Losing your job-based health insurance can be stressful, but you have multiple options to stay covered. Whether your employer can shut off your medical insurance depends on several factors, including the size of the company, your employment status, and the specific circumstances surrounding the termination of your coverage. If you lose your job-based insurance, you may be able to continue your existing coverage through COBRA, enroll in a new plan through the Affordable Care Act Marketplace, or explore other government-sponsored programs like Medicaid and CHIP. Understanding your rights and options is essential to ensure you maintain access to the healthcare services you need.

| Characteristics | Values |

|---|---|

| Can an employer terminate an employee's health insurance? | Yes, but only if the employer is a small business. Large businesses cannot legally cancel an employee's insurance. |

| What is considered a large business? | A company with more than 50 full-time employees (full-time defined as working more than 30 hours a week). |

| What happens if an employee loses their insurance due to job loss? | The employee can keep their health plan through COBRA for up to 18 months, but it can be expensive. |

| Are there other options for employees who lose their insurance? | Yes, they can shop for insurance through the Marketplace and may qualify for a subsidy or government programs like Medicaid or CHIP. |

| Can an employee cancel their employer-provided insurance? | Yes, but only in specific situations, such as changes in marital status, dependents, employment, or address. |

| Can an employee be punished for taking approved leave? | No, the Family and Medical Leave Act (FMLA) prohibits employers from discriminating or retaliating against employees who take approved leave. |

| Can an employee drop their employer insurance for Medicare? | Yes, but it is recommended to consider the cost and coverage options of both plans before making a decision. |

Explore related products

What You'll Learn

- If your employer drops your insurance, you can keep it for a limited time with COBRA

- If you lose your job, you may qualify for a subsidy to help purchase insurance

- If there is no valid reason for cancelling your insurance, you may have grounds for a lawsuit

- If you are laid off, you can buy your own individual plan

- If you are enrolled in insurance through your employer, large businesses cannot legally cancel your insurance

![]()

If your employer drops your insurance, you can keep it for a limited time with COBRA

If your employer decides to drop your insurance, you are protected by the Consolidated Omnibus Budget Reconciliation Act, or COBRA. This legislation applies to employers with 20 or more employees, but some states have Mini-COBRA laws that extend similar requirements to small businesses. Under COBRA, you can keep your employer-sponsored health insurance for a limited time, usually 18 months, but this can vary from 18 to 36 months. This temporary coverage gives you the flexibility to find other health insurance options.

To be eligible for COBRA, you need to have been a covered employee with insurance coverage at the time your employment ended. You have 60 days to enrol in COBRA once your employer-sponsored benefits end, and your coverage will be retroactive to the date your previous insurance ended. Your former employer is required to give you information about deadlines for enrolment, and you will receive details about the cost of your plan, how to enrol, and where to make premium payments.

It is important to note that COBRA can be expensive, as you may be required to pay the entire group rate premium out of pocket, plus a 2% administrative fee. Therefore, it is recommended to compare the cost of COBRA with other plans available through the Marketplace before deciding on your health insurance. You can shop for insurance through the Marketplace online at healthcare.gov, and you may qualify for a subsidy to help with purchasing insurance, depending on your income.

If your employer drops your insurance, it is essential to act quickly to ensure you have continuous health coverage. Review your options carefully and choose the plan that best suits your needs.

Get Emergency Medical Insurance: Quick, Easy, and Stress-Free

You may want to see also

Explore related products

![]()

If you lose your job, you may qualify for a subsidy to help purchase insurance

If you lose your job, you may be able to keep your job-based health plan through COBRA continuation coverage. COBRA is a law that lets you keep your company's health insurance for a limited time after your job ends, usually for up to 18 months. However, you will likely have to pay the full cost of the premiums yourself as your former employer will no longer be contributing.

If you are unable to afford COBRA coverage, you can enrol in a Marketplace plan within 60 days of losing your job-based coverage. You may qualify for a subsidy to help you purchase insurance, depending on your income. The Marketplace will determine your eligibility for a subsidy based on your estimated income and household information. You can also compare the cost of COBRA with plans available through the Marketplace before deciding on health insurance.

If you are self-employed, retired before becoming eligible for Medicare, or working for a company that doesn't offer health benefits, you may be eligible for premium tax credits or other savings on a Marketplace plan. These savings are based on your estimated income and household information. You can also look into government programs such as Medicaid and the Children's Health Insurance Program (CHIP) which provide free or low-cost coverage to those who qualify.

It is important to note that if you are enrolled in health insurance through your employer and they suddenly stop paying for your plan, you should contact your employer's HR department or your supervisor for answers. Additionally, if you decline your employer's insurance and buy an individual-market plan, you will likely have to pay full price and may not be eligible for a subsidy.

Medical Insurance Group Numbers: Are They Confidential?

You may want to see also

Explore related products

![]()

If there is no valid reason for cancelling your insurance, you may have grounds for a lawsuit

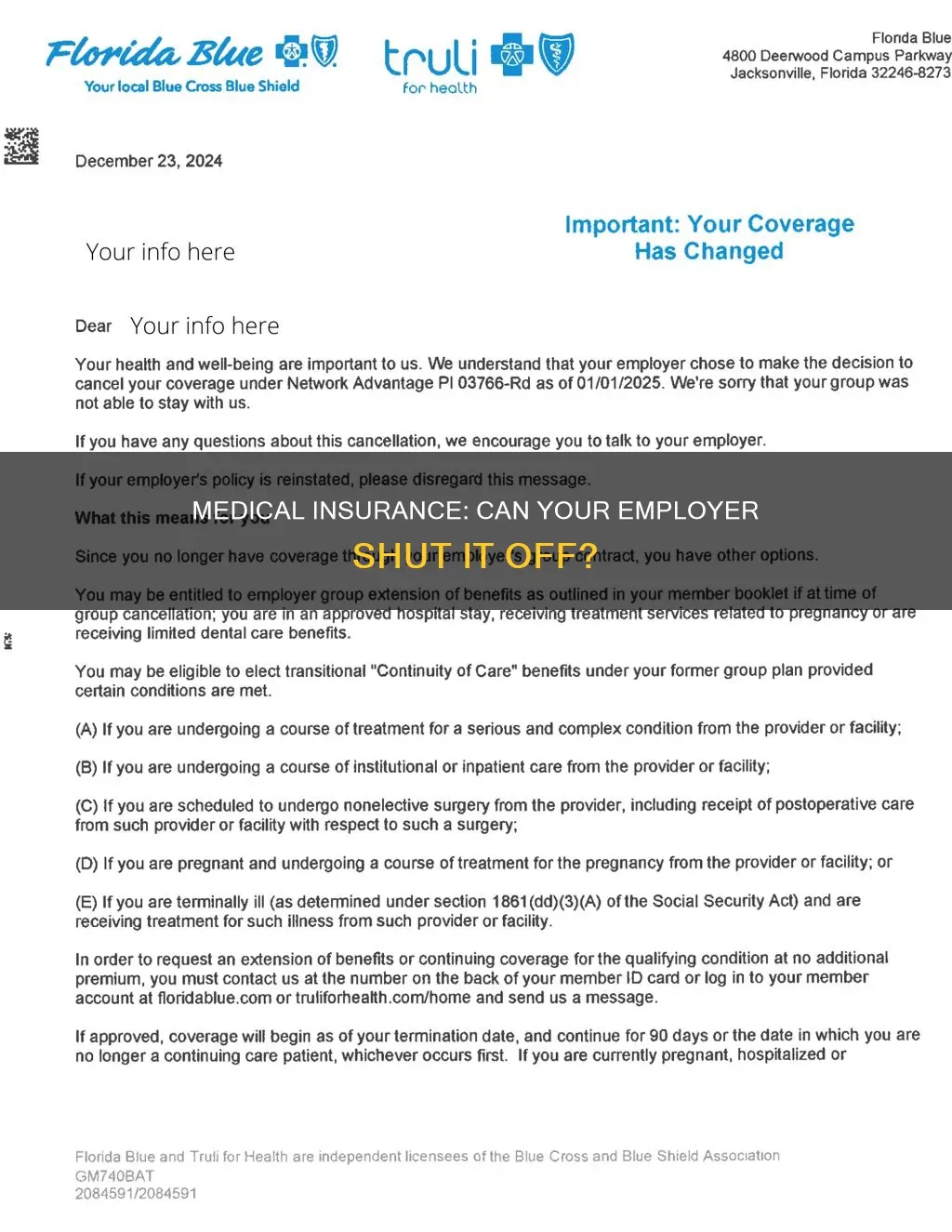

If your employer provides you with health insurance, it is possible for them to cancel it. However, the legality of this depends on several factors, including the size of the company, the reason for cancellation, and the location of the company.

Large employers (those with more than 50 full-time employees) are required to provide health insurance to their employees under the Affordable Care Act (ACA). If your employer is a large business, they cannot legally cancel your insurance without valid reasoning. If there is no valid reason for cancelling your insurance, you may have grounds for a lawsuit. In this case, it is important to contact a lawyer to discuss your options.

Small businesses have more discretion when it comes to providing health insurance. If your employer is a small business, they may be able to cancel your insurance without notice, although the law surrounding this is unclear.

It is important to note that if you are on FMLA leave, your employer is required to maintain your health insurance coverage under the same conditions as if you were still working. Additionally, if you choose not to keep your health insurance during FMLA leave, you have the right to be reinstated to the same coverage levels when you return to work.

If your employer cancels your health insurance, you may be able to continue your coverage through COBRA (Consolidated Omnibus Budget Reconciliation Act) or by purchasing your own individual plan through the Marketplace. COBRA allows you to keep your job-based health insurance for a limited time, usually up to 18 months, after your employment ends. However, you are typically responsible for the full premium and administrative fees, which can be costly. On the other hand, purchasing an individual plan through the Marketplace may provide you with more affordable options, especially if you qualify for subsidies or tax credits based on your income.

Understanding Triterm Medical Insurance: Comprehensive Coverage, Explained

You may want to see also

Explore related products

$14.97 $22.79

![]()

If you are laid off, you can buy your own individual plan

If you are in a state that hasn't expanded Medicaid and your household income for the year is below the poverty line, you can enroll in a subsidized health insurance plan later in the year if you find a job that puts your income above the poverty level. If you cannot afford an ACA-qualified plan, you might consider a short-term health insurance plan. However, these plans are not regulated by the ACA, so they use medical underwriting, don't cover pre-existing conditions, and impose caps on benefits.

If you are enrolled in health insurance benefits through your employer, whether or not your employer can terminate your health insurance depends on the size of the company. Large employers (those with more than 50 full-time employees) are required to provide health insurance to employees under the Affordable Care Act and cannot legally cancel your insurance. Small businesses have more discretion and may be able to cancel your health insurance without notice in some cases, although the law is unclear on this.

If you are covered by your employer's group health plan, you can cancel your coverage at any time if you do not pay your health insurance premiums through payroll deductions on a pre-tax basis. If your premium payments use pre-tax dollars, you can only cancel or change your group coverage in specific situations, such as changes in marital status, dependents, employment, or ZIP code.

If you are laid off, you may be able to continue coverage through your employer-based health plan even after employment ends. Under federal law, employees are eligible for COBRA coverage for up to 18 months after a job loss involving an employer with 20 or more employees. With COBRA, you pay to stay on your job-based health insurance for a limited time, usually 18 months, and you must pay the full premium yourself, plus a small administrative fee. Many states also have "mini-COBRA" rules that allow for the continuation of coverage when an employee works for a smaller business.

How to Add Medical Services to Your New Insurance

You may want to see also

Explore related products

![[8 Pack 4" x 5 Yards] Beige-Self Adhesive Cohesive Bandage Wrap, Self Adherant Non-Woven Wrap Rolls, Atheletic Tape for Wrist, Ankle, Hand, Leg, Premium-Grade Medical Stretch Wrap](https://m.media-amazon.com/images/I/81wGnSXRl8L._AC_UL320_.jpg)

![]()

If you are enrolled in insurance through your employer, large businesses cannot legally cancel your insurance

If you are enrolled in an insurance plan through your employer, it is important to understand the terms and conditions of your coverage, including any changes that may occur. While employees generally wonder if their employers can terminate their health insurance, it is essential to know that this depends on the size of the company.

Large employers, typically those with more than 50 full-time employees, are mandated by the Affordable Care Act (ACA) to provide health insurance to their employees. This means that if you are enrolled in insurance through your employer, and the company is classified as a large business, they cannot legally cancel your insurance without providing a valid reason. This applies regardless of whether they choose to provide notice or not.

On the other hand, small businesses have more discretion when it comes to providing health insurance. The law is somewhat ambiguous regarding the legality of small businesses cancelling employee health insurance. If your employer is a small business and decides to discontinue your health insurance, they may be able to do so without any legal repercussions, although the situation may vary depending on the specific circumstances and local state laws.

It is worth noting that employees do have some control over their insurance plans. For instance, if you are paying for your group coverage with pre-tax dollars, the IRS considers it a cafeteria plan, which can only be changed or cancelled under specific circumstances, such as changes in marital status, dependents, employment, or ZIP code. Additionally, if your employer suddenly stops paying for your health insurance plan, it is recommended to contact the HR department or your supervisor to address the issue.

The Best Time to Sign Up for Medical Insurance

You may want to see also

Frequently asked questions

If your employer is a large business, they cannot legally cancel your insurance with or without notice. Large businesses are defined as those with more than 50 full-time employees (those working over 30 hours per week). Small businesses have more discretion and may be able to cancel your insurance without notice in some cases.

Contact your employer's HR department or your supervisor to get answers. You can also call a toll-free number to get your questions answered or seek face-to-face help in your area.

You can shop for insurance online through the Marketplace. You will qualify for a special enrollment period and may also qualify for a subsidy depending on your income. You can also look into government programs such as Medicaid and CHIP.

Yes, you can keep your health plan through COBRA continuation coverage. You will have to pay the full premium yourself, plus a small administrative fee. This can be expensive, but it will ensure you have continued coverage for up to 18 months.