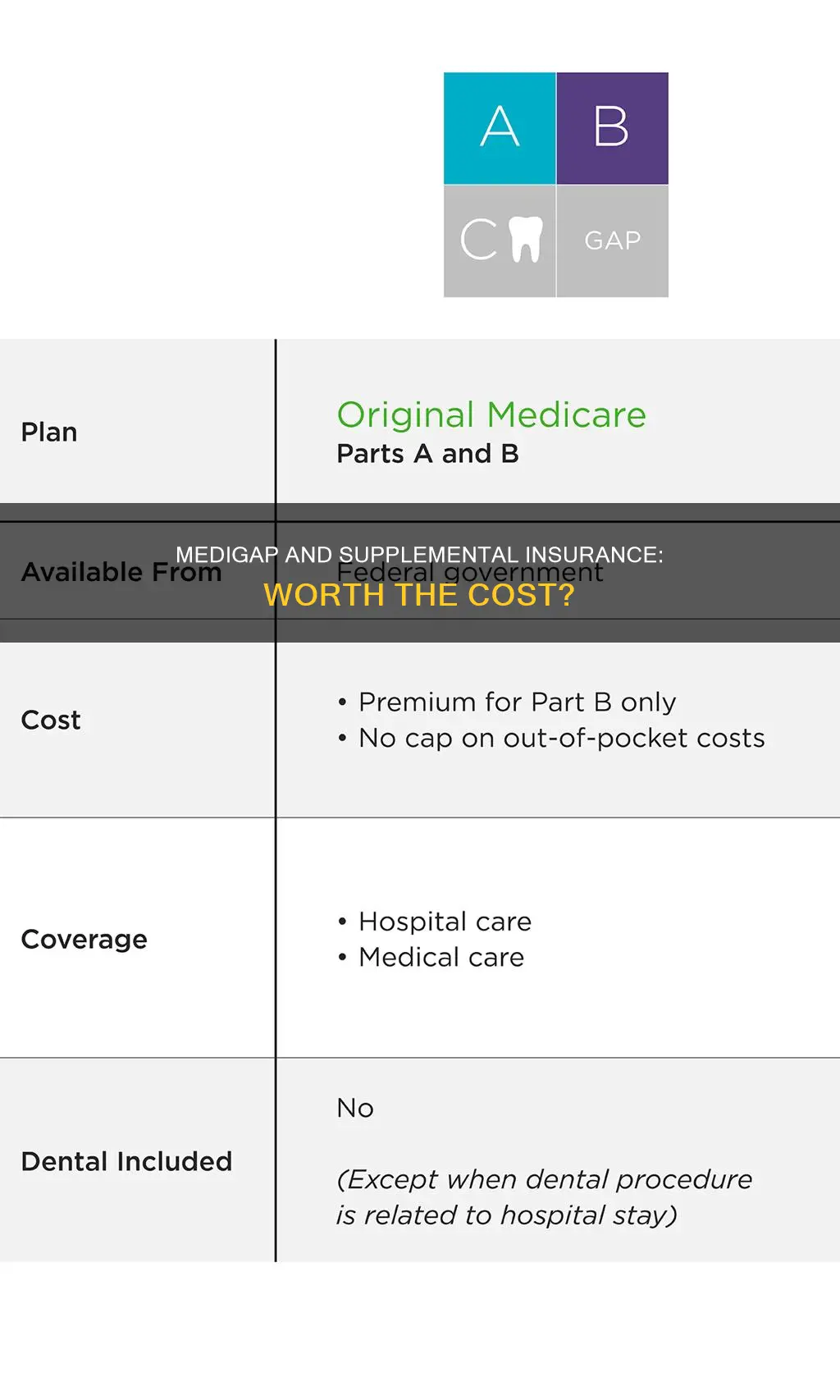

Medicare Supplement Insurance, also known as Medigap, is an optional add-on that can fill gaps in Medicare Part A and Part B. It is extra insurance that can be purchased from a private health insurance company to help pay for out-of-pocket costs that Original Medicare does not cover. Medigap policies are designed to cover expenses such as deductibles, co-pays, and coinsurance, as well as costs associated with emergency care outside the US. While Medigap can provide peace of mind and financial security, it is not for everyone, and the decision to purchase it depends on an individual's financial situation, health, and lifestyle goals.

| Characteristics | Values |

|---|---|

| What is Medigap? | Medicare Supplement Insurance (Medigap) is extra insurance that can be bought from a private health insurance company to help pay out-of-pocket costs in Original Medicare. |

| Who is it for? | People with Medicare Part A and B. |

| What does it cover? | Depending on the level of coverage chosen, Medigap pays some or all of the costs Medicare doesn't cover. Some policies also cover costs related to services not covered by Medicare, including emergency care outside the U.S. |

| How much does it cost? | The cost of Medigap may depend on age, health, gender, marital status, smoking status, and location. |

| When should I buy it? | It is best to buy a Medigap policy when you first enroll in Medicare. |

| Is it worth it? | This depends on your unique financial situation, health, lifestyle goals, and other considerations. Medigap can help safeguard your finances against costly and unexpected out-of-pocket expenses, but it is not mandatory and may not be necessary if you are happy with your current healthcare situation. |

Explore related products

$15.75

What You'll Learn

![]()

Medigap covers out-of-pocket expenses

Medigap, also known as Medicare Supplemental Insurance, is an optional add-on that can fill "gaps" in Medicare Part A and Part B. It is extra insurance that you can buy from a private health insurance company to help pay your share of out-of-pocket costs in Original Medicare. It is important to note that Medigap is not available for people with private Medicare Advantage policies (also known as Medicare Part C).

The cost of Medigap policies varies depending on factors such as age, health, gender, marital status, smoking status, and location. For example, a 65-year-old non-smoking woman in Dallas may pay a monthly premium of $99.30, while a man in Phoenix may pay $532.72. It is worth noting that Medigap premiums can be lower with a Medicare SELECT policy, which requires the use of in-network hospitals and doctors for non-emergency services.

Medigap can provide peace of mind and financial security by safeguarding your finances against costly and unexpected out-of-pocket expenses. It offers more choices and covers a large network of healthcare providers, giving you freedom and flexibility in choosing your doctor. However, it is important to carefully compare plans and weigh the costs before deciding if Medigap is worth it for your unique financial situation, health, and lifestyle goals.

Police Reports: Impacting Your Insurance Claims

You may want to see also

Explore related products

![]()

Medigap offers financial predictability

Medigap, or Medicare Supplement Insurance, is an optional add-on that fills the gaps in Medicare Part A and Part B. It is a form of private insurance that covers out-of-pocket expenses that Original Medicare does not, such as deductibles and co-pays. It also covers costs related to services not covered by Medicare, including emergency care outside the US.

The cost of Medigap policies varies depending on factors such as age, health, gender, marital status, smoking status, and location. It is generally recommended to purchase a Medigap policy when first enrolling in Medicare, as it can be more expensive or difficult to obtain one later on.

While Medigap can provide financial peace of mind, it is not for everyone. It is important to carefully compare plans and weigh the costs before deciding if Medigap is worth the investment for your unique financial situation, health, and lifestyle goals.

Unraveling the Mystery: Are Farmers Insurance Client Relations Managers Commission-Based?

You may want to see also

Explore related products

![]()

Medigap provides nationwide provider access

Medigap, also known as Medicare Supplement Insurance, is extra insurance that can be purchased from a private health insurance company. It helps to cover out-of-pocket costs that Original Medicare (Part A and Part B) does not, such as extensive treatment or long-term hospitalization. Medigap is designed to fill the gaps in Medicare coverage, providing financial predictability and peace of mind for beneficiaries.

One of the key advantages of Medigap is that it provides nationwide provider access. This means that beneficiaries are not restricted to a specific network of doctors and hospitals, as is the case with some other insurance plans. With Medigap, individuals have the freedom to choose their own healthcare providers as long as they accept Medicare. This can be especially beneficial for those who value doctor choice and want to be in charge of their own care, rather than having an insurance company make those decisions.

The ability to choose any provider across the nation can be particularly advantageous in several scenarios. For example, if an individual is travelling or temporarily residing in a different state and requires medical attention, they can easily access healthcare services without worrying about network restrictions. Additionally, if an individual has specific medical needs that require specialized care, they are not limited to seeking treatment within their immediate geographic area and can instead opt for the provider that best suits their needs, regardless of location.

Medigap's nationwide provider access also ensures continuity of care for individuals who split their time between multiple residences or have seasonal residences. They can maintain relationships with healthcare providers in different locations without being constrained by network limitations. This feature of Medigap can provide peace of mind and convenience for individuals who frequently travel or maintain multiple residences.

While Medigap offers nationwide provider access, it is important to remember that it may not be the most cost-effective option for everyone. The premiums for Medigap policies can vary significantly based on factors such as age, health, gender, marital status, smoking status, and location. Therefore, individuals considering Medigap should carefully compare plans and weigh the costs to determine if it aligns with their budget and healthcare needs.

Reporting Insurance Fraud: Massachusetts Guide

You may want to see also

Explore related products

![]()

Medigap premiums vary by company, plan, and location

Medigap, or Medicare Supplement Insurance, is an optional add-on that can fill "gaps" in Medicare Part A and Part B. It is extra insurance that helps pay for out-of-pocket costs in Original Medicare, which can be extensive in the case of Part A's hospital costs and Part B's doctor bills, outpatient care, and medical equipment. Medigap policies are sold by private health insurers and are not available for people with private Medicare Advantage policies (Part C).

- Community-rated (or no-age-rated): With this model, age doesn't affect what you pay; premiums are the same for everyone in your area. A community-rated policy can be a better buy if you first purchase it years after turning 65.

- Issue-age-rated: Premiums are based on your age when you buy the policy. For example, if you buy at a younger age, you will pay lower premiums over time than if you had bought at an older age.

- Attained-age-rated: Premiums increase as you age. This model may be cheaper when you first buy the policy but could become more expensive as you get older.

For example, the American Association for Medicare Supplement Insurance survey of Plan G costs for a non-smoking 65-year-old found monthly premiums in 2023 ranging from $99.30 for a woman in Dallas to $532.72 for a man in Phoenix. Annualized, that’s a range of $1,188 to $6,396.

Medigap premiums can also be affected by whether you are a smoker or a non-smoker, with some insurers offering premium discounts for non-smokers. Additionally, some states offer Medicare SELECT policies, which tend to cost less than other Medigap policies because you must use hospitals and doctors in their networks for non-emergency services.

Understanding No-Fault Insurance: Wage Verification Report

You may want to see also

![]()

Medigap is optional

Medigap is an optional add-on that can fill "gaps" in Medicare Part A and Part B. It is extra insurance that can be purchased from a private health insurance company to help pay for out-of-pocket costs in Original Medicare. Medigap policies are designed to cover the out-of-pocket expenses that Original Medicare doesn't pay, such as Medicare Part A's hospital costs and Part B's doctor bills, outpatient care, and medical equipment. These out-of-pocket costs can be enormous, and Medigap can provide lower out-of-pocket costs and more predictable healthcare expenses.

Medigap is not required, and whether or not it is worth it depends on an individual's financial situation, health, and lifestyle goals. For those with Medicare, about 41% had Medigap in 2022. For the remaining 59%, there are gaps in Medicare that could result in costly expenses. Medigap can help safeguard finances against these unexpected out-of-pocket expenses. However, Medigap premiums can also be expensive, and for some, the supplement prices may be too high. It's important to compare plans and weigh the costs before deciding if Medigap is worth it for your personal situation.

Medigap is typically purchased by those with Original Medicare, as it is not available for people with private Medicare Advantage policies (Medicare Part C). Medicare Advantage replaces all of the basic government coverage with a private insurance plan, so a separate Medigap plan is not needed. Additionally, Medigap only covers one person, so spouses must purchase separate supplemental insurance plans.

Medigap premiums can vary depending on the insurance company, plan, and location. Factors that can affect the cost of Medigap include age, health, gender, marital status, smoking status, and how long someone has been enrolled in Medicare. It is generally recommended to buy a Medigap policy when first enrolling in Medicare and then sticking with it. This is because Medigap policies purchased later may be more expensive or even impossible to get due to medical underwriting.

Title Insurance: Is It Worth the Cost for Homeowners?

You may want to see also

Frequently asked questions

Medicare Supplement Insurance (Medigap) is extra insurance that helps pay your share of out-of-pocket costs in Original Medicare (Parts A and B).

Medigap is worth considering if you want more predictable healthcare expenses and financial security. It's also a good option if you want freedom of choice when it comes to choosing your doctor.

It's best to buy a Medigap policy when you first enroll in Medicare and stick with it. You can buy any Medigap plan during the six-month window that starts when you enroll in Medicare Part B, without the need for a health screening.

The cost of Medigap policies varies depending on the insurance company, your location, age, health, gender, marital status, and whether you smoke. Monthly premiums in 2023 ranged from $99.30 to $532.72 for a 65-year-old non-smoker.