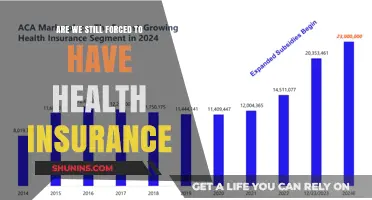

The question of whether individuals are being fined for not having health insurance in relation to their income tax has been a topic of significant interest and confusion, particularly following changes to the Affordable Care Act (ACA). Prior to 2019, the ACA mandated that most Americans maintain health insurance or pay a penalty, known as the individual shared responsibility payment, which was assessed on their federal income tax returns. However, starting in 2019, the federal penalty for not having health insurance was effectively eliminated, as the Tax Cuts and Jobs Act reduced the penalty to $0. While some states have implemented their own health insurance mandates and associated penalties, at the federal level, the absence of health insurance no longer directly impacts income tax liabilities. This shift has raised questions about current enforcement and potential state-level fines, prompting taxpayers to seek clarity on their obligations and the implications for their tax returns.

| Characteristics | Values |

|---|---|

| Penalty for No Health Insurance (2023) | There is currently no federal penalty for not having health insurance in the United States. The individual mandate penalty under the Affordable Care Act (ACA) was eliminated starting in 2019. |

| State-Level Penalties | Some states have implemented their own penalties for not having health insurance. As of 2023, these states include: California, Massachusetts, New Jersey, Rhode Island, and the District of Columbia. Penalties vary by state and are typically assessed on state tax returns. |

| Penalty Calculation (State-Level) | Penalties are usually calculated as a percentage of income or a flat fee, whichever is higher. For example, in California, the penalty is 2.5% of household income or a minimum of $800 per adult and $400 per child, whichever is greater. |

| Exemptions | Individuals may be exempt from state penalties if they meet certain criteria, such as: low income, short coverage gaps (less than 3 months), or qualifying for a hardship exemption. |

| Enforcement | State penalties are enforced through state tax returns. If you owe a penalty, it will be assessed when you file your state taxes. |

| Impact on Federal Taxes | Since there is no federal penalty, not having health insurance does not directly impact your federal income tax return. However, state penalties may still apply, as mentioned earlier. |

| Future Changes | There is ongoing debate about reinstating a federal penalty or making changes to state-level penalties. Stay informed about potential legislative changes that may affect these rules. |

Explore related products

What You'll Learn

- Penalty Amounts: How much is the fine for not having health insurance under income tax laws

- Exemptions: Who is exempt from the health insurance penalty on income tax returns

- Reporting Requirements: How to report health insurance status on your income tax forms

- State vs. Federal: Differences in health insurance fines between state and federal income taxes

- Avoiding Penalties: Strategies to avoid fines for lacking health insurance on your tax return

![]()

Penalty Amounts: How much is the fine for not having health insurance under income tax laws?

The Affordable Care Act (ACA) once mandated a federal penalty for individuals lacking health insurance, but this changed in 2019. The Tax Cuts and Jobs Act eliminated the federal individual mandate penalty, meaning you won’t face a fine on your federal income tax return for being uninsured. However, some states have stepped in to fill the void, imposing their own penalties for residents without coverage. Understanding these state-specific fines is crucial, as they vary widely in structure and amount.

California, for instance, imposes a penalty based on a percentage of your household income or a flat fee per uninsured adult and child, whichever is higher. For 2023, the penalty is 2.5% of your household income above the state’s tax filing threshold or $800 per adult and $400 per child, capped at a family maximum of $2,400. In contrast, New Jersey uses a flat fee approach: $327 per uninsured individual or 2.5% of household income, whichever is greater. These examples highlight the importance of checking your state’s specific rules, as penalties can significantly impact your tax liability.

If you’re unsure whether your state enforces a penalty, consult the official state tax agency website or a tax professional. Some states, like Massachusetts, have had individual mandates long before the ACA and continue to enforce them. Others, like Washington, introduced penalties post-2019. Notably, states with penalties often offer exemptions for financial hardship, religious beliefs, or short coverage gaps, providing relief for those who qualify.

To minimize the risk of penalties, consider enrolling in a health insurance plan during the annual Open Enrollment Period or a Special Enrollment Period if you qualify. For those in states with mandates, exploring subsidized plans through the ACA marketplace can make coverage more affordable. Keeping track of your insurance status throughout the year and documenting any qualifying exemptions can also protect you from unexpected fines during tax season.

Ultimately, while the federal penalty for being uninsured is gone, state-level fines remain a reality for many. Staying informed about your state’s laws and taking proactive steps to maintain coverage or qualify for exemptions can save you from unnecessary financial strain. Ignoring these requirements could turn a manageable tax season into a costly ordeal.

Best Medical Insurance Companies: Your Comprehensive Guide

You may want to see also

Explore related products

![]()

Exemptions: Who is exempt from the health insurance penalty on income tax returns?

The Affordable Care Act (ACA) introduced the individual shared responsibility payment, commonly known as the health insurance penalty, which required most U.S. citizens and residents to have qualifying health coverage or pay a fee on their federal income tax returns. However, not everyone is subject to this penalty. Certain individuals qualify for exemptions, which can be claimed on their tax returns to avoid the fine. Understanding these exemptions is crucial for those who might struggle to afford health insurance or face unique circumstances that make coverage impractical.

One category of exemptions is based on financial hardship. For instance, if the cost of the cheapest available health insurance plan exceeds 8.5% of your household income, you may qualify for a hardship exemption. This calculation is automatically performed when you apply for insurance through the Health Insurance Marketplace, but you can also claim it directly on your tax return. Additionally, individuals with incomes below the tax filing threshold are exempt, as they are not required to file a federal income tax return. This exemption is particularly relevant for low-income earners who might otherwise face a penalty they cannot afford.

Another set of exemptions applies to specific groups of people. Members of federally recognized Native American tribes, for example, are exempt from the penalty. Similarly, individuals who are incarcerated or those with a short coverage gap (less than three consecutive months in a year) may also qualify. Religious conscience exemptions are available for members of recognized religious sects with religious objections to insurance, such as the Amish or certain Mennonite groups. Each of these exemptions requires specific documentation or forms to be filed with your tax return, so it’s essential to gather the necessary proof in advance.

Certain life situations can also trigger exemptions. If you experienced a significant hardship, such as homelessness, eviction, or domestic violence, you might be eligible for a hardship exemption. Similarly, individuals facing substantial medical expenses or those whose insurance plans were canceled and who cannot afford a new one may qualify. To claim these exemptions, you must complete and submit Form 8965 with your tax return, providing details about your circumstances.

Finally, some exemptions are tied to immigration or residency status. Non-citizens who are not legally present in the U.S., such as undocumented immigrants, are exempt from the penalty. Additionally, individuals who live abroad for at least 330 full days within a 12-month period or who qualify as residents of a foreign country under the IRS’s physical presence or bona fide residence tests are also exempt. These exemptions highlight the ACA’s focus on penalizing only those who have access to affordable coverage but choose not to enroll.

In summary, while the health insurance penalty aims to encourage widespread coverage, numerous exemptions protect those facing financial, personal, or circumstantial challenges. By understanding these exemptions and properly documenting your eligibility, you can avoid unnecessary fines and ensure compliance with tax laws. Always consult the IRS guidelines or a tax professional to determine which exemptions apply to your specific situation.

Can Repairable Write-Offs Be Insured? Exploring Insurance Company Policies

You may want to see also

Explore related products

![]()

Reporting Requirements: How to report health insurance status on your income tax forms

The Affordable Care Act (ACA) introduced a shared responsibility payment, often referred to as the individual mandate penalty, for taxpayers who did not maintain minimum essential health coverage. Although this federal penalty was effectively reduced to $0 starting in 2019, some states, such as California, Massachusetts, New Jersey, Rhode Island, and the District of Columbia, have implemented their own health insurance mandates with associated penalties. Understanding how to report your health insurance status on your income tax forms is crucial to avoid fines and comply with state-specific requirements.

Reporting Health Insurance Status: A Step-by-Step Guide

When filing your federal income tax return (Form 1040), you’ll encounter a section asking about your health insurance coverage. For most taxpayers, this involves checking a box indicating whether you had coverage for the entire year. If you had coverage through an employer, the marketplace, Medicaid, or another qualifying plan, you’ll typically receive Form 1095-B (from your insurer) or Form 1095-C (from your employer). These forms provide essential details to verify your coverage. If you purchased insurance through the marketplace, you’ll also receive Form 1095-A, which includes information about any premium tax credits received. Accurately reporting this information ensures compliance and avoids potential audits.

State-Specific Reporting and Penalties

In states with individual mandates, reporting requirements and penalties vary. For example, California requires residents to report their health insurance status on state tax forms (Form 540) and imposes a penalty for non-compliance, calculated as a percentage of household income or a flat fee, whichever is higher. In Massachusetts, residents must complete Schedule HC to report coverage, with penalties assessed per uninsured individual. To avoid fines, familiarize yourself with your state’s rules and ensure your tax forms reflect accurate coverage details.

Practical Tips for Accurate Reporting

Keep all health insurance documents organized, including Forms 1095 and proof of coverage. If you experienced gaps in coverage, note the months without insurance, as some states allow exemptions for short periods (e.g., less than 3 months in California). Use tax software or consult a tax professional to navigate state-specific requirements, especially if you’re subject to penalties. Proactive reporting not only ensures compliance but also helps you take advantage of available exemptions or hardship waivers.

The Takeaway: Compliance Is Key

While the federal penalty for lacking health insurance has been eliminated, state mandates remain a critical consideration. Properly reporting your health insurance status on both federal and state tax forms is essential to avoid fines and legal repercussions. By understanding the reporting process, staying organized, and seeking guidance when needed, you can navigate these requirements with confidence and peace of mind.

Providence Medical Group: Insurance Coverage and Your Options

You may want to see also

Explore related products

![]()

State vs. Federal: Differences in health insurance fines between state and federal income taxes

The Affordable Care Act (ACA) introduced the individual mandate, which required most Americans to have health insurance or pay a penalty. While this federal penalty was eliminated starting in 2019, some states have implemented their own mandates and fines for lacking coverage. Understanding the differences between state and federal approaches to health insurance fines is crucial for taxpayers navigating their obligations.

State Mandates: A Patchwork of Penalties

Several states, including California, Massachusetts, New Jersey, Rhode Island, and the District of Columbia, have enacted their own individual mandates to ensure residents maintain health coverage. These states impose penalties on uninsured individuals through their state income tax returns. For example, California’s penalty for 2023 is calculated as either a flat fee of $800 per adult and $400 per child, or 2.5% of household income above the state’s tax filing threshold, whichever is higher. In contrast, Massachusetts uses a percentage-based approach, fining individuals up to 50% of the lowest-cost monthly premium for a state-approved health plan. These state penalties vary widely, reflecting local priorities and healthcare landscapes.

Federal Approach: The Penalty-Free Era

At the federal level, the ACA’s individual mandate penalty, known as the Shared Responsibility Payment, was reduced to $0 starting in 2019. This means the IRS no longer fines taxpayers for lacking health insurance on their federal returns. However, the federal government still requires taxpayers to report their health insurance status on Form 1040. While there’s no federal penalty, this reporting helps states enforce their own mandates by identifying uninsured residents.

Key Differences: Compliance and Consequences

The primary difference between state and federal fines lies in compliance requirements and financial consequences. Federally, taxpayers face no monetary penalty but must still declare their insurance status. In states with mandates, failure to comply results in tangible fines deducted from state tax refunds or billed separately. For instance, New Jersey’s penalty for 2023 is the greater of $713 per uninsured individual or 2.78% of household income above the filing threshold. Taxpayers in these states must carefully review their coverage to avoid unexpected fines.

Practical Tips for Taxpayers

To navigate these differences, taxpayers should first determine whether their state has an individual mandate. If so, they must ensure they have qualifying health coverage or apply for exemptions, such as those based on income or religious beliefs. For federal returns, accurately reporting insurance status is essential, even though no penalty applies. Using tax software or consulting a professional can help avoid errors and ensure compliance with both state and federal requirements.

The Takeaway

While the federal government no longer fines individuals for lacking health insurance, several states have stepped in to enforce their own mandates. Taxpayers must remain vigilant about their state’s rules to avoid penalties. By understanding these differences and taking proactive steps, individuals can minimize financial surprises during tax season and maintain compliance with applicable laws.

Understanding Aither Health Insurance: Coverage, Benefits, and How It Works

You may want to see also

Explore related products

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UY218_.jpg)

![TurboTax Desktop Deluxe 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71uOJaU7UvL._AC_UY218_.jpg)

![TurboTax Desktop Premier 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71RgxnEm-tL._AC_UY218_.jpg)

![]()

Avoiding Penalties: Strategies to avoid fines for lacking health insurance on your tax return

In the United States, the Affordable Care Act (ACA) introduced the individual mandate, which requires most individuals to have health insurance or pay a penalty. However, since 2019, the federal government has eliminated the penalty for not having health insurance, also known as the "individual shared responsibility payment." Despite this change, some states have implemented their own mandates and penalties for lacking coverage. To avoid fines on your tax return, it's essential to understand these state-specific requirements and take proactive steps to comply.

State-Specific Mandates and Penalties

Several states, including California, Massachusetts, New Jersey, Rhode Island, and the District of Columbia, have enacted their own health insurance mandates. For example, California imposes a penalty of $800 per adult and $400 per child (up to $2,400 per family) for not having qualifying coverage in 2023. To avoid these fines, familiarize yourself with your state’s rules. Check your state’s official tax or health insurance marketplace website for details on coverage requirements and exemptions. If you live in a state with a mandate, ensure you have a qualifying health plan or apply for an exemption if eligible.

Qualifying Health Coverage and Exemptions

To avoid penalties, your health insurance must meet the minimum essential coverage (MEC) standards. This includes employer-sponsored plans, Medicaid, Medicare, and plans purchased through the marketplace. If you cannot afford coverage, you may qualify for an exemption based on income, hardship, or other criteria. For instance, if the cheapest available plan exceeds 8.5% of your household income, you may be exempt from the penalty. Keep detailed records of your attempts to obtain coverage and any exemptions claimed, as these may be required when filing your taxes.

Strategic Planning for Coverage Gaps

If you experience a coverage gap during the year, act quickly to minimize penalties. Short-term health plans, while not MEC, can provide temporary coverage until you enroll in a qualifying plan. Additionally, take advantage of open enrollment periods or special enrollment periods (SEPs) triggered by life events like marriage, job loss, or moving. For example, if you lose employer-sponsored insurance, you have 60 days to enroll in a new plan through the marketplace without facing a penalty. Proactive planning can help bridge gaps and ensure continuous coverage.

Filing Your Taxes Accurately

When filing your tax return, accurately report your health insurance status to avoid unnecessary penalties. Use IRS Form 8965 to claim exemptions if applicable. If you owe a state penalty, ensure you include the correct amount on your state tax return. Consider consulting a tax professional or using reputable tax software to navigate these requirements. Proper documentation and attention to detail can save you from fines and complications. By staying informed and taking targeted actions, you can avoid penalties for lacking health insurance on your tax return.

Understanding CHIP: Medical Insurance for Children

You may want to see also

Frequently asked questions

As of 2019, the federal penalty for not having health insurance (individual mandate) was eliminated. However, some states have their own penalties for lacking coverage, which may affect your state taxes.

The IRS no longer requires proof of health insurance on federal tax returns. However, if you live in a state with a health insurance mandate, the state may require verification.

At the federal level, there is no penalty for not having health insurance. However, check your state’s laws, as some states (e.g., California, Massachusetts) impose fines for lacking coverage.

Not having health insurance will not directly impact your federal tax refund, as the federal penalty no longer exists. However, state penalties, if applicable, may reduce your state refund or increase your state tax liability.

![TurboTax Desktop Home & Business 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71KOcfYElCL._AC_UY218_.jpg)

![H&R Block Tax Software Premium 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51dMIAMHkkL._AC_UY218_.jpg)

![TurboTax Desktop Deluxe 2025, Federal Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71zRbfw0RdL._AC_UY218_.jpg)

![H&R Block Tax Software Deluxe 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51Mlng5FWYL._AC_UY218_.jpg)

![H&R Block Tax Software Premium & Business 2025 Win [PC Online code]](https://m.media-amazon.com/images/I/618kxmZlTGL._AC_UY218_.jpg)

![TurboTax Desktop Business 2025, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71UL+5xLOeL._AC_UY218_.jpg)

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UY218_.jpg)