Federally insured credit unions offer a safe place for members to save money. The National Credit Union Share Insurance Fund (NCUSIF) insures deposits of over 135 million account holders in all federal credit unions and most state-chartered credit unions. Each member has at least $250,000 in total coverage for share accounts, and members can calculate their insured funds using the NCUA's Share Insurance Estimator. However, it's important to note that the NCUA does not insure safe deposit boxes or their contents, digital assets, or money invested in stocks, bonds, and certain other investment products, even if offered by federally insured credit unions.

Explore related products

What You'll Learn

![]()

Federally insured credit unions

The NCUA does not insure money invested in stocks, bonds, mutual funds, life insurance policies, annuities, or municipal securities, even if these investment or insurance products are sold at a federally insured credit union. Credit unions often provide these services to their members through third parties, and the investment and insurance products are not insured by the Share Insurance Fund. In addition, the NCUA does not insure safe deposit boxes or their contents, nor does it insure digital assets such as cryptocurrencies.

The NCUA is the government agency that insures deposits at member credit unions and regulates and supervises federal credit unions. It is responsible for managing and closing credit unions that fail, liquidating the institution, and returning funds from accounts to its members. The NCUA also protects consumers and educates the public on consumer protection and financial literacy issues.

Understanding Insurance Indications: What You Need to Know

You may want to see also

Explore related products

![]()

NCUA insurance coverage

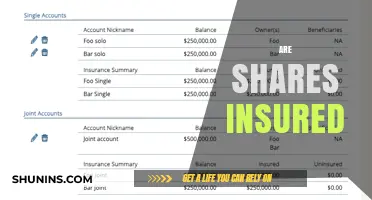

The National Credit Union Administration (NCUA) offers insurance coverage for deposits in federally insured credit unions. This insurance is provided automatically when one joins a federally insured credit union, with individual accounts insured for up to $250,000. The insurance covers various account types, including individual ownership, joint ownership, payable-on-death accounts, living trusts, and IRAs. Additionally, it separately protects retirement accounts, such as IRA and KEOGH accounts, also up to $250,000.

It is important to note that the NCUA does not insure certain investments, such as stocks, bonds, mutual funds, life insurance policies, annuities, or municipal securities, even if these are offered by a federally insured credit union. Safe deposit boxes and their contents, as well as digital assets like cryptocurrencies, are also not insured by the NCUA. Federally insured credit unions must display the official NCUA insurance sign at teller stations and on their websites.

To calculate the amount of insurance coverage, members can use the NCUA's Share Insurance Estimator on MyCreditUnion.gov. This tool works for personal, business, or government accounts. For questions about share insurance coverage, the NCUA provides a phone number (1.800.755.1030, option 1) and an email address ([email protected]).

The NCUA is an independent federal agency established by Congress in 1970 to regulate and supervise federal credit unions. It operates and manages the National Credit Union Share Insurance Fund, which is similar to the deposit insurance coverage provided by the Federal Deposit Insurance Corporation. The fund is backed by the full faith and credit of the United States, ensuring the safety of deposits in federally insured credit unions.

Northwestern Mutual: Drug Testing for Life Insurance Policies

You may want to see also

Explore related products

![]()

NCUA-insured savings limits

The National Credit Union Administration (NCUA) is an independent federal agency established by Congress in 1970 to insure member share accounts at federally insured credit unions. The NCUA manages the National Credit Union Share Insurance Fund, which insures member savings in federally insured credit unions, accounting for about 98% of all credit unions operating in the United States.

The Share Insurance Fund covers deposits in a share draft account, share savings account, or time deposit such as a share certificate. The insurance covers members' accounts at each federally insured credit union, dollar-for-dollar, including principal and any accrued dividends through the date of the insured credit union's closing, up to the insurance limit. This limit is $250,000 per individual depositor, and it applies to Single Ownership Accounts, Joint Ownership Accounts, and certain retirement accounts like IRAs and KEOGH plans. The coverage also extends to non-member deposits when permitted by law.

It is important to note that the NCUA does not insure all types of investments or assets. Money invested in stocks, bonds, mutual funds, life insurance policies, annuities, or municipal securities is not covered, even if these products are sold at a federally insured credit union. Additionally, the NCUA does not insure safe deposit boxes or their contents, and it does not cover digital assets like cryptocurrencies.

To confirm their credit union is federally insured, members can use the NCUA's Credit Union Locator tool. The NCUA also provides a Share Insurance Estimator on its consumer website, MyCreditUnion.gov, to help members calculate their insured funds. All federally insured credit unions must display the official NCUA insurance sign at each teller station and where they accept share deposits or open accounts.

Life Insurance for Word of Life Missionaries Explained

You may want to see also

Explore related products

![]()

Non-insured investments

The FDIC and NCUSIF provide insurance for deposit accounts held in banks and credit unions, respectively, and this insurance coverage is backed by the full faith and credit of the United States government. In the event of a bank failure, depositors with insured accounts are typically compensated and have never lost a penny of insured deposits.

However, not all investments are insured. Non-insured investments include stocks, bonds, mutual funds, annuities, life insurance policies, U.S. Treasury bills, and municipal securities. These investments are often subject to market risk, meaning their value can fluctuate with market conditions, and there is a possibility of losing the principal amount invested.

Another example of a non-insured investment is the contents of a safe deposit box. While the box itself may be protected, its contents are not insured by the FDIC or the credit union. However, separate insurance options may be available for these items, such as fire and theft insurance, which can be added to a homeowner's or tenant's insurance policy.

It is important for investors to understand the risks associated with non-insured investments and to carefully consider their financial goals, risk tolerance, and other factors before purchasing these products. While some non-insured investments may be low risk, such as money market accounts, others may carry a higher risk of losing value.

Borrowing Against Globe Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

State-chartered credit unions

Federally insured credit unions are insured by the National Credit Union Share Insurance Fund (NCUSIF), which is managed by the NCUA. The NCUA is an independent federal agency created by Congress in 1970 to insure member share accounts at federally insured credit unions. The NCUSIF provides up to $250,000 in coverage for each single ownership account and an additional $250,000 for each account holder in jointly owned accounts. Credit union members do not need to apply for share insurance coverage as it is provided automatically when they join a federally insured credit union.

The NCUA regulates and insures federal credit unions, and federal credit unions must display the official NCUA insurance sign at each teller station and where insured deposits are accepted. The NCUA also offers a Share Insurance Estimator on its website, MyCreditUnion.gov, which allows members to calculate the amount of coverage their insured funds have.

While the NCUA does not insure money invested in stocks, bonds, mutual funds, life insurance policies, annuities, or municipal securities, it does protect members against losses if a federally insured credit union fails. No one has lost insured deposits at a federally insured credit union.

BMI: A Life Insurance Risk Factor?

You may want to see also

Frequently asked questions

Yes, savings in federally insured credit unions are insured by the National Credit Union Share Insurance Fund (NCUSIF). The NCUSIF is managed by the NCUA and is backed by the full faith and credit of the United States government. The NCUSIF provides coverage of up to $250,000 per individual depositor.

Some deposits at state-chartered credit unions are insured by private insurers. These private insurers provide non-federal share insurance coverage that is not backed by the US government. You can check if your credit union is federally insured by searching for it on the NCUA's website.

The NCUSIF protects members against losses if a federally insured credit union fails. If a credit union is taken over by another credit union, funds will be transferred to the surviving credit union. If not, the federal government may decide to refund your money in part or in full.

![[2025 Upgraded] Windshield Cover for Ice and Snow [Full Coverage Winter Protection]-Heavy Duty Car Snow Cover, Against Snow, Ice, Frost and Water, Suitable for Cars, SUVs, and Trucks-Large](https://m.media-amazon.com/images/I/81Lm+6nFqHL._AC_UL320_.jpg)