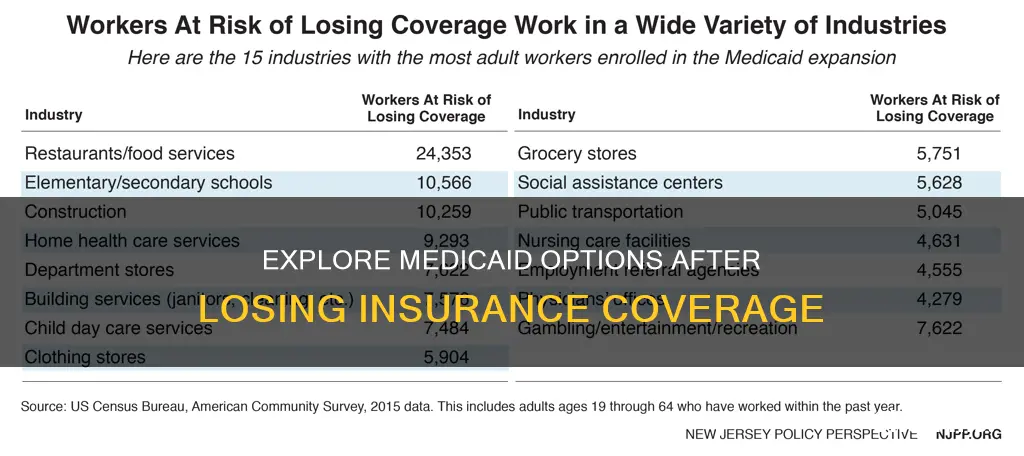

Millions of Americans are set to lose their Medicaid coverage in the coming months, as states start cutting people from government-funded plans when they no longer qualify based on income. This will push many into the unfamiliar territory of the health insurance marketplace. While all states have insurance markets where people who lose Medicaid can buy new coverage with help from subsidies, shopping for affordable insurance that covers regular doctors and prescriptions can be daunting.

| Characteristics | Values |

|---|---|

| Number of people covered by Medicaid | Nearly 85 million |

| Focus of Medicaid | People with low incomes |

| Coverage losses | Regular doctors or important medicines |

| Time to find a new plan | 60 days |

| Individual insurance | More care choices |

| Medicaid coverage | Ends for millions of Americans in the coming months |

Explore related products

What You'll Learn

![]()

Job-based insurance loss

If you lose your job-based health insurance, you may qualify for a "Special Enrollment Period" and can follow the prompts at HealthCare.gov. You may need to provide proof of your loss of coverage.

You can also sign up for Medicaid at any time. If your entire household qualifies for Medicaid, the fastest way to get coverage is likely to start at the state Medicaid agency's website. You will be asked for eligibility information, including your social security number and current monthly income. Many people will need to provide proof of their address and their current monthly income, so it may be helpful to gather documents like a utility bill and a notice about unemployment insurance benefits.

Medicaid is usually free or requires only a nominal premium. A single person with a monthly income below $1467 or a family of four with a monthly income below $3013 will qualify. In most states, people with low incomes can qualify for Medicaid. In 37 states, Medicaid is available to anyone with income below 138% of the Federal Poverty Level ($17,609 per year for an individual, $36,156 per year for a family of four).

If you are unable to afford an ACA-qualified plan while you are between jobs, you might consider a short-term health insurance plan. These plans are less expensive than an ACA-qualified plan, but they are not regulated by the ACA, so they use medical underwriting, don't cover pre-existing conditions, impose caps on benefits, and don't have to cover preventive care.

If you start working again, your Medicaid coverage can continue, even if your earnings become too high to receive SSI. Under the Continued Medicaid Eligibility Work Incentive, you may qualify for continued Medicaid coverage when your SSI payments stop if you meet certain requirements. Each state has a different threshold amount, including different amounts for people who are blind.

Chiropractor Visits: Understanding Medical Insurance Coverage

You may want to see also

Explore related products

![]()

Income and eligibility

Medicaid is a health care program that provides coverage for Americans with low incomes. The Affordable Care Act of 2010 expanded Medicaid to cover nearly all low-income Americans under the age of 65. This act established a new methodology for determining eligibility, based on Modified Adjusted Gross Income (MAGI). MAGI considers an individual's taxable income and tax filing relationships to determine financial eligibility. It is important to note that MAGI-based income counting rules do not apply to individuals whose eligibility is based on blindness, disability, or age (65 and older).

To be eligible for Medicaid, individuals must meet certain non-financial criteria as well. They must be residents of the state in which they are receiving Medicaid and be either citizens of the United States or certain qualified non-citizens, such as lawful permanent residents. Additionally, some eligibility groups are limited by age, pregnancy, or parenting status. For example, young adults who meet the eligibility requirements as former foster care recipients are eligible at any income level.

While income is a significant factor in determining eligibility, it is not the only criterion. There may be asset limits and level of care requirements, and these specifics vary by state. For instance, North Carolina has expanded its Medicaid coverage to include individuals aged 19-64, and individuals in Medicaid-funded nursing homes are generally permitted to have a monthly income of up to $2,901 in 2025.

The best way to determine eligibility is to apply, and there are resources available to help individuals navigate the process, such as the NC Navigator Consortium, which provides free advice and assistance with applications.

Navigating Insurance Appeals: Can You Challenge an Appeal Decision?

You may want to see also

Explore related products

![]()

Work requirements

Losing your insurance can be scary, but there are options to ensure you remain covered. One option is Medicaid, a joint state and federal health insurance program for people with low incomes.

Medicaid work requirements are not new. During the Trump administration, state Medicaid agencies were encouraged to test work requirements, with the Centers for Medicare and Medicaid Services (CMS) approving 11 state proposals for implementing waiver-based demonstration programs between 2017 and 2021. However, most of these proposals were never implemented due to legal challenges and the economic disruption caused by the COVID-19 pandemic.

The primary objective of Medicaid is to provide health coverage to people with low incomes. Traditionally, eligibility for Medicaid has been based on income, but work requirements add a new condition, making coverage contingent on working, volunteering, or engaging in educational activities for a minimum number of hours. Most proposals require working-age beneficiaries (ages 18 to 64) to prove they are working or engaging in other approved activities for 80 hours a month.

While work requirements may encourage people to improve their financial situation, they can also be overly burdensome, leading to people losing their much-needed healthcare coverage. This can result in increased medical debt and untreated medical conditions and higher costs for the state through emergency room visits and interactions with the judicial and behavioral health systems.

Some groups are exempt from work requirements, including people with disabilities, pregnant women, those deemed medically frail, and caregivers for young children or family members with disabilities. It is important to note that the majority of adult Medicaid beneficiaries who can work already do, with 71% being in school or working full or part-time as of 2023.

As of January 2025, only two states, Arkansas and Texas, have implemented Medicaid work requirements. However, if Congress adopts nationwide work requirements, millions could lose their Medicaid coverage, primarily due to confusion over the new reporting requirements.

Insurance Options at Valley Medical: What You Need to Know

You may want to see also

Explore related products

![]()

Loss due to fraud

Medicaid is an insurance program that provides free or low-cost health coverage to some low-income people, families and children, pregnant women, the elderly, and people with disabilities. Many states have expanded their Medicaid programs to cover all people below certain income levels.

If you lose your insurance due to fraud, it is important to understand the implications and your options for maintaining health coverage. Here are some key points to consider:

Impact of Fraud on Eligibility:

Medicaid eligibility is typically determined by factors such as income, assets, household size, and specific state criteria. If you have engaged in fraudulent activities, such as misreporting income or assets, your eligibility for Medicaid may be compromised. It is crucial to provide accurate and honest information to avoid disqualification due to fraud.

Reporting Fraud:

If you become aware of Medicaid fraud, whether by medical professionals, healthcare facilities, patients, or other parties, it is important to report it to the appropriate authorities. All states have Medicaid Fraud Control Units (MFCUs) responsible for investigating and addressing potential fraud. Reporting fraud helps protect the integrity of the Medicaid program and ensures that funds are used appropriately to support those in need.

Reapplying for Medicaid:

If your Medicaid coverage is terminated due to fraud, you may have the option to reapply for Medicaid at a later date. Each state has its own guidelines for reapplying, and it is essential to understand the specific requirements and waiting periods that may apply. Contact your state's Medicaid agency to inquire about the reapplication process and provide any necessary documentation to support your case.

Exploring Alternative Coverage Options:

While you may not be eligible for Medicaid due to the circumstances of your coverage loss, alternative coverage options are available. You can explore the Health Insurance Marketplace to shop for and enroll in health insurance plans. The Marketplace offers a range of plans, including those that may be more affordable or suitable for your needs. Additionally, if you have children, they may still be eligible for the Children's Health Insurance Program (CHIP), which covers children in families with higher household incomes than those eligible for Medicaid.

Preventing Fraud:

It is essential to provide accurate information and follow the guidelines to maintain your eligibility and avoid fraudulent activities. Understand the consequences of fraud and be cautious when providing personal information to prevent identity theft and unauthorized use of your Medicaid benefits.

Insurance Options at Advocate Medical Group: What You Need to Know

You may want to see also

Explore related products

![]()

State-specific schemes

While Medicaid is a federal program, it is administered by states, and each state has its own rules and benefits. This means that eligibility and coverage vary across the country.

In addition, each state has its own income eligibility limits for adults and children. For example, North Carolina has its own expansion group for Medicaid, which includes 100% of the Federal Poverty Level (FPL) for a family of three and an individual.

It is important to note that while all states offer insurance markets where people who lose Medicaid can buy new coverage with subsidies, the specific plans and subsidies available can vary significantly from state to state. This means that the process of shopping for new insurance after losing Medicaid coverage may be quite different depending on where you live.

To summarize, while Medicaid is a federal program, state-specific schemes play a crucial role in determining eligibility, coverage, and the transition process for individuals who lose their Medicaid coverage.

Understanding PPO: A Guide to Preferred Provider Organizations

You may want to see also

Frequently asked questions

Losing Medicaid coverage can be daunting, especially when it comes to finding new insurance that covers your regular doctors and prescriptions. However, all states have insurance markets where people who lose Medicaid can buy new coverage with help from subsidies. You will have 60 days to find a new plan once you register to shop in the insurance marketplace.

It is recommended that you start shopping for new insurance before your Medicaid coverage ends. This gives you plenty of time to sort through the various options available. It is also a good idea to seek assistance, especially if you need help figuring out your income for the coming year, as this is needed to calculate subsidies.

Individual insurance can give people more care choices. Many doctors do not accept Medicaid, and states may pay for only a limited amount of prescriptions.