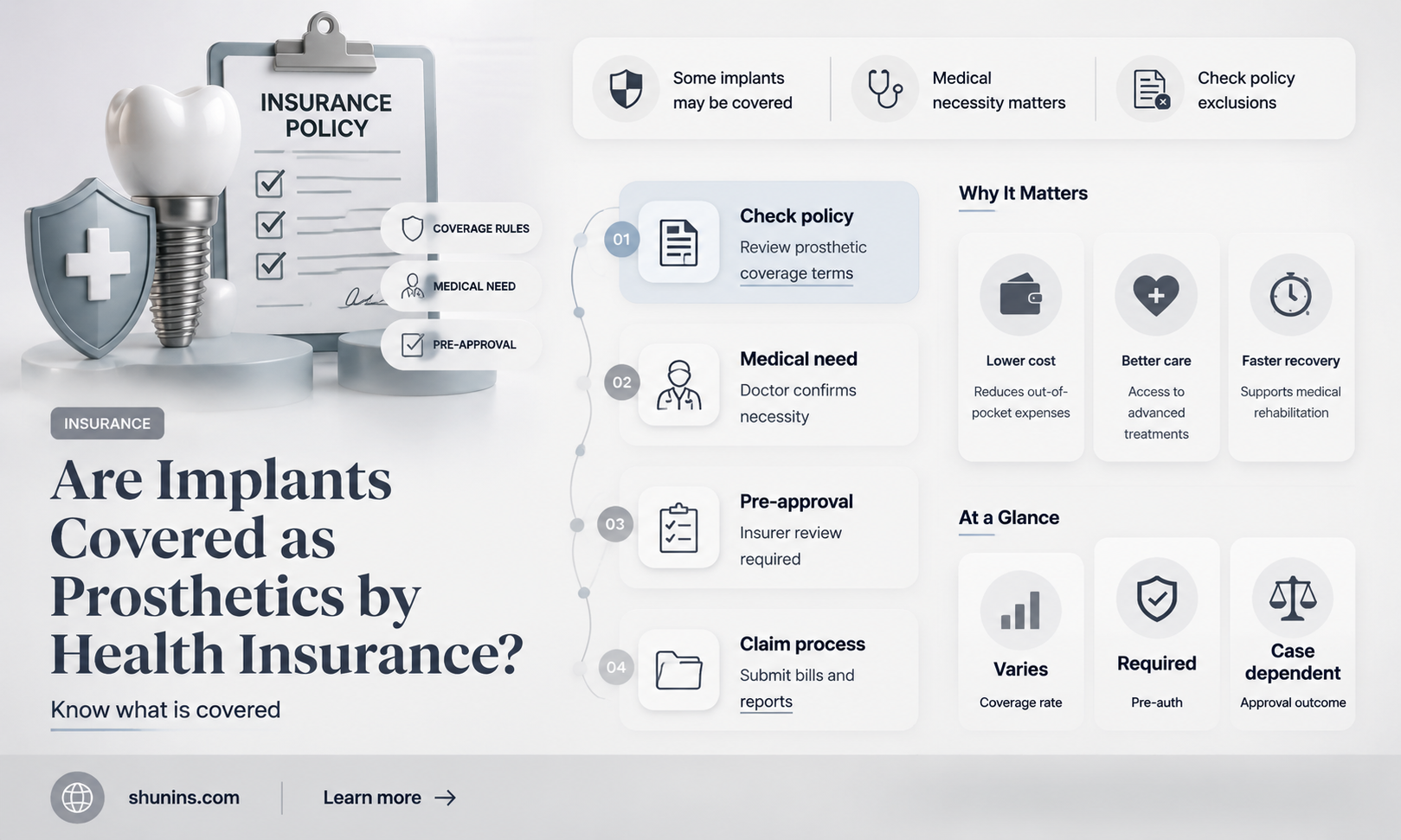

The classification of implants as a prosthesis under health insurance is a critical topic for individuals seeking coverage for medical devices that replace or support bodily functions. Implants, such as dental, joint, or cochlear implants, often blur the line between cosmetic enhancements and medically necessary prosthetics, leading to varying interpretations by insurance providers. While some policies explicitly categorize implants as prostheses, eligible for coverage under durable medical equipment benefits, others may exclude them based on criteria like permanence or functionality. Understanding these distinctions is essential for patients navigating insurance claims, as it directly impacts out-of-pocket costs and access to life-enhancing treatments. Clear guidelines and advocacy for consistent classification are needed to ensure equitable coverage for those relying on implants to improve their quality of life.

| Characteristics | Values |

|---|---|

| Definition of Prosthesis | A device that replaces a missing body part to restore function or appearance. |

| Implants as Prosthesis | Generally considered a prosthesis if they replace a missing or non-functional body part (e.g., dental, joint, breast implants after mastectomy). |

| Health Insurance Coverage | Coverage varies by policy, insurer, and type of implant. Often covered if deemed medically necessary. |

| Dental Implants | Typically not covered under basic health insurance but may be covered under dental insurance or supplemental plans. |

| Joint Implants (e.g., hip, knee) | Usually covered under health insurance as they are considered medically necessary. |

| Breast Implants | Covered if for reconstructive purposes (e.g., post-mastectomy); cosmetic implants are rarely covered. |

| Cochlear Implants | Often covered under health insurance as they are considered medically necessary for hearing restoration. |

| Policy Exclusions | Cosmetic implants (e.g., breast augmentation for aesthetic reasons) are often excluded from coverage. |

| Pre-Authorization Requirement | Many insurers require pre-authorization to determine medical necessity before covering implant procedures. |

| Out-of-Pocket Costs | Even with coverage, patients may incur out-of-pocket costs like deductibles, copays, or coinsurance. |

| Geographic Variations | Coverage policies may differ by country, state, or region. For example, some countries have universal coverage for certain implants. |

| Private vs. Public Insurance | Private insurance plans may offer more flexibility in coverage compared to public insurance programs. |

| Documentation Needed | Medical documentation proving necessity (e.g., doctor’s recommendation, diagnosis) is often required for approval. |

| Experimental or Investigational Implants | May not be covered if the implant is considered experimental or not FDA-approved. |

| Lifetime Coverage Limits | Some policies may have limits on the number of implants or procedures covered over a lifetime. |

| Appeal Process | If coverage is denied, patients can often appeal the decision with additional medical evidence. |

Explore related products

What You'll Learn

- Implant Definition vs. Prosthesis: Clarifying terminology differences in medical device classification

- Insurance Coverage Criteria: Examining policies for implant inclusion as prosthetics

- Medical Necessity: Assessing if implants meet health insurance necessity standards

- Procedure Coding: How implants are coded for insurance billing purposes

- Policy Exclusions: Identifying common exclusions for implants in health plans

![]()

Implant Definition vs. Prosthesis: Clarifying terminology differences in medical device classification

The distinction between implants and prostheses in medical device classification is nuanced, yet critical for insurance coverage and patient care. Implants, such as dental crowns or pacemakers, are devices placed inside the body to replace or support a biological structure. Prostheses, like artificial limbs or external breast forms, are external devices designed to replace a missing body part. While both aim to restore function or appearance, their classification under health insurance policies often hinges on their placement relative to the body. This distinction can determine coverage eligibility, out-of-pocket costs, and even the type of specialist required for fitting or maintenance.

Analyzing insurance policies reveals a lack of uniformity in how implants and prostheses are categorized. For instance, dental implants are frequently classified as cosmetic rather than prosthetic, leading to limited coverage despite their functional necessity. Conversely, cochlear implants, which are internal devices, are often covered under prosthetic benefits due to their role in restoring sensory function. This inconsistency highlights the need for clearer guidelines in medical device classification. Patients and providers must scrutinize policy language to ensure accurate billing and avoid unexpected expenses, especially when dealing with high-cost devices like joint replacements or insulin pumps.

From a practical standpoint, understanding these classifications empowers patients to advocate for their coverage. For example, a patient requiring a hip implant should verify whether their insurer categorizes it as a prosthetic device or surgical procedure, as this affects pre-authorization requirements and reimbursement rates. Similarly, individuals with mastectomies should confirm if their policy covers both internal reconstructive implants and external prostheses, as some plans separate these into distinct benefit categories. Proactive communication with insurers and healthcare providers can prevent financial surprises and ensure access to necessary care.

Comparatively, the European Union’s Medical Device Regulation (MDR) offers a structured framework for classifying implants and prostheses based on risk and intended use, which could serve as a model for standardizing insurance coverage globally. Under the MDR, a hip implant is classified as a Class III device due to its high-risk profile, whereas an external prosthetic hand might fall under Class IIa. Adopting similar risk-based classifications in insurance policies could reduce ambiguity and improve consistency in coverage decisions. Until such standards are universally adopted, patients must navigate the existing landscape with vigilance and informed persistence.

In conclusion, the terminology differences between implants and prostheses are not merely semantic but have tangible implications for health insurance coverage. By understanding these distinctions, patients can better navigate policy complexities, advocate for their needs, and secure appropriate care. Healthcare providers and insurers, meanwhile, should prioritize clarity in their classifications to ensure equitable access to life-enhancing medical devices. As the field of medical technology advances, so too must the frameworks governing their accessibility and affordability.

Claiming Double: Medical Insurance from Two Companies

You may want to see also

Explore related products

$35.99

![]()

Insurance Coverage Criteria: Examining policies for implant inclusion as prosthetics

Health insurance policies often classify medical devices based on their function and necessity, but the line between what constitutes a prosthesis and what doesn’t can blur when it comes to implants. Dental implants, for instance, are frequently categorized as cosmetic rather than prosthetic, despite restoring essential functions like chewing and speaking. This distinction matters because prosthetics are more likely to be covered under insurance, whereas cosmetic procedures often require out-of-pocket payment. Understanding how insurers define these terms is the first step in navigating coverage for implants.

Insurers typically evaluate implants based on medical necessity, the type of implant, and the policyholder’s specific plan. For example, breast implants following a mastectomy are often covered as reconstructive prosthetics, while those for cosmetic augmentation are not. Similarly, cochlear implants, which restore hearing, are generally included under prosthetic coverage, but bone-anchored hearing aids may face scrutiny. Policies may also require pre-authorization, detailed medical documentation, or proof that less invasive alternatives have been considered. Knowing these criteria can help patients advocate for coverage effectively.

A comparative analysis of policies reveals inconsistencies across providers. Some insurers, like Blue Cross Blue Shield, explicitly include certain implants (e.g., joint replacements) under prosthetic coverage, while others, such as Aetna, may require riders or supplemental plans. Internationally, countries like Canada and the UK often cover implants as prosthetics under public health systems, but private insurers in the U.S. vary widely. Patients should scrutinize their policy’s definitions of "prosthetic devices" and "medically necessary procedures" to identify potential coverage gaps or opportunities.

Practical tips for securing coverage include obtaining a detailed prescription from a specialist, using ICD-10 codes that emphasize functional impairment rather than aesthetics, and appealing denials with evidence of medical necessity. For example, a patient seeking coverage for a dental implant might highlight its role in preventing bone loss or maintaining nutritional intake. Additionally, exploring bundled payment options or financing plans through providers can offset costs when insurance falls short. Proactive engagement with both healthcare providers and insurers is key to maximizing coverage for implants as prosthetics.

Twin City Fire Insurance Company: History, Services, and Coverage Explained

You may want to see also

Explore related products

![]()

Medical Necessity: Assessing if implants meet health insurance necessity standards

Implants, whether dental, orthopedic, or cosmetic, often blur the line between medical necessity and elective enhancement. Health insurance providers typically scrutinize these procedures through a lens of "medical necessity," a term that hinges on whether the implant is deemed essential for restoring function, alleviating pain, or preventing further health deterioration. For instance, a hip implant for a patient with severe osteoarthritis is more likely to be covered than breast implants for purely aesthetic reasons. Understanding this distinction is crucial for patients navigating insurance claims, as it directly impacts out-of-pocket costs and approval likelihood.

Assessing medical necessity for implants involves a multi-step process. First, insurers evaluate the patient’s medical history and current condition to determine if the implant is the only viable solution. For example, a dental implant might be considered necessary if a patient has lost a tooth due to trauma or decay and other options like bridges or dentures are unsuitable. Second, insurers review clinical guidelines and peer-reviewed studies to ensure the procedure aligns with established medical standards. A cochlear implant for a child with profound hearing loss, supported by FDA approvals and clinical trials, would likely meet this criterion.

However, complications arise when implants serve both functional and cosmetic purposes. For instance, breast reconstruction after a mastectomy is often covered, but insurers may dispute coverage if the procedure includes augmentation beyond restoring the original size. Patients must provide detailed documentation, including surgeon recommendations, diagnostic imaging, and evidence of failed conservative treatments, to strengthen their case. Proactive communication with both the healthcare provider and insurer can clarify expectations and reduce the risk of denied claims.

Age and health status also play a role in determining medical necessity. For example, knee implants for elderly patients with advanced arthritis are more likely to be approved than for younger individuals with minor joint issues. Insurers may require patients to exhaust non-surgical options, such as physical therapy or medication, before considering an implant. Additionally, pre-authorization is often mandatory, requiring patients to submit a formal request detailing the procedure’s rationale before scheduling surgery.

In conclusion, proving medical necessity for implants requires a strategic approach. Patients should collaborate closely with their healthcare providers to compile comprehensive medical evidence, adhere to insurer-specific guidelines, and advocate for their needs. While the process can be daunting, understanding the criteria and preparing thoroughly can significantly improve the chances of insurance coverage, ensuring access to life-enhancing treatments without financial burden.

Medicare-for-All: Private Insurance's End?

You may want to see also

Explore related products

![]()

Procedure Coding: How implants are coded for insurance billing purposes

Implants, whether dental, orthopedic, or cosmetic, present unique challenges in procedure coding for insurance billing. The crux of the issue lies in distinguishing between what insurers classify as a prosthesis versus a medically necessary device. For instance, dental implants are often coded using CDT (Code on Dental Procedures and Nomenclature) codes, such as D6000-D6199, which specifically address implant services. However, not all insurers recognize these as covered procedures, frequently categorizing them as cosmetic rather than restorative. This discrepancy underscores the importance of precise coding to maximize reimbursement potential.

Analyzing the coding process reveals a layered approach. Orthopedic implants, like hip or knee replacements, typically fall under CPT (Current Procedural Terminology) codes, such as 27130 for total hip arthroplasty. These codes are more likely to be covered under health insurance because they address functional restoration. In contrast, breast implants post-mastectomy are coded using CPT codes like 19300-19399, often covered under reconstructive surgery benefits. The key takeaway here is that the same type of implant can be coded differently based on its purpose—reconstructive versus cosmetic—and insurers scrutinize these distinctions closely.

A critical caution in procedure coding is avoiding bundling errors. For example, the placement of a dental implant (coded as D6000) and the abutment (D6056) are separate procedures and should be billed individually. Bundling them could result in denied claims or reduced payments. Similarly, for orthopedic implants, the surgery (e.g., 27130) and post-operative care (e.g., 99024 for additional supplies) must be coded distinctly. Understanding these nuances ensures accurate billing and minimizes the risk of audits or rejections.

Practical tips for providers include verifying insurer-specific policies before coding. For instance, some plans cover dental implants only if they replace teeth lost due to trauma or disease, not for elective reasons. Additionally, using modifiers like -51 (multiple procedures) or -RT/-LT (right/left side) can clarify the extent of the service. Documentation is equally vital; detailed operative notes linking the implant to a diagnosed condition (e.g., severe osteoarthritis for a knee replacement) can justify medical necessity and support the chosen codes.

In conclusion, procedure coding for implants demands precision, awareness of insurer policies, and strategic documentation. By mastering these elements, providers can navigate the complexities of billing, ensuring both compliance and optimal reimbursement. Whether coding for dental, orthopedic, or reconstructive implants, the goal remains the same: to align the procedure with insurer criteria for coverage, thereby bridging the gap between medical necessity and financial viability.

Our Medical Insurance: Affordable, Accessible, and Comprehensive

You may want to see also

Explore related products

![]()

Policy Exclusions: Identifying common exclusions for implants in health plans

Health insurance policies often categorize implants as prosthetics, but this classification doesn’t guarantee coverage. Policy exclusions for implants vary widely, leaving patients vulnerable to unexpected out-of-pocket costs. Common exclusions include cosmetic implants (e.g., breast augmentation), experimental procedures, and implants deemed non-medically necessary. For instance, while a dental implant for a missing tooth due to trauma might be covered, one for purely aesthetic reasons likely won’t be. Understanding these exclusions requires scrutinizing policy language, as terms like "medically necessary" are often open to interpretation by insurers.

A critical step in navigating these exclusions is reviewing the policy’s definition of "prosthetic devices." Some plans explicitly exclude implants from this category, treating them as separate entities with stricter coverage criteria. For example, joint replacements may be covered under prosthetics, but cochlear implants might fall under a different category with limited benefits. Additionally, age restrictions can apply; some plans exclude coverage for implants in patients over 65, citing alternative treatment options as more cost-effective. Always cross-reference the policy’s list of covered procedures with its exclusions to identify gaps.

Persuasive arguments for coverage often hinge on demonstrating medical necessity, but insurers frequently counter with cost-saving alternatives. For instance, a patient seeking coverage for a spinal implant might be denied if the insurer deems physical therapy a viable option. To counter this, gather detailed medical documentation, including failed conservative treatments, to strengthen your case. Pre-authorization is another critical tool; submitting a request with supporting evidence can preempt denials, though it doesn’t guarantee approval. Be prepared to appeal, as many exclusions are overturned upon review.

Comparatively, group health plans may offer more lenient exclusions than individual policies, thanks to employer negotiations. However, even these plans often exclude implants related to pre-existing conditions or those not FDA-approved. For example, a cutting-edge retinal implant might be excluded if it lacks long-term efficacy data. Patients with high-deductible plans should also note that meeting the deductible doesn’t ensure coverage if the procedure itself is excluded. Always verify coverage specifics before proceeding, as assumptions can lead to financial strain.

Descriptive examples illustrate the real-world impact of these exclusions. Consider a 45-year-old with severe hearing loss who is denied coverage for a cochlear implant because their plan excludes "hearing devices not classified as prosthetics." Another scenario involves a patient needing a dental implant after an accident, only to discover their plan covers extractions but not replacements. Such cases highlight the need for proactive policy analysis and, if necessary, supplemental insurance tailored to implant coverage. Without diligence, patients risk bearing the full cost of procedures insurers deem excludable.

Aviva Medical Insurance: Is It Worth the Cost?

You may want to see also

Frequently asked questions

Yes, dental implants are typically classified as a prosthesis under health insurance, though coverage varies by policy and provider.

Coverage for implants as a prosthesis depends on the insurance plan; some may cover part of the cost, while others may exclude it entirely.

Breast implants may be considered a prosthesis if they are medically necessary (e.g., post-mastectomy), but cosmetic procedures are often not covered.

No, health insurance policies often differentiate between types of implants (e.g., dental, joint, breast) and their coverage as a prosthesis based on medical necessity.

Yes, you can appeal a denial of coverage for implants as a prosthesis, especially if they are deemed medically necessary by your healthcare provider.