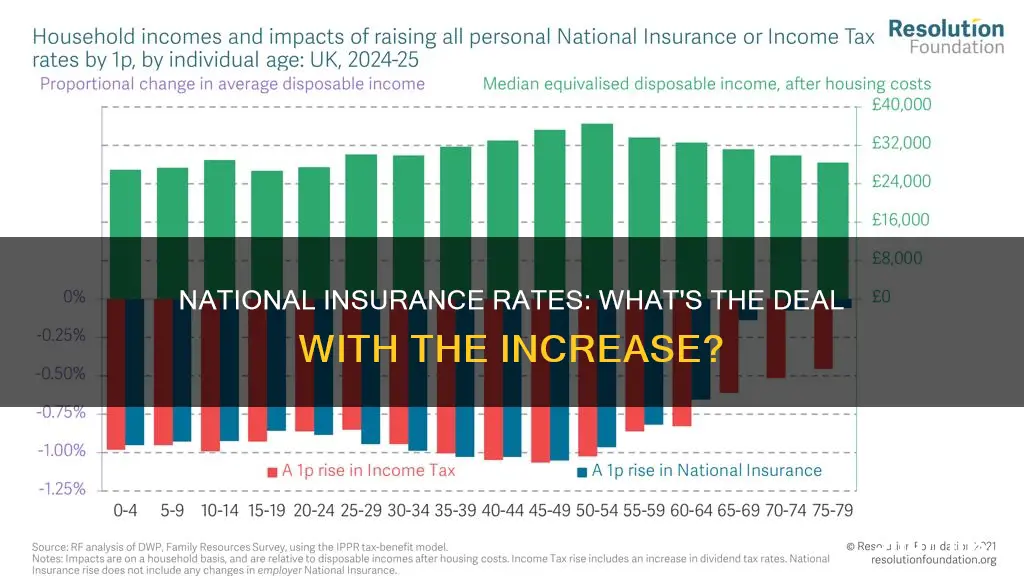

National Insurance (NI) contributions have been subject to several changes in recent years, with rates fluctuating for both employers and employees. While the main rates of NI for workers have remained unchanged, the amount paid by employers increased in April 2025, rising from 13.8% to 15%. This shift has had a significant impact on businesses, particularly small businesses, as they navigate rising costs and changing tax thresholds. The government has stated that these changes are expected to generate an additional £25 billion annually, but the implications for employment and wages remain to be seen.

| Characteristics | Values |

|---|---|

| Date of change | 6 April 2025 |

| Rate of employer’s NI contributions (NICs) | Increased by 1.2 percentage points to 15% |

| Threshold at which employers start paying NICs | Lowered from £9,100 to £5,000 |

| Self-employed Class 4 National Insurance contributions | Decreased from 9% to 6% |

| Self-employed Class 2 National Insurance contributions | Scrapped in April 2024 |

| Starting rate for NI for employees | Decreased twice in 2024: from 12% to 10%, and then to 8% |

| Self-employed Class 4 NI contributions on earnings between £12,570 and £50,270 | Decreased from 9% to 6% |

| NI rate on income and profits above £50,270 | Remains at 2% for all workers |

| Higher rate | 40% on earnings between £50,271 and £125,140 |

| Losing the £12,570 tax-free personal allowance | £1 of personal allowance lost for every £2 that income exceeds £100,000 |

Explore related products

![Manual of Compensation and Liability Insurance ; Rules and Rates. (1916) [Leather Bound]](https://m.media-amazon.com/images/I/61FbOFgXaEL._AC_UY218_.jpg)

What You'll Learn

![]()

National Insurance rates for employers

The rise in employer NICs will affect payroll costs, with firms expected to pass on 60% of the higher costs to workers and consumers through lower real wages and higher prices. To manage these increased costs, businesses can consider introducing or enhancing salary sacrifice schemes, where employees take a lower salary in exchange for pension contributions. This strategy can help reduce NIC bills and provide tax-efficient benefits to employees.

Additionally, the Employment Allowance has increased from £5,000 to £10,500, benefiting small businesses with annual Class 1 NI liabilities of up to £100,000. This allowance can be offset against NIC liability, potentially reducing it to nil.

To remain resilient in the face of rising costs, businesses are encouraged to engage in proactive planning and adopt sound accounting practices. While some businesses may choose to absorb the increased costs, others may explore cost-saving measures, such as zero-based budgeting and data analytics, to identify growth opportunities and maintain profitability.

Overall, the rise in employer NICs is expected to significantly impact businesses, and proactive strategies are necessary to mitigate the financial burden and maintain a competitive edge in the market.

High-Rise Condo Insurance: What's Covered?

You may want to see also

Explore related products

![]()

National Insurance rates for employees

National Insurance contributions have undergone several changes in recent years, with rates fluctuating for both employees and employers. In April 2024, National Insurance contributions were reduced for employees, with the starting rate for 27 million employees dropping twice, first from 12% to 10% and then to 8%. Self-employed individuals also witnessed a decrease in their Class 4 National Insurance contributions, with rates dropping from 9% to 6%. Additionally, self-employed Class 2 National Insurance contributions were completely abolished during the same month.

However, these reductions in National Insurance contributions were followed by an increase in April 2025, primarily impacting employers. The rate of employer National Insurance contributions (NICs) rose from 13.8% to 15%, and the threshold at which employers start paying NICs was lowered from £9,100 to £5,000 per year. This change resulted in more employees being included in the taxable bracket. While the government did not directly increase National Insurance rates for employees, the rise in costs for employers could have indirect effects on employees, potentially leading to lower pay increases or reduced hiring.

The changes in National Insurance contributions are part of the government's tax policies, with the Labour Party pledging to keep rates of National Insurance, income tax, and VAT unchanged for working people. The Chancellor, Rachel Reeves, confirmed this pledge, stating that there would be no increases in workers' National Insurance rates. Instead, the focus has been on adjusting employer contributions and thresholds.

It's important to note that National Insurance contributions are separate from income tax. Income tax rates are different in Scotland, where a new 45% band took effect in April 2024, and the top rate rose from 47% to 48%. Additionally, individuals earning over £100,000 start losing their £12,570 tax-free personal allowance. The additional rate of income tax of 45% applies to all earnings above £125,140 per year in England, Wales, and Northern Ireland.

Malpractice Insurance: Are Lawyers Required to Have It?

You may want to see also

Explore related products

![TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UL320_.jpg)

![]()

National Insurance thresholds

The National Insurance thresholds for the 2025/2026 financial year have been updated, with changes taking effect from 6 April 2025. While the specific figures for the Lower Earnings Limit (LEL) and Upper Earnings Limit (UEL) have not been released, it is known that the UEL for the 2025-2026 tax year is £125,140, which also serves as the upper secondary threshold. The Secondary Threshold, where employers start paying National Insurance contributions for their staff, will be adjusted, with the weekly amount yet to be confirmed.

The Apprentice Upper Secondary Threshold will be introduced, impacting how employers calculate contributions for apprentices. Changes will also be made to the upper secondary thresholds, affecting contributions for various employment categories, including those under 21, apprentices, and veterans.

It is important to note that the government has pledged not to increase taxes for working people, including National Insurance rates. However, employers' National Insurance contributions have increased, rising from 13.8% to 15% from April 2025. Additionally, the threshold at which employers start paying National Insurance has been lowered, resulting in more employees being included in the taxable bracket.

Understanding Insurance Citations: Impact and Implications

You may want to see also

Explore related products

![TurboTax Premier 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71yj6wGqynL._AC_UL320_.jpg)

![]()

National Insurance and inflation

National Insurance contributions have changed significantly in the past year. In April 2024, National Insurance was cut for employees and the self-employed, but in April 2025, rates increased for employers. The rate of employer's National Insurance Contributions (NICs) rose by 1.2% to 15%. This increase, combined with the lowering of the secondary threshold, means that employers now pay NICs on employee earnings from £5,000, instead of the previous £9,100 threshold.

While the government has not directly increased National Insurance rates for workers, many will likely feel the effects. The rise in employer NICs has increased costs for businesses, which could lead to lower pay increases or less hiring. The lowering of the earnings threshold has also made NICs payable for more part-time workers and those on lower incomes.

The changes to NICs have also impacted different types of workers. For example, self-employed Class 4 NICs were cut in April 2024, decreasing from 9% to 6%. At the same time, self-employed Class 2 NICs were eliminated. However, as wages increase and income tax and National Insurance thresholds remain frozen, more people will be pulled into paying tax for the first time or pushed into higher tax bands.

The impact of these changes is also influenced by inflation. While NIC rates for workers have not increased, inflation forecasts indicate that average earners could pay hundreds of pounds more in taxes by 2028. This is because income tax thresholds are not rising with inflation, resulting in fiscal drag. As a result, even with savings from NIC cuts, many workers will end up paying more in taxes.

The Office for National Statistics (ONS) has also addressed insurance industry inflation in correspondence with the Treasury Select Committee. ONS data sources and methods for calculating insurance inflation are publicly available, and they follow a fixed basket approach, comparing like-for-like each month. However, the ONS acknowledges that its inflation measures capture inflationary pressures and adjust for changes in quality.

How Speeding Tickets Impact Your Insurance Rates

You may want to see also

Explore related products

![H&R Block Tax Software Premium 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51tob7UDgCL._AC_UL320_.jpg)

$78.99 $84.99

![TurboTax Business 2024 Tax Software, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71NKT0cDwnL._AC_UL320_.jpg)

![]()

National Insurance and Labour's pledge

National Insurance contributions have undergone several changes in recent years. In April 2024, National Insurance was cut for employees and the self-employed. However, in April 2025, these contributions increased for employers. The rate rose from 13.8% to 15%, and the threshold at which employers start paying National Insurance Contributions (NICs) was lowered from £9,100 to £5,000 per year. These changes have raised questions about Labour's pledge on National Insurance.

Labour's manifesto pledge stated, "Labour will not increase taxes on working people, which is why we will not increase National Insurance, the basic, higher, or additional rates of Income Tax, or VAT." This commitment was reaffirmed by Chancellor Rachel Reeves, who confirmed that Labour would keep its pledge to maintain the rates of National Insurance, Income Tax, and VAT for working people.

However, the interpretation of "working people" has been disputed. Labour has argued that its pledge applied specifically to employees and not employers. This distinction has been challenged, with some arguing that increasing employer NICs does breach Labour's manifesto commitment. The increase in employer NICs has led to concerns about its potential impact on employees, with forecasts suggesting that a portion of these additional costs will be passed on to employees through lower real wages.

Labour's pledge on National Insurance has been a subject of controversy, with different interpretations of the manifesto's wording. While Labour maintains that its commitment applies to employees and not employers, the increase in employer NICs has sparked debates about the scope and clarity of the pledge. The confusion stems from the manifesto's lack of explicit definition of "working people," leaving the interpretation open to debate.

In conclusion, while National Insurance rates for employees have remained unchanged, the increase in employer NICs has brought Labour's pledge into the spotlight. The distinction between employees and employers in the manifesto's wording has fueled discussions about the pledge's fulfillment and its potential impact on workers. Labour's interpretation of the pledge has been a subject of debate, with ongoing discussions about the true nature of their commitment on National Insurance.

Concealed Carry Insurance: Protection for Gun Owners

You may want to see also

Frequently asked questions

Yes, the National Insurance (NI) paid by employers went up by 1.2% from 13.8% to 15% in April 2025.

Yes, National Insurance contributions were cut for both employees and the self-employed in April 2024.

Yes, self-employed Class 4 National Insurance contributions were cut from 9% to 6% in April 2024.

Yes, self-employed Class 2 National Insurance contributions were scrapped entirely in April 2024.

Yes, the starting rate for NI for employees fell twice in 2024: from 12% to 10%, and then again to 8%.

![H&R Block Tax Software Premium & Business 2024 Win with Refund Bonus Offer (Amazon Exclusive) [PC Online code]](https://m.media-amazon.com/images/I/51yZ-hIg8vL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe 2024 Win/Mac with Refund Bonus Offer (Amazon Exclusive) [PC/Mac Online Code]](https://m.media-amazon.com/images/I/512dhP2BIfL._AC_UL320_.jpg)

![TurboTax Deluxe 2024 Tax Software, Federal Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71QcK4dsRbL._AC_UL320_.jpg)