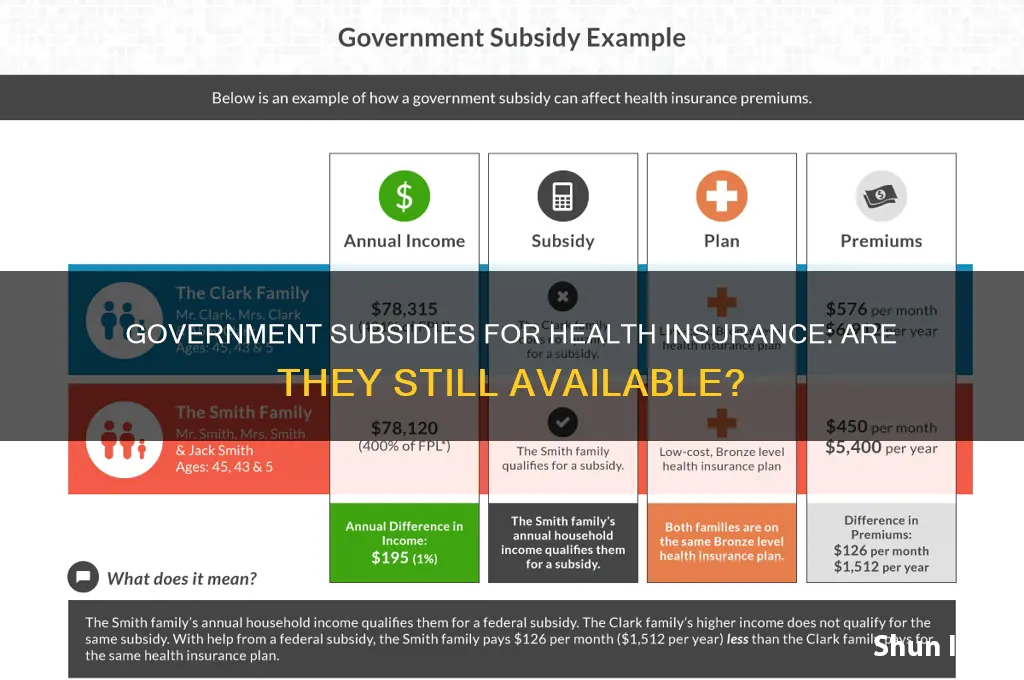

The question of whether government subsidies for health insurance still exist is a pressing concern for many individuals and families navigating the complexities of healthcare costs. In the United States, the Affordable Care Act (ACA) introduced premium tax credits and cost-sharing reductions to make health insurance more affordable for eligible individuals and households with moderate incomes. These subsidies, which are still available, are designed to lower monthly premiums and out-of-pocket expenses for those who purchase coverage through the Health Insurance Marketplace. However, the availability and amount of subsidies depend on factors such as income, household size, and the cost of benchmark plans in a given area. As healthcare policies continue to evolve, it is essential for consumers to stay informed about current subsidy programs and eligibility requirements to maximize their benefits and minimize financial burdens.

| Characteristics | Values |

|---|---|

| Availability of Subsidies | Yes, government subsidies for health insurance are still available. |

| Type of Subsidies | Premium Tax Credits (PTC), Cost-Sharing Reductions (CSR), Medicaid, CHIP. |

| Eligibility Criteria | Based on income level (e.g., 100%-400% of the Federal Poverty Level). |

| Marketplace | Available through Health Insurance Marketplaces (Healthcare.gov). |

| Purpose | Reduce out-of-pocket costs and make health insurance more affordable. |

| Recent Updates (2023) | Enhanced subsidies extended through 2025 under the Inflation Reduction Act. |

| Income-Based Subsidies | Higher subsidies for lower-income individuals and families. |

| State-Specific Programs | Some states offer additional subsidies or expanded Medicaid coverage. |

| Enrollment Period | Annual Open Enrollment Period (typically Nov 1 - Dec 15) or Special Enrollment Periods. |

| Verification Process | Income and household information verified during application. |

| Impact on Premiums | Subsidies significantly lower monthly premiums for eligible individuals. |

| Cost-Sharing Reductions | Reduces deductibles, copayments, and coinsurance for CSR-eligible plans. |

| Medicaid Expansion | Available in most states for individuals below 138% of the FPL. |

| CHIP (Children's Health Insurance Program) | Covers children in families with incomes too high for Medicaid. |

| Tax Implications | Premium Tax Credits can be claimed in advance or at tax filing. |

| Renewal Process | Subsidies must be renewed annually during Open Enrollment. |

Explore related products

What You'll Learn

- ACA Marketplace Subsidies: Eligibility and income limits for premium tax credits

- Medicaid Expansion: State-specific coverage and federal funding availability

- Cost-Sharing Reductions: Subsidies for out-of-pocket costs in ACA plans

- Small Business Subsidies: Tax credits for employers offering health insurance

- State-Specific Programs: Local government subsidies beyond federal assistance

![]()

ACA Marketplace Subsidies: Eligibility and income limits for premium tax credits

The Affordable Care Act (ACA) Marketplace subsidies, specifically premium tax credits, remain a critical tool for making health insurance affordable for millions of Americans. These subsidies are designed to reduce the monthly cost of health insurance premiums for eligible individuals and families who purchase coverage through the ACA Marketplace. Understanding the eligibility criteria and income limits is essential for maximizing these benefits.

Eligibility Criteria

To qualify for premium tax credits, you must meet several key requirements. First, your household income must fall within a specific range, typically between 100% and 400% of the Federal Poverty Level (FPL). For 2023, this translates to an annual income of $13,590 to $54,360 for an individual and $27,750 to $111,000 for a family of four. Second, you must not have access to affordable health insurance through an employer or a government program like Medicare or Medicaid. Lastly, you must be a U.S. citizen or lawfully present in the U.S. and reside in a state where you’re applying for coverage.

Income Limits and Subsidy Calculation

The amount of your premium tax credit is based on a sliding scale tied to your income. For example, if your income is closer to 100% of the FPL, you’ll receive a larger subsidy, significantly reducing your premium costs. Conversely, those earning closer to 400% of the FPL will receive smaller subsidies. The ACA ensures that eligible individuals pay no more than 8.5% of their household income toward the benchmark plan premium. For instance, if the benchmark plan costs $500 per month and your income qualifies you to pay 6% of it, your monthly premium would be $300, with the subsidy covering the remaining $200.

Practical Tips for Maximizing Subsidies

To ensure you receive the maximum subsidy, accurately report your income when applying for coverage. If your income changes during the year, update your information promptly to avoid repaying excess subsidies at tax time. Additionally, consider using the ACA’s subsidy calculator tools available on Healthcare.gov to estimate your eligibility and potential savings. Finally, enroll during the Open Enrollment Period or a Special Enrollment Period if you experience a qualifying life event, such as losing job-based coverage or getting married.

Recent Changes and Extensions

The American Rescue Plan Act of 2021 expanded ACA subsidies, increasing their generosity and removing the income cap for 2021 and 2022. While these expanded subsidies were extended through 2025 under the Inflation Reduction Act, it’s crucial to stay informed about potential future changes. Monitoring updates from the Department of Health and Human Services or consulting a certified navigator can help you navigate these changes effectively.

Takeaway

ACA Marketplace subsidies are a lifeline for many seeking affordable health insurance. By understanding eligibility criteria, income limits, and practical strategies, you can optimize your benefits and ensure access to quality healthcare. Whether you’re a first-time applicant or a returning enrollee, staying informed and proactive is key to maximizing these valuable subsidies.

Aetna Insurance: Accepted at Hershey Medical Center?

You may want to see also

Explore related products

![]()

Medicaid Expansion: State-specific coverage and federal funding availability

Medicaid expansion under the Affordable Care Act (ACA) has been a transformative policy, yet its implementation varies dramatically across states, creating a patchwork of coverage that directly impacts millions of low-income Americans. As of 2023, 40 states and the District of Columbia have adopted Medicaid expansion, extending eligibility to adults earning up to 138% of the federal poverty level (FPL). However, 10 states—primarily in the South—still refuse expansion, leaving approximately 2 million people in the "coverage gap": too poor to qualify for ACA marketplace subsidies but ineligible for Medicaid. This disparity highlights the critical role of state-level decisions in determining access to healthcare.

Federal funding for Medicaid expansion is unusually generous, covering 90% of costs for newly eligible enrollees, with states contributing just 10%. This arrangement was designed to incentivize participation, and it has proven effective in states that have expanded. For example, in Kentucky, expansion reduced the uninsured rate from 14.3% in 2013 to 5.8% in 2016, while also improving access to preventive care and reducing medical debt. Conversely, in non-expansion states like Texas, where nearly 17% of residents remain uninsured, hospitals face higher uncompensated care costs, and residents struggle with limited access to affordable coverage.

States have also introduced unique modifications to their expansion programs, blending federal funding with state-specific priorities. For instance, Arkansas and Indiana implemented work requirements for Medicaid eligibility, though these policies were later struck down by federal courts. Other states, like Michigan and Virginia, have used waivers to include additional benefits, such as dental care or substance use treatment, tailored to their populations' needs. These variations underscore the flexibility of Medicaid expansion while revealing the tension between federal guidelines and state autonomy.

For policymakers and advocates, the lesson is clear: Medicaid expansion is not a one-size-fits-all solution. States must consider their demographic, economic, and political landscapes when designing programs. Practical steps include conducting thorough needs assessments, engaging stakeholders, and leveraging federal funding to maximize impact. For individuals, understanding state-specific eligibility rules is crucial. In expansion states, adults under 65 with incomes up to $18,754 (for an individual) or $38,295 (for a family of four) in 2023 may qualify. In non-expansion states, eligibility remains limited to traditional categories like pregnant women, children, and parents with incomes below 50% of the FPL, leaving many without options.

Ultimately, Medicaid expansion remains a cornerstone of federal efforts to subsidize health insurance, but its success hinges on state participation and innovation. While federal funding provides a strong foundation, the true potential of expansion is realized when states tailor programs to address local needs. For those in non-expansion states, advocacy for policy change remains the most effective path to closing the coverage gap and ensuring equitable access to care.

Exploring Alternative Health Insurance Providers: Top Companies to Consider

You may want to see also

Explore related products

![]()

Cost-Sharing Reductions: Subsidies for out-of-pocket costs in ACA plans

The Affordable Care Act (ACA) includes a lesser-known but crucial subsidy called Cost-Sharing Reductions (CSRs), designed to ease out-of-pocket expenses for eligible enrollees. Unlike premium tax credits, which lower monthly premiums, CSRs directly reduce costs like deductibles, copayments, and coinsurance. These subsidies are available to individuals and families earning between 100% and 250% of the federal poverty level (FPL) who enroll in Silver-level ACA plans. For context, in 2023, 250% of the FPL equates to approximately $34,000 for a single individual and $70,000 for a family of four.

Consider a practical example: A 40-year-old earning $20,000 annually (roughly 160% FPL) enrolls in a Silver plan. Without CSRs, their deductible might be $6,000, making healthcare largely inaccessible until that amount is paid. With CSRs, their deductible drops to around $500, and their copayments for doctor visits and prescriptions are significantly reduced. This transformation makes healthcare not just affordable but usable. To access these benefits, enrollees must apply through HealthCare.gov or their state’s marketplace during open enrollment, ensuring they select a Silver plan to qualify.

While CSRs are still available, their existence has been overshadowed by political and legal challenges. In 2017, federal funding for CSR payments to insurers was halted, leading to higher premiums for Silver plans. However, insurers adapted by "silver loading"—increasing Silver plan premiums to account for the lost funding, which paradoxically made CSRs more valuable for eligible enrollees. Premium tax credits also rose to offset these increases, ensuring that many consumers paid less out-of-pocket overall. This complex interplay highlights the resilience of CSRs as a vital component of the ACA’s safety net.

To maximize CSR benefits, enrollees should carefully compare Silver plans during open enrollment. While all Silver plans offer CSRs to eligible individuals, the specific cost reductions can vary by insurer and region. Additionally, those nearing the upper income limit for CSRs (250% FPL) should consider whether their expected healthcare needs justify staying within the eligibility range. For instance, someone earning slightly above 250% FPL might explore Gold plans, which offer lower out-of-pocket costs without CSRs but come with higher premiums.

In conclusion, Cost-Sharing Reductions remain a cornerstone of the ACA’s effort to make healthcare accessible for low-income individuals and families. By significantly lowering out-of-pocket costs, CSRs ensure that insurance isn’t just a piece of paper but a practical tool for managing health. Despite their under-the-radar status, understanding and leveraging CSRs can make a profound difference in financial and physical well-being. For those eligible, CSRs are not just a subsidy—they’re a lifeline.

Will Insurance Companies Pursue Uninsured Drivers? Legal Insights and Consequences

You may want to see also

Explore related products

![]()

Small Business Subsidies: Tax credits for employers offering health insurance

Small businesses often face unique challenges when it comes to providing health insurance for their employees. Fortunately, the government offers tax credits to alleviate some of this financial burden. The Small Business Health Care Tax Credit, available to qualifying employers, can cover up to 50% of the premiums paid for employee health insurance. To qualify, businesses must have fewer than 25 full-time equivalent employees, pay average annual wages below $56,000 (as of 2023), and contribute at least 50% toward employee premiums. This credit is a powerful incentive for small businesses to offer health insurance, improving employee retention and overall workplace satisfaction.

Analyzing the impact of this subsidy reveals its dual benefits: it supports small businesses financially while promoting access to healthcare for employees. For instance, a business with 10 employees paying $5,000 annually per employee in premiums could receive a tax credit of up to $25,000. This not only reduces the employer’s out-of-pocket costs but also makes health insurance more affordable for workers. However, the credit is non-refundable, meaning it can only offset tax liability, not provide a cash refund. Businesses should consult a tax professional to ensure they maximize this benefit while complying with IRS guidelines.

Persuasively, small business owners should view this tax credit as a strategic investment rather than an administrative burden. Offering health insurance can differentiate a small business in a competitive job market, attracting and retaining talent. Additionally, healthier employees tend to be more productive and take fewer sick days, indirectly boosting the company’s bottom line. While the application process may seem daunting, resources like the IRS’s Small Business Health Care Tax Credit Calculator simplify eligibility determination and estimation of potential savings.

Comparatively, this subsidy stands out from other health insurance incentives, such as those under the Affordable Care Act (ACA), by targeting a specific demographic: small businesses. Unlike individual marketplace subsidies, which are income-based, this tax credit focuses on employer size and contribution. It also contrasts with larger corporate tax breaks, which often favor bigger companies. For small businesses, this credit is a rare opportunity to level the playing field, offering benefits typically associated with larger employers without straining their limited budgets.

Practically, to take advantage of this subsidy, employers should follow a clear set of steps. First, ensure eligibility by verifying employee count, wage thresholds, and contribution levels. Second, choose a qualified health insurance plan through the Small Business Health Options Program (SHOP) Marketplace, as only SHOP plans qualify for the credit. Third, file IRS Form 8941 with your tax return to claim the credit. Finally, maintain detailed records of premiums paid and contributions made, as these will be essential for audit purposes. By proactively leveraging this subsidy, small businesses can provide valuable health benefits while strengthening their financial health.

Understanding AmFirst Health Insurance: Benefits, Coverage, and Enrollment Guide

You may want to see also

Explore related products

![]()

State-Specific Programs: Local government subsidies beyond federal assistance

Beyond federal programs like Medicaid and the Affordable Care Act (ACA) subsidies, states have carved out their own paths to address healthcare affordability. These state-specific initiatives, often tailored to local demographics and needs, demonstrate a commitment to filling gaps left by federal assistance. For instance, California’s Covered California program offers additional subsidies to middle-income earners, reducing premiums for households earning up to 600% of the federal poverty level (FPL). This contrasts with federal ACA subsidies, which cap eligibility at 400% FPL. Such programs highlight how states can innovate to make health insurance more accessible for populations that might otherwise fall into the affordability gap.

Consider New York’s Essential Plan, a state-funded program for individuals earning up to 200% FPL. This plan provides comprehensive coverage with minimal or no premiums, often including vision and dental care—benefits not always covered by federal programs. Similarly, Massachusetts’ Health Safety Net program covers medically necessary services for uninsured residents, regardless of income or immigration status. These examples illustrate how state-specific subsidies can address unique challenges, such as high costs of living or large uninsured populations, in ways that federal programs cannot.

However, navigating these programs requires careful attention to eligibility criteria and application processes, which vary widely. For example, Minnesota’s MinnesotaCare program is available to residents earning up to 200% FPL, but applicants must meet specific work or community engagement requirements. In contrast, Washington’s Cascade Care Savings program focuses on reducing out-of-pocket costs for silver-level plans, benefiting enrollees who frequently use healthcare services. Prospective applicants should research their state’s offerings through official health insurance marketplaces or local health departments to ensure they meet all requirements.

A comparative analysis reveals that while federal subsidies provide a baseline, state programs often offer more targeted relief. For instance, while federal ACA subsidies primarily reduce premiums, state programs like Colorado’s Omnibus Health Bill (HB21-1232) also cap insulin costs at $100 per month, addressing specific affordability crises. This layered approach—federal subsidies plus state-specific aid—can significantly reduce healthcare expenses for vulnerable populations. However, disparities exist; states with more robust programs, like California and New York, tend to have higher tax revenues or political will to prioritize healthcare, leaving residents in other states at a disadvantage.

To maximize benefits, individuals should first determine their eligibility for federal subsidies via Healthcare.gov, then explore state-specific programs. Practical tips include checking for open enrollment periods, which may differ from federal timelines, and leveraging local community health centers for assistance with applications. For example, Oregon’s Health CO-OP program offers reduced premiums for cooperative members, a unique model that combines state subsidies with community-based healthcare delivery. By combining federal and state resources, individuals can create a more comprehensive safety net tailored to their needs.

Vision Exams: Are They Covered by Medical Insurance?

You may want to see also

Frequently asked questions

Yes, government subsidies for health insurance are still available, particularly through the Affordable Care Act (ACA) marketplace. These subsidies, known as Advanced Premium Tax Credits (APTC), help reduce monthly premiums for eligible individuals and families.

Individuals and families with incomes between 100% and 400% of the federal poverty level (FPL) typically qualify for subsidies. However, eligibility can vary based on household size, income, and location.

You can apply for subsidies by enrolling in a health insurance plan through the Health Insurance Marketplace (Healthcare.gov) during the annual Open Enrollment Period or during a Special Enrollment Period if you qualify.

Yes, recent legislation, such as the American Rescue Plan Act (ARPA), expanded subsidies to include more people, reduced costs for many enrollees, and increased the amount of financial assistance available.

Generally, if you have access to affordable employer-sponsored health insurance, you are not eligible for marketplace subsidies. However, if your employer’s plan doesn’t meet affordability or minimum coverage standards, you may qualify for subsidies.