Health insurance is a critical aspect of financial planning, providing individuals and families with protection against high medical costs. One common question many people have is whether health insurance requires monthly payments. The answer is yes; most health insurance plans operate on a monthly premium basis, where policyholders pay a fixed amount each month to maintain their coverage. These premiums vary widely depending on factors such as the type of plan, coverage level, location, age, and health status. Understanding the structure of these payments is essential for budgeting and ensuring continuous access to healthcare services. Additionally, some individuals may qualify for subsidies or assistance programs that reduce their monthly costs, making health insurance more affordable.

| Characteristics | Values |

|---|---|

| Payment Frequency | Monthly payments are the most common for health insurance premiums. |

| Premium Amount | Varies based on plan type, age, location, and coverage level. |

| Plan Types | Individual, family, employer-sponsored, and government-funded plans. |

| Billing Methods | Automatic payments, online portals, checks, or credit/debit cards. |

| Grace Period | Typically 30 days to pay before coverage is canceled. |

| Late Payment Fees | May apply if payment is not made by the due date. |

| Subsidies/Assistance | Available for eligible individuals through ACA marketplaces. |

| Coverage Start Date | Coverage begins after the first premium payment is processed. |

| Cancellation Policy | Coverage can be canceled if premiums are not paid. |

| Annual vs. Monthly | Monthly payments are standard; annual payments may offer discounts. |

| Marketplace Plans | Monthly payments required for plans purchased through healthcare.gov. |

| Employer-Sponsored Plans | Premiums often deducted directly from paychecks monthly. |

| Medicare/Medicaid | Monthly premiums may apply for certain Medicare plans; Medicaid varies. |

| Short-Term Plans | Monthly payments required for temporary coverage. |

| COBRA Coverage | Monthly payments typically higher than employer-sponsored plans. |

Explore related products

What You'll Learn

![]()

Monthly Premiums Explained

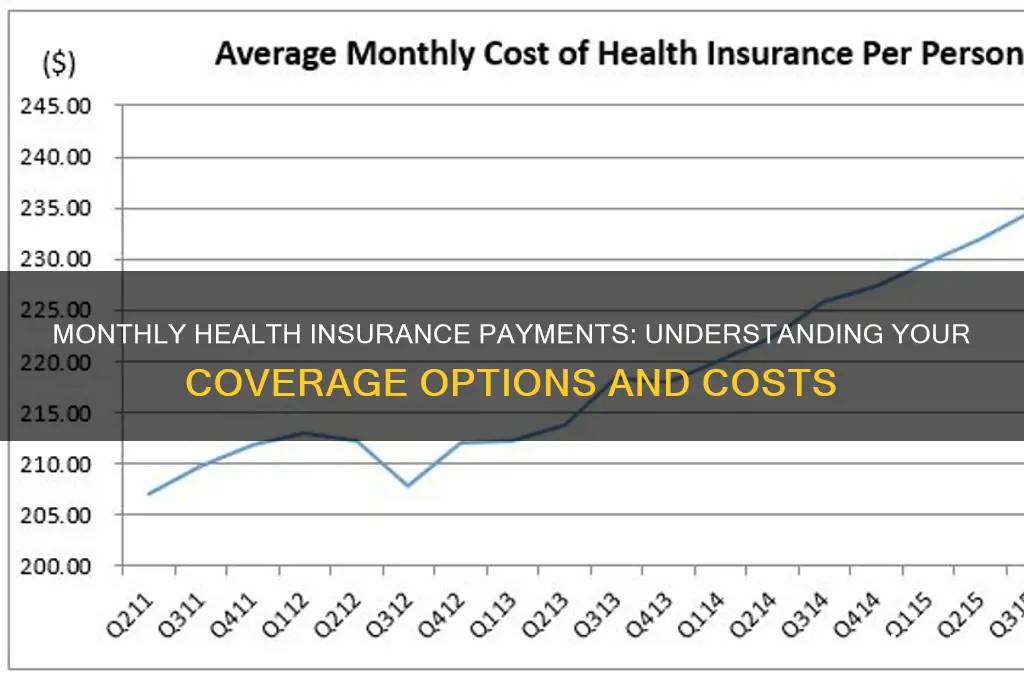

Health insurance often involves monthly payments, known as premiums, which are a fundamental aspect of how coverage is structured. These payments are your ongoing contribution to maintain active insurance, ensuring that you have access to medical services when needed. Premiums vary widely based on factors like age, location, plan type, and provider. For instance, a healthy 30-year-old in a low-cost-of-living area might pay $200–$400 monthly for a mid-tier plan, while a family of four could pay $1,000 or more for comprehensive coverage. Understanding these costs is crucial for budgeting and selecting a plan that aligns with your financial and health needs.

Analyzing premium structures reveals that they are not arbitrary but calculated based on risk and coverage level. Insurers assess factors like your medical history, lifestyle, and the plan’s benefits to determine your rate. For example, a high-deductible health plan (HDHP) typically has lower monthly premiums but higher out-of-pocket costs when you use services, while a low-deductible plan has higher premiums but lower immediate costs for care. Knowing this trade-off helps you decide whether to prioritize lower monthly payments or more predictable expenses when you need care.

To manage monthly premiums effectively, consider these practical tips. First, evaluate your annual healthcare usage—if you rarely visit the doctor, an HDHP paired with a Health Savings Account (HSA) might save you money. Second, take advantage of employer-sponsored plans, which often subsidize premiums, reducing your share of the cost. Third, explore government subsidies through the Affordable Care Act (ACA) marketplace if your income qualifies; these can significantly lower your monthly payments. For example, a single individual earning up to $54,360 annually (as of 2023) may be eligible for premium tax credits.

Comparing monthly premiums across providers and plans is essential but can be overwhelming. Use online tools like Healthcare.gov or insurance comparison platforms to streamline the process. Pay attention to the plan’s metal tier (Bronze, Silver, Gold, Platinum), which indicates the balance between premiums and out-of-pocket costs. For instance, Bronze plans have the lowest premiums but cover only 60% of healthcare costs on average, while Gold plans have higher premiums but cover 80%. Your choice should reflect your anticipated healthcare needs and financial flexibility.

Finally, remember that skipping or delaying premium payments can lead to coverage lapses, leaving you uninsured during critical times. Set up automatic payments or reminders to ensure continuity. If you’re struggling to afford premiums, contact your insurer or a healthcare navigator to explore payment assistance options or alternative plans. Monthly premiums are an investment in your health and financial stability, so treat them as a non-negotiable part of your budget.

Life Insurance Companies and Your Medical History: What's Known?

You may want to see also

Explore related products

![]()

Payment Frequency Options

Health insurance payment frequency isn't one-size-fits-all. Most insurers offer monthly payments as the standard option, providing predictable budgeting and aligning with typical income cycles. This structure is particularly beneficial for individuals and families managing tight finances, as it breaks down the annual cost into manageable chunks. However, monthly payments often come with slight administrative fees, making them slightly more expensive over time compared to less frequent payment options.

For those seeking to minimize costs, annual or semi-annual payments are worth considering. Paying the full year's premium upfront can result in significant savings, as insurers often waive administrative fees or offer discounts for lump-sum payments. This approach requires a larger initial outlay but can be advantageous for those with stable finances and a preference for simplicity. Semi-annual payments strike a balance, reducing fees compared to monthly payments while avoiding the burden of a single large payment.

Quarterly payments are another option, offering a middle ground between monthly and annual frequencies. This structure can be particularly appealing to self-employed individuals or those with fluctuating income, as it spreads costs more evenly throughout the year without requiring a substantial upfront payment. However, like monthly payments, quarterly installments may include administrative fees, though typically lower than those for monthly plans.

Choosing the right payment frequency depends on your financial situation and preferences. If cash flow is a concern, monthly payments provide flexibility and predictability. For those with the means to pay more upfront, annual or semi-annual payments can yield savings. Quarterly payments offer a compromise, balancing cost and convenience. Regardless of the option chosen, it’s essential to review the insurer’s fee structure and discounts to make an informed decision. Always consider how the payment frequency aligns with your budget and long-term financial goals.

Stay Loyal: Why Switching Insurance Companies May Not Be Worth It

You may want to see also

Explore related products

![]()

Cost Factors Affecting Payments

Monthly health insurance premiums are influenced by a complex interplay of factors, each contributing to the final cost you pay. Understanding these variables is crucial for navigating the often-confusing landscape of health insurance pricing.

Age and Health Status: Think of these as the foundation of your premium. Younger, healthier individuals generally pose less risk to insurers, resulting in lower monthly payments. Conversely, older individuals or those with pre-existing conditions may face higher premiums due to the increased likelihood of medical claims. For example, a 25-year-old in good health might pay significantly less than a 55-year-old with diabetes.

Location: Geography plays a surprising role in health insurance costs. Premiums vary widely across states and even within regions due to differences in healthcare costs, provider networks, and state regulations. Urban areas often have higher premiums than rural areas due to the concentration of medical facilities and specialists.

Plan Type and Coverage Level: This is where you have some control. Health insurance plans come in various tiers, typically categorized as Bronze, Silver, Gold, and Platinum. Bronze plans offer the lowest premiums but higher out-of-pocket costs (deductibles, copays, coinsurance), while Platinum plans have the highest premiums but lower out-of-pocket expenses. Choosing a plan with a higher deductible can significantly reduce your monthly payment, but be prepared to pay more upfront if you need medical care.

Network Size and Provider Choice: Plans with larger provider networks, allowing access to a wider range of doctors and hospitals, often come with higher premiums. If you have a preferred doctor or specialist, ensure they are in-network to avoid additional out-of-network charges.

Lifestyle Choices: While not always directly factored into premiums, lifestyle choices can indirectly impact your health insurance costs. Smoking, for instance, is a significant risk factor for various health conditions, potentially leading to higher premiums or exclusions in some cases. Maintaining a healthy weight, exercising regularly, and managing stress can contribute to better overall health, potentially lowering your long-term healthcare costs.

Obamacare: Understanding Your Medical Insurance Options

You may want to see also

Explore related products

$9.97 $19.99

$9.09 $12.99

$8

![]()

Subsidies and Financial Aid

Health insurance premiums can be a significant monthly expense, but subsidies and financial aid programs exist to ease the burden for eligible individuals and families. These programs, often income-based, can substantially reduce your out-of-pocket costs, making health coverage more accessible.

Understanding your eligibility for these programs is crucial. The Affordable Care Act (ACA) marketplaces offer premium tax credits, which directly lower your monthly premium. These credits are calculated based on your household income and the cost of benchmark plans in your area. For example, a family of four earning up to $104,800 in 2023 may qualify for subsidies.

Beyond premium reductions, cost-sharing reductions (CSRs) can further lessen your financial responsibility. CSRs lower deductibles, copayments, and coinsurance for plans purchased through the marketplace. Eligibility for CSRs is tied to income and plan selection, typically benefiting those with incomes below 250% of the federal poverty level.

Additionally, Medicaid and the Children's Health Insurance Program (CHIP) provide comprehensive coverage for low-income individuals and families. Eligibility criteria vary by state, but these programs often cover essential health services with minimal or no monthly premiums.

Navigating these programs can be complex. Utilizing resources like healthcare.gov or consulting with a certified enrollment counselor can help you determine your eligibility and find the most suitable plan. Remember, taking advantage of available subsidies and financial aid can make health insurance significantly more affordable.

Accessing Medication Without Insurance: What Are Your Options?

You may want to see also

Explore related products

![]()

Late Payment Consequences

Missing a health insurance payment can trigger a cascade of consequences, each more problematic than the last. First, expect a late fee. This is a standard penalty, typically a flat rate or a percentage of your missed payment, added directly to your balance. Think of it as a financial slap on the wrist, a reminder that timeliness matters.

Next, your coverage could be suspended. This means you're essentially uninsured during the lapse period. Any medical expenses incurred during this time become your sole responsibility. Imagine a surprise trip to the ER without coverage – a financial nightmare waiting to happen.

The longer the delay, the more severe the repercussions. After a grace period (usually 30-90 days, depending on your provider and state regulations), your policy could be terminated entirely. This leaves you completely uninsured, forcing you to reapply for coverage, potentially facing higher premiums due to a lapse in coverage history.

Think of it like a gym membership – if you stop paying, you lose access. But with health insurance, the stakes are infinitely higher.

To avoid this downward spiral, prioritize timely payments. Set up automatic payments if possible, ensuring consistency. If you foresee difficulty making a payment, contact your insurer immediately. Many companies offer payment plans or temporary adjustments to help you stay covered. Remember, late payments aren't just about fees – they jeopardize your access to essential healthcare.

Stepchildren as Dependents: Health Insurance Eligibility Explained

You may want to see also

Frequently asked questions

Yes, most health insurance plans require monthly payments, also known as premiums, to maintain coverage.

Monthly premiums vary widely based on factors like location, age, plan type, and coverage level, ranging from $50 to $500 or more per person.

No, monthly payments (premiums) are required to keep your health insurance active, though some plans may offer annual payment options.

In some cases, health insurance premiums may be tax-deductible, especially for self-employed individuals or those with certain qualifying expenses. Check with a tax professional for details.