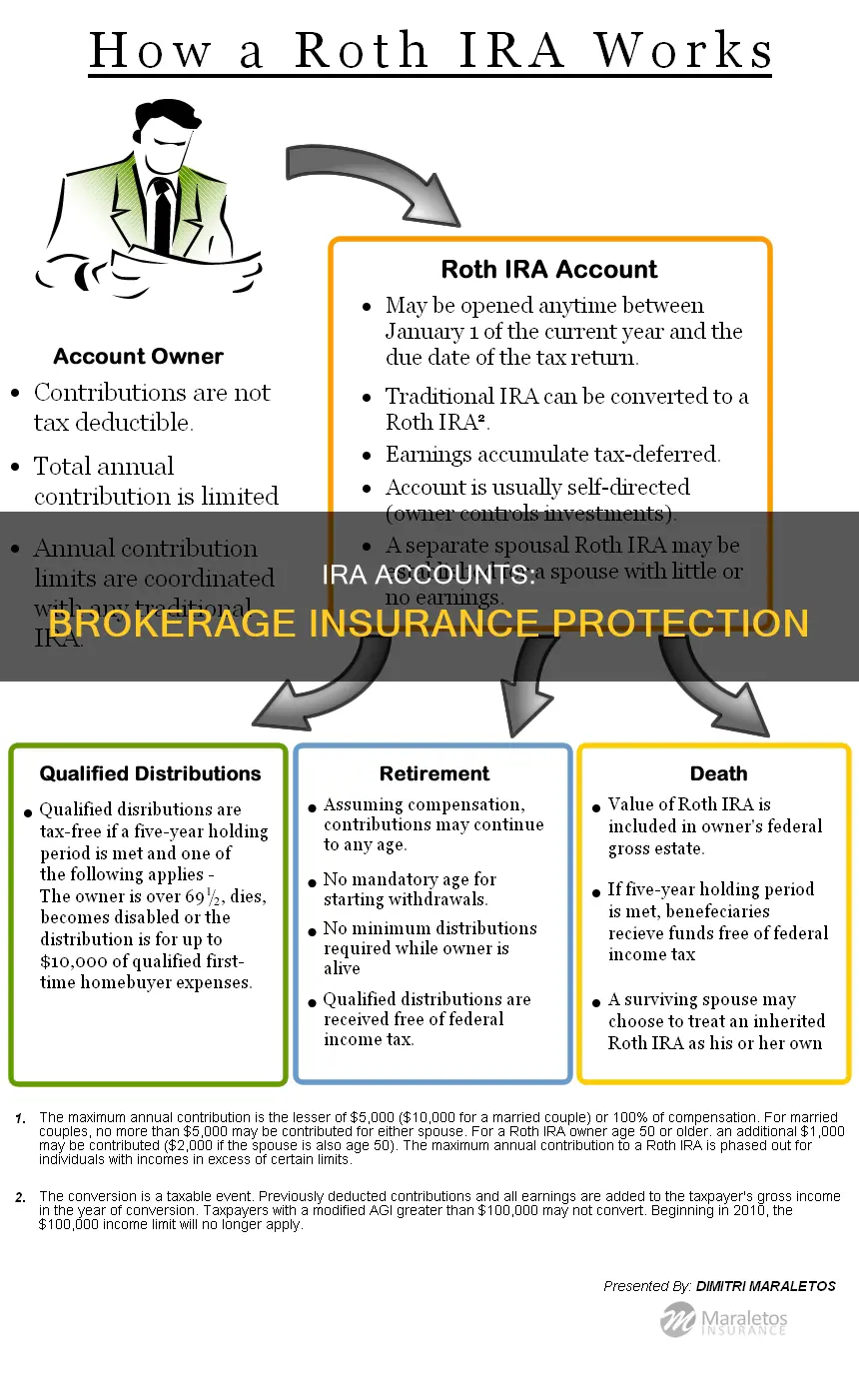

IRAs and brokerage accounts have some similarities, but they also have distinct differences. IRAs are long-term investment vehicles with strict rules around withdrawals and annual contributions, while brokerage accounts offer more flexibility, allowing investors to buy, sell, and trade for short-term or long-term gains. Given these differences, it's important to understand how these accounts are insured. FDIC insurance protects deposits in banks or savings associations, while SIPC insurance covers brokerage accounts. FDIC insurance covers up to $250,000 per depositor, per bank, and per ownership category, while SIPC insurance provides up to $500,000 in coverage, with the potential for more depending on the types of accounts held.

| Characteristics | Values |

|---|---|

| IRA accounts insured by | Securities Investor Protection Corporation (SIPC) or Federal Deposit Insurance Corporation (FDIC) |

| SIPC insurance coverage | Up to $500,000 in securities, including up to $250,000 in cash balances |

| FDIC insurance coverage | Up to $250,000 per depositor, per bank, per ownership category |

| FDIC-insured assets | Checking and savings accounts, money market deposit accounts, certificates of deposit |

| Institutions covered by FDIC | FDIC-insured banks and savings associations |

| Institutions not covered by FDIC | Credit unions, investment companies, brokerages |

| Institutions covered by SIPC | Broker-dealers |

| Institutions not covered by SIPC | Investment banks |

| IRA account minimum deposit | $1,000 |

| Brokerage account minimum deposit | None |

| IRA withdrawals | Strict rules and penalties |

| Brokerage withdrawals | No withdrawal requirements or penalties |

| IRA taxation | Tax-deferred or tax-free |

| Brokerage taxation | Taxable |

Explore related products

What You'll Learn

- FDIC insurance covers IRA accounts held at FDIC-insured banks

- FDIC insurance covers up to \$250,000 per depositor, per bank, and per ownership category

- SIPC insurance covers investors for up to \$500,000 in securities

- Brokerage accounts have no contribution limits, unlike IRAs

- IRAs are long-term investment accounts, while brokerage accounts allow for short-term investments

![]()

FDIC insurance covers IRA accounts held at FDIC-insured banks

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the US government that protects bank depositors against losing their insured deposits in the event of an FDIC-insured bank or savings association failing. FDIC insurance covers customer deposits at FDIC-insured banks, including those held in checking accounts, savings accounts, money market deposit accounts, and certificates of deposit (CDs).

FDIC insurance covers traditional deposit accounts, and depositors do not need to apply for it. Coverage is automatic whenever a deposit account is opened at an FDIC-insured bank or financial institution. The FDIC covers all types of deposits received at an insured bank, including checking accounts, savings accounts, and time deposits such as CDs.

The FDIC covers customer deposits held at FDIC-insured banks or savings and loan associations, including assets held in IRA accounts. The limit on FDIC insurance is $250,000 per depositor, per institution, for each account ownership category. This means that if you have a retirement account such as an IRA, FDIC insurance can cover up to $250,000. For example, if you have a single deposit account and a revocable trust account with one beneficiary at the same FDIC-insured bank, both accounts are covered by FDIC insurance.

It's important to note that not all IRA accounts are treated the same by the FDIC. It depends on their type and the financial institution where they are held. For instance, IRA investments held in mutual funds, exchange-traded funds (ETFs), or individual stocks are not covered by FDIC insurance. In these cases, the individual bears all the risk if the securities lose value, even if the account was established through an FDIC-insured institution.

Progressive Insurance Commercials: Where Are They Filmed?

You may want to see also

Explore related products

![]()

FDIC insurance covers up to \$250,000 per depositor, per bank, and per ownership category

The Federal Deposit Insurance Corporation (FDIC) protects your money in the bank. If an insured bank fails, the FDIC will reimburse its customers for their losses up to each individual’s insurance limit. The limit is $250,000 per depositor, per bank, and per ownership category. This means that if you have a single deposit account and a revocable trust account with one beneficiary at the same FDIC-insured bank, both accounts will be insured up to $250,000. You can also be eligible for $250,000 of coverage for funds held at a specific FDIC-insured bank in a single account, plus $250,000 held at the same bank in a joint account, plus $250,000 held at the same bank in a retirement account such as an IRA, for a total of $750,000 of coverage.

It is important to note that FDIC insurance does not cover all types of accounts. It only covers deposit accounts, such as checking and savings accounts, money market deposit accounts, and certificates of deposit. It does not cover investment accounts, securities, or other speculative financial products such as stocks, bonds, annuities, ETFs, or mutual funds.

If you have an IRA held at a brokerage firm, it may be insured by the Securities Investor Protection Corporation (SIPC) instead of the FDIC. SIPC insurance covers investors for up to $500,000 in securities, of which up to $250,000 can be cash balances. However, there are instances where investors are SIPC-insured for more than $500,000, depending on how the accounts are held. For example, if you have a traditional IRA and a Roth IRA at the same brokerage, they will be insured separately, and you will be insured for up to $1 million for the two accounts.

The Role of FEMA Insurance Adjusters: Navigating Disaster Claims and Recovery

You may want to see also

Explore related products

![]()

SIPC insurance covers investors for up to \$500,000 in securities

The Securities Investor Protection Corporation (SIPC) is a federally mandated, private nonprofit organisation. It was created by federal statute in 1970 as part of the Securities Investor Protection Act (SIPA) to protect investors from brokerages becoming insolvent.

SIPC insurance covers investors for up to $500,000 in securities, with up to $250,000 of this amount allowed to be cash balances. This means that if you have $500,000 in securities and $250,000 in cash, the entire amount may not be covered.

However, there are circumstances in which investors are covered for more than $500,000. This happens when investors have multiple accounts of different types. For example, if you own a traditional IRA and a Roth IRA, SIPC insures those separately, and you will be insured for up to $1 million for the two accounts at a SIPC-member broker-dealer.

It is important to note that SIPC protection is not the same as protection for your cash at a Federal Deposit Insurance Corporation (FDIC)-insured banking institution. SIPC does not protect the value of any security, and investments in the stock market are subject to fluctuations in market value. SIPC steps in when a brokerage firm fails financially and assets are missing from customer accounts.

In contrast, FDIC insurance covers customer deposits held at FDIC-insured banks or savings and loan associations, including assets held in IRA accounts. The limit on FDIC insurance is $250,000 per depositor, per bank, per ownership category.

HVAC Coverage: Commercial Insurance and Replacement

You may want to see also

![]()

Brokerage accounts have no contribution limits, unlike IRAs

Brokerage accounts and IRAs are distinct from each other in several ways. One of the key differences is that, unlike IRAs, brokerage accounts have no contribution limits. This means that there are no restrictions on how much you can invest in a brokerage account, allowing you to readily buy, sell, and trade for short-term or long-term potential gains. On the other hand, IRAs have strict rules around how much you can contribute annually and are typically considered long-term investment vehicles.

For example, in 2025, the annual contribution limit for a Roth IRA is $7,000, or $8,000 if you are aged 50 or older. Additionally, depending on your modified adjusted gross income (MAGI), you may be limited in how much you can contribute to your Roth IRA. In 2025, if you wish to contribute the full amount to a Roth IRA, your income must be less than $150,000 if you file a single tax return or $236,000 if you are married filing jointly.

Brokerage accounts, on the other hand, do not have such income requirements or contribution limits. This flexibility allows you to invest in a diverse range of assets, including stocks, bonds, exchange-traded funds (ETFs), and mutual funds. You can also withdraw funds from a brokerage account at any time without early withdrawal penalties, although you will be taxed on capital gains once you sell a security.

It is important to note that brokerage accounts and IRAs have different tax implications. Brokerage accounts are taxed at nearly all levels, including dividends, capital gains, and interest. On the other hand, IRAs offer tax advantages, with traditional IRAs allowing you to deduct contributions from your taxable income, and Roth IRAs providing tax-free withdrawals in retirement.

In summary, brokerage accounts offer flexibility in terms of contribution limits and investment options, while IRAs have stricter rules and contribution limits but provide tax advantages for long-term retirement savings.

Smart Insurance Savings: Strategies to Cut Costs

You may want to see also

![]()

IRAs are long-term investment accounts, while brokerage accounts allow for short-term investments

IRAs (Individual Retirement Accounts) are long-term investment accounts that carry specific tax benefits and contribution and distribution restrictions. Traditional IRAs and Roth IRAs differ in terms of when you get a tax break. Traditional IRAs offer upfront benefits, as you can generally deduct your contributions from your taxable income, while Roth IRAs provide a tax break after you begin to make withdrawals, typically during retirement. IRAs are subject to strict rules regarding the maximum amount that can be contributed annually and when you can withdraw without penalty. For example, if you're younger than 50 years old, your maximum IRA contribution for 2025 is $7,000. If you're 50 or older, the maximum contribution is $8,000.

Brokerage accounts, on the other hand, allow for short-term investments and withdrawals. They provide investors with more flexibility and freedom than IRAs. There are no contribution limits or withdrawal penalties with brokerage accounts, but they are taxable. Investors must pay taxes on any earnings generated in a brokerage account, including capital gains and dividends. These taxes are levied at different rates depending on how long an investor held an asset before selling it. Profits on assets held for less than a year are considered short-term capital gains and are taxed as ordinary income, while profits on assets held for more than a year are taxed at discounted rates. Brokerage accounts may charge per-transaction fees or sliding-scale commission fees based on trade size.

In terms of insurance, FDIC insurance covers customer deposits held at FDIC-insured banks or savings and loan associations, including assets held in IRA accounts. The FDIC protects against the loss of deposits in an insured bank or savings association that fails. The limit on FDIC insurance is $250,000 per depositor, per bank, per ownership category. SIPC insurance, on the other hand, protects your assets in a brokerage account. SIPC insurance covers investors for up to $500,000 in securities, of which up to $250,000 can be cash balances.

Marketplace Insurance and the Intricacies of Adjusted Gross Income

You may want to see also

Frequently asked questions

IRA accounts held by a brokerage firm may be insured by the Securities Investor Protection Corporation (SIPC). The SIPC is a non-profit corporation that protects customers of SIPC-member broker-dealers if the firm fails financially. The coverage limit is $500,000 in securities, with up to $250,000 in cash balances. However, if you have multiple accounts of different types, such as a traditional IRA and a Roth IRA, each account is insured separately, resulting in a total coverage of up to $1 million.

The Federal Deposit Insurance Corporation (FDIC) protects deposit account owners, while the SIPC protects investment account owners. FDIC insurance covers customer deposits at FDIC-insured banks or savings and loan associations, including assets held in certain IRA accounts, up to $250,000 per depositor, per bank, and per ownership category.

Your IRA account may be FDIC-insured if your bank is FDIC-insured and you hold a deposit account instead of investments. You can confirm if your financial institution is FDIC-insured by searching the FDIC website or contacting your bank directly.

SIPC insurance covers most brokerage firms, as more than 3,200 brokerage firms are SIPC members. It is important to check with your brokerage firm to understand the specifics of their SIPC coverage and any exclusions.