Health insurance is a vital financial safeguard, protecting individuals from the potentially ruinous costs of medical treatment. Understanding the intricacies of health insurance is essential for newcomers, especially the process of making a claim, which is a formal request by a healthcare provider to an insurance company for payment of medical services provided to a patient. The claim outlines all services and procedures performed, serving as a detailed invoice. This invoice is an informative tool that helps the patient understand their medical expenses and the coverage provided by their insurance plan. While the process of making a claim is important to understand, it is also crucial to know what type of insurance plan one has, as this dictates the level of coverage and the costs that the patient will have to bear. For example, bronze plans usually have the lowest monthly premiums but the highest costs when care is needed, while silver plans fall in the middle, and gold plans offer more comprehensive coverage. Additionally, certain dependents can be added to one's health insurance plan, such as children up to the age of 26, and in some cases, parents. Understanding these nuances of health insurance is key to making informed decisions about one's medical care and financial planning.

| Characteristics | Values |

|---|---|

| What is a health insurance claim? | A formal request by a healthcare provider to an insurance company for payment of medical services provided to a patient. |

| Who can be added as a dependent? | Biological child, stepchild, adopted child, foster child, spouse, parents, and other relatives. |

| What are the requirements for adding a child as a dependent? | The child must have lived with the policyholder for at least six months, be under 26 years old, and not file a joint tax return. |

| Can a medical claim be added to new health insurance? | Yes, but the process and cost depend on the type of claim, such as cashless claims or reimbursements. |

| Can insurance premiums be claimed as tax deductions? | Yes, but only if they are itemized and exceed 7.5% of the adjusted gross income. Self-employed individuals with a net profit for the year can also claim deductions. |

| Can insurers charge different premiums based on health characteristics? | No, since the passage of the Health Insurance Portability and Accountability Act (HIPAA) in 1996 and the Affordable Care Act (ACA) in 2009. |

| Can insurers adjust premiums based on other factors? | Yes, they can adjust premiums based on geographic location, age, family size, and tobacco use. |

Explore related products

What You'll Learn

![]()

Understanding health insurance claims

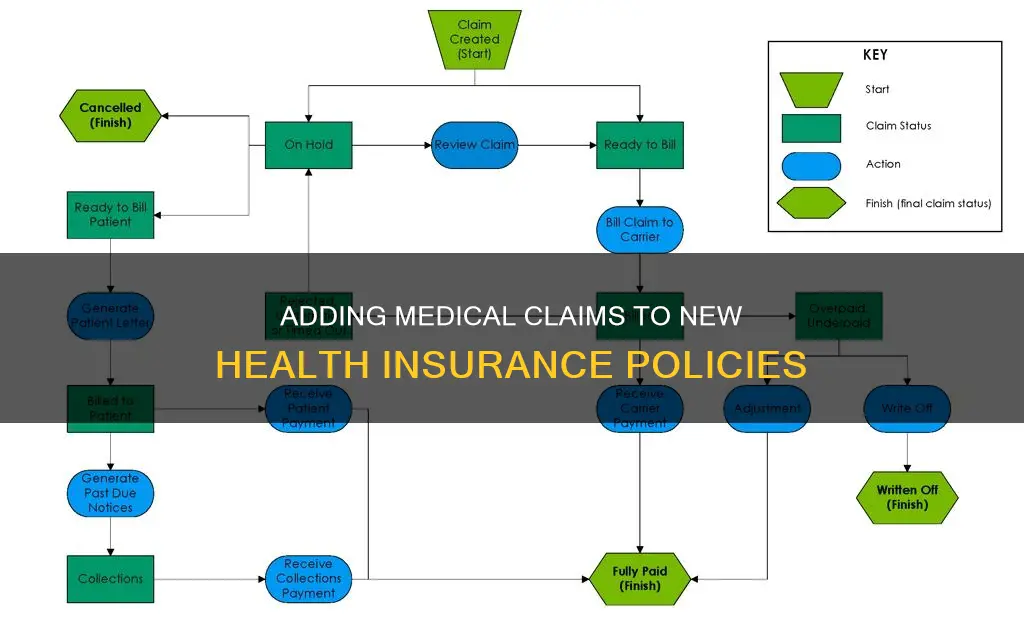

The process typically begins with you or your doctor filing a claim with your insurance provider. If your doctor is part of your insurance plan's network, they will usually file the claim on your behalf. If not, you may have to file the claim yourself. There are two common claim forms: the CMS-1500 and the UB-04. The form you use depends on whether the healthcare facility is institutional (hospitals) or non-institutional (private practices). Once the claim is filed, a claims processor from your insurance provider will review it and verify that the treatments you received are covered by your insurance plan. They may contact you or your healthcare provider for additional information.

The claims processor then decides whether to accept or reject the claim. If the claim is accepted, the insurance provider will reimburse your healthcare provider by paying for some or all of the services. If the claim is rejected, the claims processor will provide a detailed description of why the services are not covered, and you will be billed for the remaining balance. It is important to note that the billing process can be complex, as insurance companies and healthcare providers negotiate prices, and there may be varying levels of coverage depending on your insurance plan.

To file a claim, you will typically need to provide key information such as your insurance policy number, member number, or group plan number. Additionally, you will need to indicate whether the services were received by yourself or a dependent/spouse. It is also advisable to obtain an itemized bill from your medical provider, which lists all the services rendered and their associated costs, including any medications.

Submitting health insurance claims online offers several benefits, including faster processing times. With an online account, you can often access information about the benefits and refunds you are entitled to, as well as any out-of-pocket expenses. You can also track the status of your claim and see if your insurer has received the submitted documents.

Medicaid and Private Insurance: Florida's Dual Coverage Option

You may want to see also

Explore related products

$64.99

$24.79

![]()

Adding parents to your health insurance plan

Adding your parents to your health insurance plan can be a complicated process. The first factor to consider is your parents' age. If they are 65 or older, they are eligible for Medicare, which means they cannot be on your plan. In this case, you can support them financially by paying their premium. If your parents are younger than 65 and low-income, they may qualify for free or low-cost coverage under Medicaid. Eligibility requirements vary by state.

If your parents are not eligible for Medicare or Medicaid, you can check the rules about adding them to your plan. Generally, your parents must be claimed as tax dependents. However, there is no mandate requiring health plans to offer parents coverage, so this will require research. If your health insurance won't allow you to add your parents, you can enroll them in a separate health plan through the Marketplace or Medicare.

It is important to note that the Affordable Care Act (ACA) mandates that children be eligible for coverage under their parents' insurance until the age of 26, but there is no similar protection for parents. Additionally, dependent coverage under a parent's plan may end if the dependent gets married, gains access to employer-sponsored coverage, or turns 26.

Medicaid and Pregnancy: Understanding Coverage with Existing Insurance

You may want to see also

Explore related products

![]()

Adding adult children to your health insurance plan

There are a few things to keep in mind when adding an adult child to your health insurance plan. Firstly, check the specific rules of your insurance policy. While most plans allow adult children as dependents, some may have different age limits or criteria. For instance, if your child is a college student, there might be some caveats to their inclusion. Secondly, be aware of the different categories of health insurance plans, often referred to as "metal levels." These include Bronze, Silver, Gold, and Platinum, and they differ in how the costs are split between the insurer and the insured. Bronze plans, for example, typically have lower monthly premiums but higher costs when you need care and may be suitable for those who generally use few medical services. On the other hand, Silver plans offer moderate premiums and costs and are a good option if you qualify for "cost-sharing reductions."

You can add your adult child to your health insurance plan during the yearly Open Enrollment Period, which usually runs from November 1 to January 15. However, if you've experienced certain life events, such as losing health coverage or having a change in household size, you may qualify for a Special Enrollment Period, allowing you to add your child outside of the regular timeframe. During this special period, you can choose a new plan from the same category as your current one or, in some cases, select a plan from a different category.

It's important to note that once your adult child is added to your plan, they can generally stay on it until they turn 26, even if your own coverage changes. This continuity of coverage provides stability for young adults, ensuring they have access to healthcare regardless of their employment status or health history. However, it's always a good idea to check with the employer or plan, as some states and plans may have different rules regarding dependent coverage.

In conclusion, adding adult children to your health insurance plan can be a straightforward process, providing valuable healthcare coverage for young adults as they navigate the early stages of independence. By understanding the specifics of your insurance policy and the different plan categories, you can make an informed decision to ensure your child receives the best possible coverage during this critical period of their lives.

Medical Travel: Using US Insurance in Mexico

You may want to see also

Explore related products

![]()

Adding other relatives to your health insurance plan

Adding relatives to your health insurance plan is a great way to ensure that your loved ones have access to essential healthcare services. While the specific rules regarding adding dependents to your health insurance plan are determined by your employer or health plan, there are generally accepted guidelines on who can be added. Here is what you need to know about adding other relatives to your health insurance plan:

Spouses

In most cases, you can add your spouse to your health insurance plan. After getting married, you usually have up to 60 days to enroll your spouse as a dependent. It is important to note that if you or your spouse have access to employer-sponsored health insurance but choose to buy your own family plan, you may not qualify for Obamacare subsidies. Additionally, an ex-spouse is usually not eligible for dependent coverage after a divorce.

Children

You can typically add your children to your health insurance plan. A child can be your biological child, stepchild, adopted child, or foster child. In some cases, you can also include grandchildren or other children related to your child. The age limit for children to be covered under your plan is usually 26 years, and they may be required to live with you for at least six months to qualify as your dependent. It is important to note that your child's marital status, school enrolment, or eligibility for employer-based coverage does not affect their eligibility to be added to your plan.

Domestic Partners

Some health insurance plans allow you to add a domestic partner to your plan, especially if you have a child together. You may be required to provide proof of your committed relationship, such as living together for a certain period or having a joint financial account. In some states, civil unions and common-law spouses are also recognized as legal partnerships, allowing them to be added as dependents.

Other Relatives

In certain situations, you may be able to add other relatives, such as siblings, to your health insurance plan if they are financially dependent on you and have lived with you for at least a year. Additionally, if you can claim someone as a dependent on your taxes, they are also considered a dependent on your health insurance plan.

It is important to remember that the specific rules and requirements for adding dependents to your health insurance plan may vary, so be sure to review your plan's guidelines or consult with your employer or a licensed insurance agent to understand the options available to you and your family.

Understanding Pennsylvania's Essential Medical Insurance Coverage

You may want to see also

Explore related products

![]()

The Health Insurance Marketplace® plan categories

Bronze plans typically have lower monthly premiums but higher costs when medical care is needed. These plans are suitable for individuals who generally use few medical services and primarily seek protection from high costs in the event of a serious illness or injury. Silver plans fall in the middle, with moderate monthly premiums and moderate costs when care is required. Silver plans are the only option for individuals who qualify for "cost-sharing reductions" or "extra savings," which can significantly reduce out-of-pocket expenses for deductibles, copayments, and coinsurance. Gold and Platinum plans likely have higher monthly premiums but lower costs when care is required.

When comparing plans within these categories, it's important to consider factors such as the specific benefits offered, the quality of care, and the overall costs. All Marketplace plans must cover the same ten essential health benefits, including preventive services. Some plans may also offer additional benefits, such as vision care or medical management programs for specific needs.

It's worth noting that the Health Insurance Marketplace® operates differently from the traditional insurance market before the Affordable Care Act. Under the Marketplace, individuals can enrol during the yearly Open Enrollment Period or qualify for a Special Enrollment Period due to certain life events, such as losing health coverage, moving, or having a change in household size. When enrolling, it's essential to understand the specific requirements and protections provided under the Affordable Care Act and the Health Insurance Portability and Accountability Act (HIPAA). These laws prohibit discrimination in plan eligibility, premiums, or coverage based on health status, gender, race, or other factors.

Medical Insurance Premiums: Social Security Tax Exemption?

You may want to see also

Frequently asked questions

A health insurance claim is a formal request by a healthcare provider to an insurance company for payment of medical services provided to a patient. It lists all the services and procedures done, serving as a detailed invoice.

Yes, you can add your biological, step, adopted, or foster child to your health insurance plan. Your child must have lived with you for at least six months and their income must be less than half of the cost of their support expenses.

No, your child does not need to be living with you at the time of enrollment, and their marital status and school enrolment status are also irrelevant. They can also be enrolled in your plan even if they are eligible for employer-based coverage.

This depends on the terms of your policy. Your parents must generally be claimed as tax dependents. If your health insurance won't allow you to add your parents, you can enroll them in a separate health plan.